October Market Update

September represented a notable transformation in Bay Area availability patterns, with most regions recording annual reductions for the initial time in months, propelled by enhanced transaction pace rather than new listing expansion.

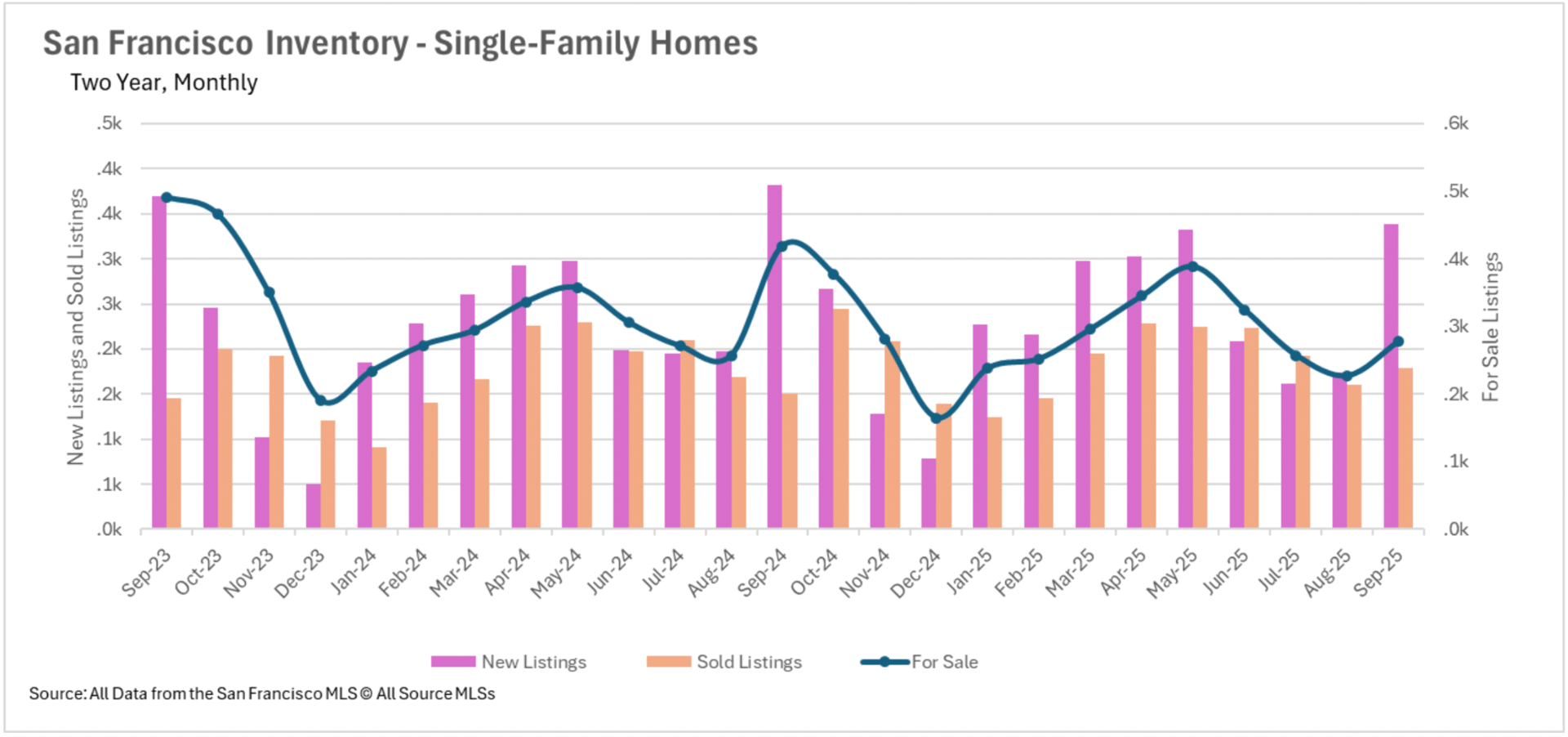

San Francisco distinguishes itself with substantial availability contractions exceeding 30% and accelerating single-family property values, while other regions demonstrate more moderate value fluctuations within established ranges.

Transaction momentum continues intensifying throughout most Bay Area regions, with properties transacting more rapidly despite percentage advances in marketing duration, as absolute figures remain exceptionally minimal.

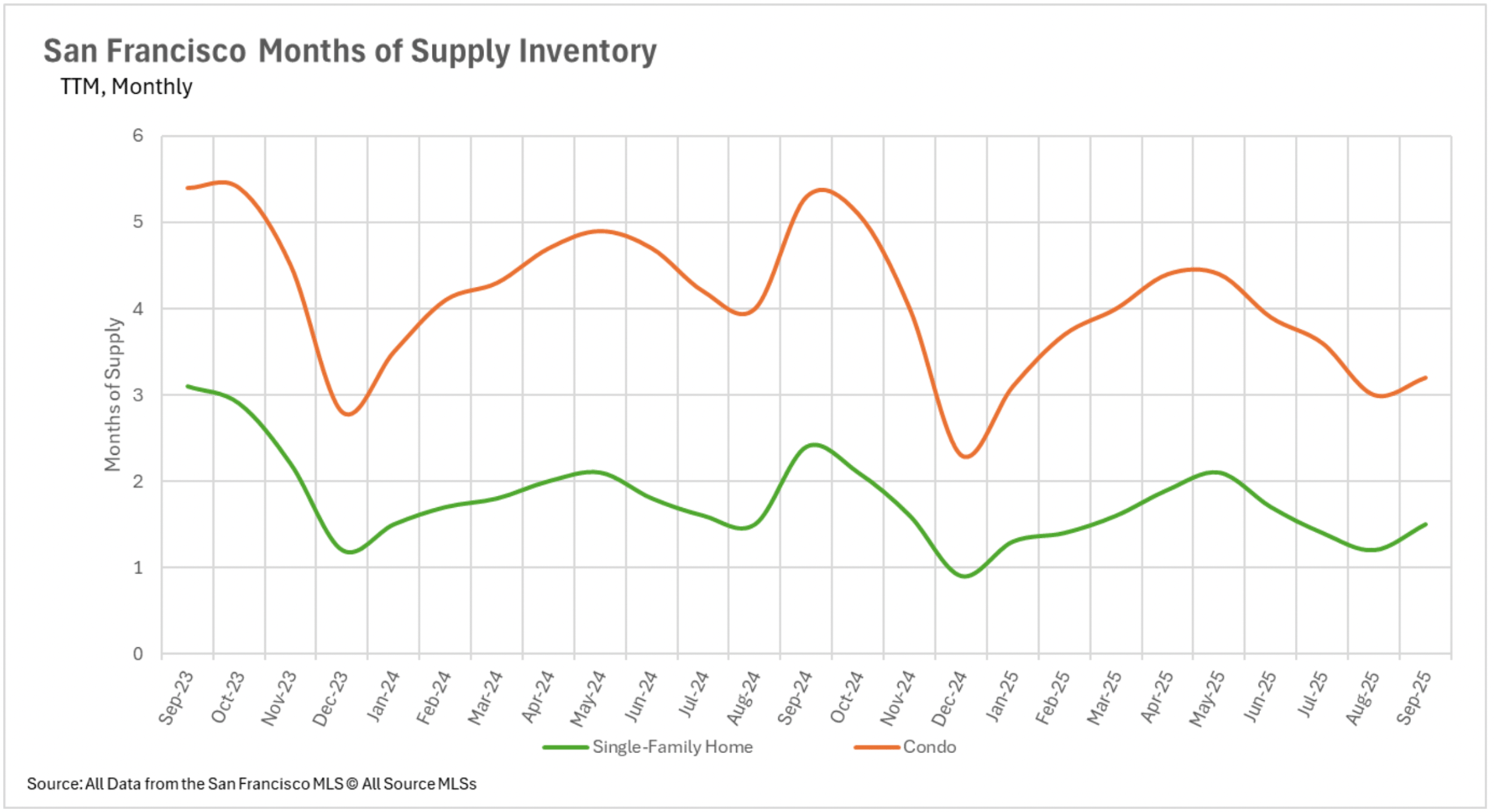

The regionwide progression toward seller-favorable markets strengthens as availability stabilization advances, with San Francisco's condominium sector nearing seller territory and other regions displaying consistent movement in that trajectory.

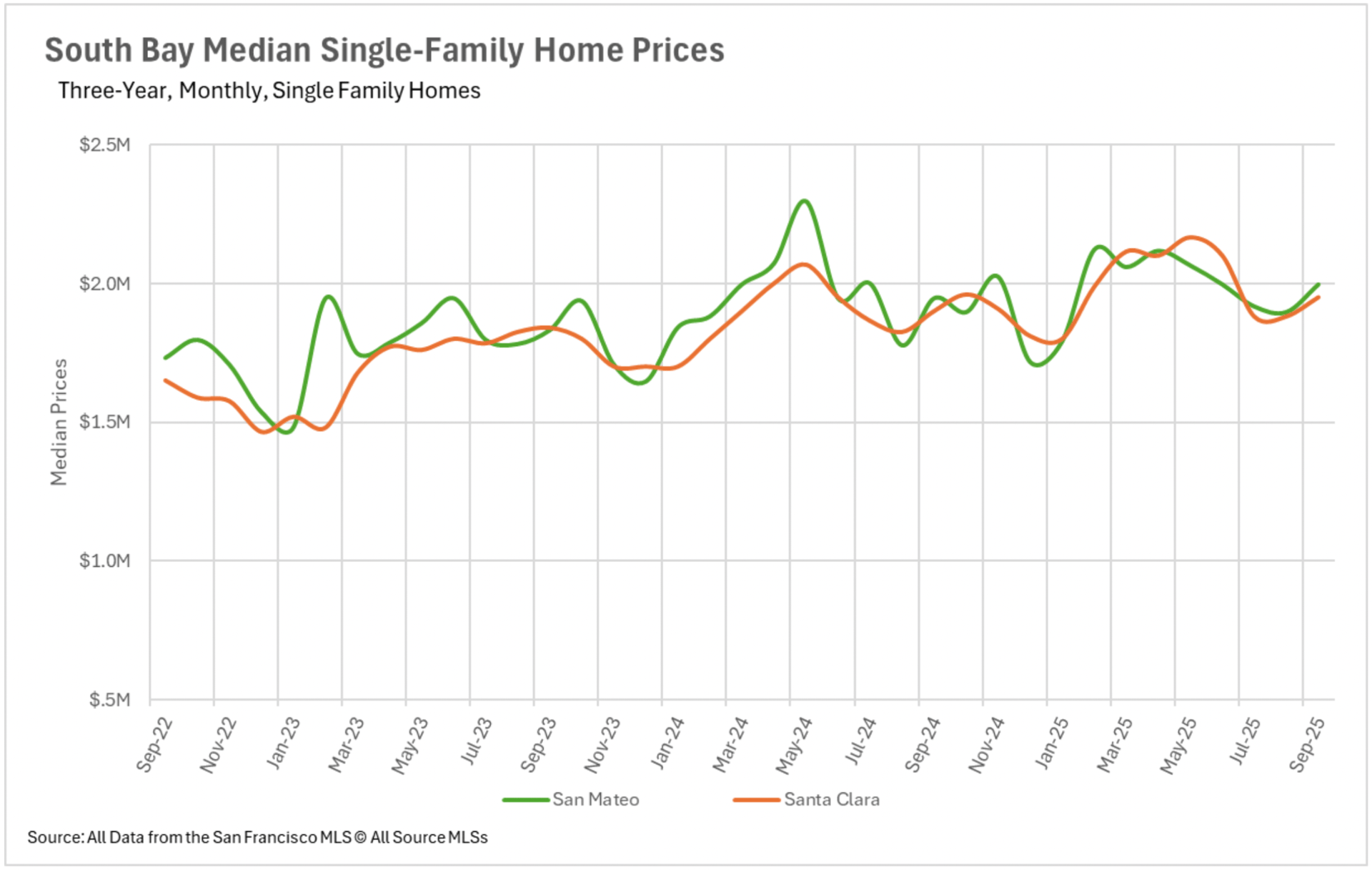

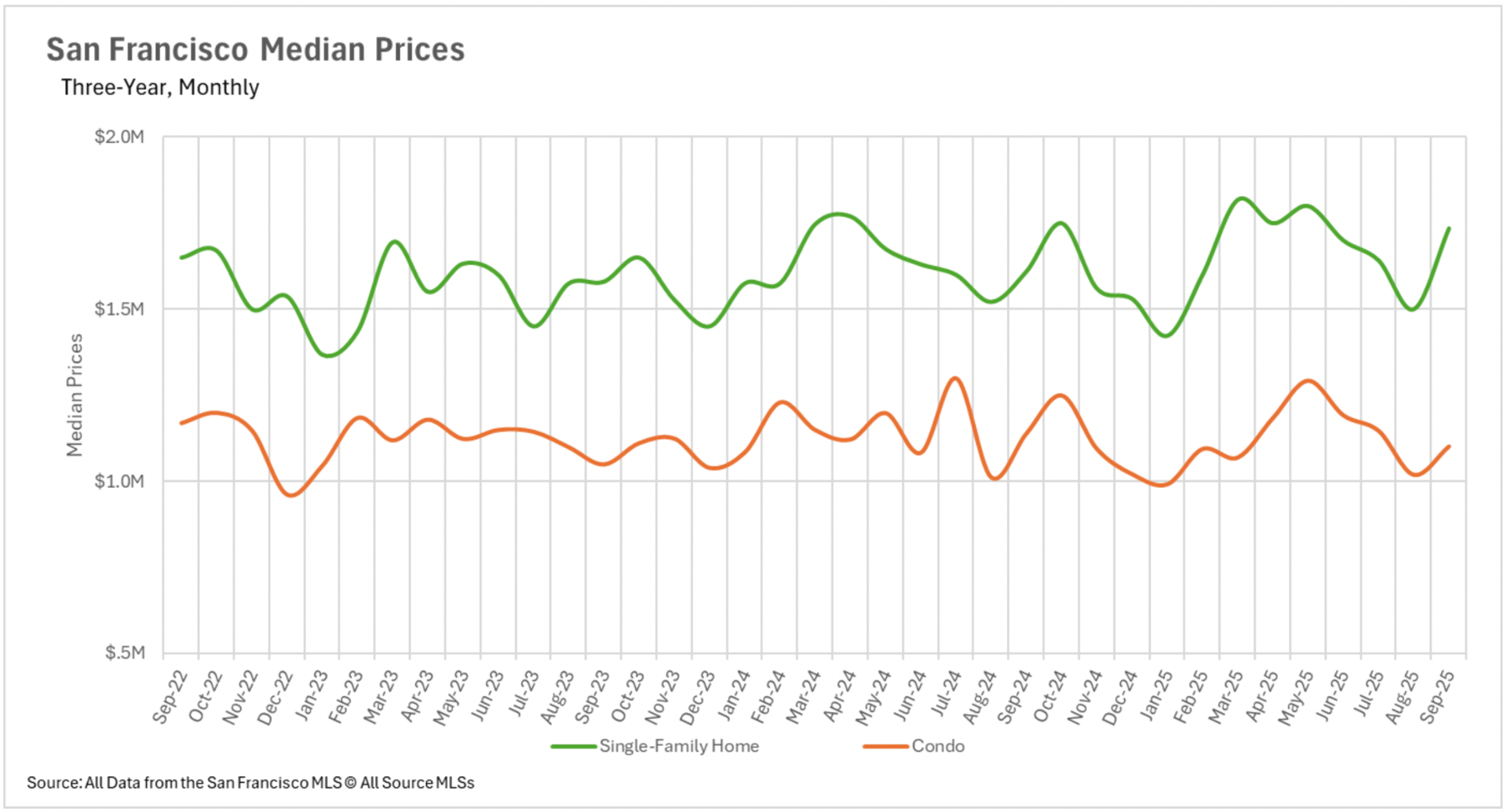

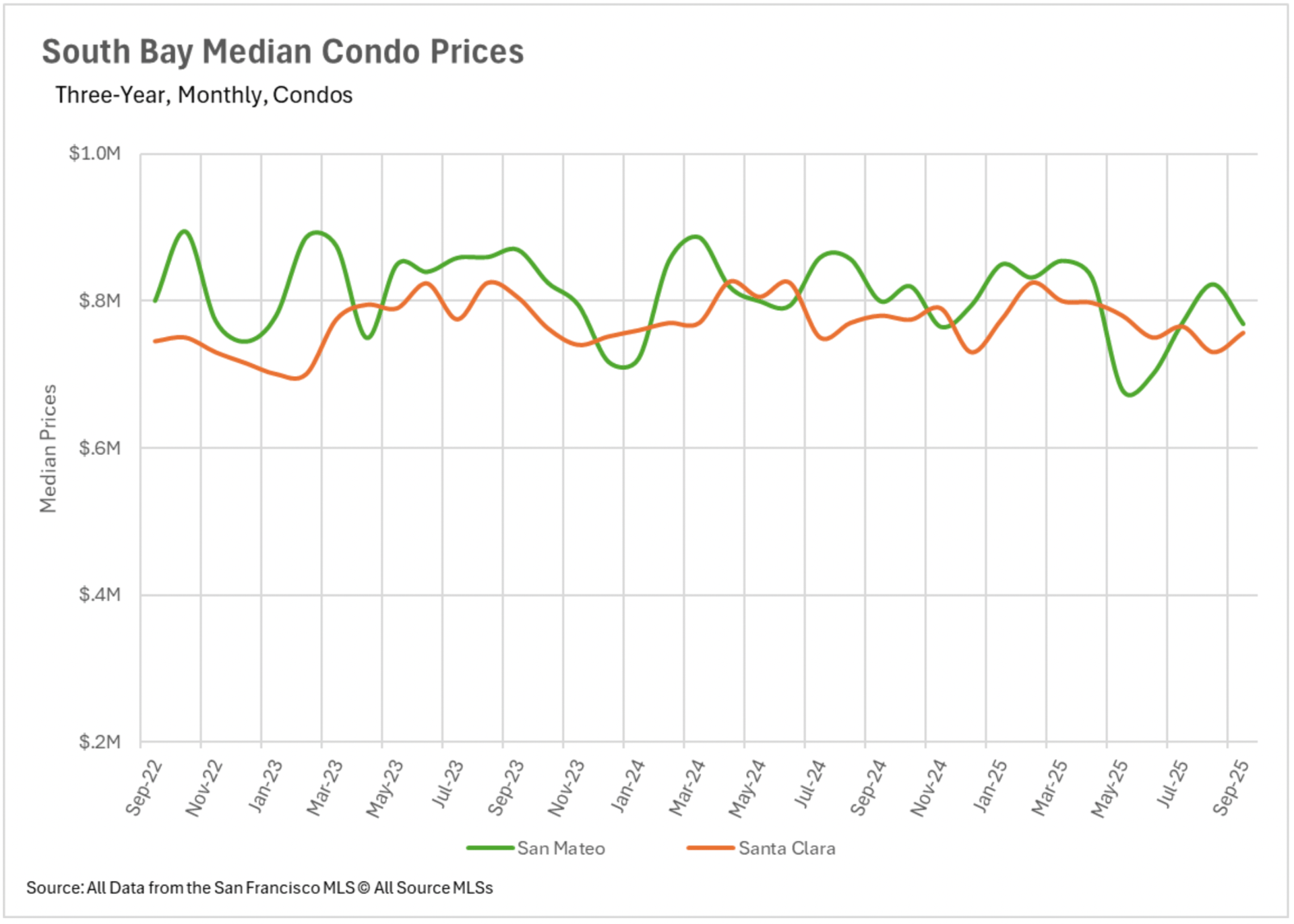

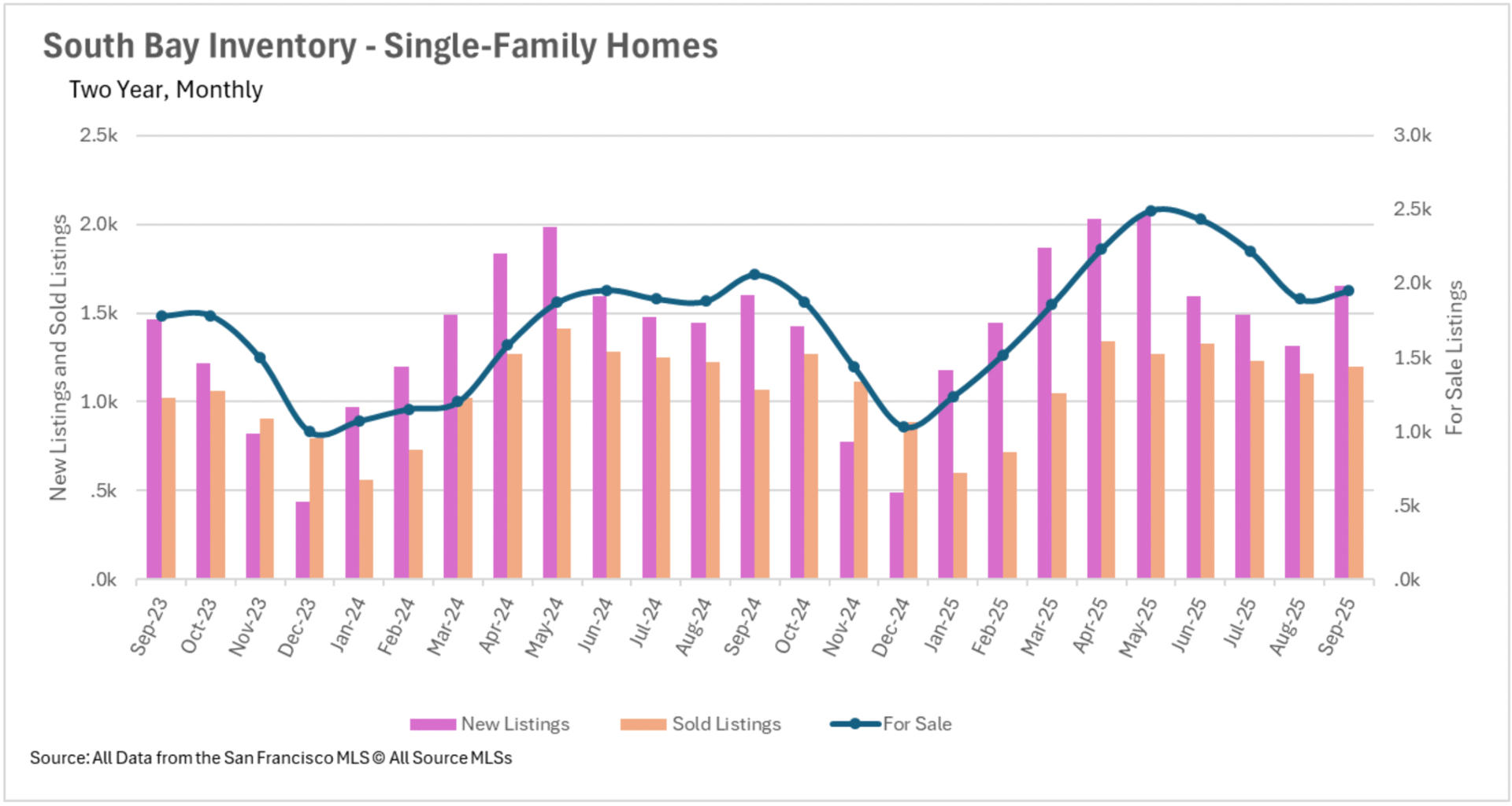

September highlighted contrasting value patterns throughout the Bay Area, with San Francisco recording a substantial surge while other regions sustained relative equilibrium. San Francisco's single-family residential sector jumped 7.76% annually, establishing the most significant increase the market has recorded all year, though condominiums retreated 3.29%. Significantly, the typical San Francisco condominium is now transacting at a modest premium to listing value for the initial time since May. Silicon Valley exhibited exceptional steadiness with single-family properties maintaining their established value parameters - San Mateo and Santa Clara Counties registered moderate advances of 2.56% and 2.63% respectively, while Santa Cruz County declined 4.30%.

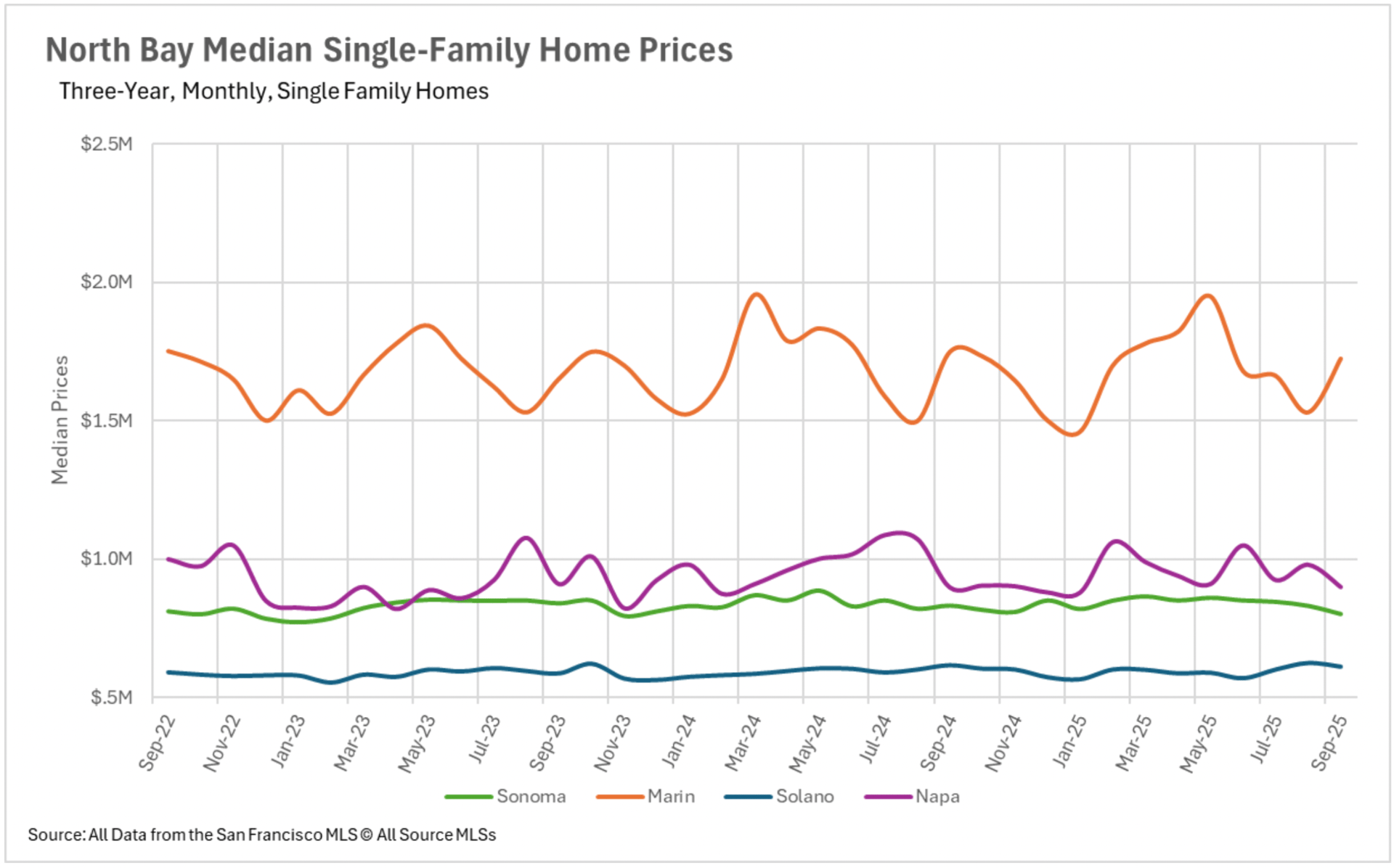

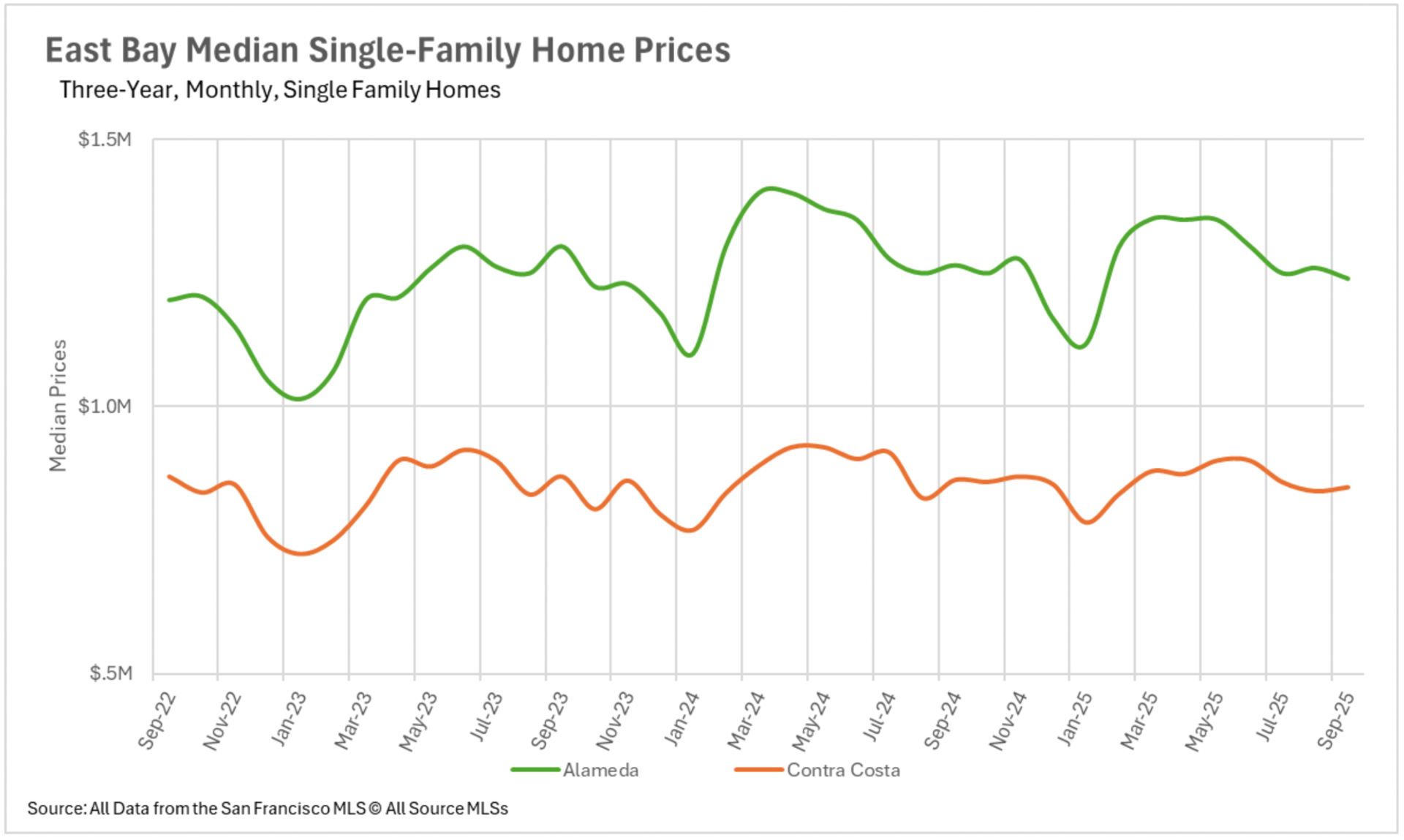

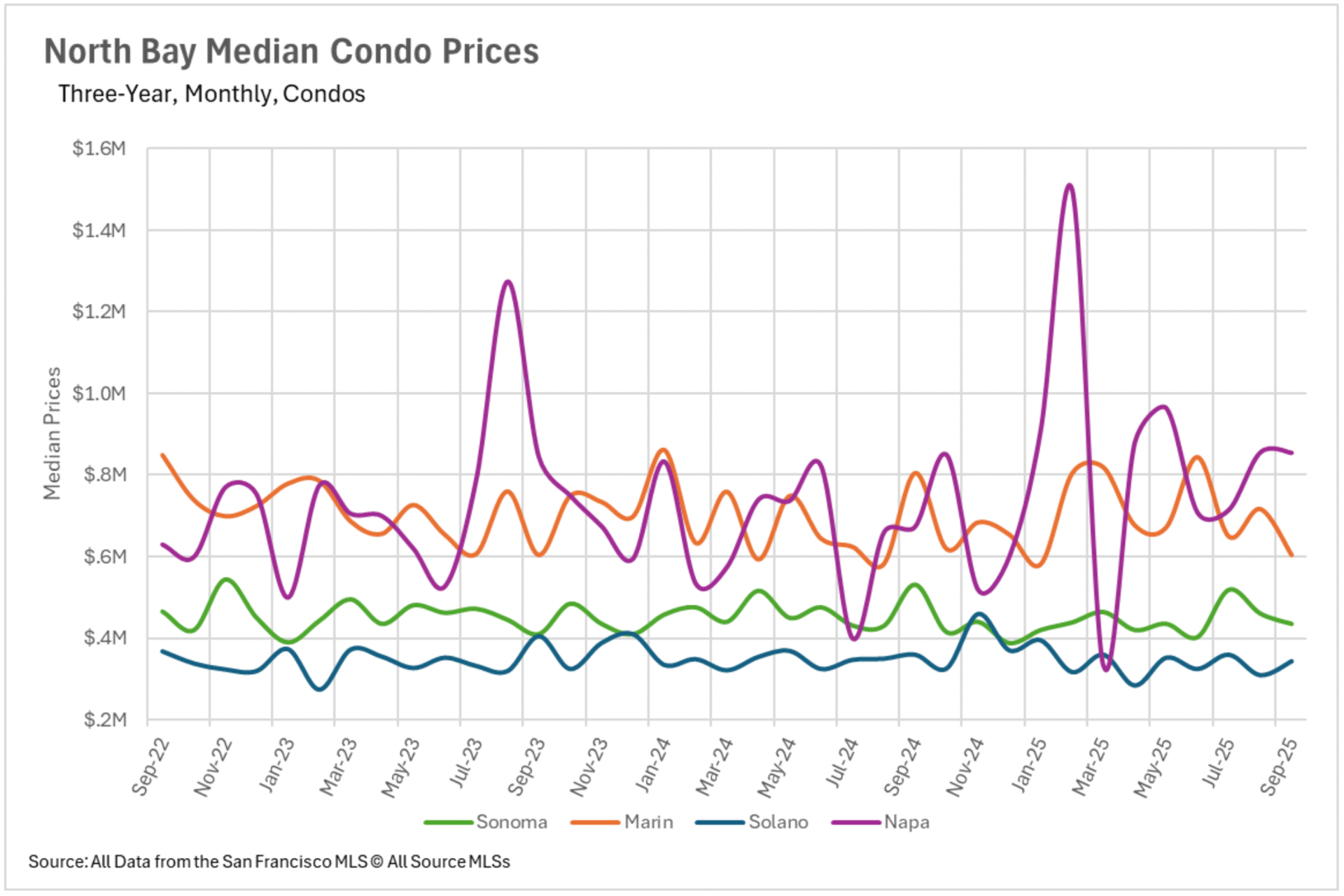

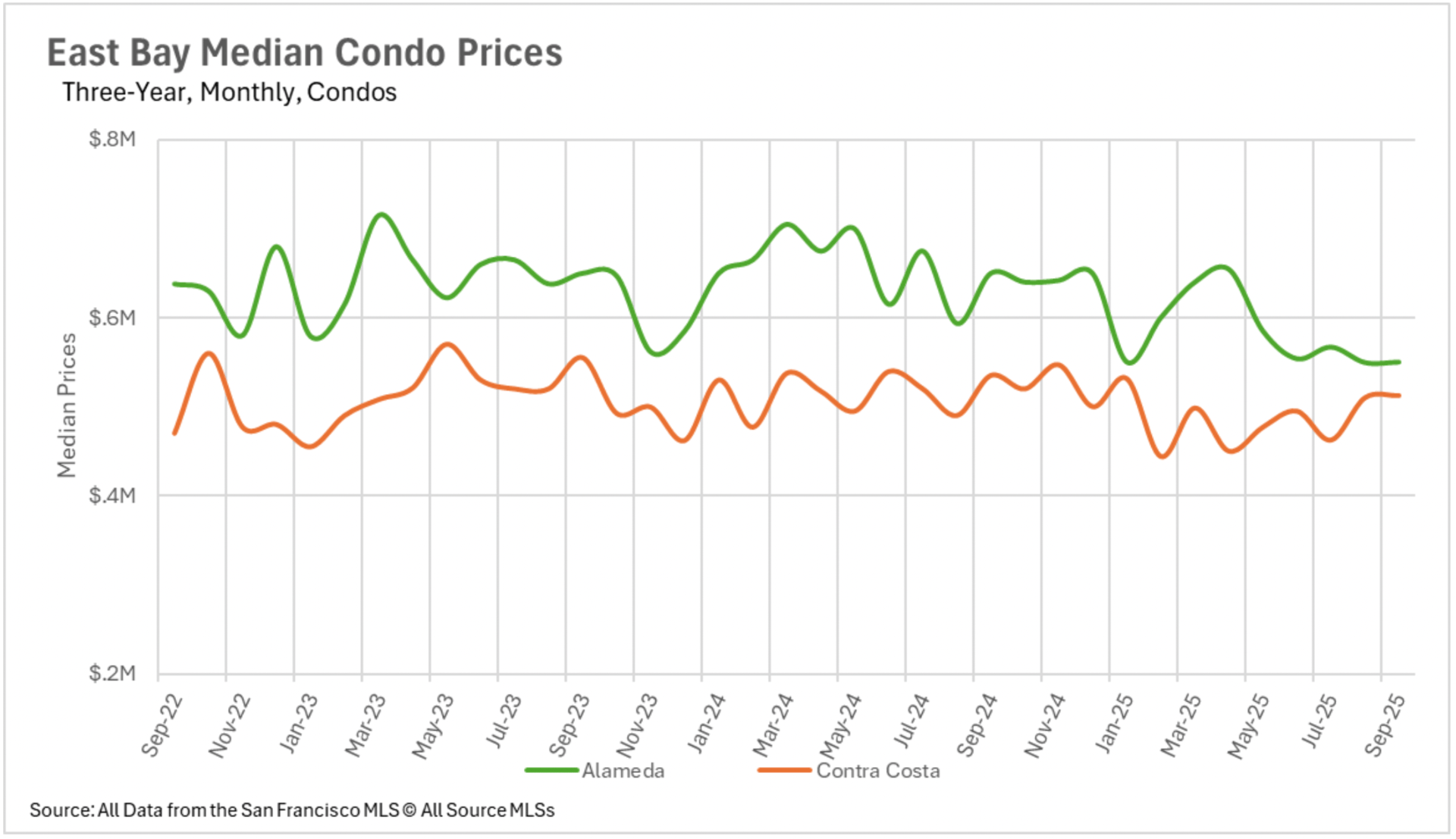

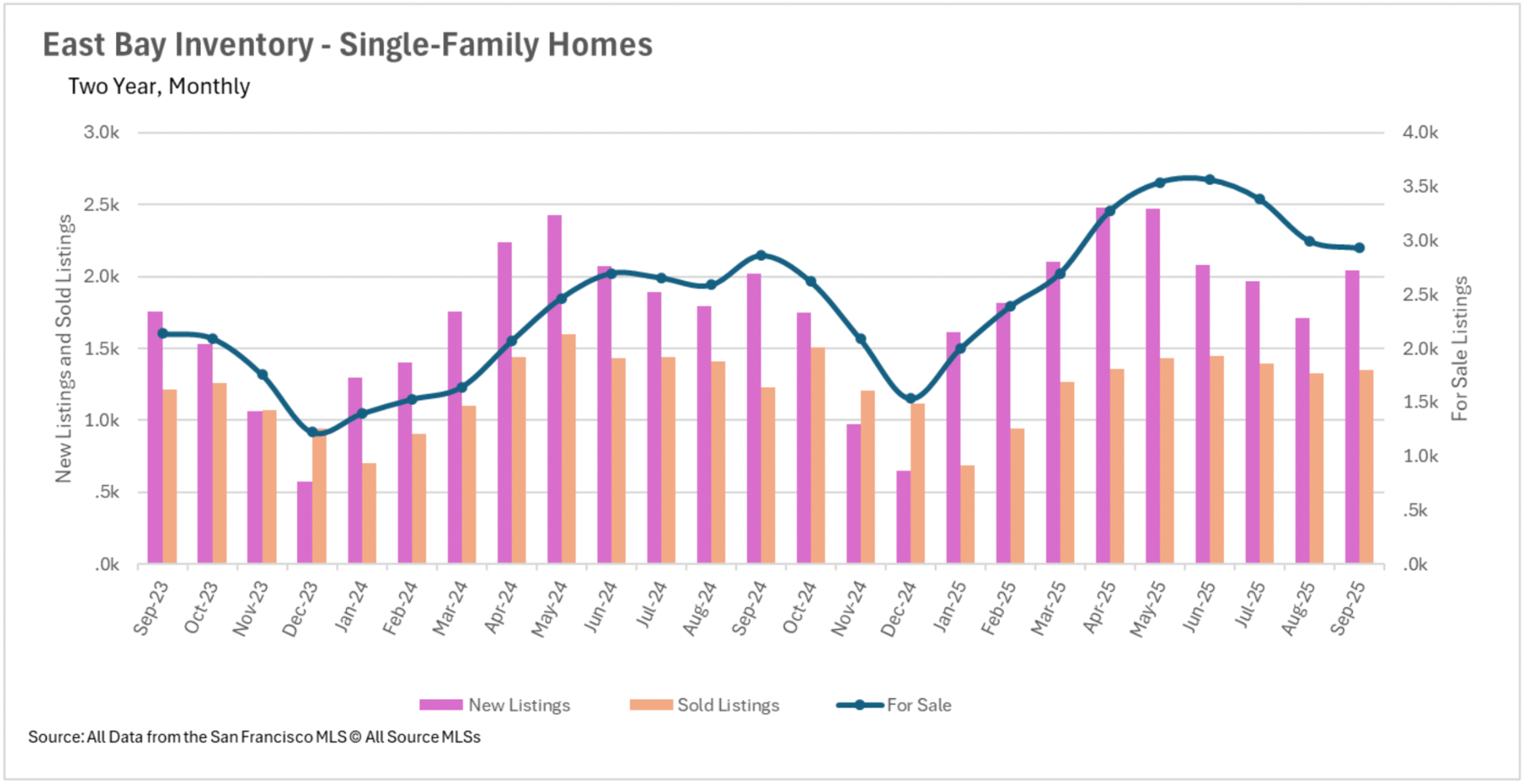

The condominium sector perpetuated its downward trajectory for the second straight month with retreats of 3.88% in San Mateo, 3.01% in Santa Clara, and 2.53% in Santa Cruz. East Bay markets reverted to annual declines following August's temporary recovery, with single-family properties down 1.98% in Alameda County and 1.59% in Contra Costa, though values remain comfortably within their established parameters. Condominiums in Contra Costa County declined 4.21% annually. North Bay regions displayed the most consistent pattern with near-stagnant valuation throughout - Sonoma, Marin, and Solano Counties all recorded modest retreats of 3.47%, 1.43%, and 0.81% respectively, while Napa County achieved a minimal 0.17% premium to previous year values.

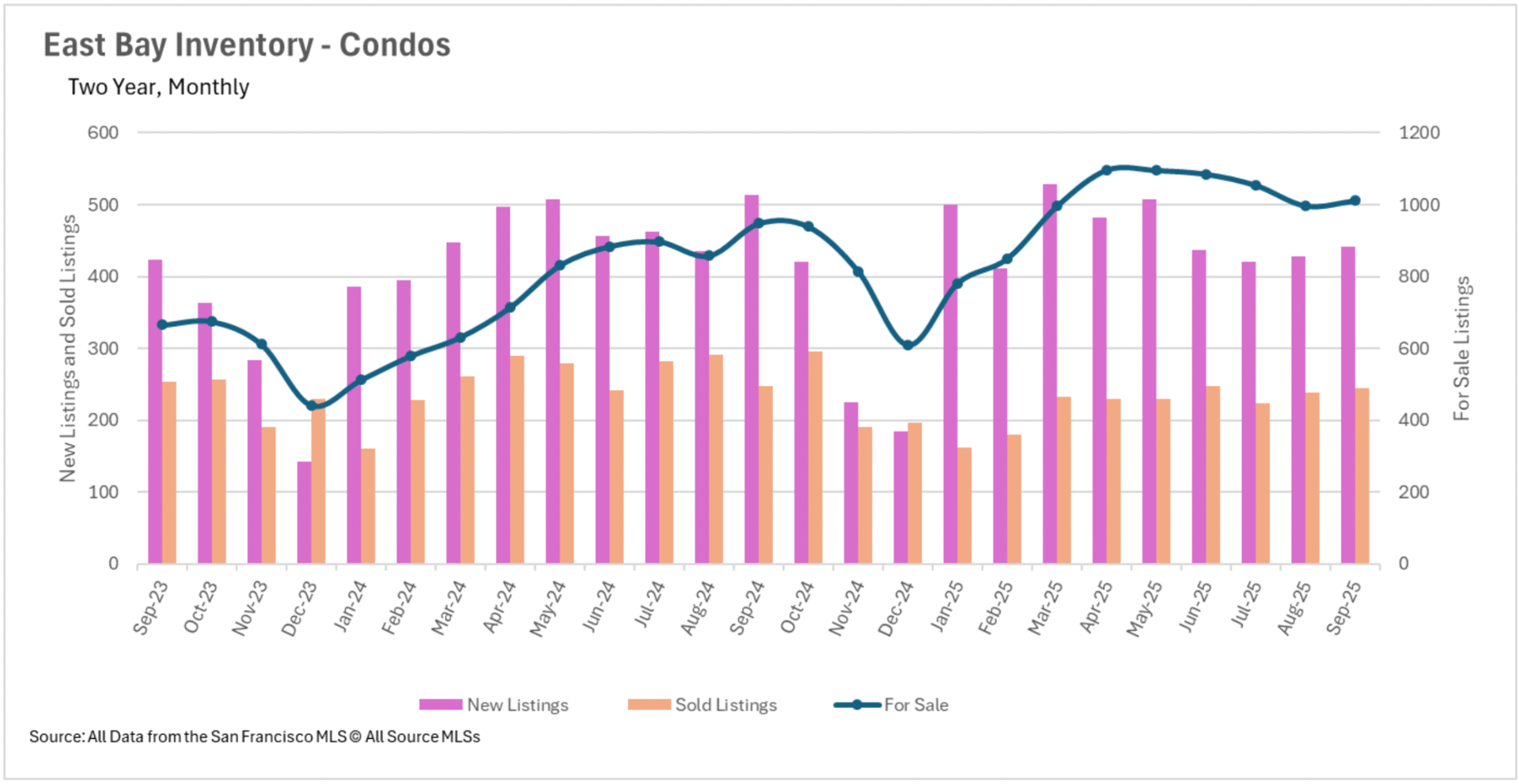

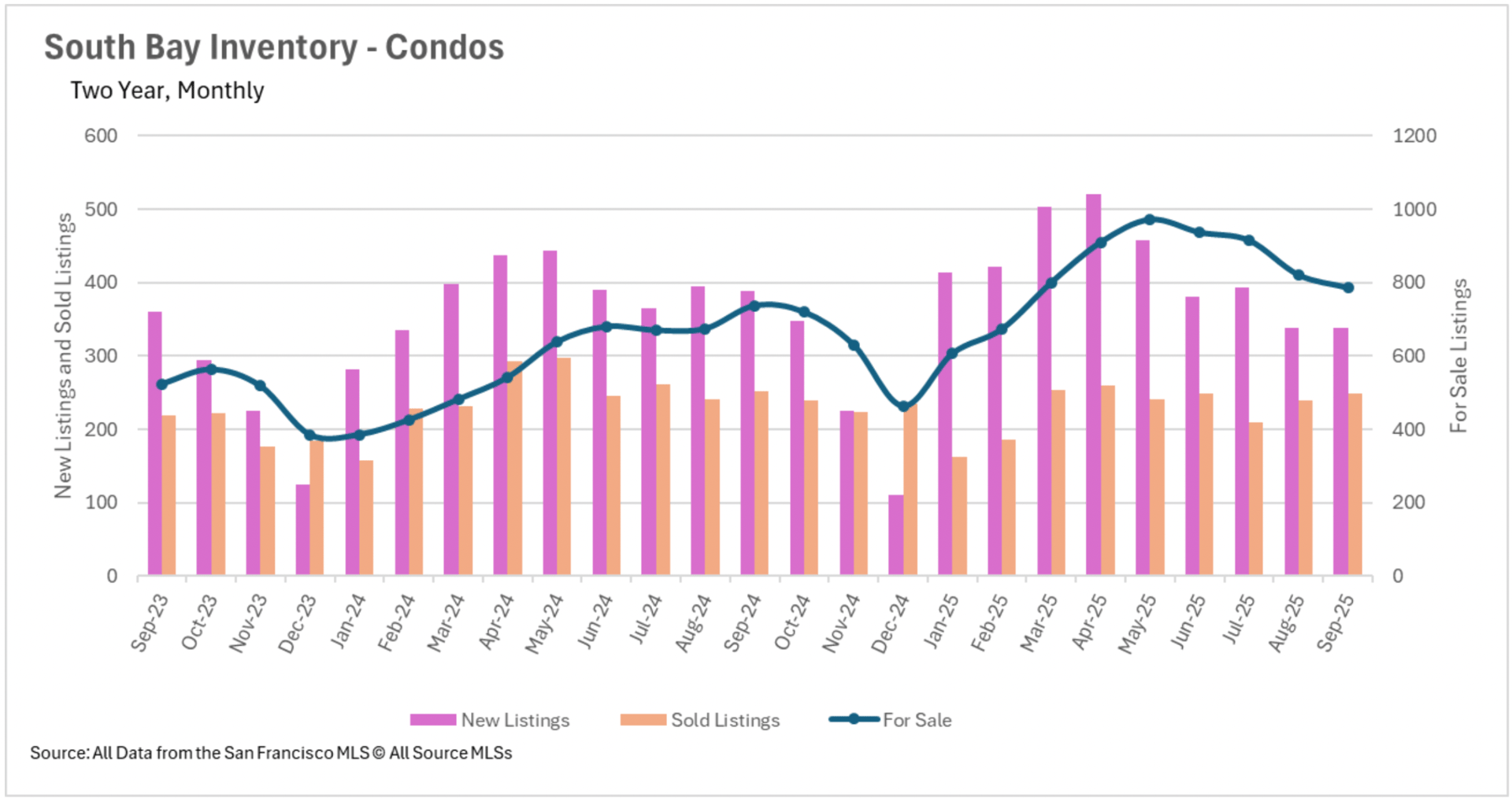

September constituted a pivotal development for Bay Area availability levels, with most regions documenting their initial annual reductions in months. San Francisco commanded with the most substantial availability compression, as single-family property listings plummeted 33.65% and condominium supply declined 32.22% annually. This resulted from a combination of 11.26% reduced new single-family listings, 7.61% reduced new condominium listings, and surging transactions with 19.33% more single-family properties and an exceptional 51.82% more condominiums sold. Silicon Valley's single-family sector accomplished a significant turnaround, recording 5.34% fewer active listings than last year, predominantly due to 12.56% more properties sold. Nevertheless, the condominium sector remained moderately elevated at 6.65% above previous year levels.

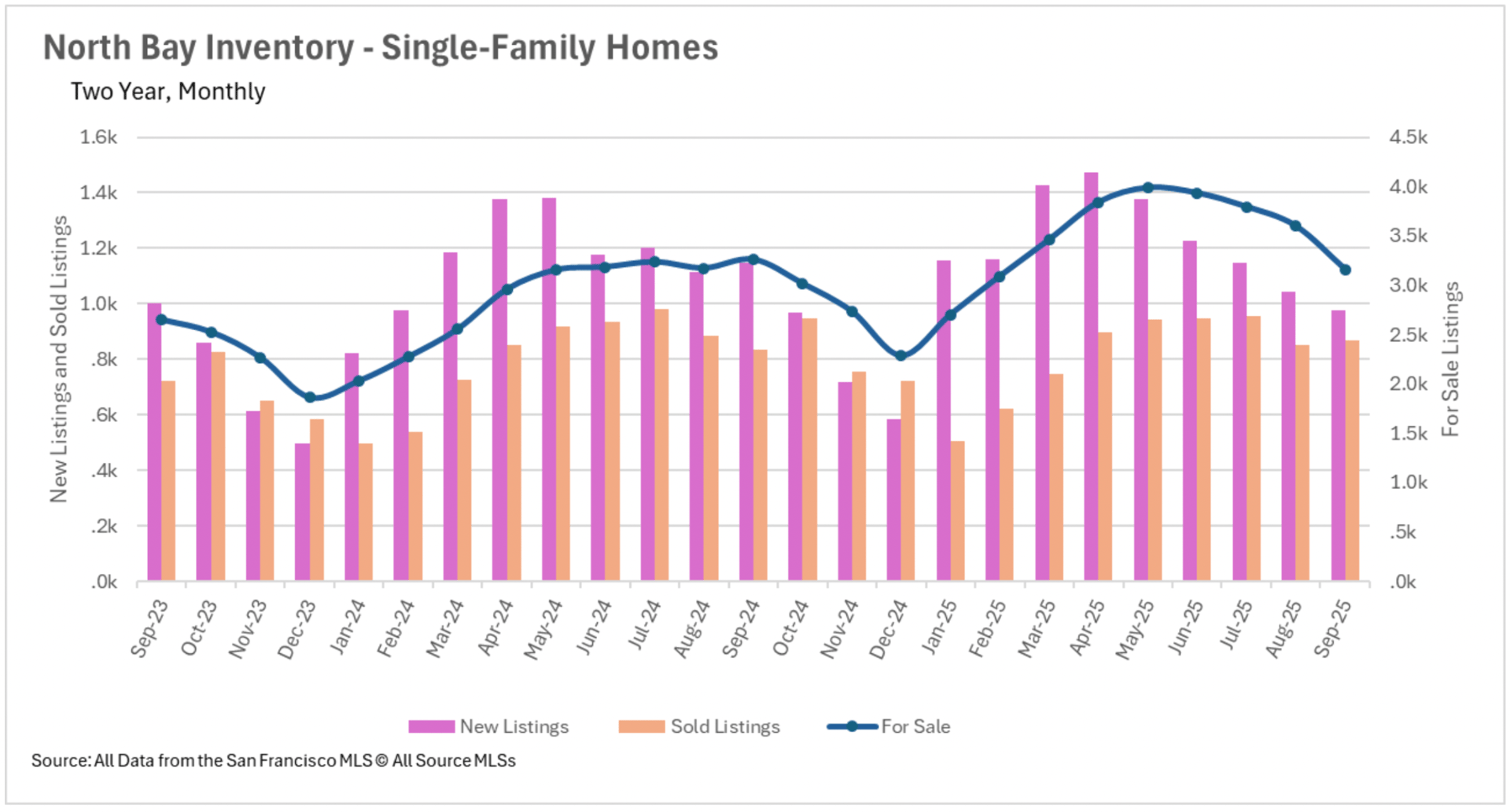

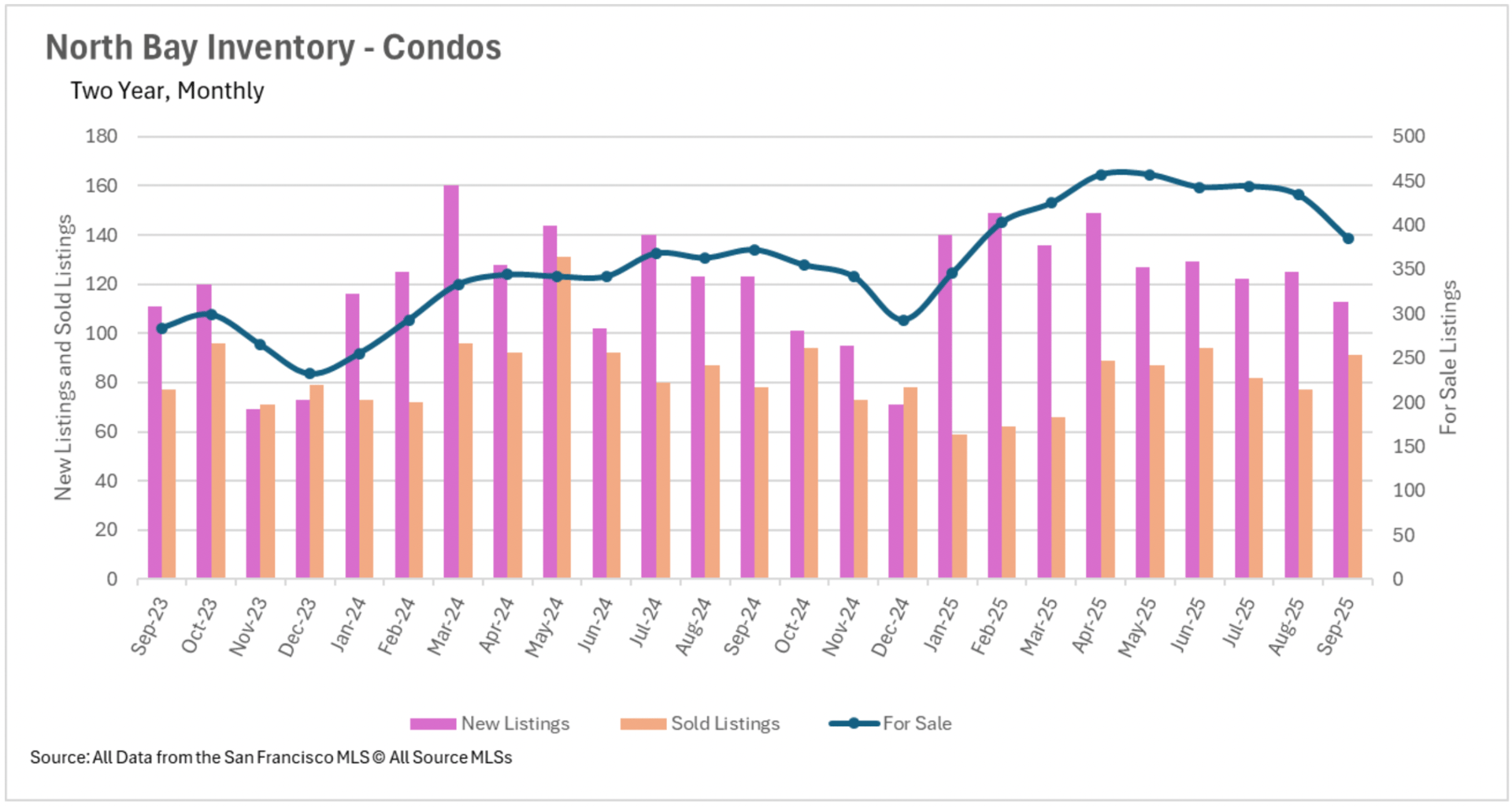

North Bay regions recorded their initial annual availability reduction in several months, with single-family listings declining 2.98%, propelled by a pronounced 14.75% decrease in new listings and a 3.95% increase in sold listings, producing a substantial 12.14% monthly availability decline. Condominium supply remained moderately elevated at 3.49% above last year. East Bay markets demonstrated continued stabilization with single-family availability at merely 2.41% above last year and condominiums at 6.75% above, both representing considerable improvements from summer peaks. The stabilization benefited from nearly 10% more single-family properties sold in September compared to last year.

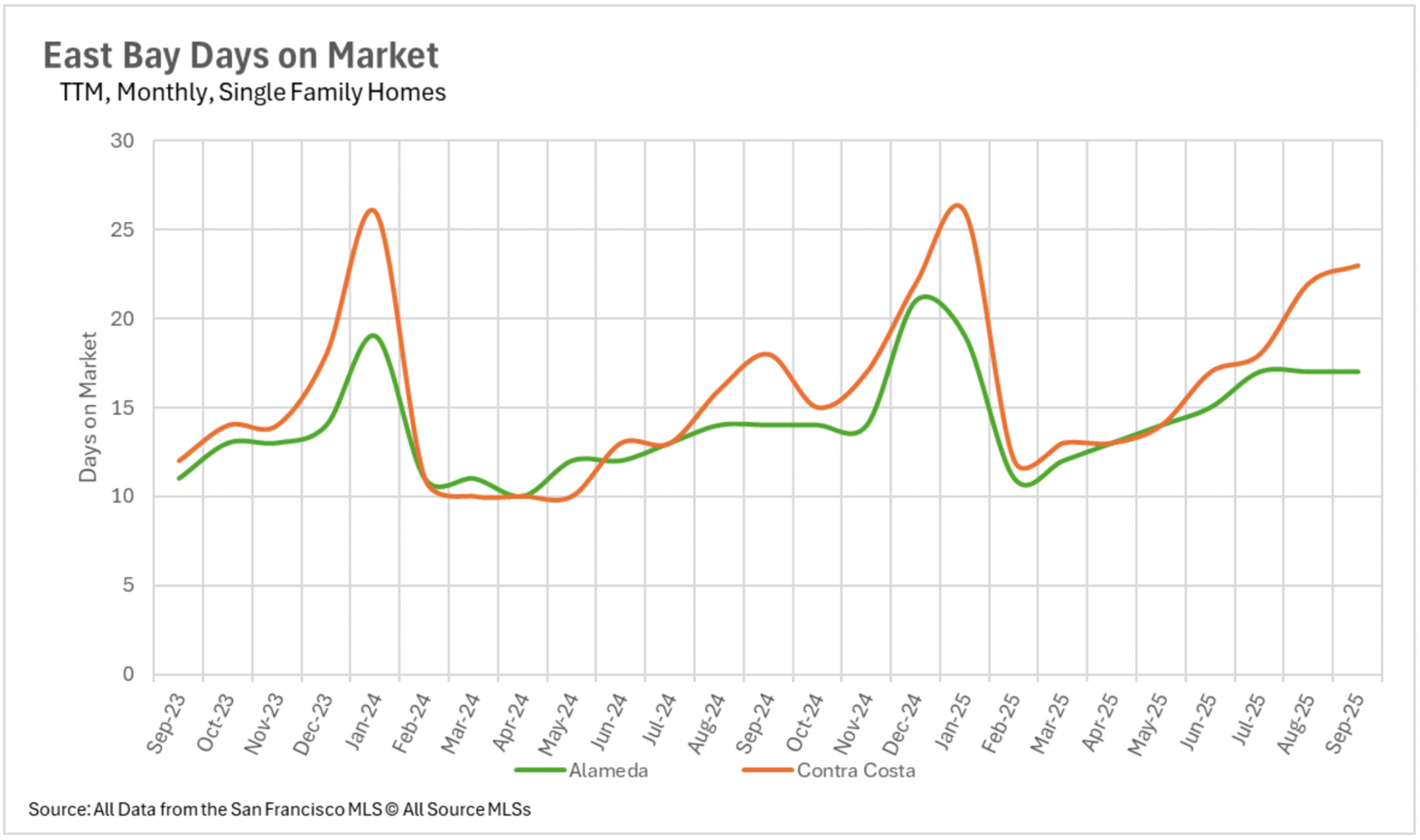

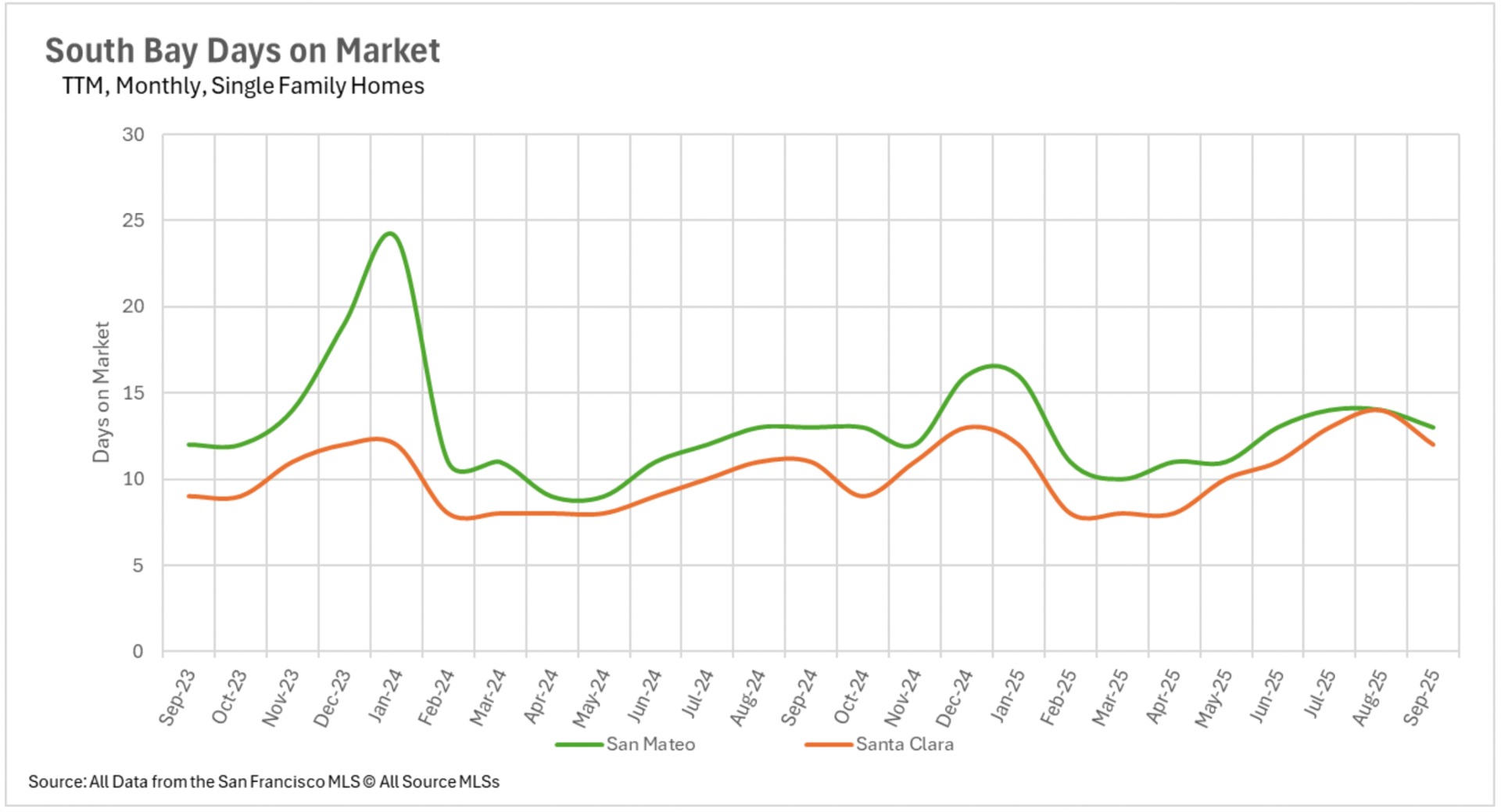

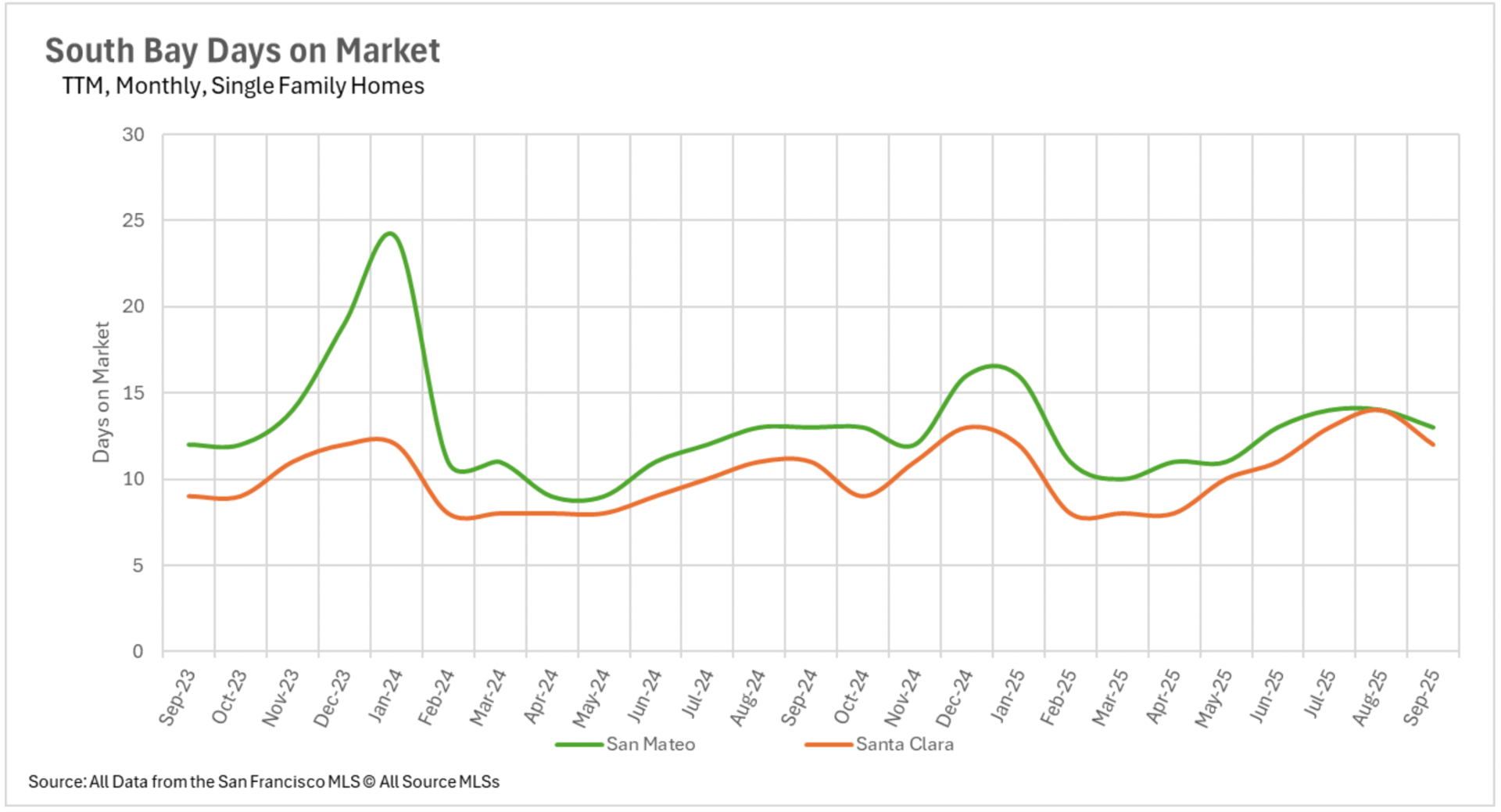

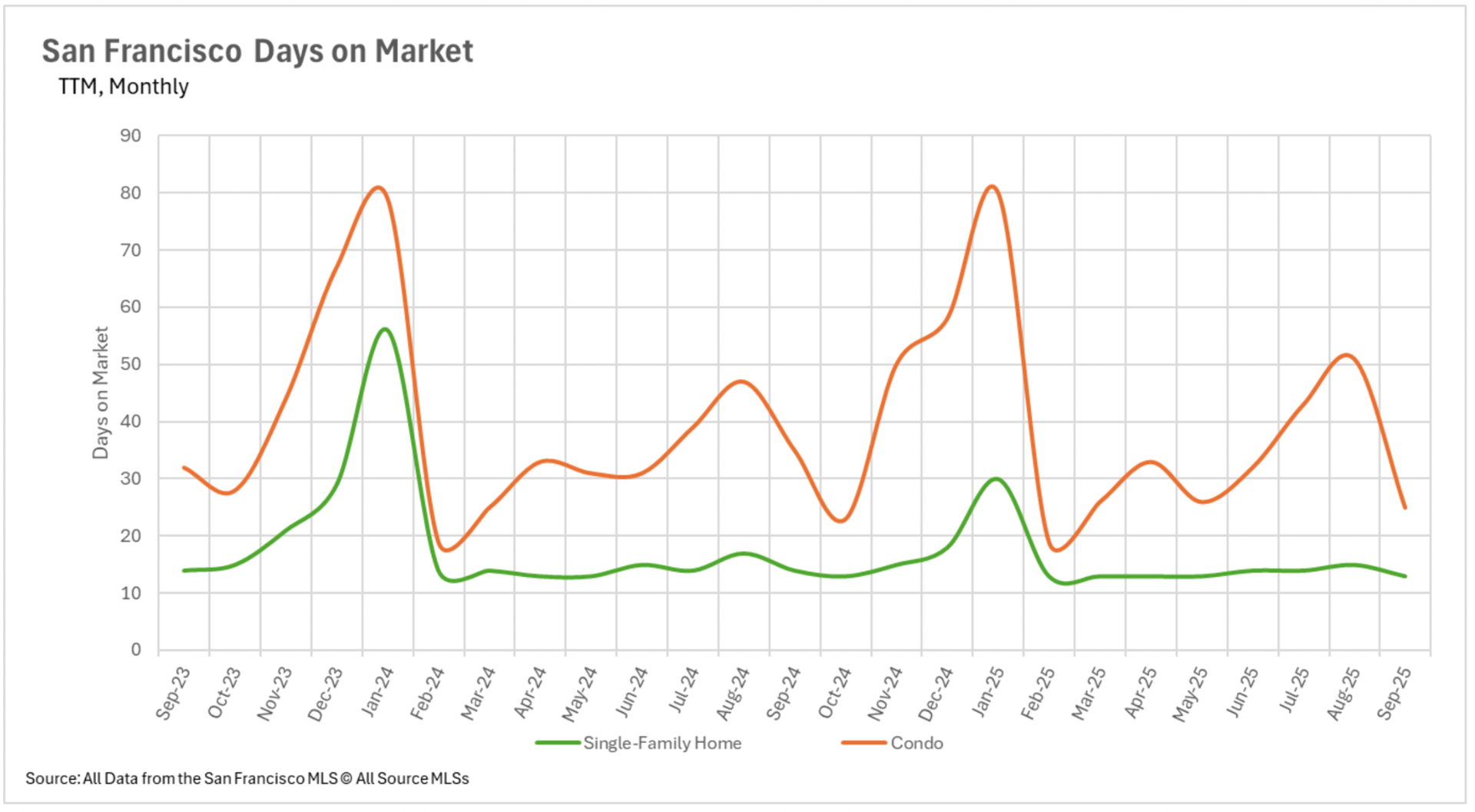

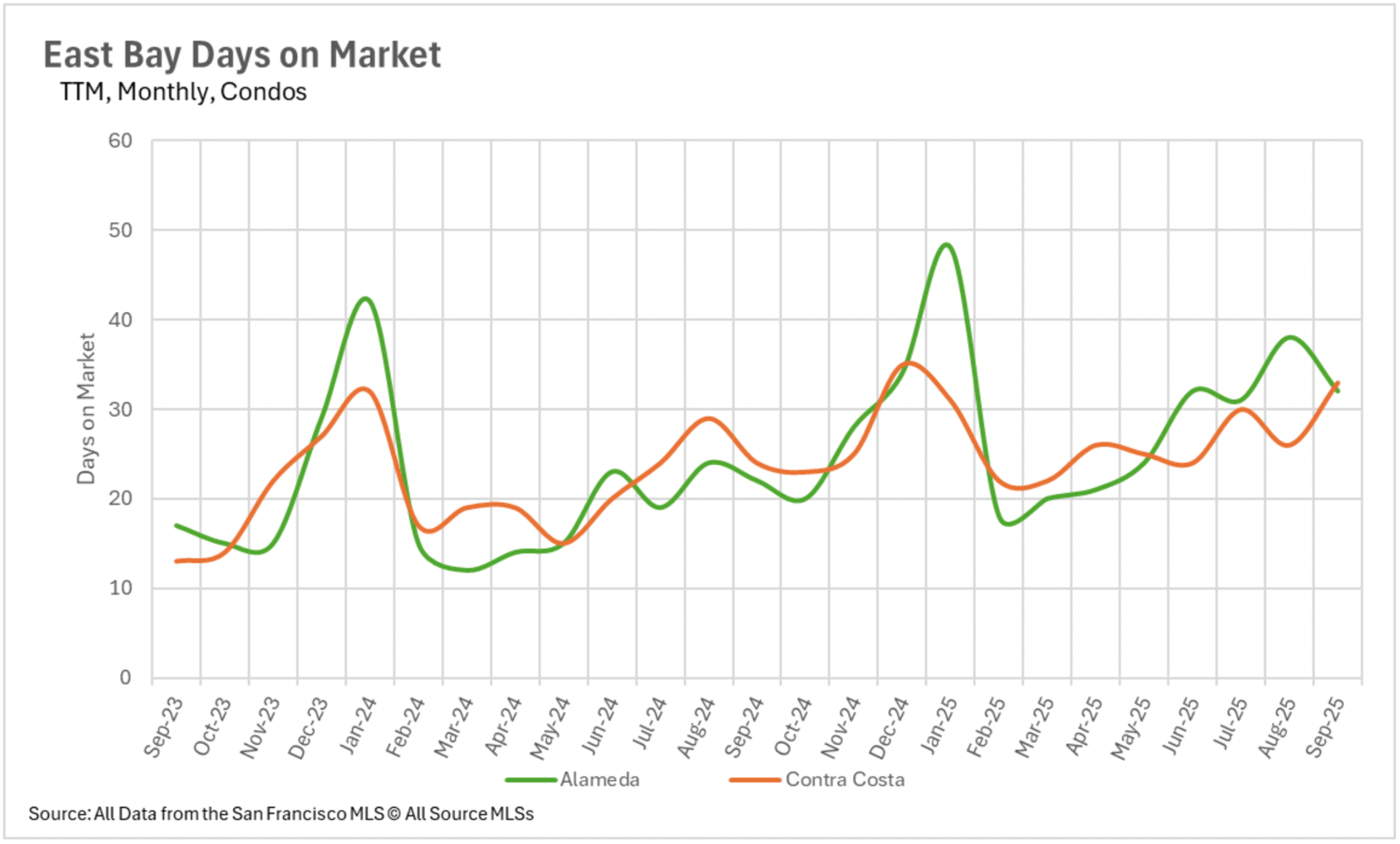

September unveiled a compelling contradiction throughout the Bay Area: while percentage increases in marketing duration appear meaningful, absolute figures remain exceptionally minimal, signaling robust underlying demand. San Francisco demonstrated intensifying efficiency with single-family properties requiring just 13 days on market (declining 7.14% annually) and condominiums contracting to 25 days (declining 28.57% annually and 50.98% monthly). Silicon Valley sustained exceptional momentum for single-family properties, with San Mateo and Santa Clara County listings acquired within two weeks, and Santa Cruz County at merely 29 days.

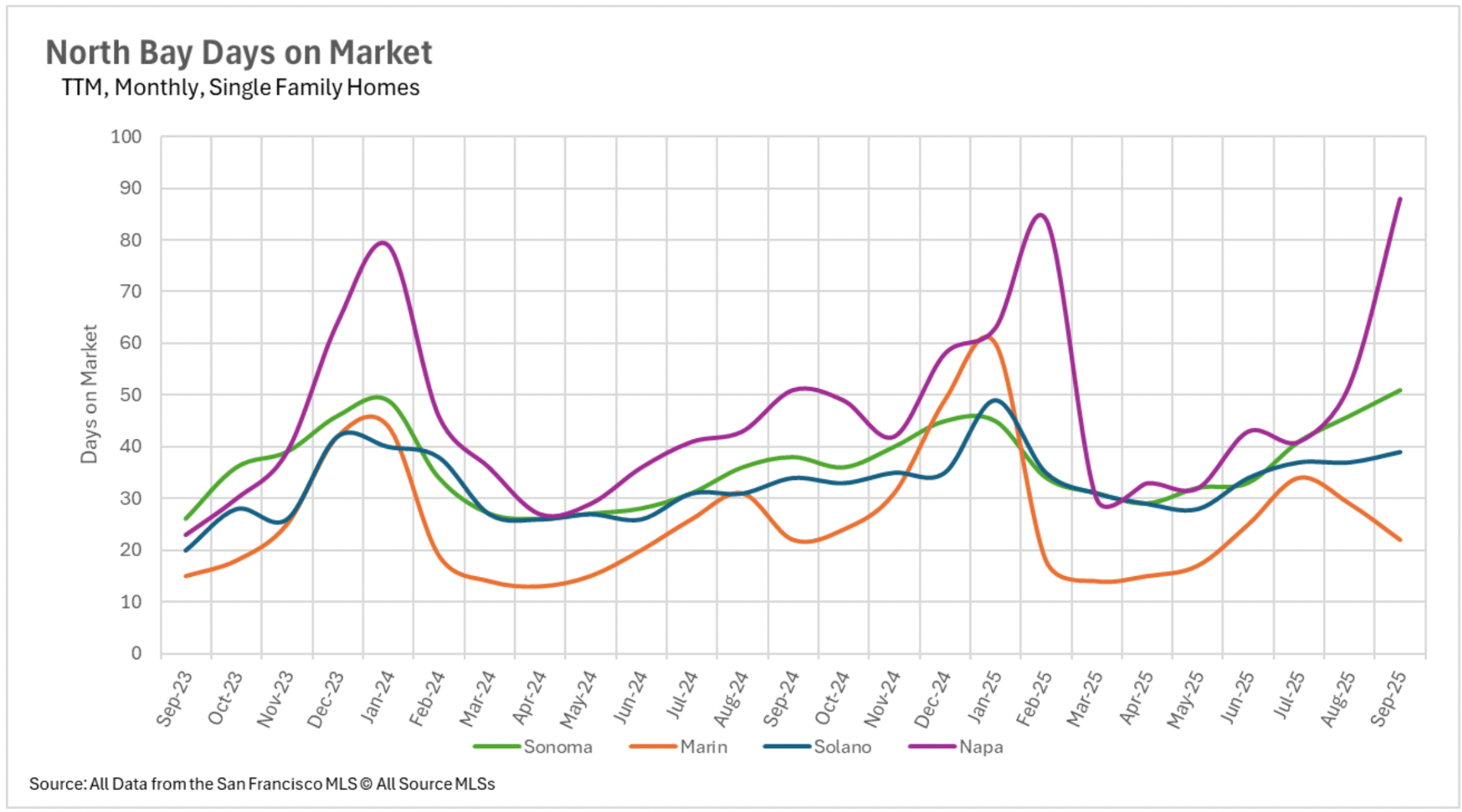

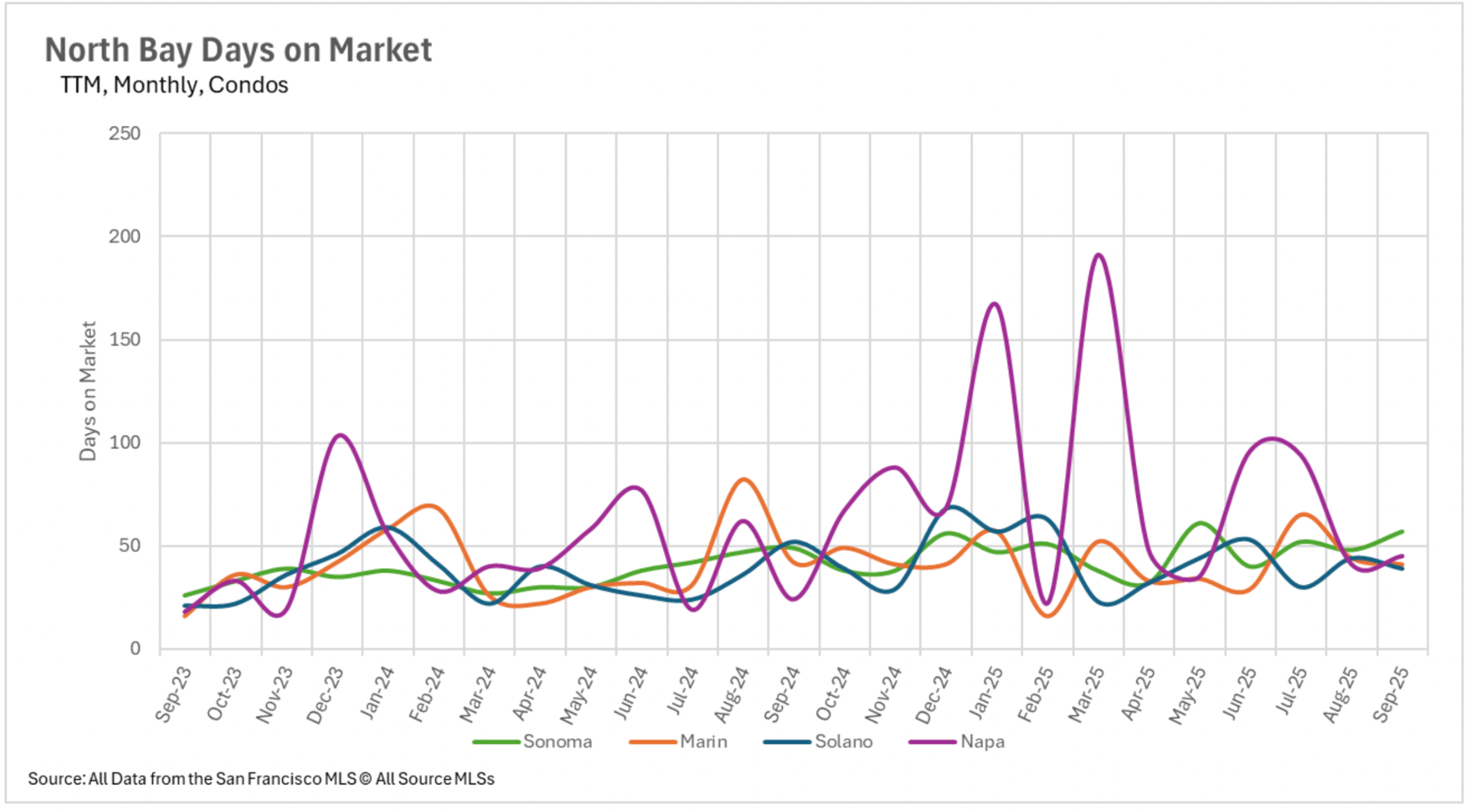

Nevertheless, condominiums are facing considerable delays with San Mateo at 40 days (+25% annually), Santa Clara at 28 days (+55.56%), and Santa Cruz at 41 days (+2.5%). East Bay markets exhibited meaningful percentage increases but preserved relatively expeditious absolute durations, with single-family properties requiring 17 days in Alameda County (+21.43% annually) and 23 days in Contra Costa (+27.78%). Condominiums transacted in 32 and 33 days respectively, despite annual increases of 45.45% and 37.50%. North Bay regions presented the most pronounced contrast, with Napa County's typical listing requiring 88 days on market (advancing 72.55% annually and 69.23% monthly), while other counties demonstrated more moderate increases. Marin County contradicted all patterns, preserving identical marketing duration as last year.

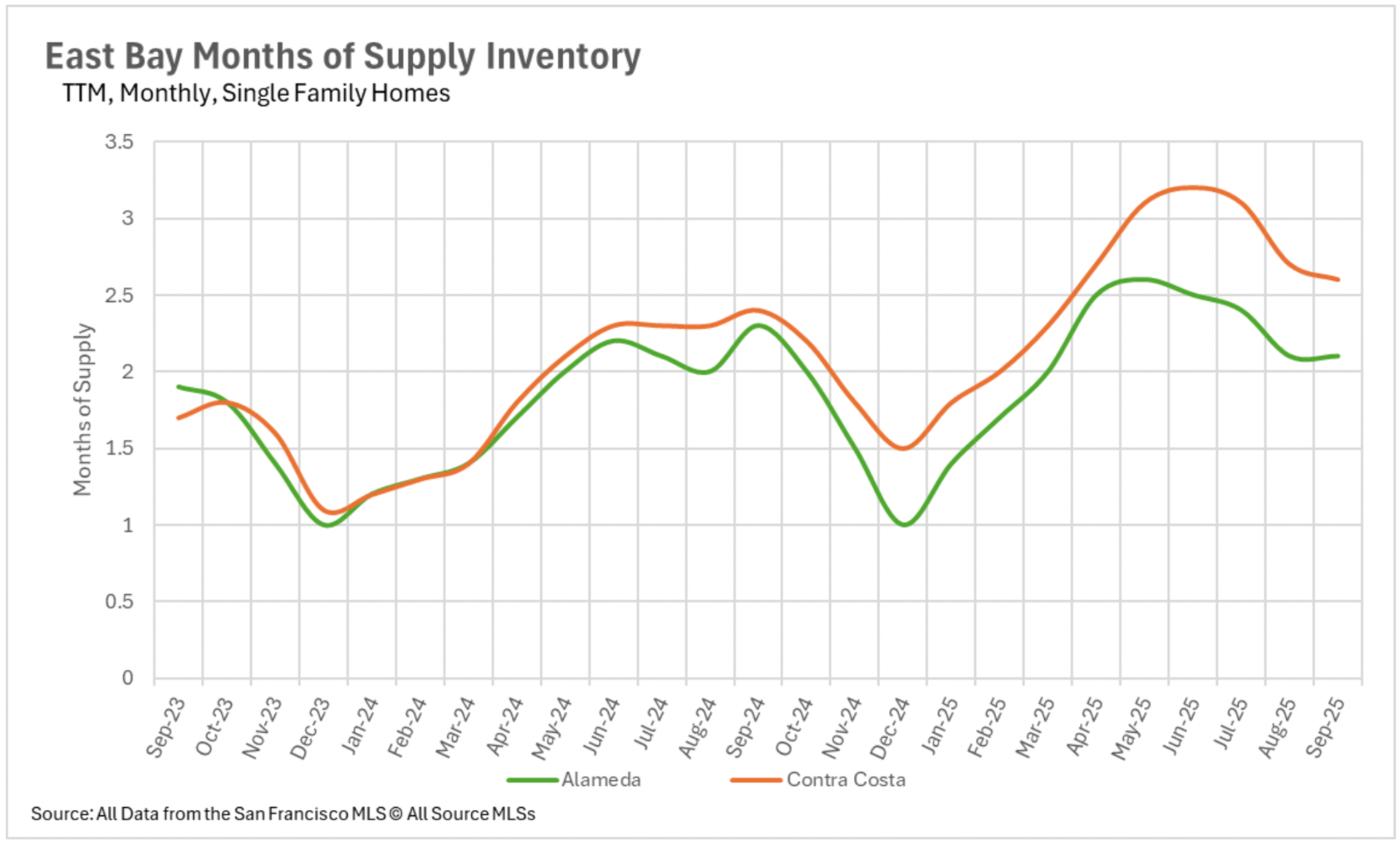

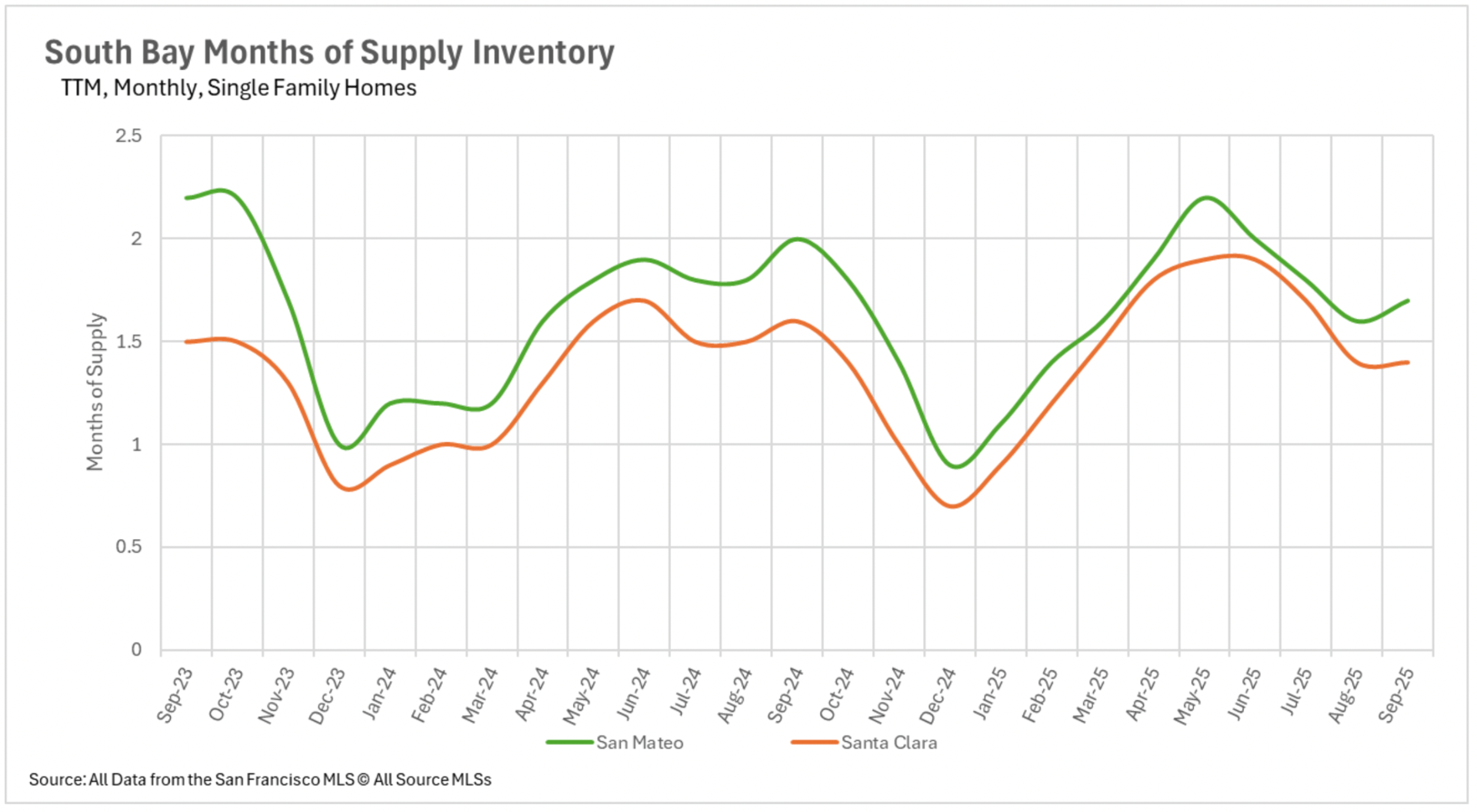

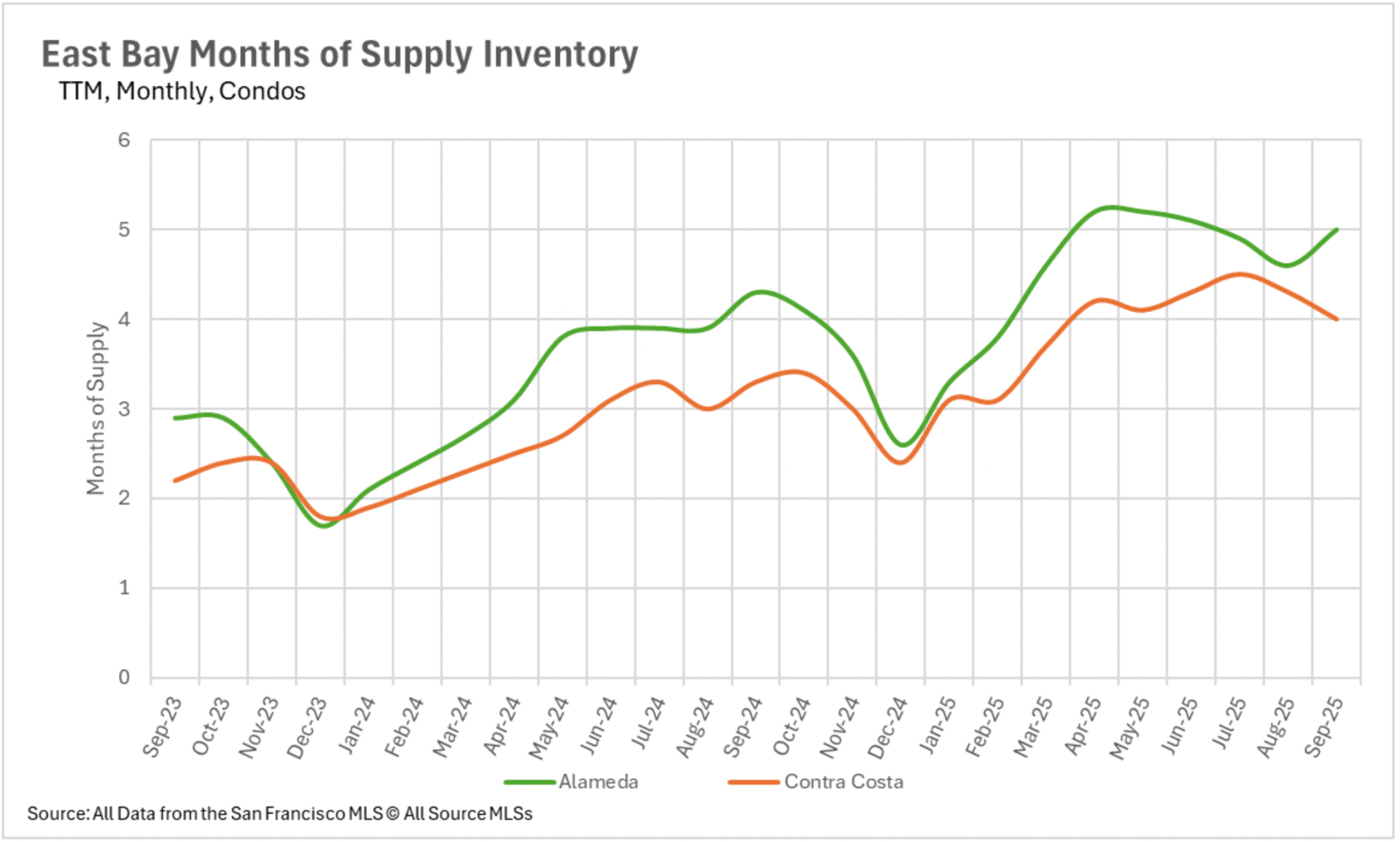

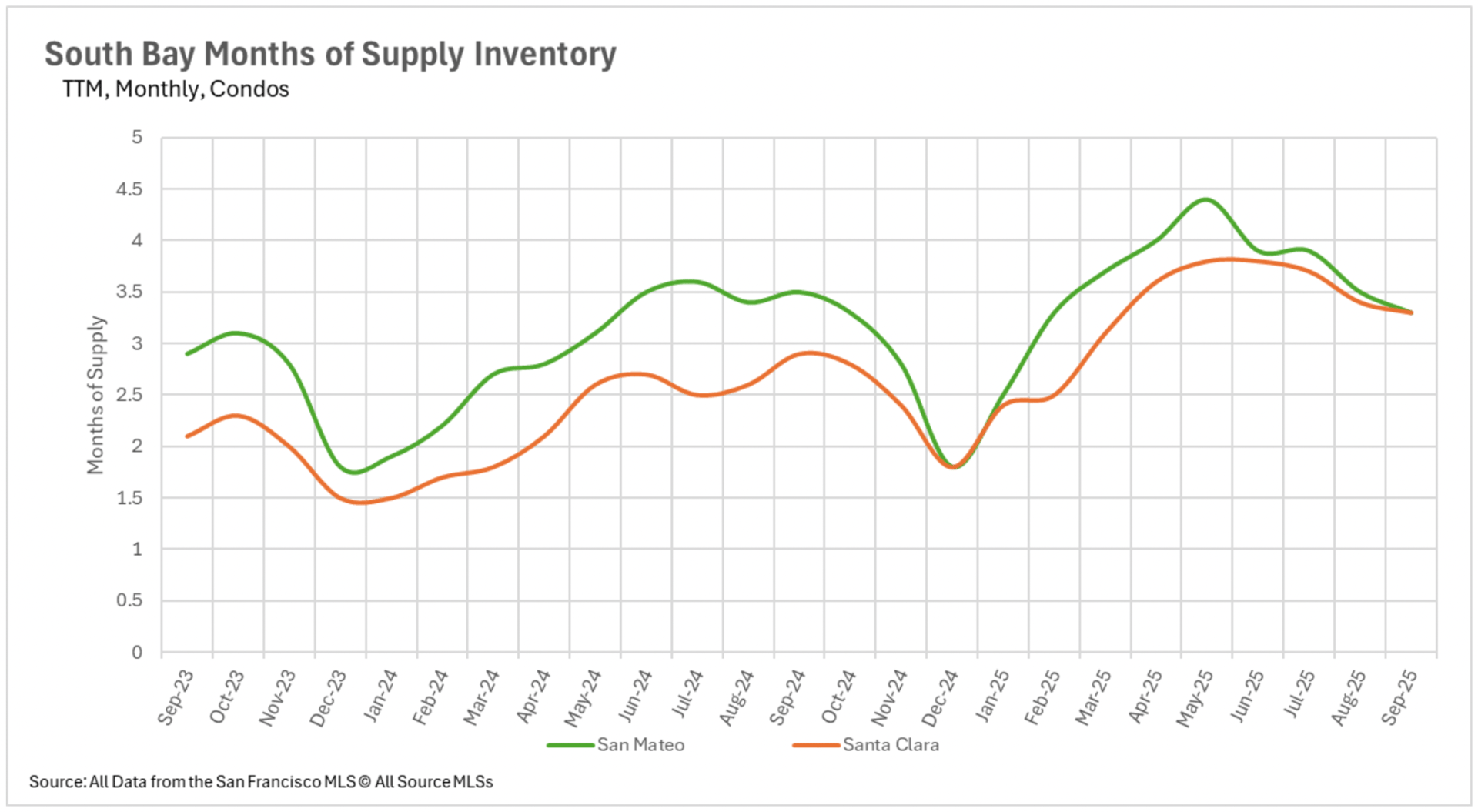

September's availability stabilization accelerated the Bay Area's transition toward seller-favorable markets, with certain regions achieving extraordinary levels of seller advantage. San Francisco's single-family sector remained decisively in seller territory at 1.5 months of supply, while the condominium sector neared seller status at just 3.2 months - the closest position in recent memory. Silicon Valley preserved its exceptionally competitive single-family position with San Mateo at 1.7 months and Santa Clara at an extraordinarily minimal 1.4 months, while Santa Cruz maintained a buyer-favorable market at 3.9 months. All Silicon Valley condominium markets support buyers with 3.3 months in San Mateo and Santa Clara, and 5.7 months in Santa Cruz. East Bay markets maintained their conventional division with single-family properties supporting sellers at 2.1 months in Alameda and 2.6 months in Contra Costa, while condominiums remained buyer-advantageous at 5.0 and 4.0 months, respectively.

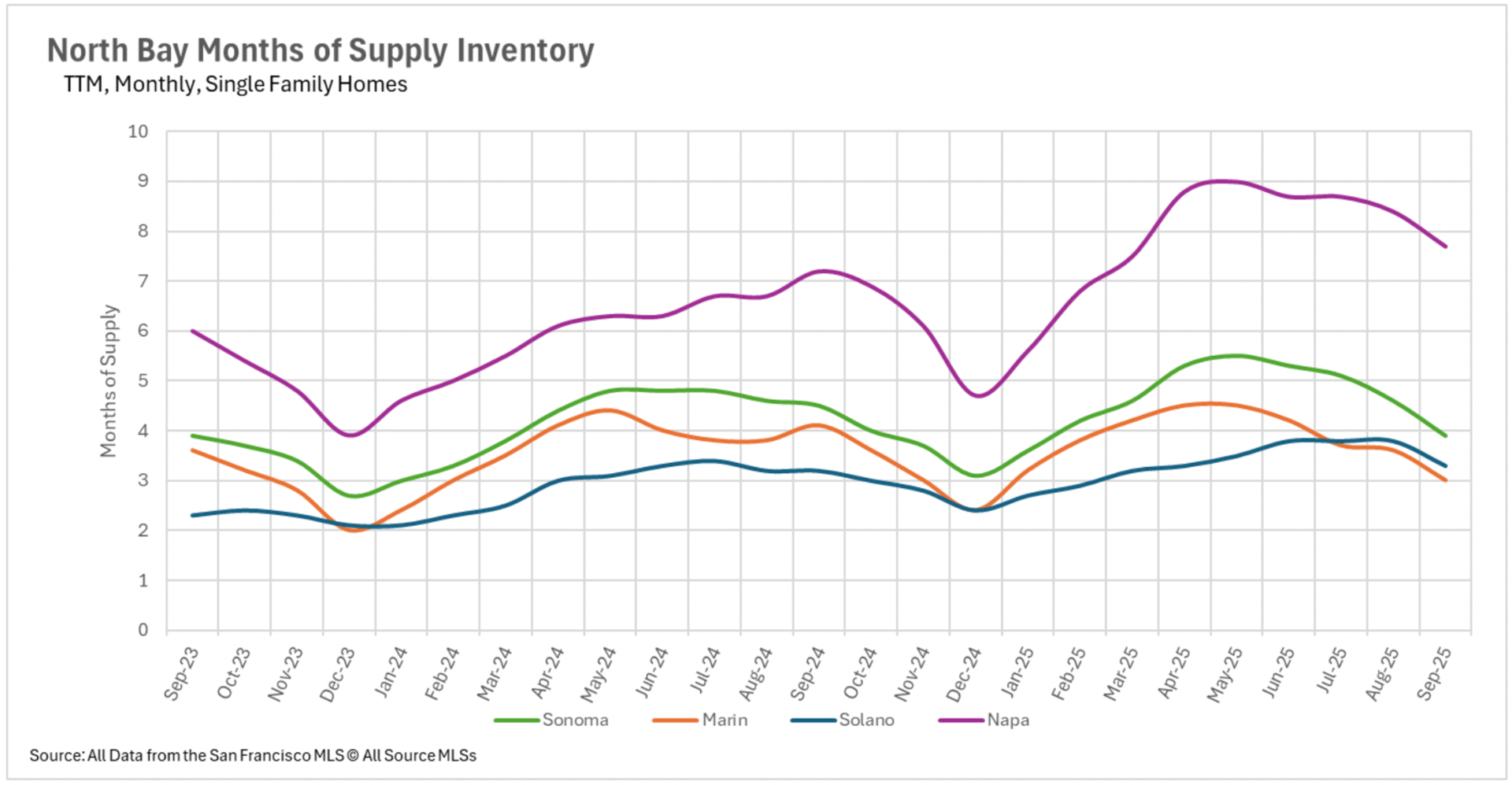

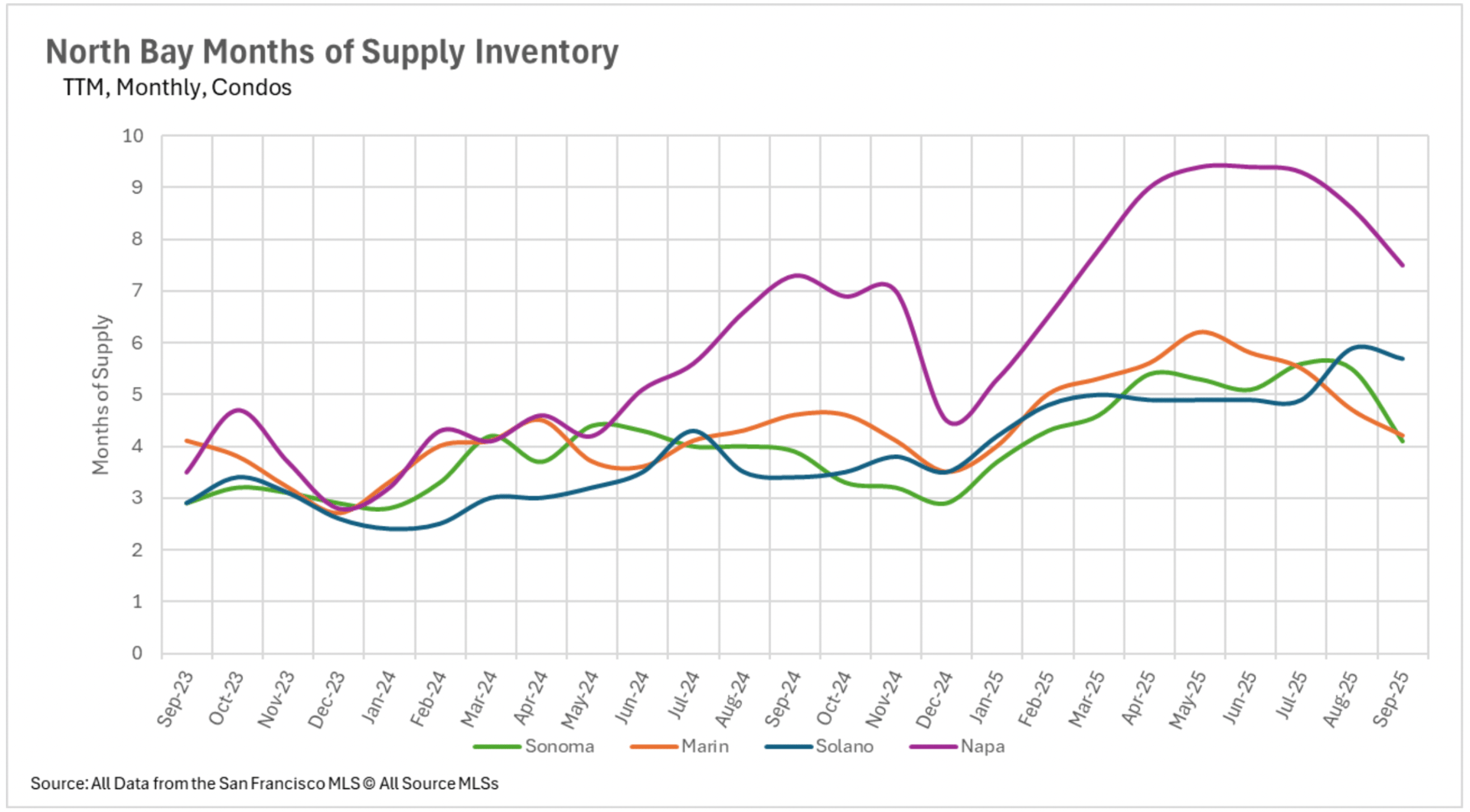

North Bay regions demonstrated the most distinct transformation toward balanced and seller-favorable markets, with Marin County establishing perfect equilibrium at precisely 3.0 months for single-family properties, while Sonoma (3.9 months), Solano (3.3 months), and Napa (7.7 months) continue progressing toward balance from buyer-favorable territory. North Bay condominiums remain entirely in buyer-favorable territory but are gradually transitioning toward balance, with supply spanning from 4.1 months in Sonoma to 7.5 months in Napa County. This regionwide configuration indicates that as the conventional autumn season advances, seller positioning is strengthening throughout most Bay Area markets.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

April 24, 2026

April 18, 2026

April 17, 2026

April 11, 2026

March 21, 2026

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

You've got questions and we can't wait to answer them.