September Market Update

August represented a pivotal moment for Bay Area residential markets, with single-family property values recovering across most regions while condominium sectors continue experiencing instability and value erosion.

Supply conditions are stabilizing regionwide following summer highs, with San Francisco achieving historically minimal availability while other markets maintain elevated annual comparisons.

Even with supply stabilization, properties are demanding considerably longer sales cycles throughout the majority of Bay Area markets, indicating heightened buyer discrimination.

Market conditions heavily favor single-family properties versus condominiums, with San Francisco establishing dual seller advantages while other regions sustain traditional property-type divisions.

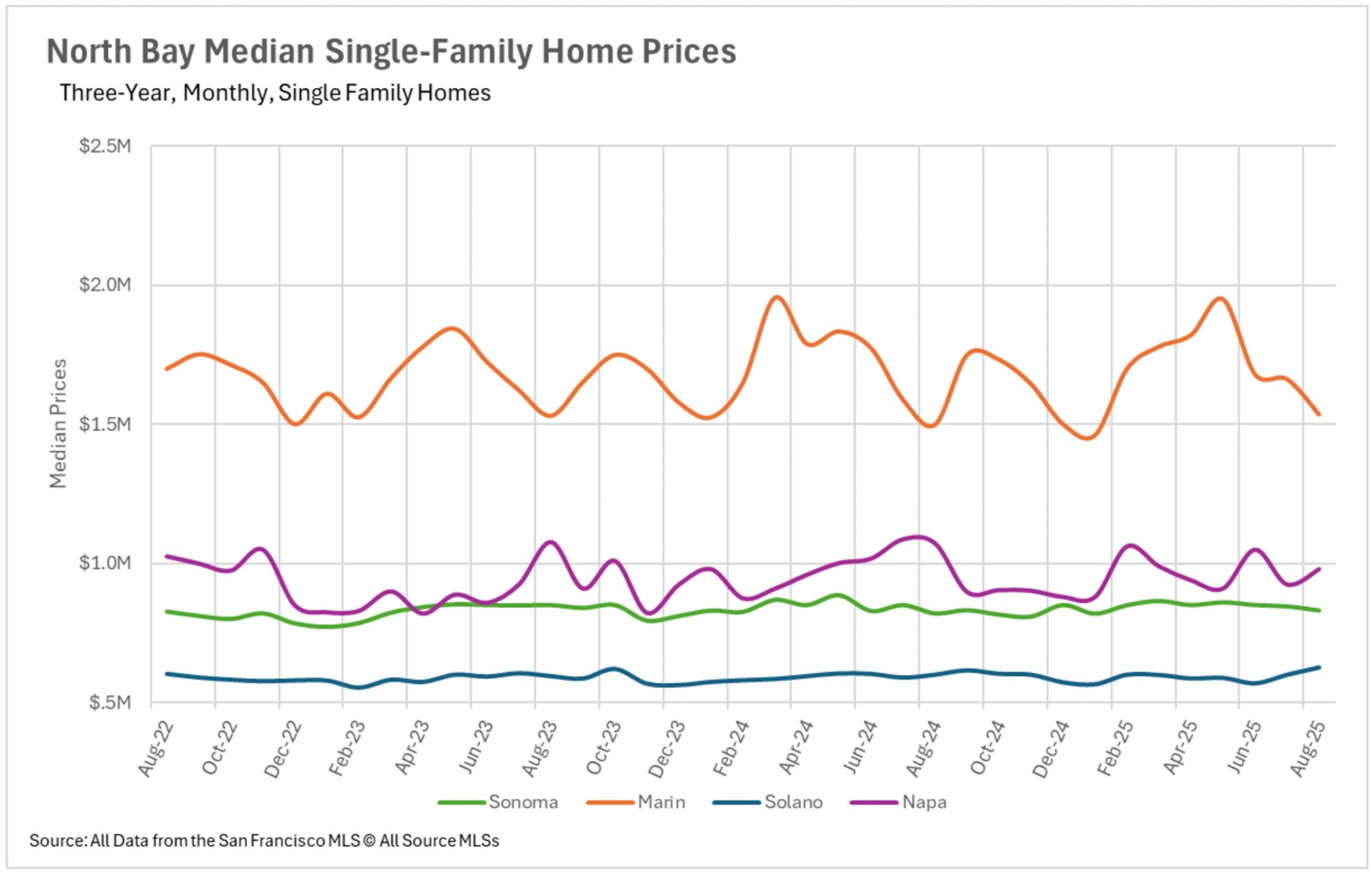

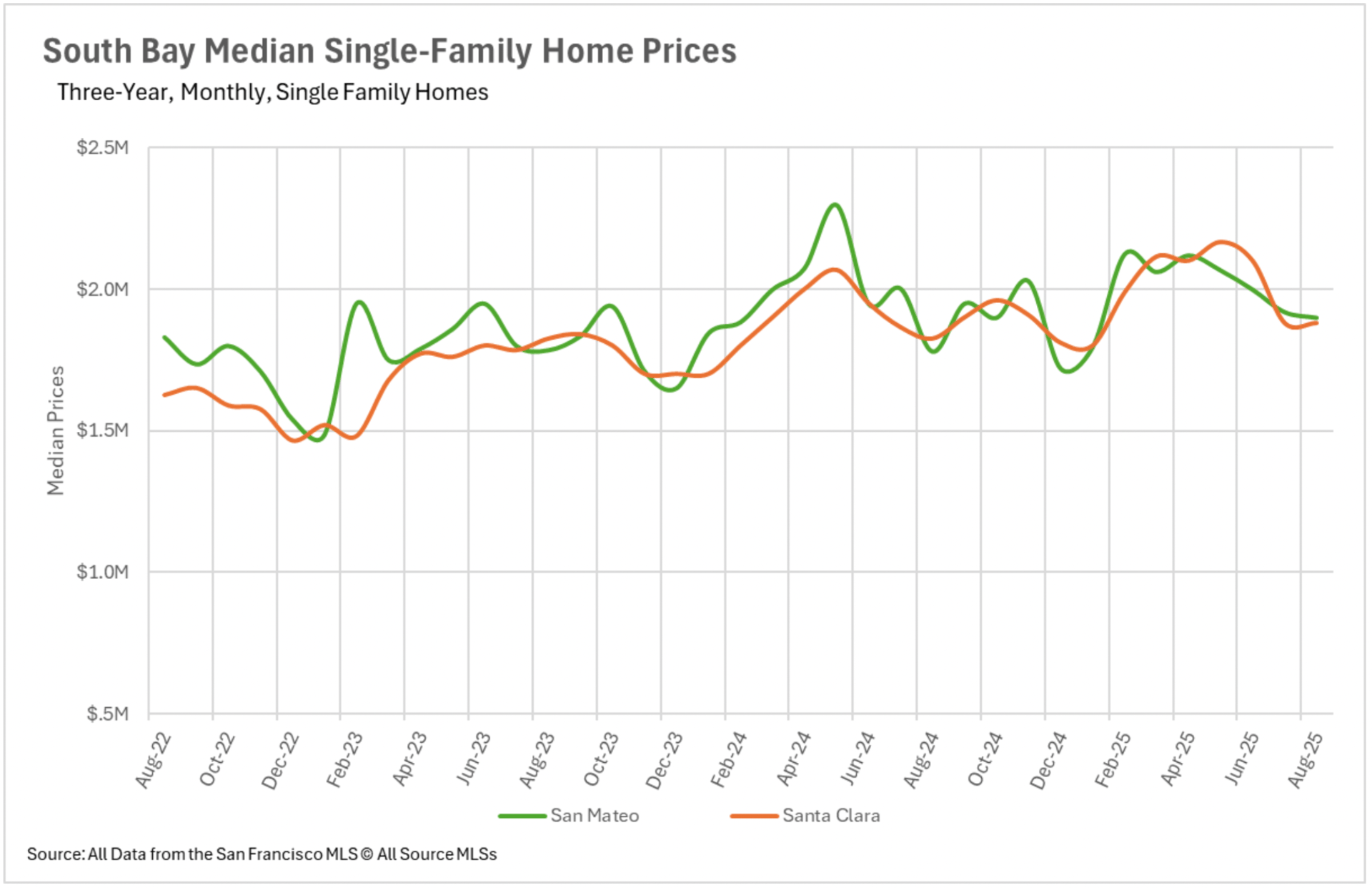

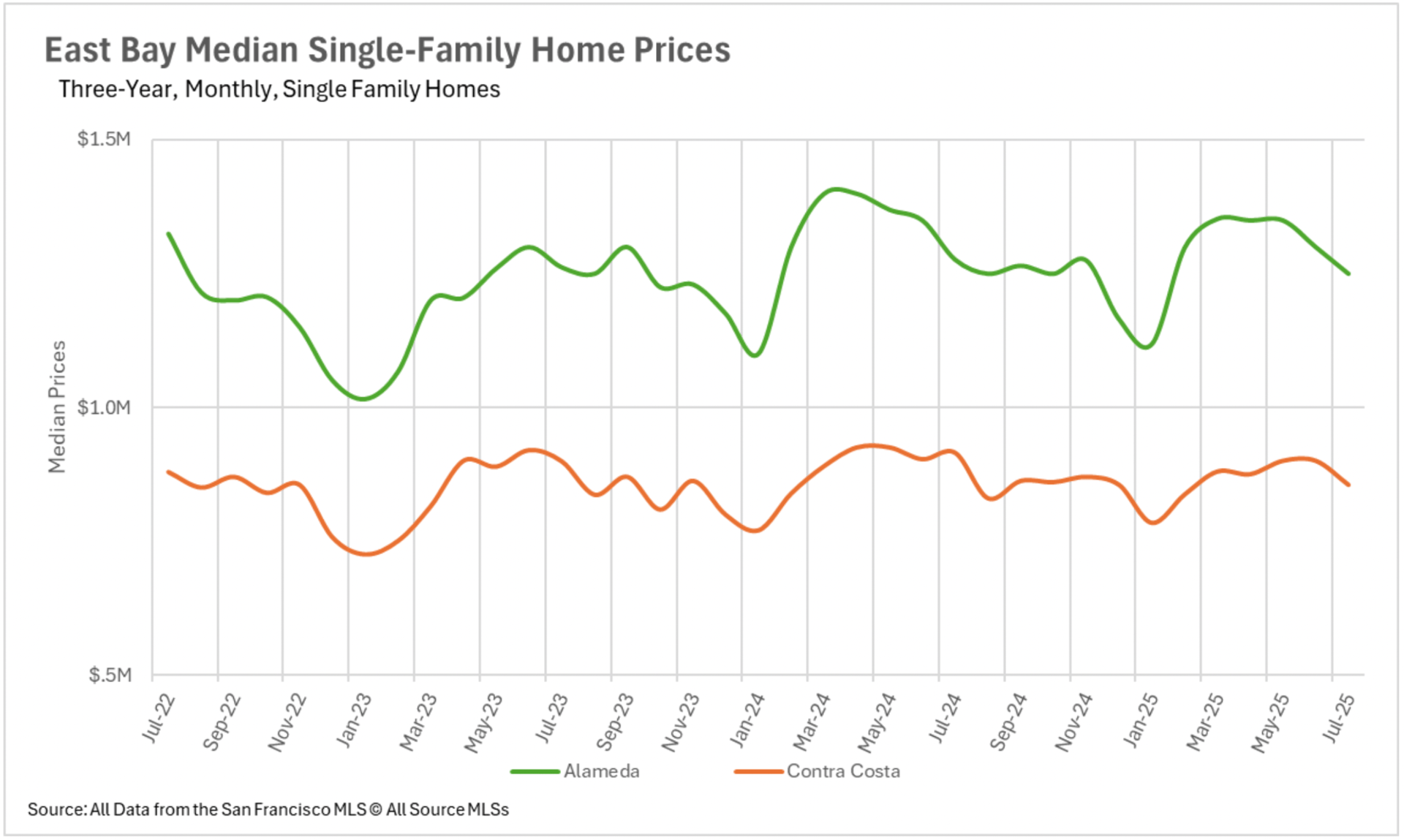

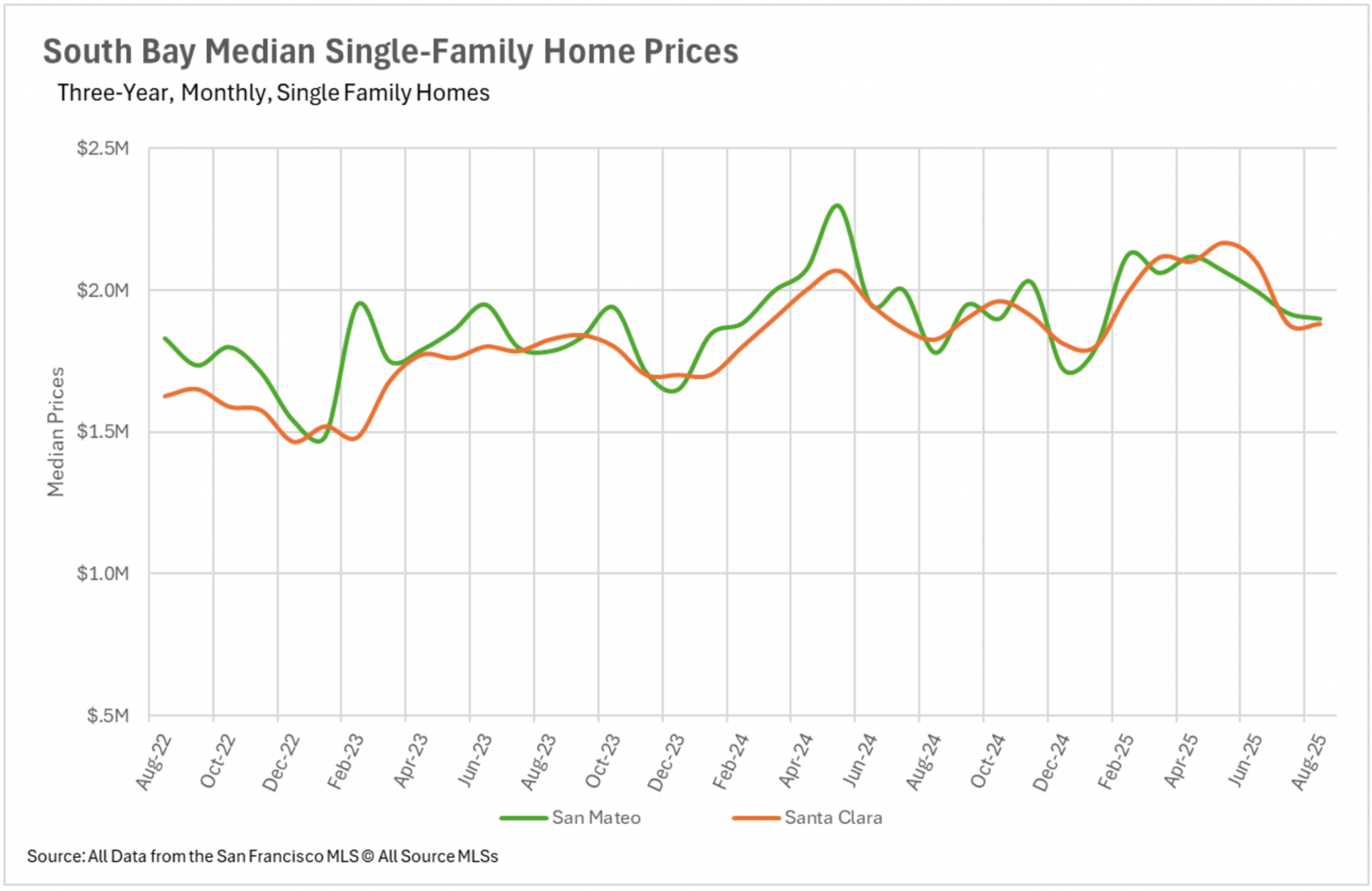

August demonstrated a significant reversal for Bay Area single-family residential markets following months of uncertainty. Silicon Valley spearheaded the resurgence with value gains throughout all counties for the initial time in four months - San Mateo County jumped 6.74%, Santa Cruz advanced 5.54%, and Santa Clara climbed 3.01% annually. East Bay markets also achieved positive performance for the first time in six months, with Alameda and Contra Costa Counties recording moderate advances of 1.20% and 1.33% respectively. North Bay regions exhibited robust results in most areas, with Solano County advancing 4.17%, Marin County gaining 2.47%, and Sonoma County increasing 1.29%, although Napa County recorded a substantial 8.67% retreat.

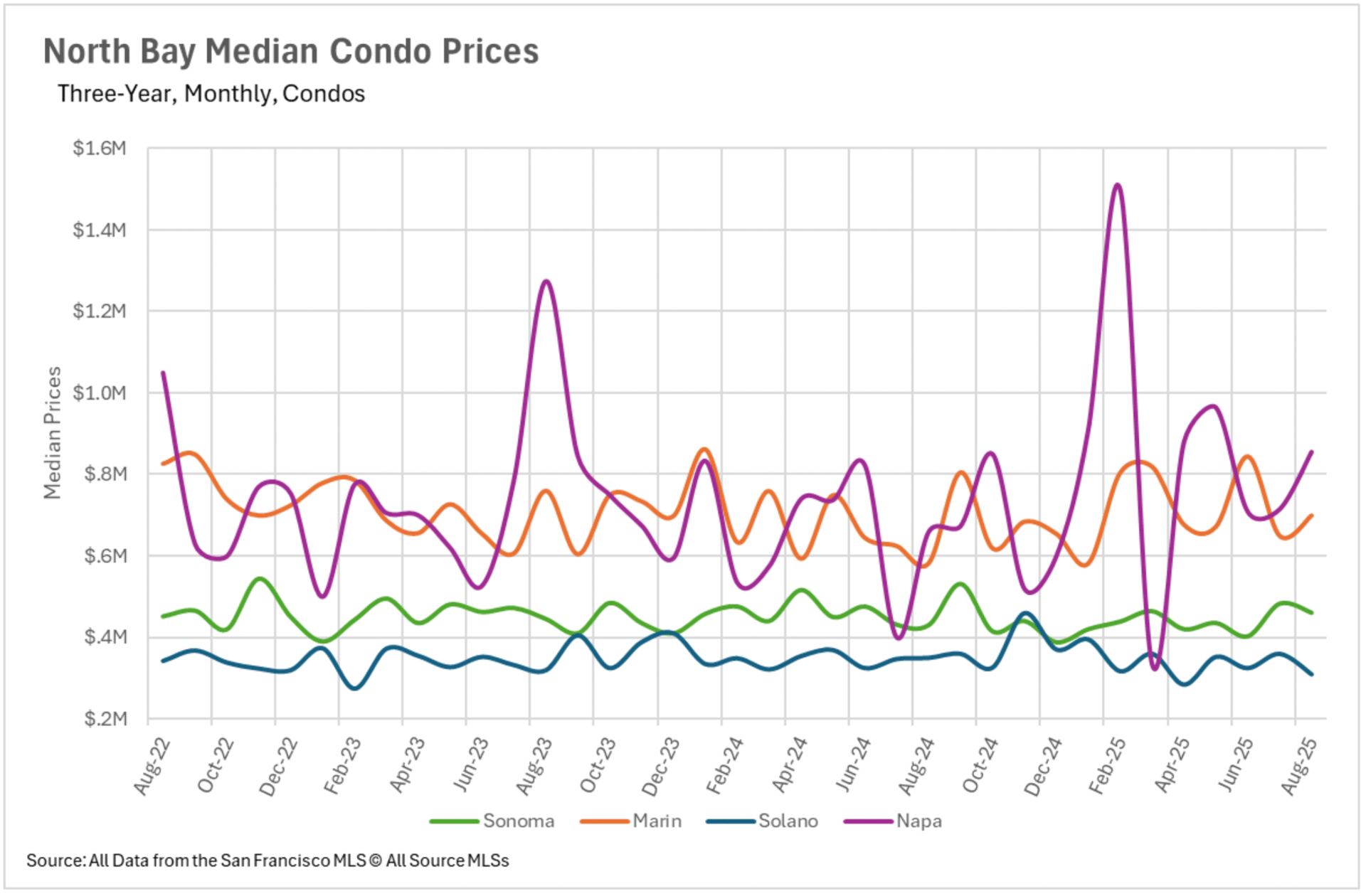

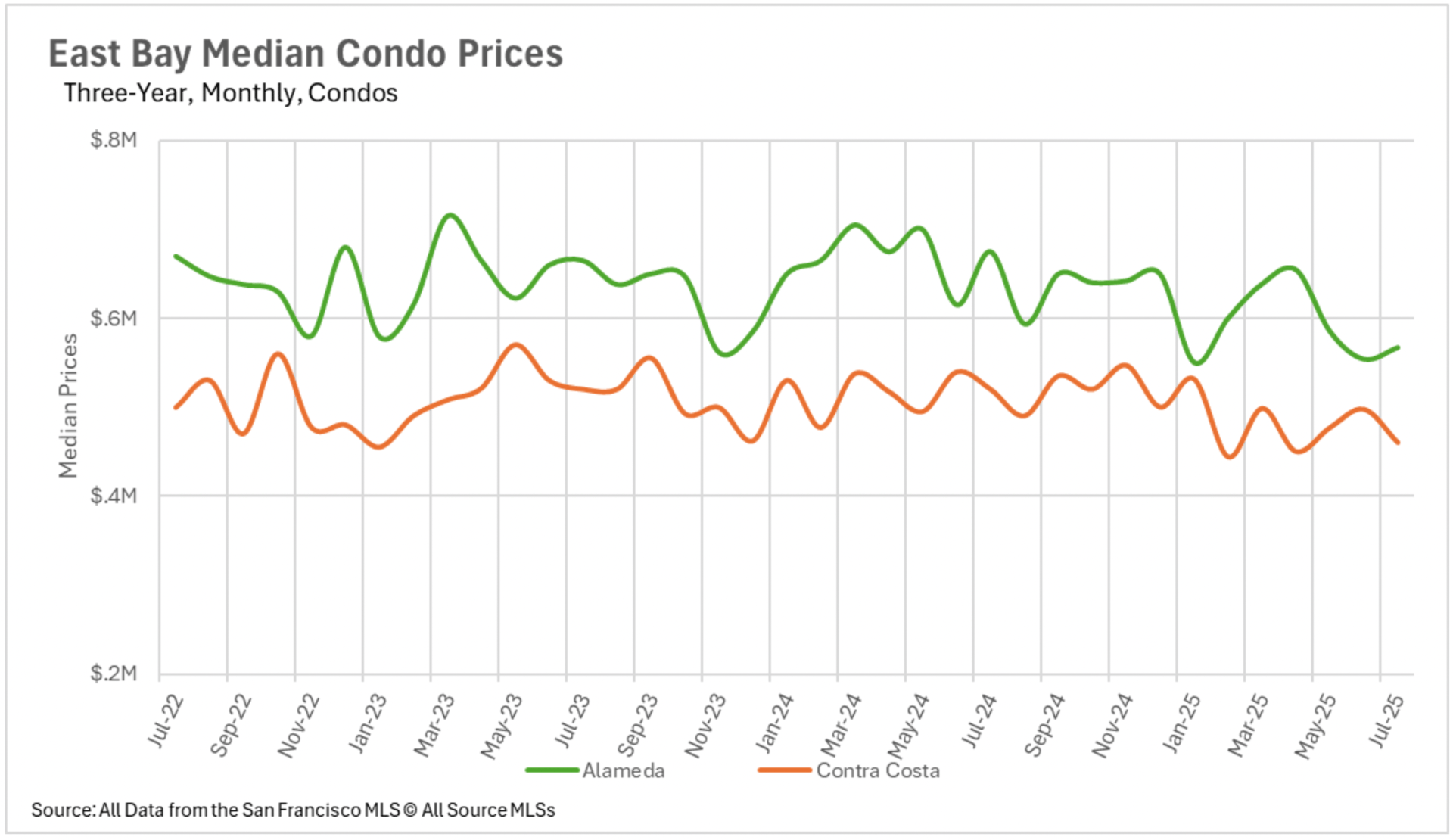

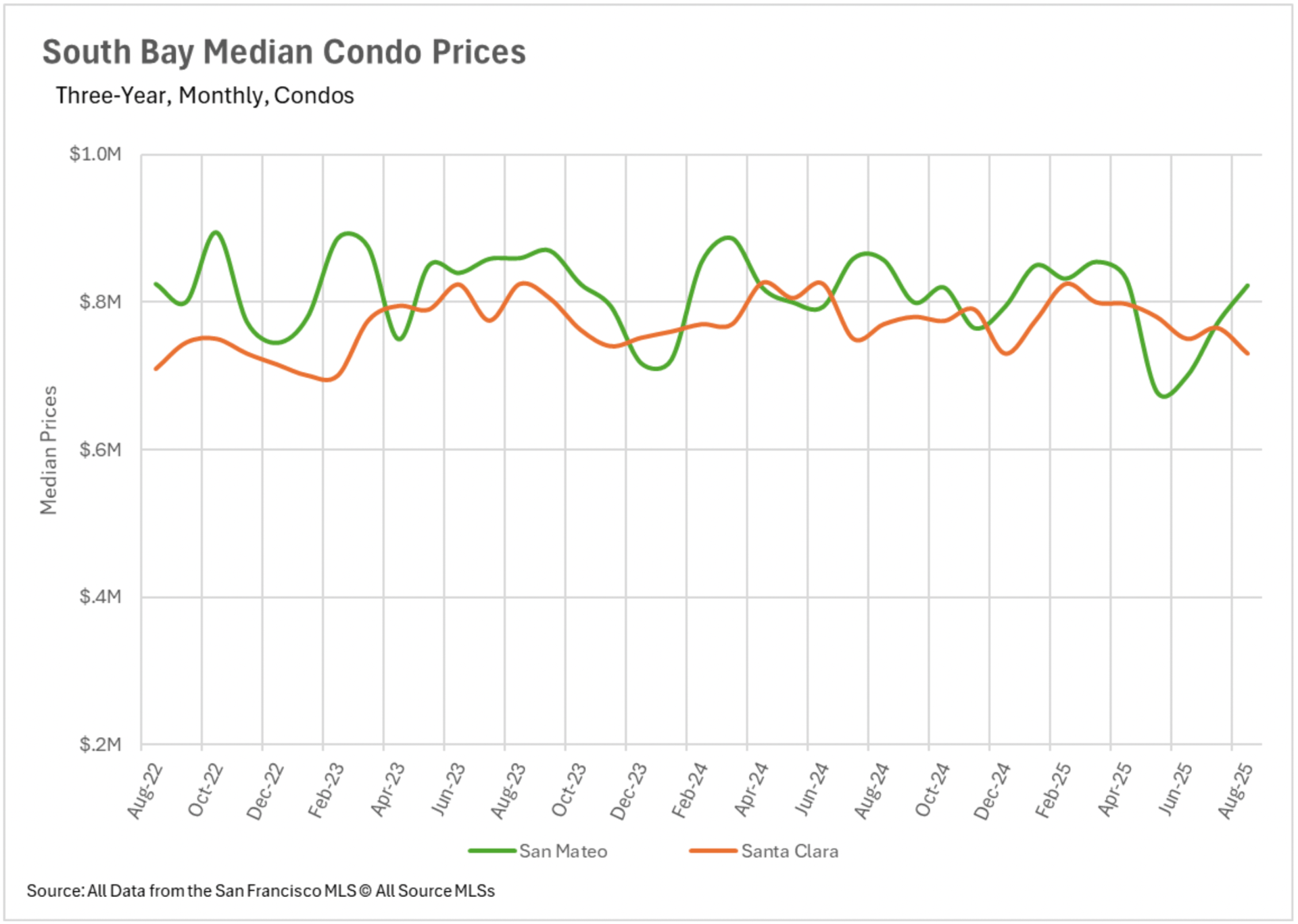

San Francisco demonstrated atypical steadiness with single-family properties declining merely 1.38% and condominiums rising a moderate 0.74% - a notable departure from its characteristic fluctuation. However, condominium markets throughout the region persisted in facing challenges, with Silicon Valley recording widespread retreats spanning from 3.64% in Santa Cruz to 5.20% in Santa Clara County. East Bay condominium conditions remained inconsistent, with Contra Costa County advancing 2.04% while Alameda County declined 7.41%. North Bay condominiums displayed exceptional fluctuation, with substantial increases in Napa (29.76%), Marin (20.07%), and Sonoma (6.98%) Counties, while Solano County retreated 11.43%.

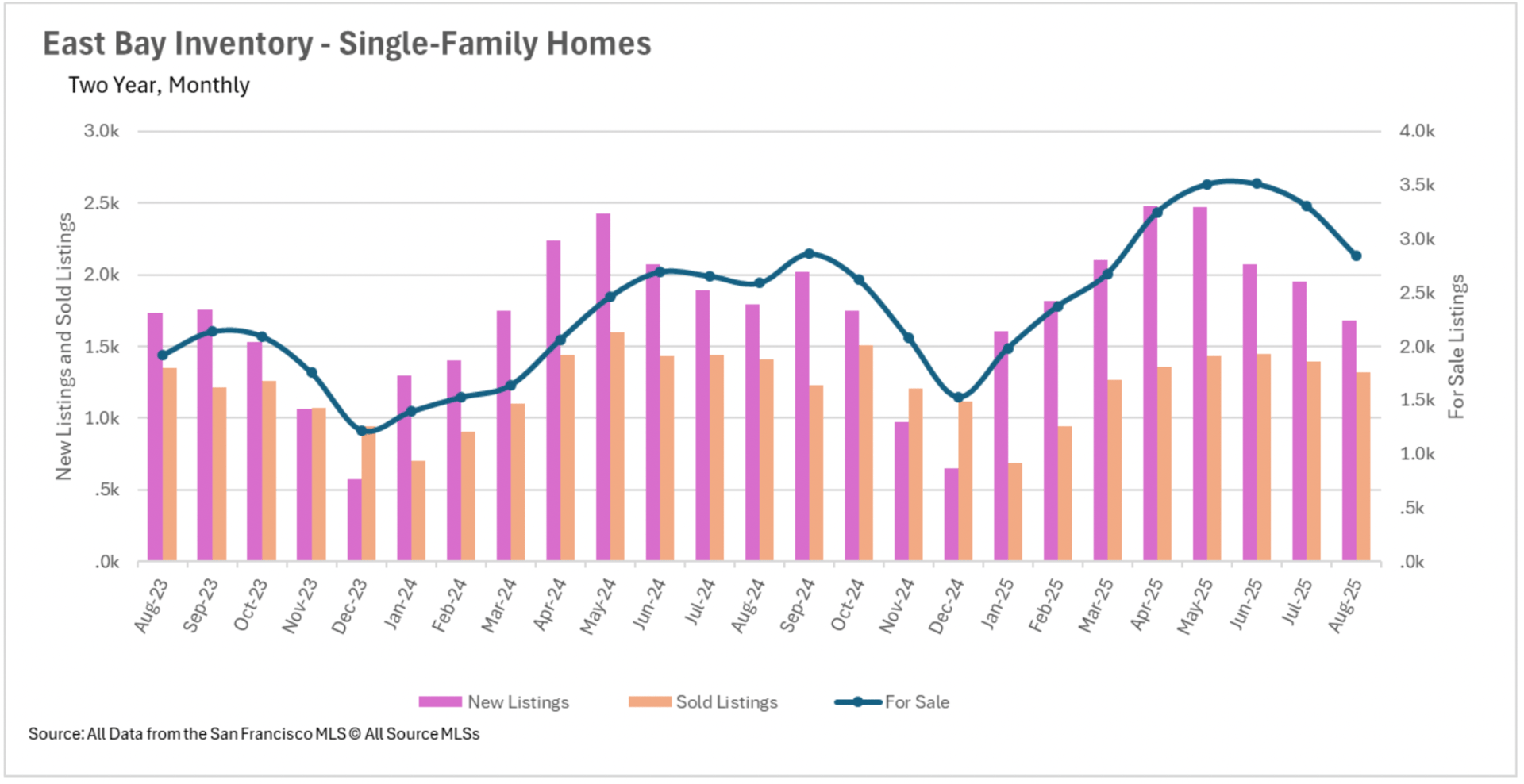

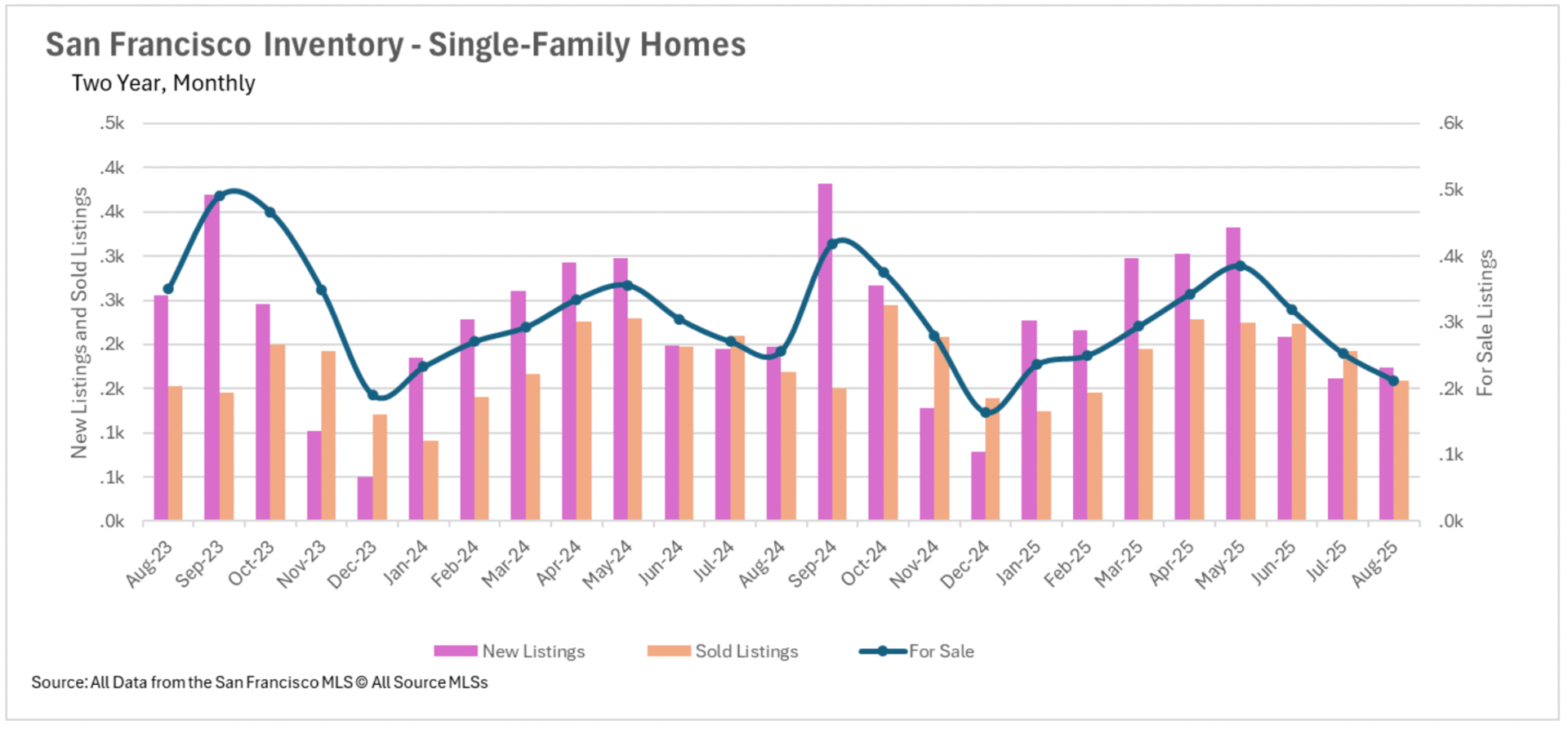

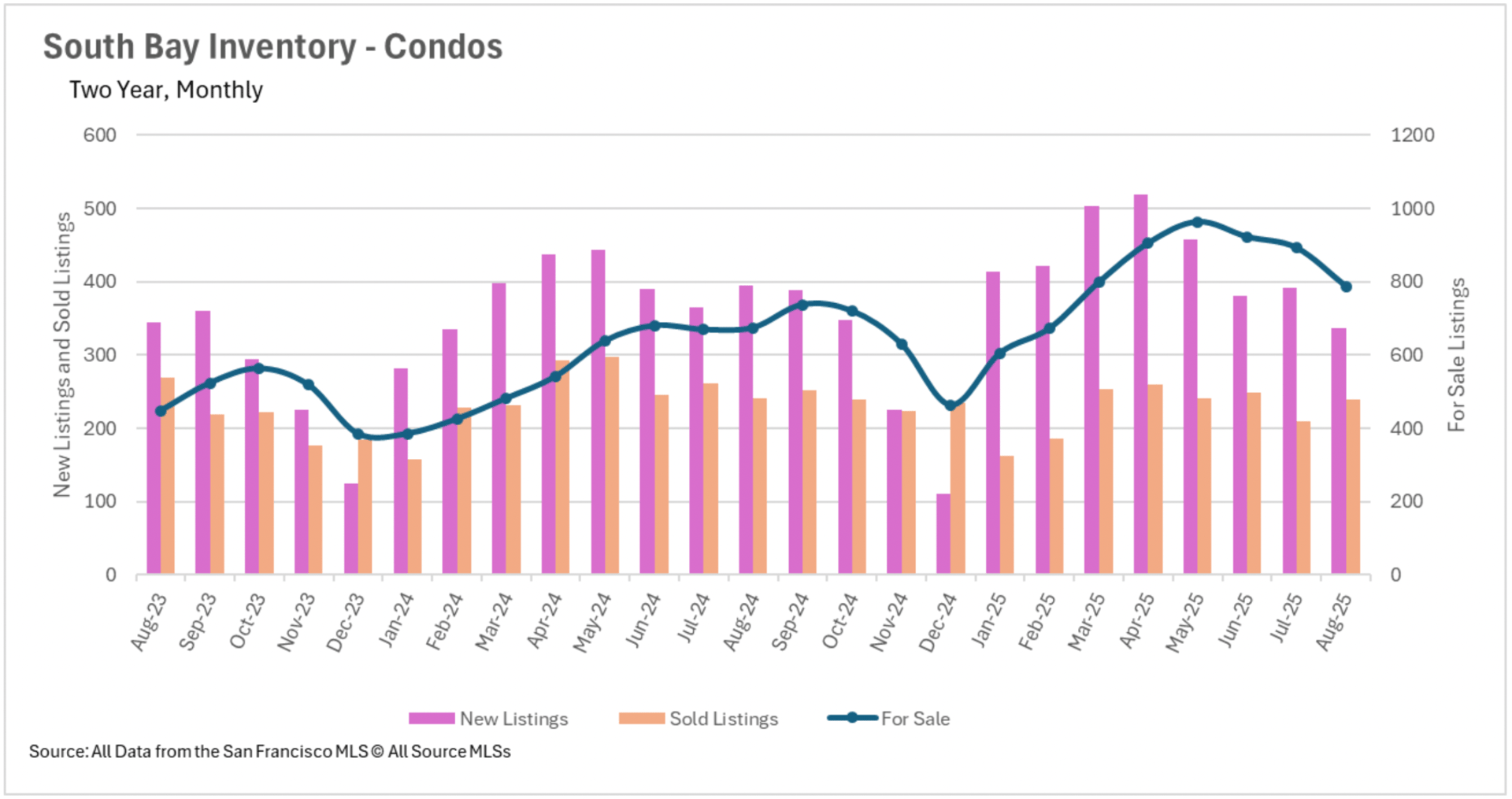

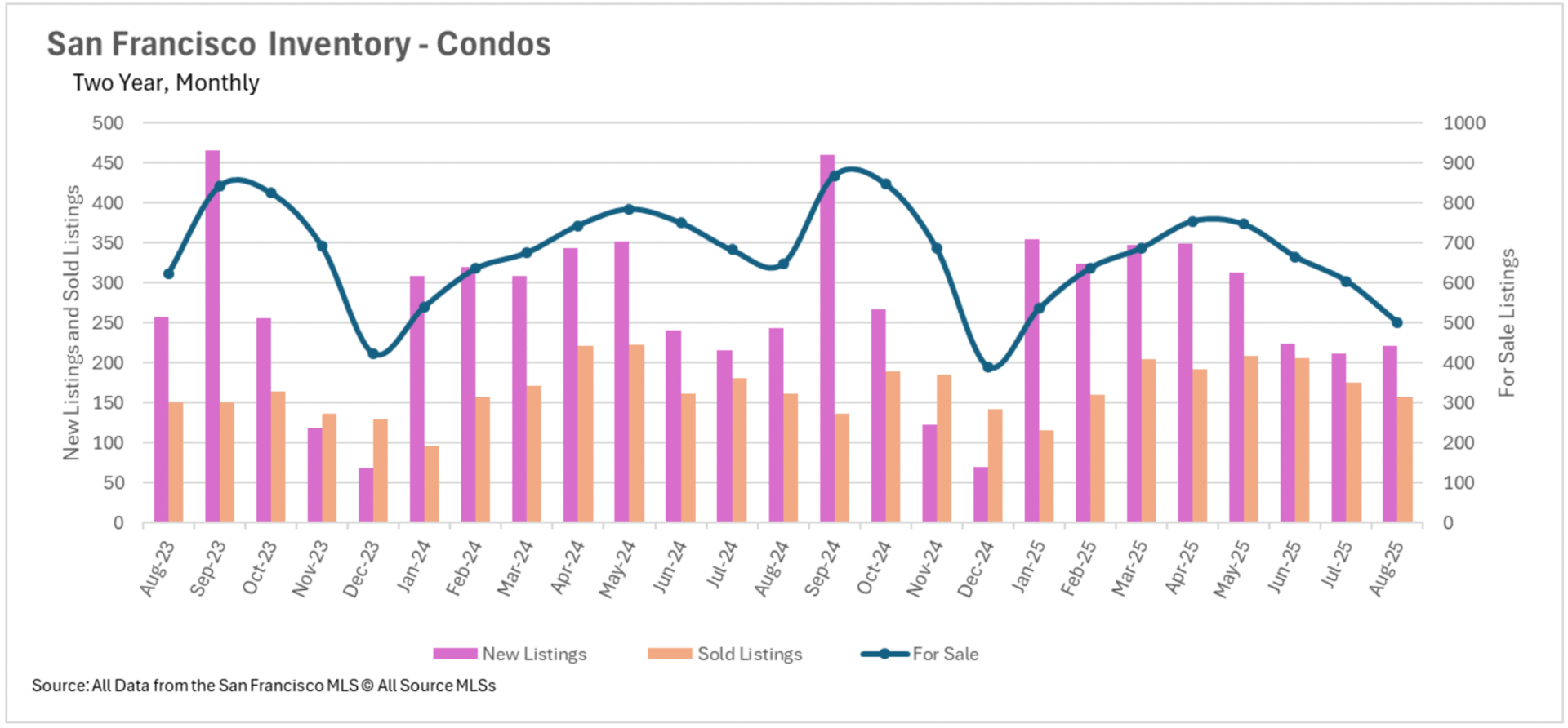

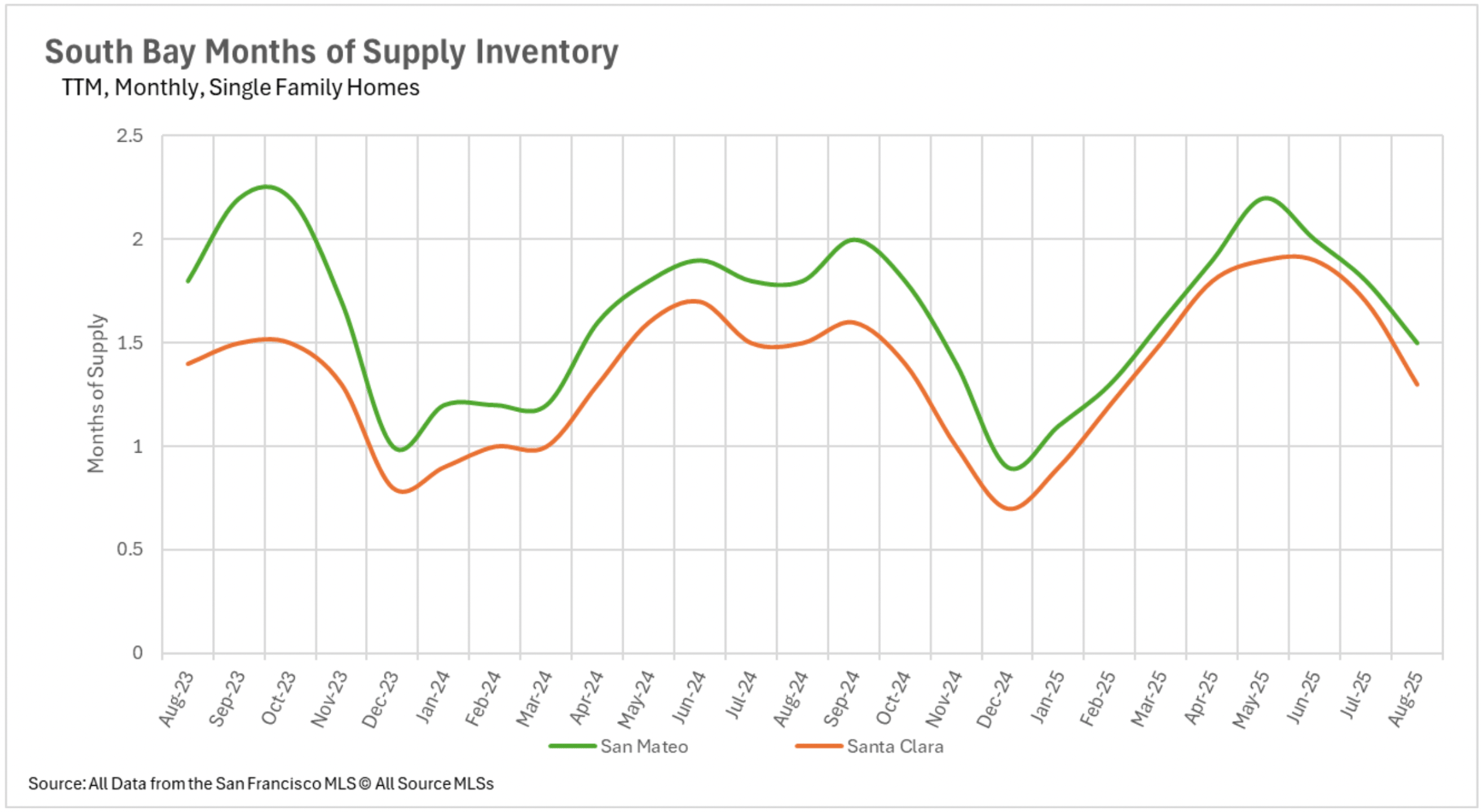

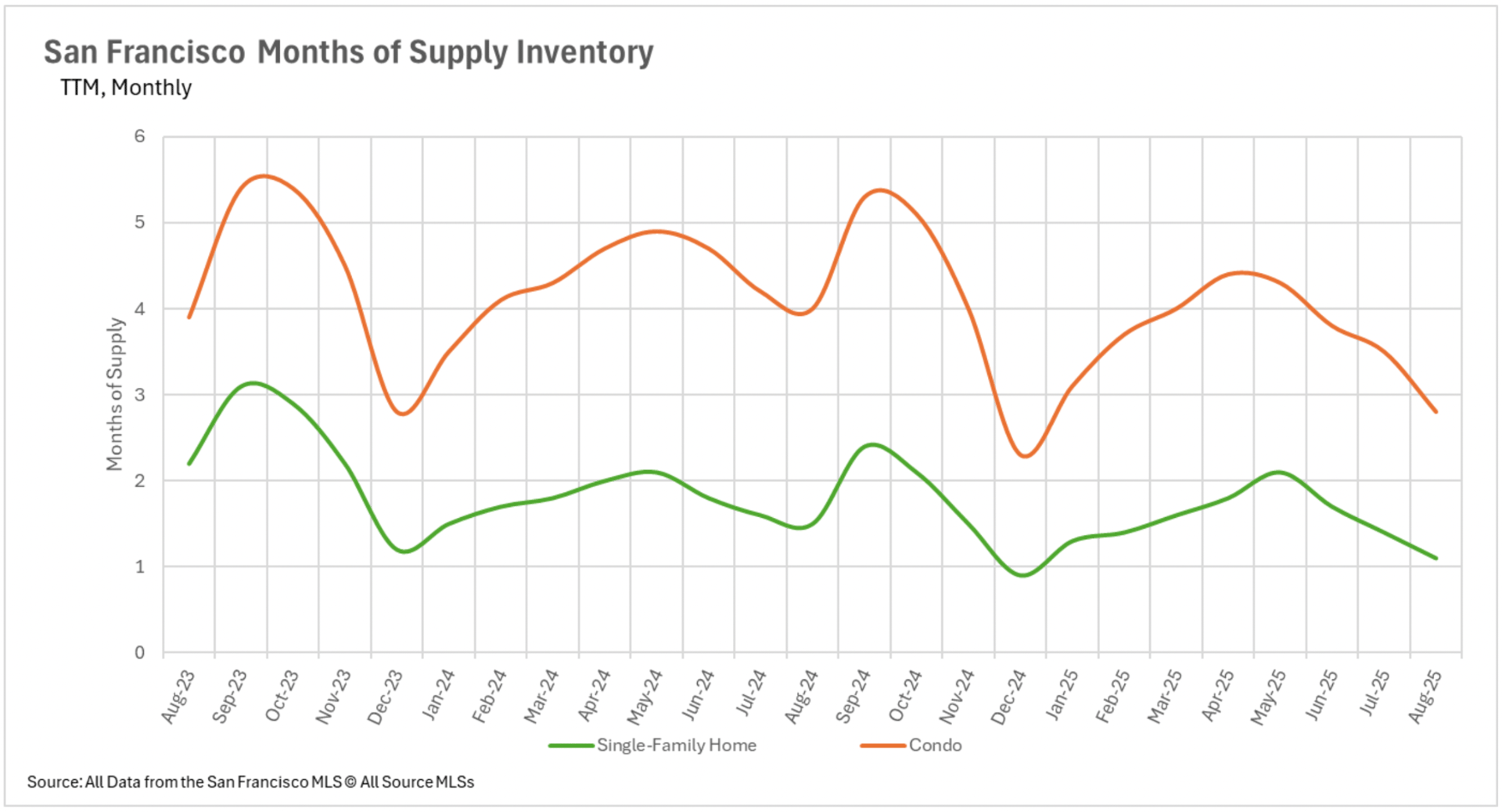

August signaled a substantial transition in Bay Area availability patterns, with most regions advancing the stabilization trend that commenced during summer months. San Francisco entered extraordinary territory with both single-family properties and condominiums attaining seller-favorable status - single-family availability contracted to merely 1.1 months of supply while condominiums decreased to 2.8 months, establishing the minimal levels ever documented in the region. Single-family availability declined 17.51% annually, while condominium supply dropped 22.69%.

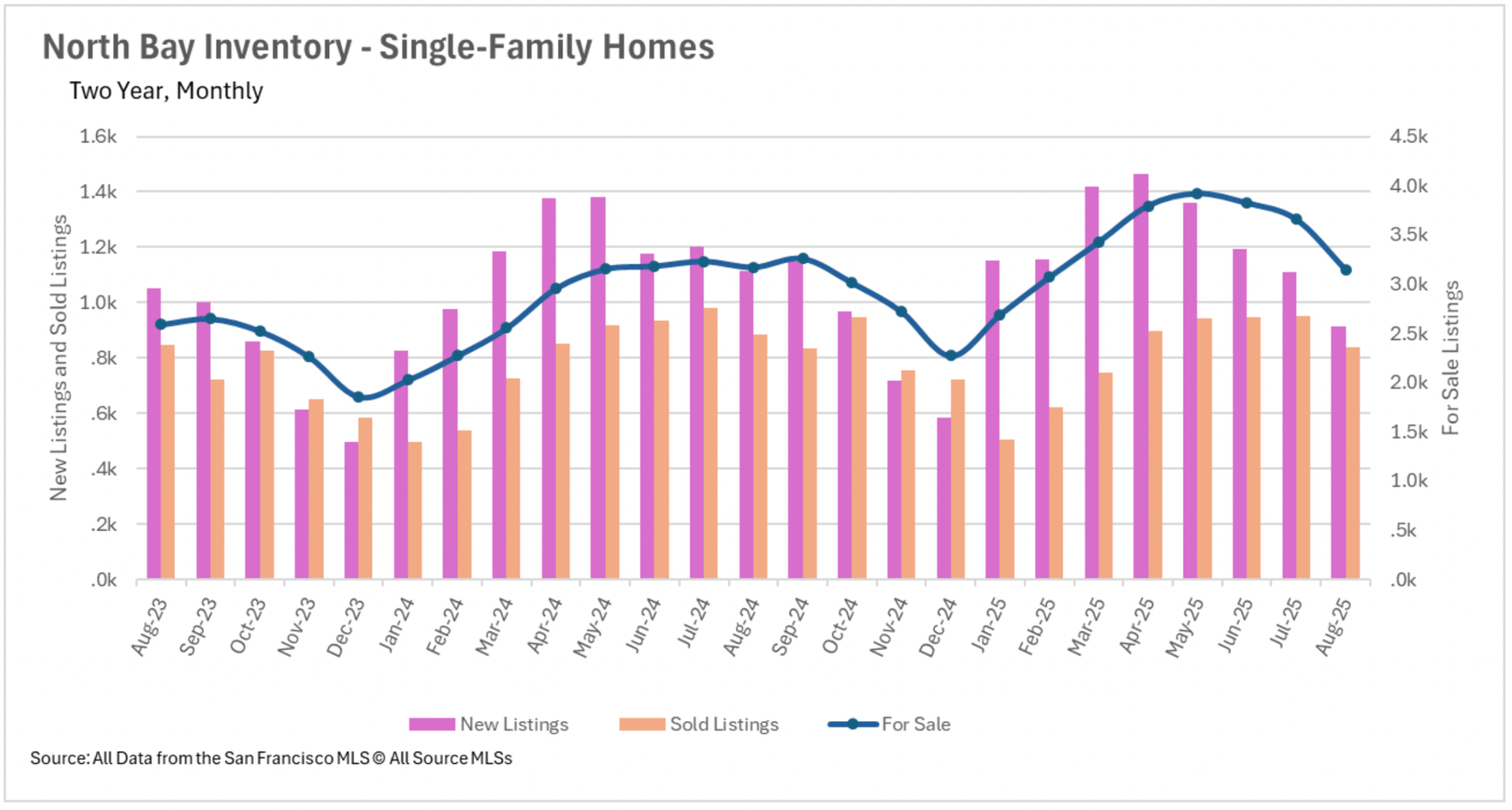

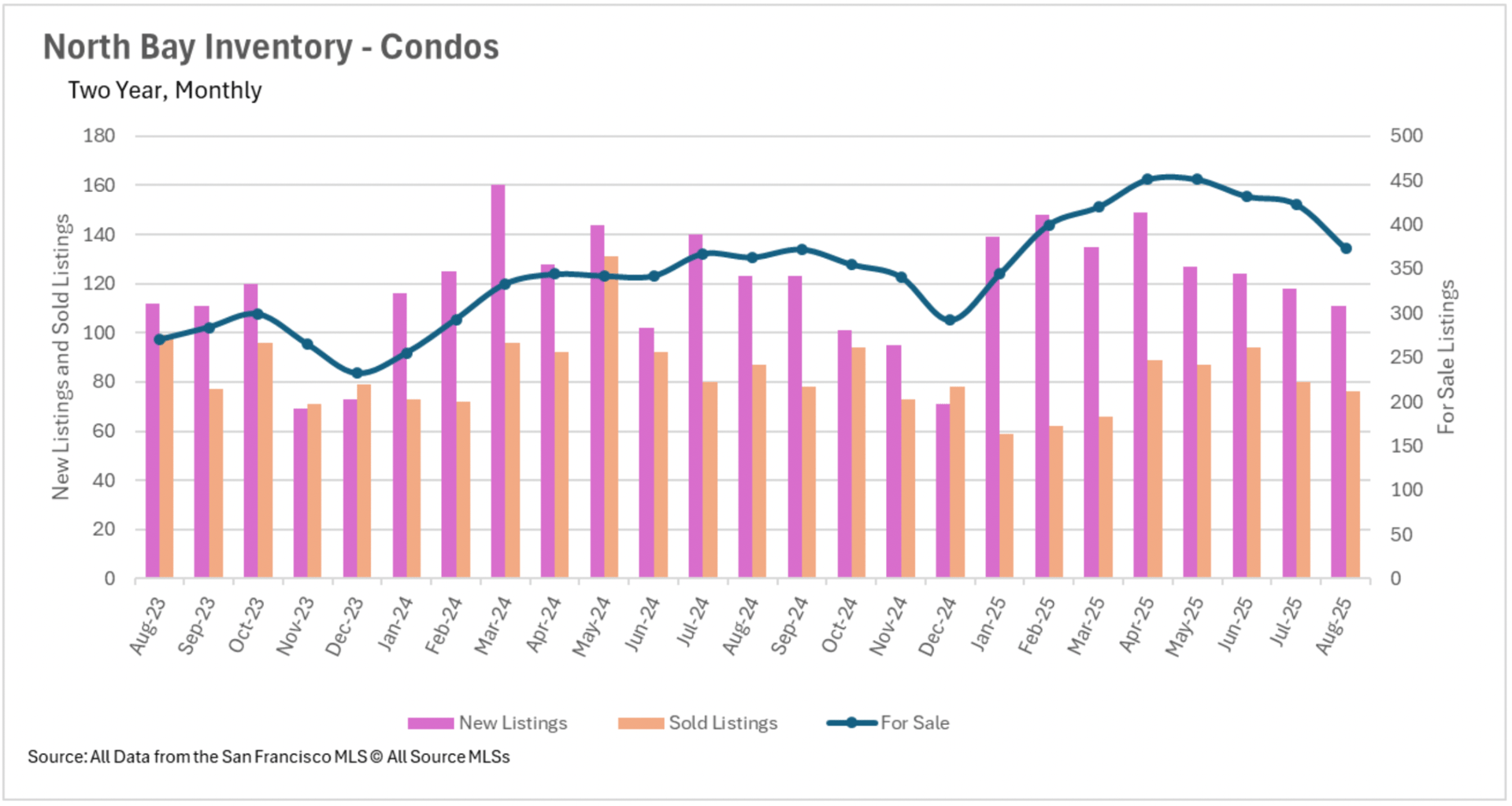

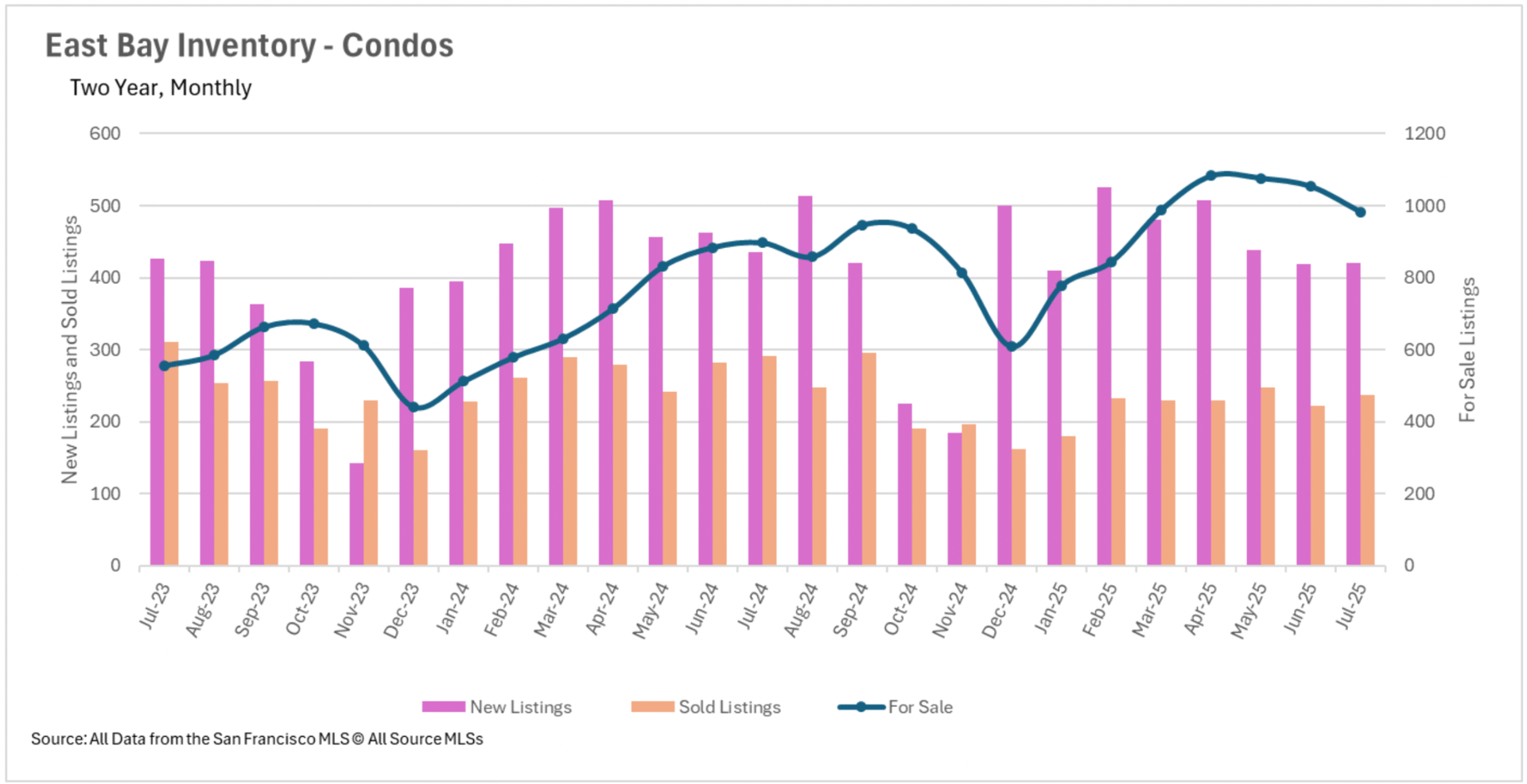

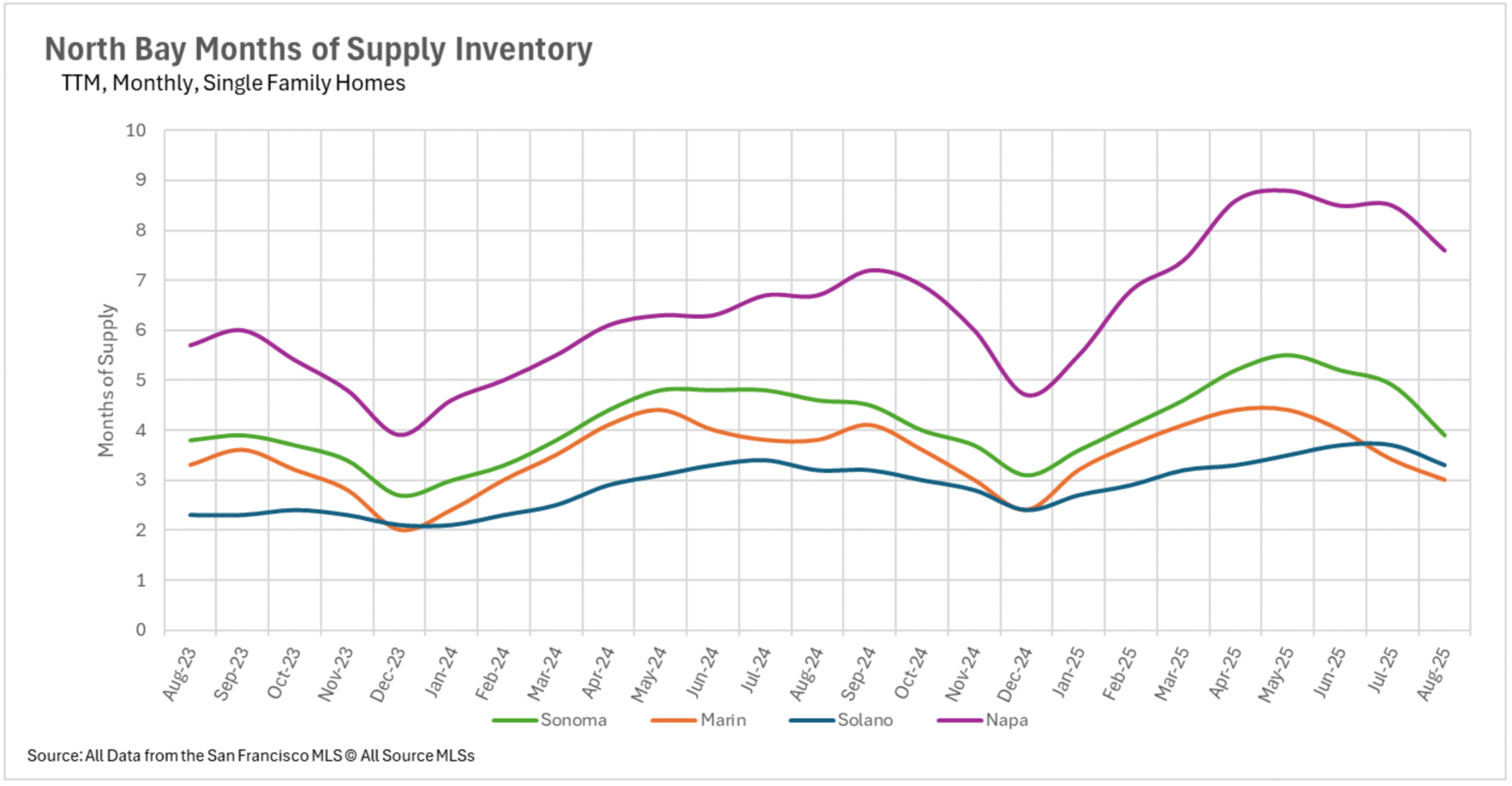

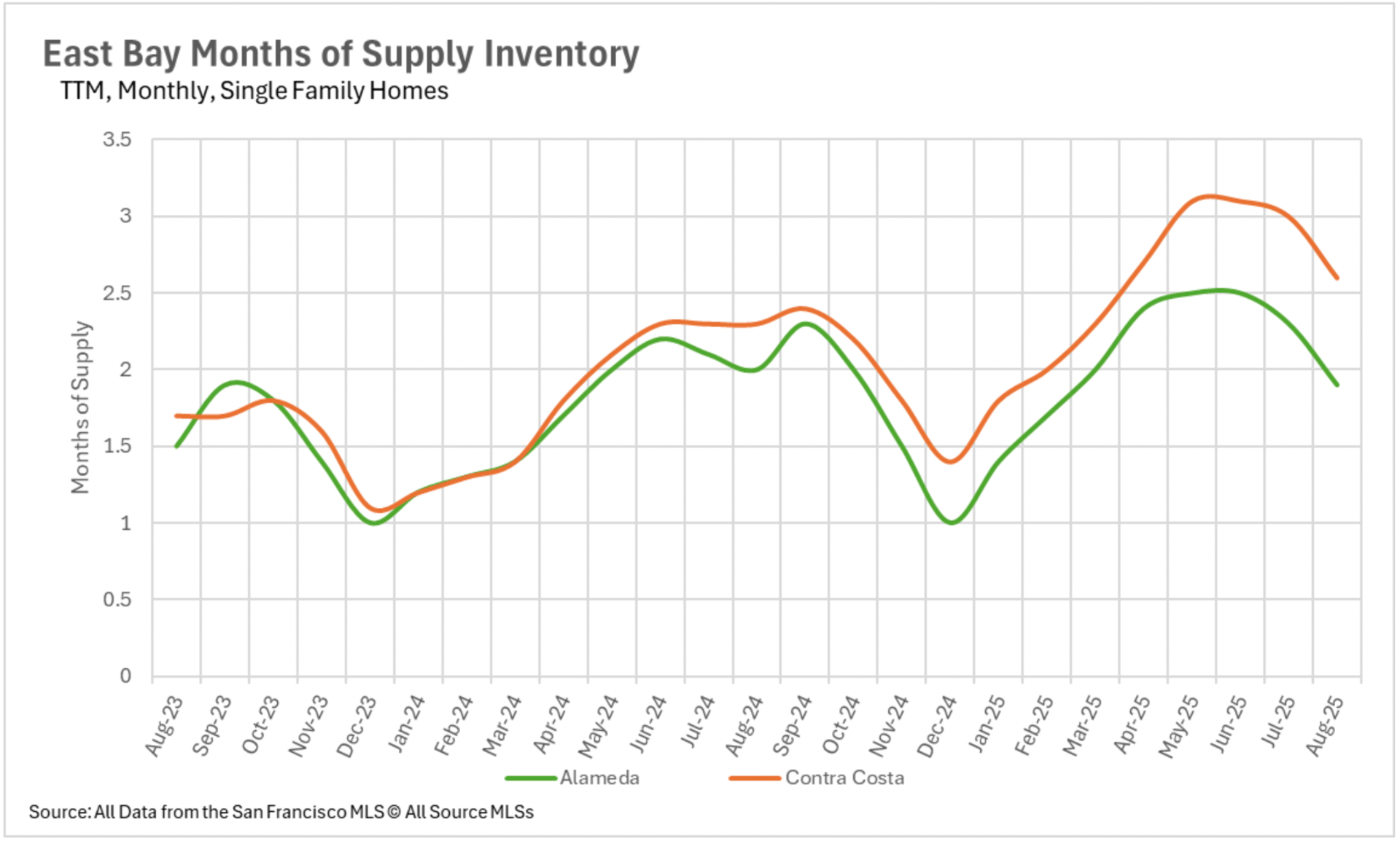

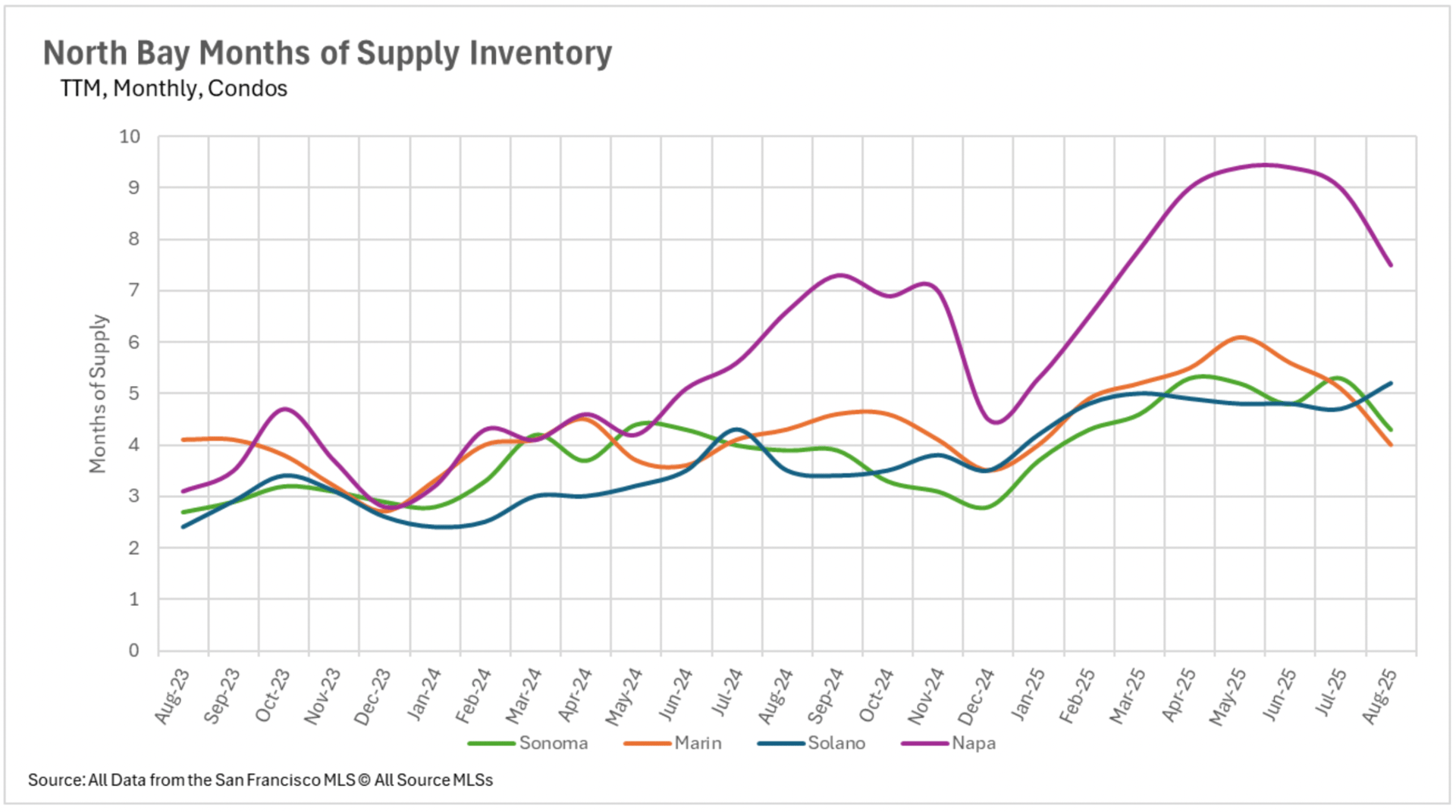

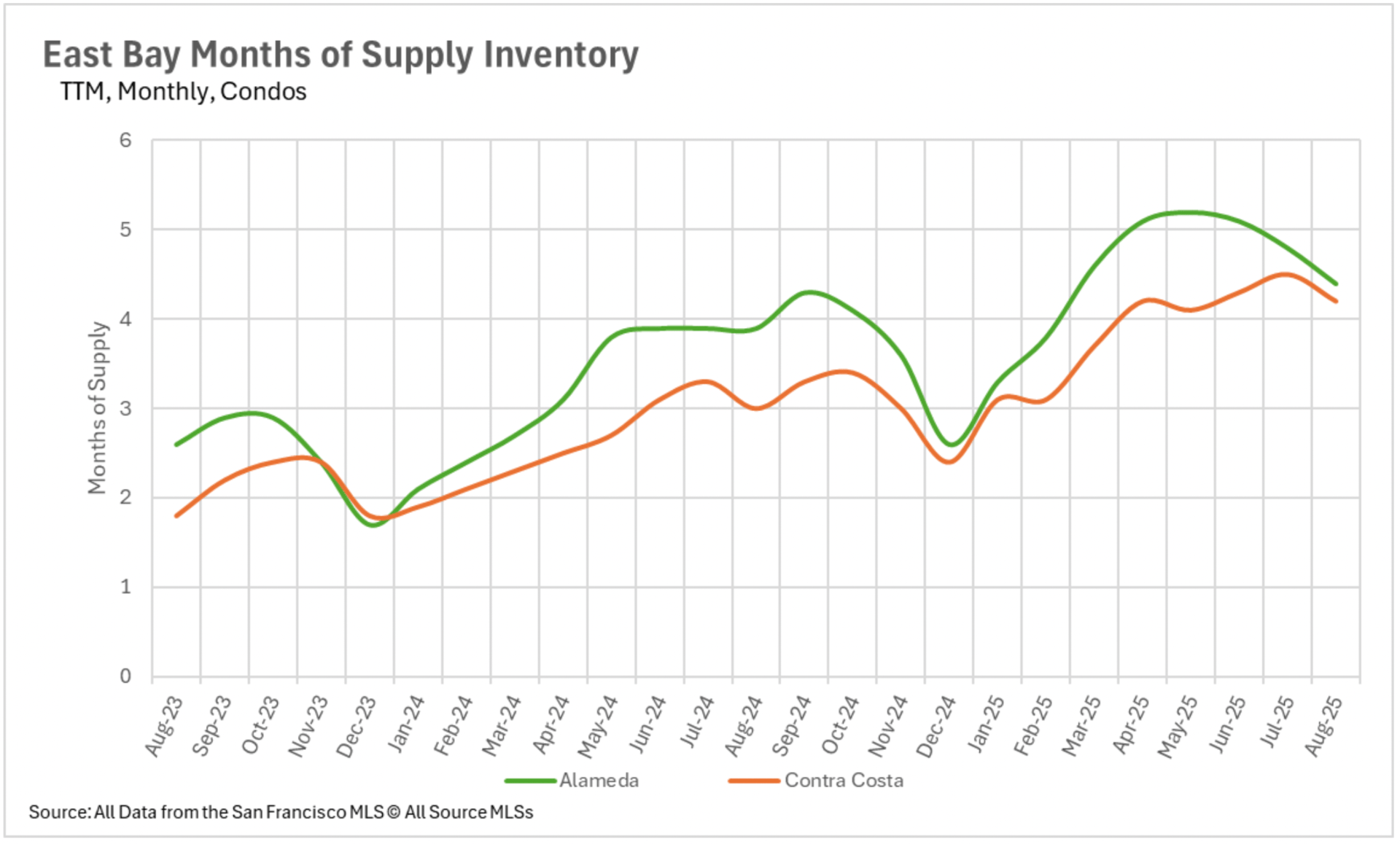

Silicon Valley executed a substantial turnaround, with single-family property availability actually declining 4.04% below previous year levels for the initial time in months, although condominium availability remained elevated at 16.77% above last year's levels - still a meaningful improvement from earlier months. North Bay regions displayed the most balanced availability scenario, with single-family properties declining just 0.73% annually and condominiums advancing a modest 2.75%, suggesting near-stabilization. East Bay markets, while still elevated, maintained their downward progression with single-family availability at 9.97% above last year and condominiums at 11.67% - considerable decreases from peak levels. Notably, most regions recorded reduced new listings entering the market annually, indicating seller reluctance rather than enhanced buyer absorption as the principal factor in availability reductions.

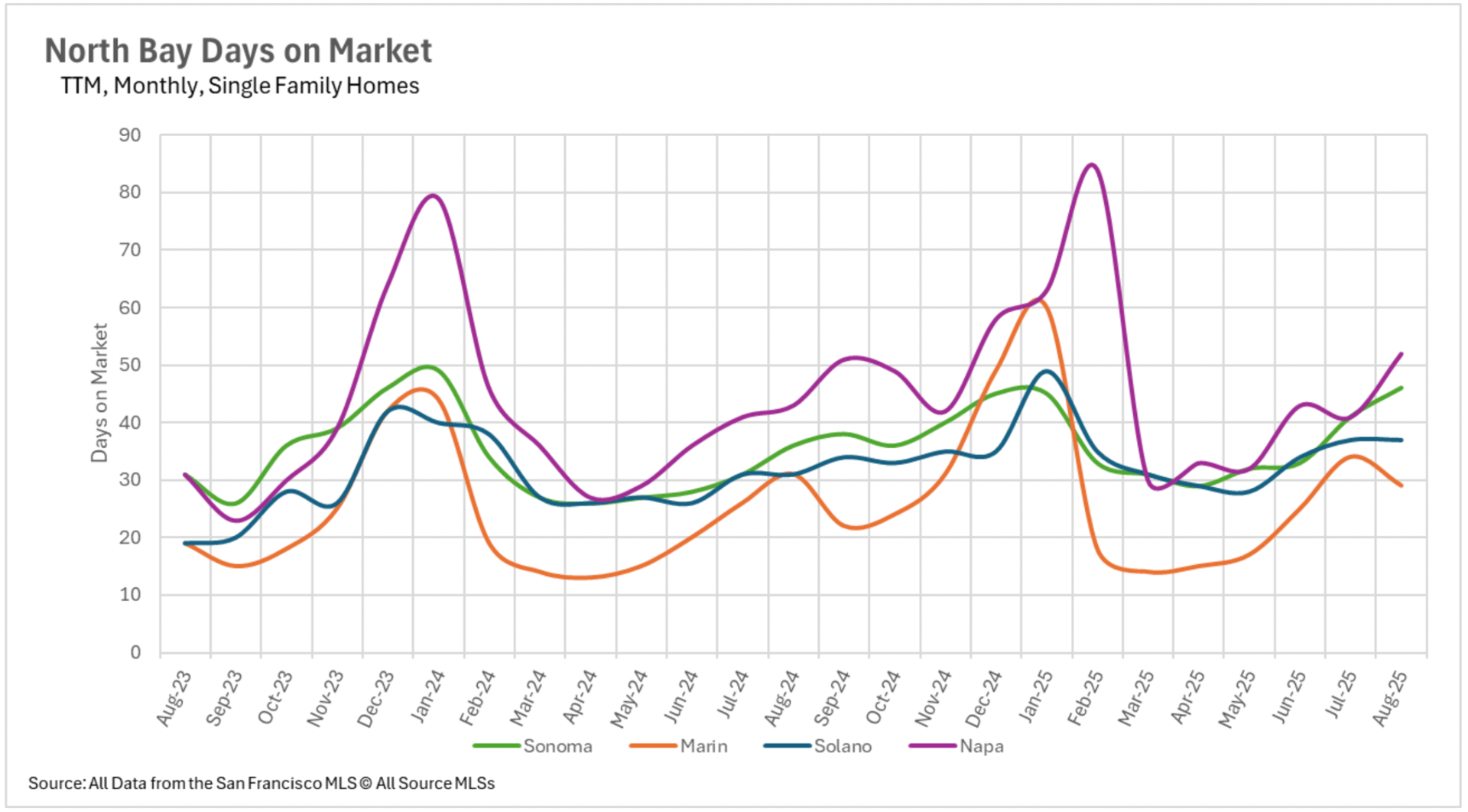

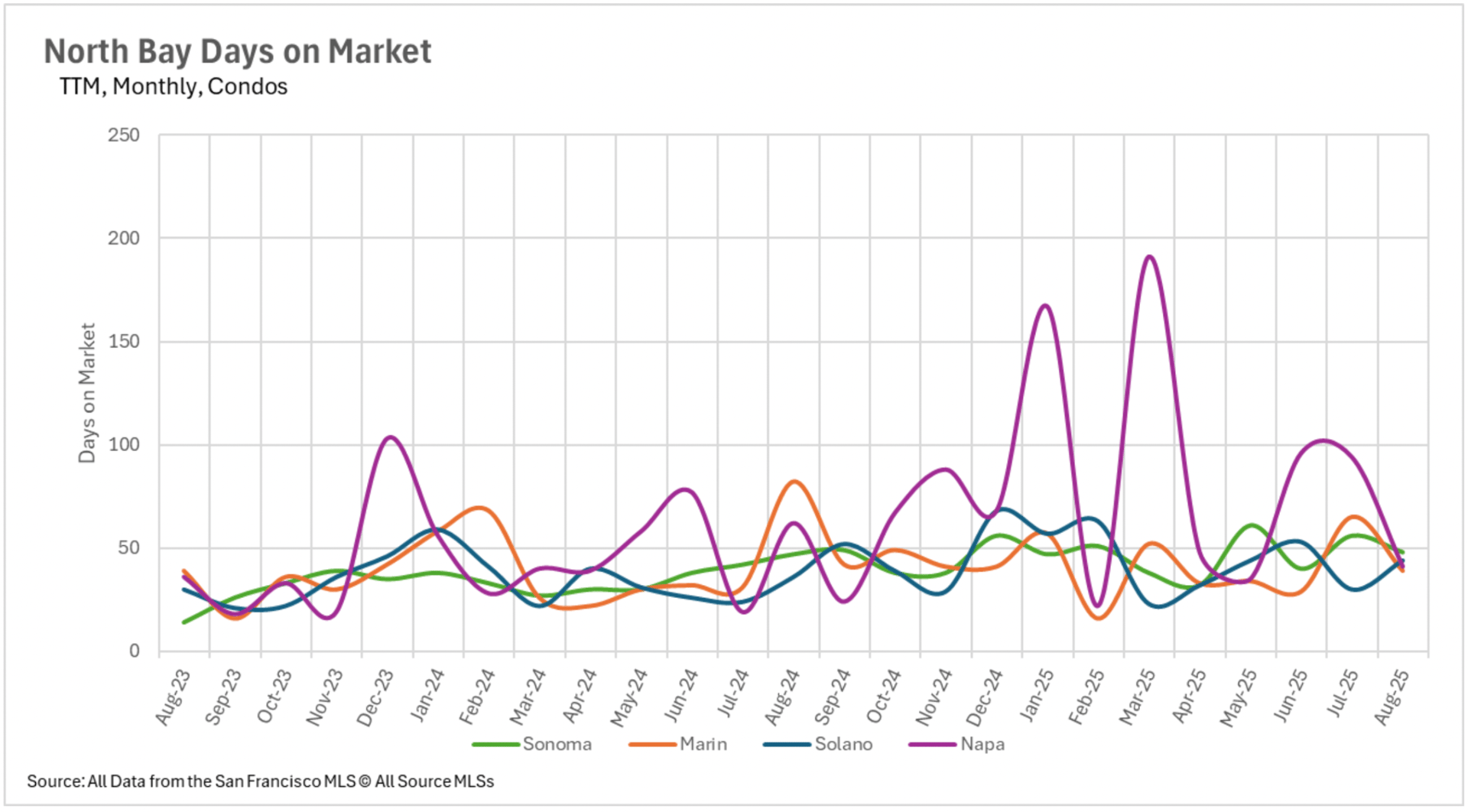

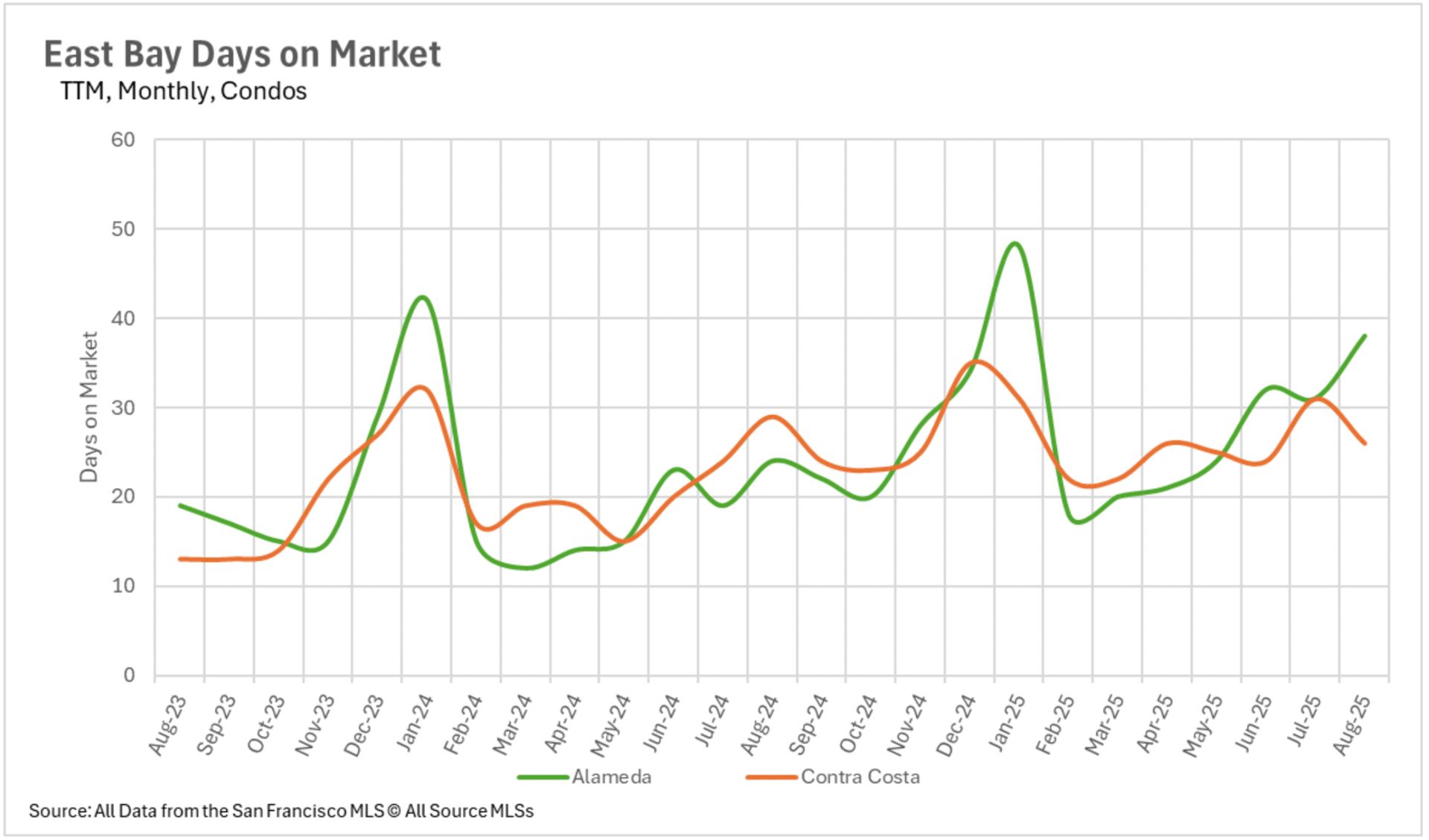

Among August's most significant developments was the persistent increase in market duration throughout most Bay Area regions, despite improving availability conditions. North Bay markets displayed the most substantial increases, with single-family properties requiring 27.78% additional market time in Sonoma County and approximately 20% longer in Solano and Napa Counties, though Marin County contradicted the pattern with a 6.45% reduction. East Bay markets exhibited considerable variations by property category and county, with single-family properties requiring 21.43% additional market time in Alameda County and 37.50% more in Contra Costa County, while condominium marketing periods showed inconsistent results - Alameda condominiums required 58.33% additional market time while Contra Costa condominiums actually decreased by 10.34%.

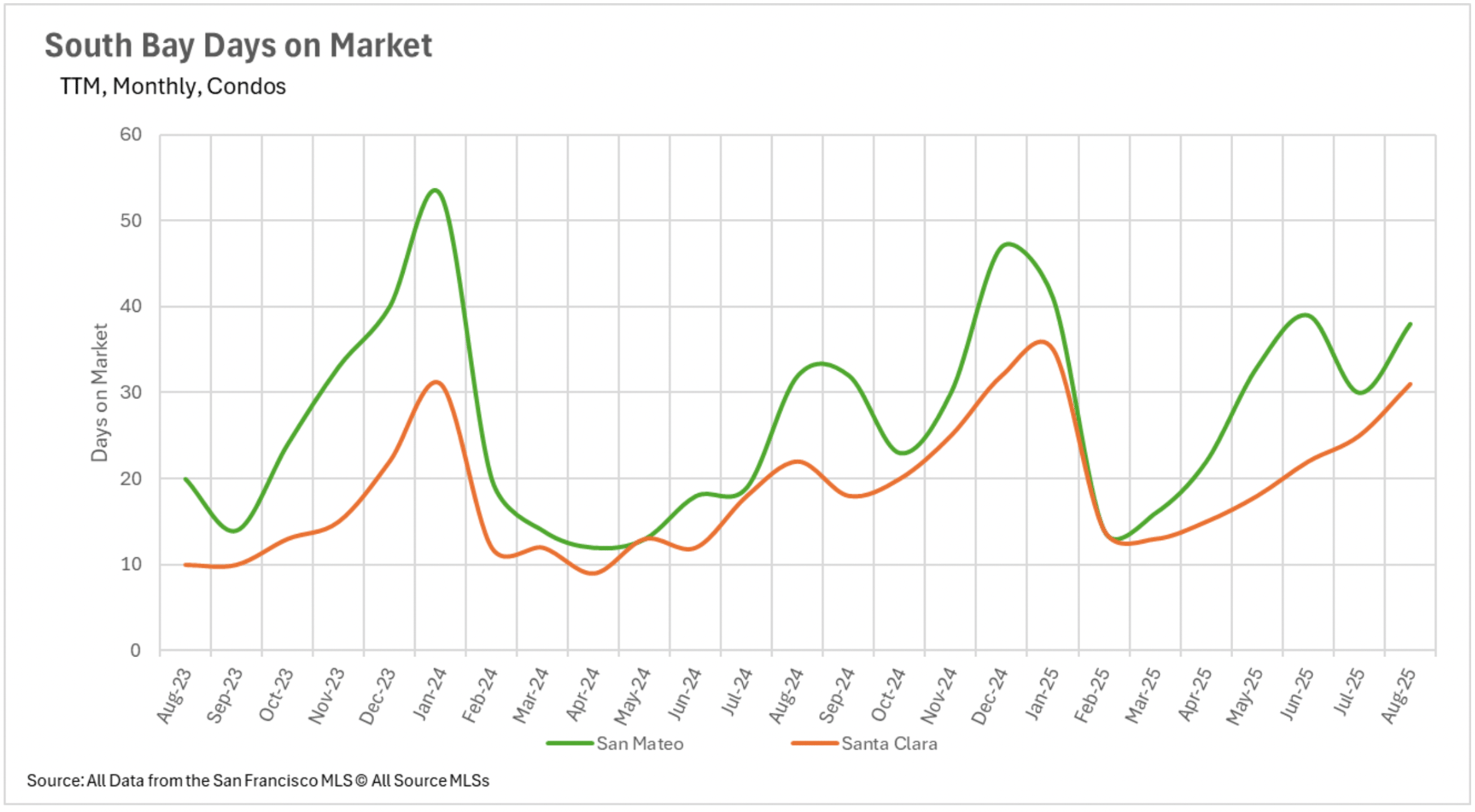

Silicon Valley sustained relatively efficient movement for single-family properties despite percentage increases, with absolute periods remaining at just 14 days in San Mateo and Santa Clara Counties and 26 days in Santa Cruz County. San Francisco exhibited the most compelling pattern, with single-family properties remaining exceptionally efficient at just 15 days while condominiums extended to 50 days (advancing 6.38% annually). These configurations indicate that while availability levels are improving, buyer conduct has fundamentally transformed toward enhanced selectivity and consideration.

August strengthened the Bay Area's distinct classification by property category rather than geographic position. San Francisco achieved prominence by establishing seller-favorable status for both single-family properties (1.1 months of supply) and condominiums (2.8 months of supply) - an uncommon development that emphasizes the region's extreme availability limitations. Silicon Valley sustained its competitive position for single-family properties, with San Mateo and Santa Clara Counties at exceptionally low 1.5 and 1.3 months respectively, while Santa Cruz County remained a buyer-favorable market at 3.9 months. All Silicon Valley condominium markets supported buyers, spanning from 3.2 months in Santa Clara to 5.5 months in Santa Cruz County.

East Bay markets maintained their conventional division with single-family properties strongly supporting sellers at 1.9 months in Alameda and 2.6 months in Contra Costa, while condominiums remained buyer-advantageous at 4.4 and 4.2 months respectively. North Bay regions demonstrated the greatest diversity, with Marin establishing perfect equilibrium at 3.0 months for single-family properties, while Solano (3.3 months), Sonoma (3.9 months), and Napa (7.6 months) all supported buyers. North Bay condominiums consistently supported buyers, with supply spanning from 4.0 months in Marin to 7.5 months in Napa County. This uniform pattern throughout the region indicates that single-family properties have preserved their premium positioning and scarcity advantage, while condominiums offer considerable opportunities for buyers prepared to manage extended timelines and expanded availability selections.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

December 4, 2025

November 19, 2025

October 21, 2025

September 24, 2025

September 23, 2025

You've got questions and we can't wait to answer them.