July Market Update

Bay Area housing conditions in June demonstrate a pronounced division between San Francisco's accelerating values and widespread condominium market weakness across neighboring regions.

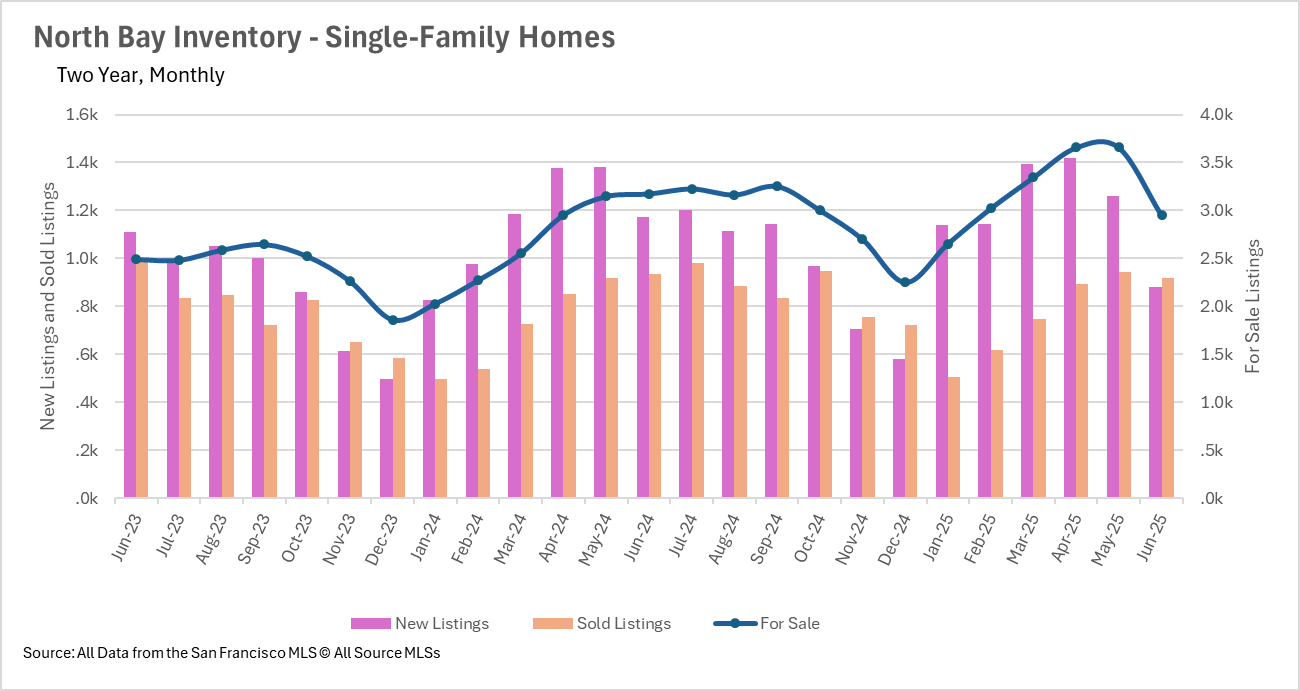

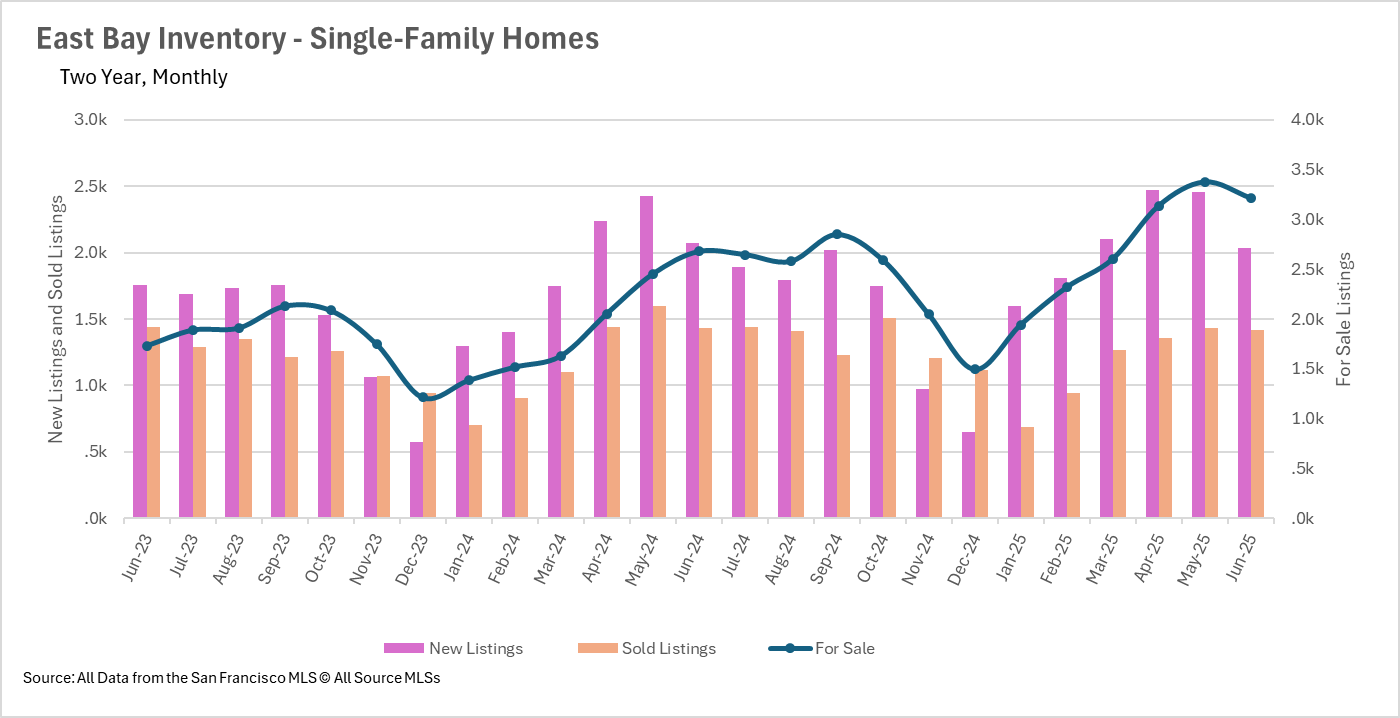

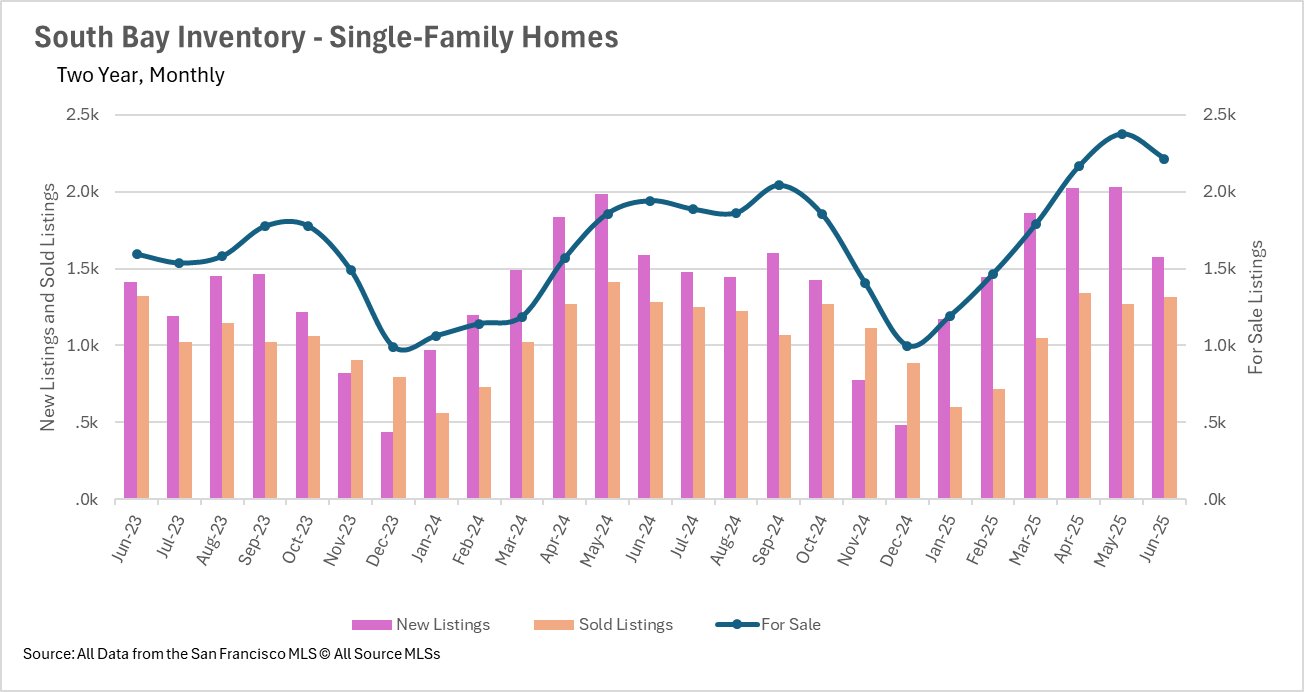

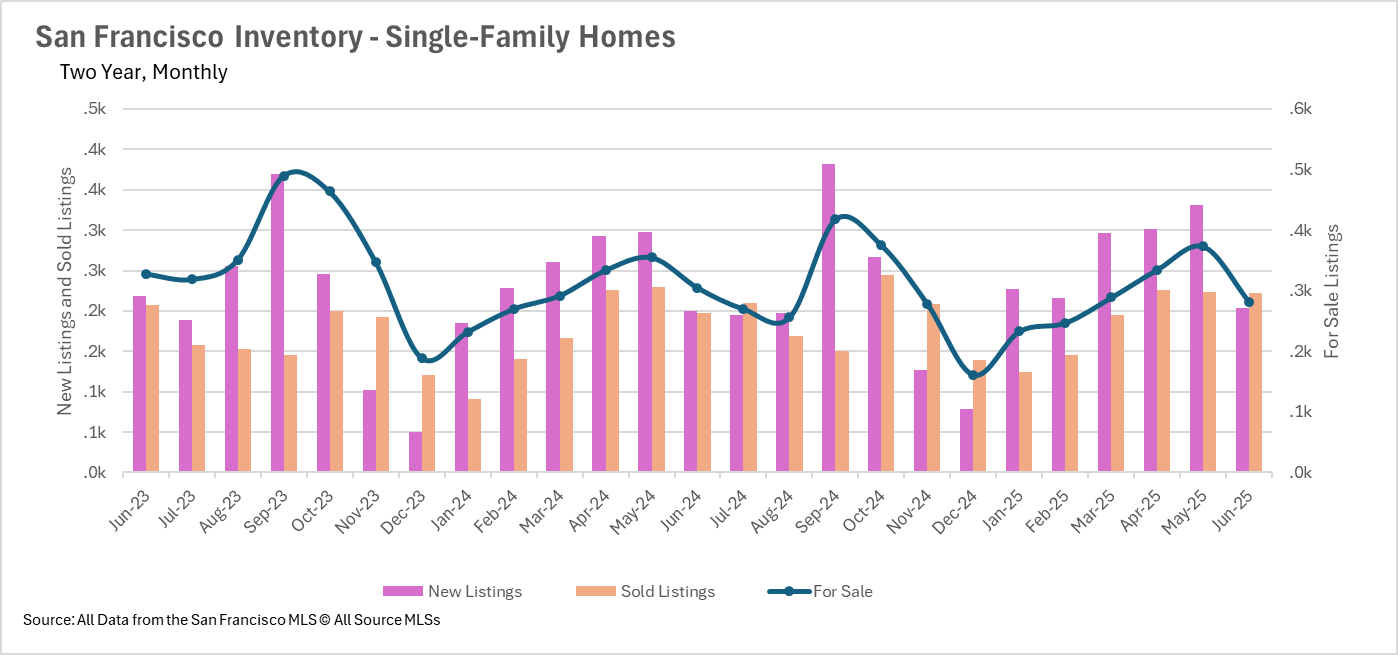

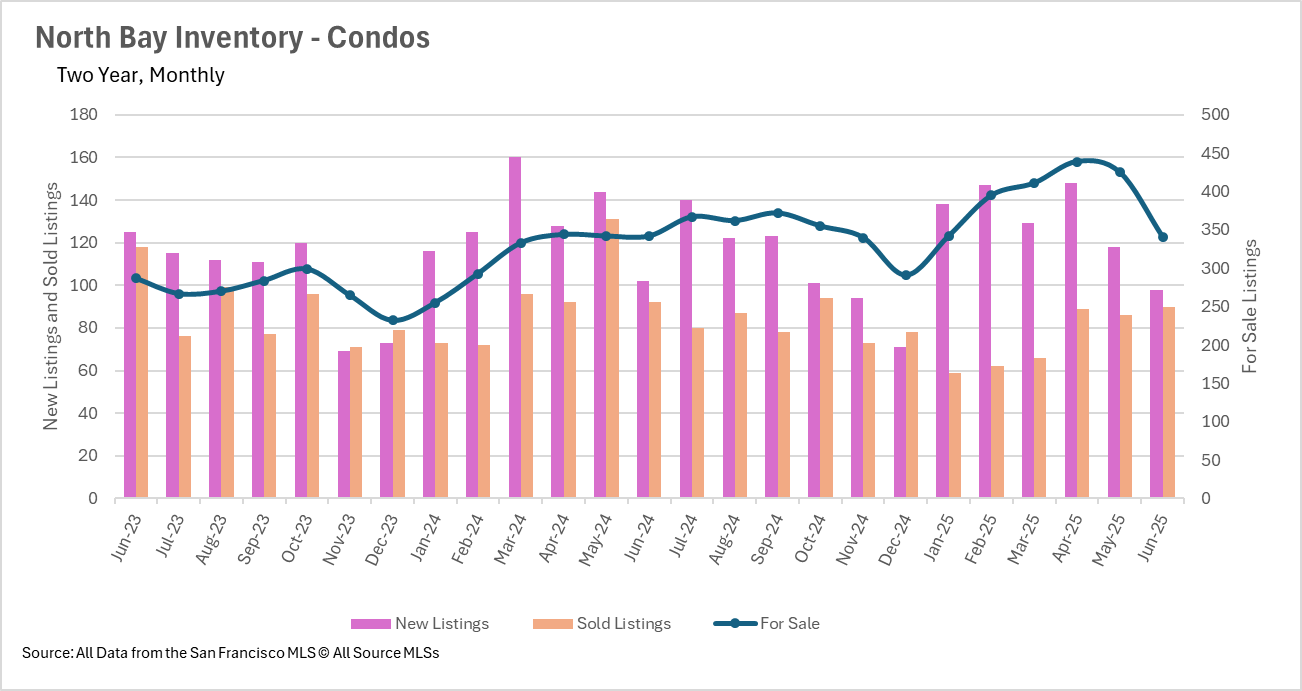

Supply levels have hit regional highs throughout most areas and are starting to contract, with the most significant reductions occurring in North Bay and San Francisco markets.

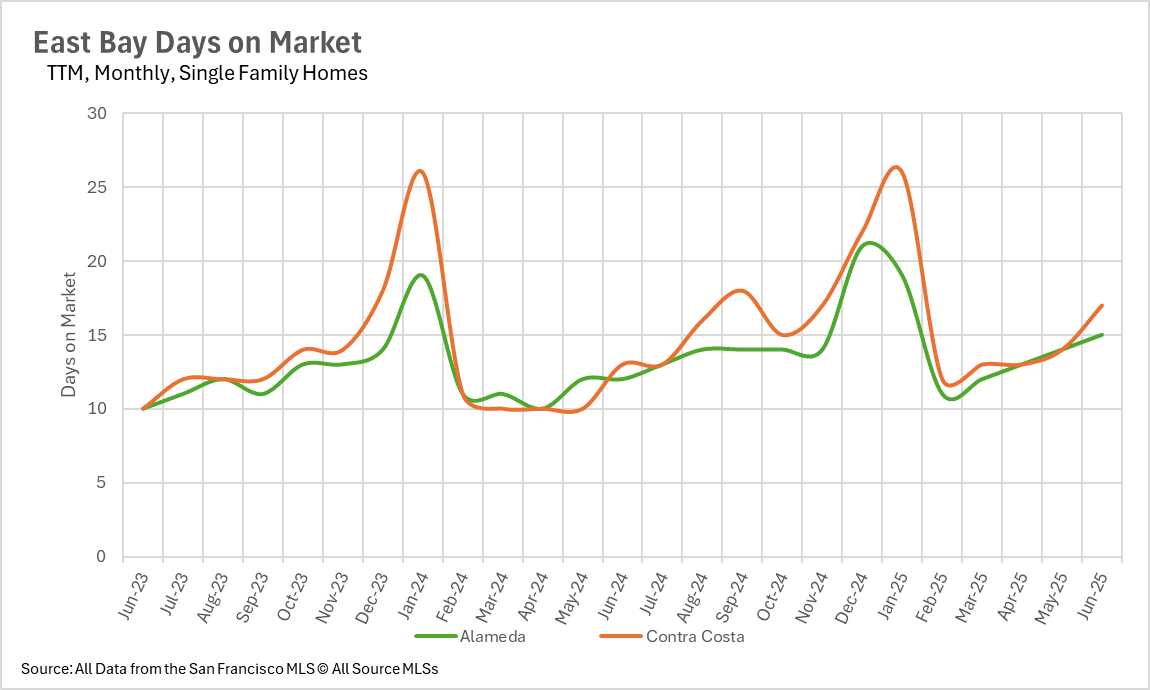

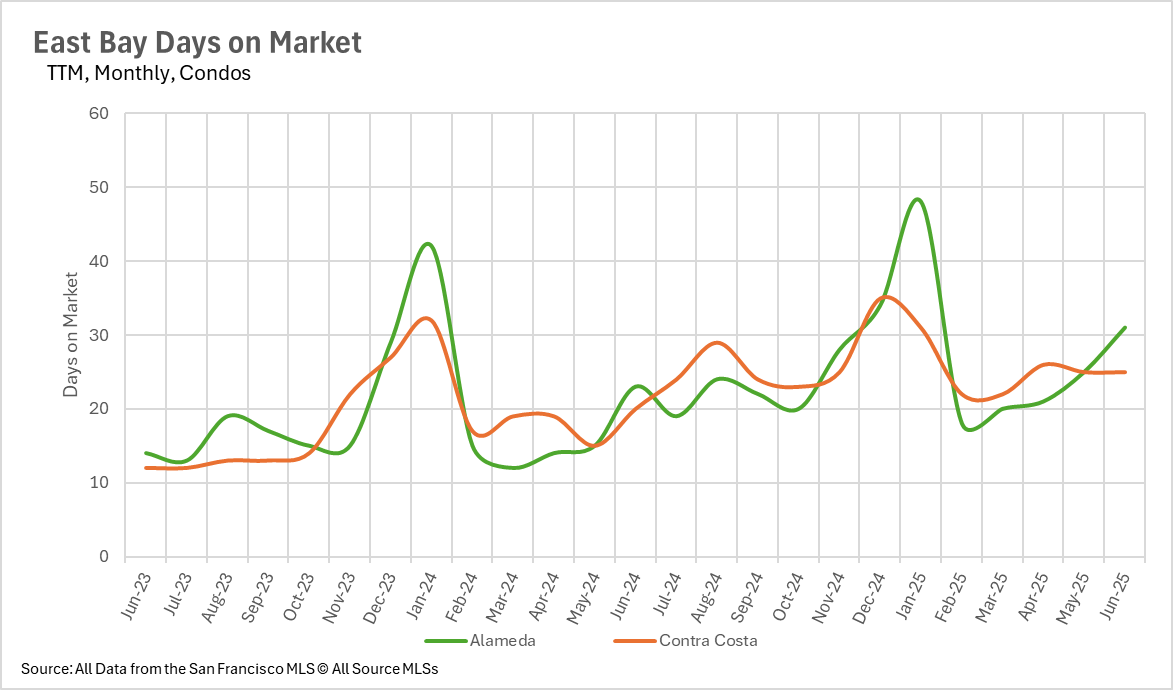

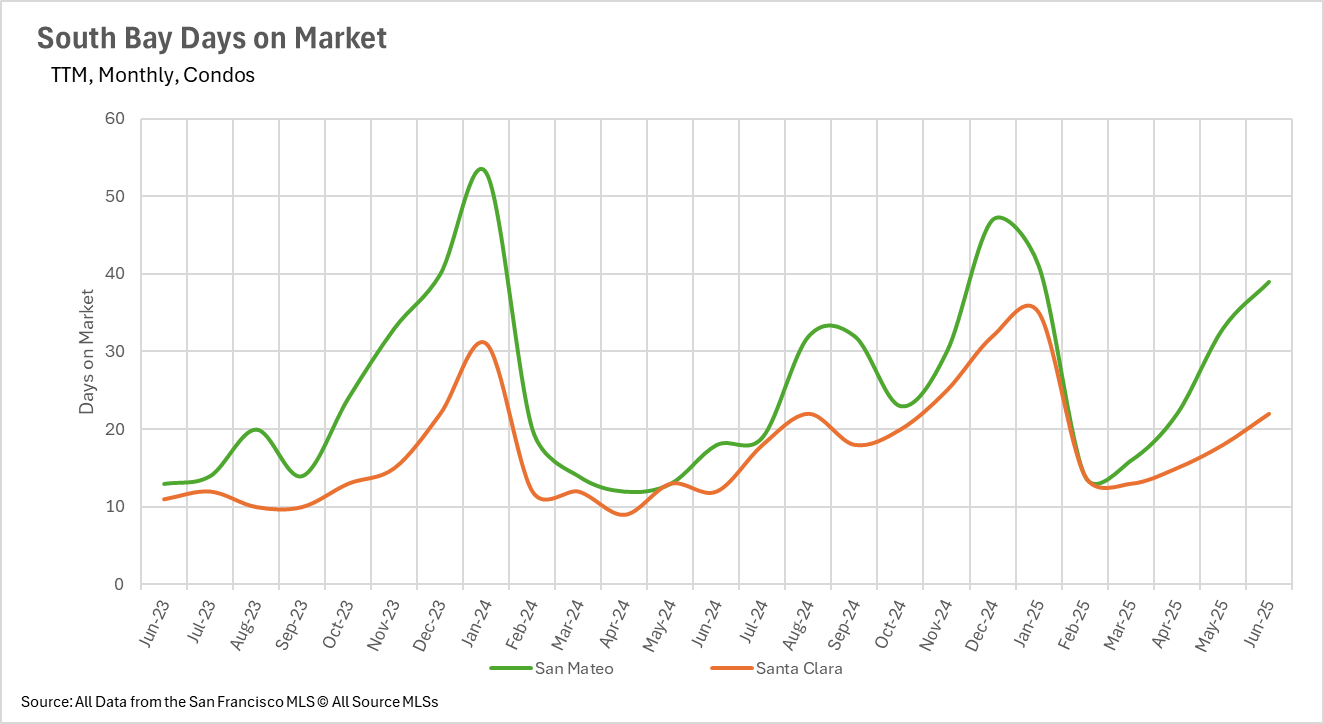

Even with inventory contractions, properties are requiring considerably longer marketing periods across the Bay Area, with condominiums facing especially pronounced increases in time on market.

Market dynamics continue to heavily favor single-family properties over condominiums, with the condominium segment offering substantial buyer advantages throughout all regions.

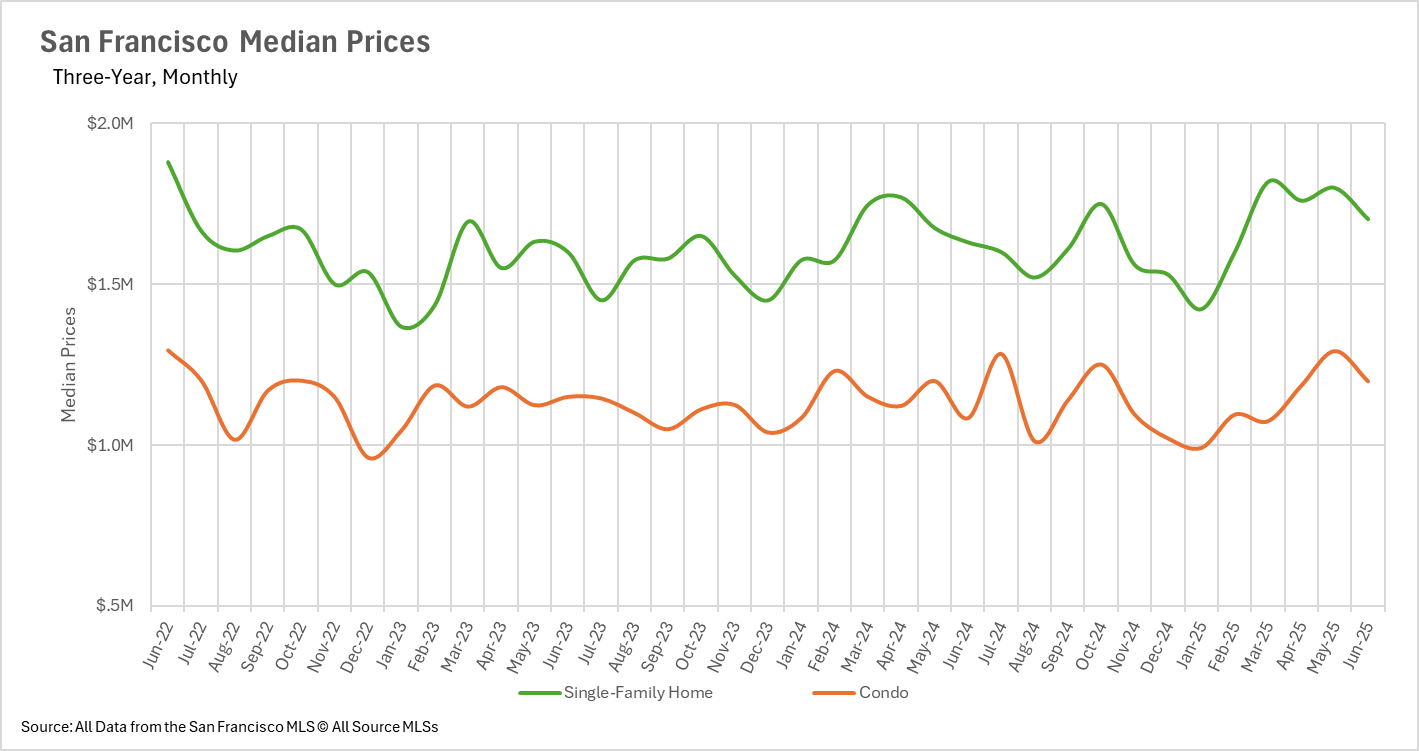

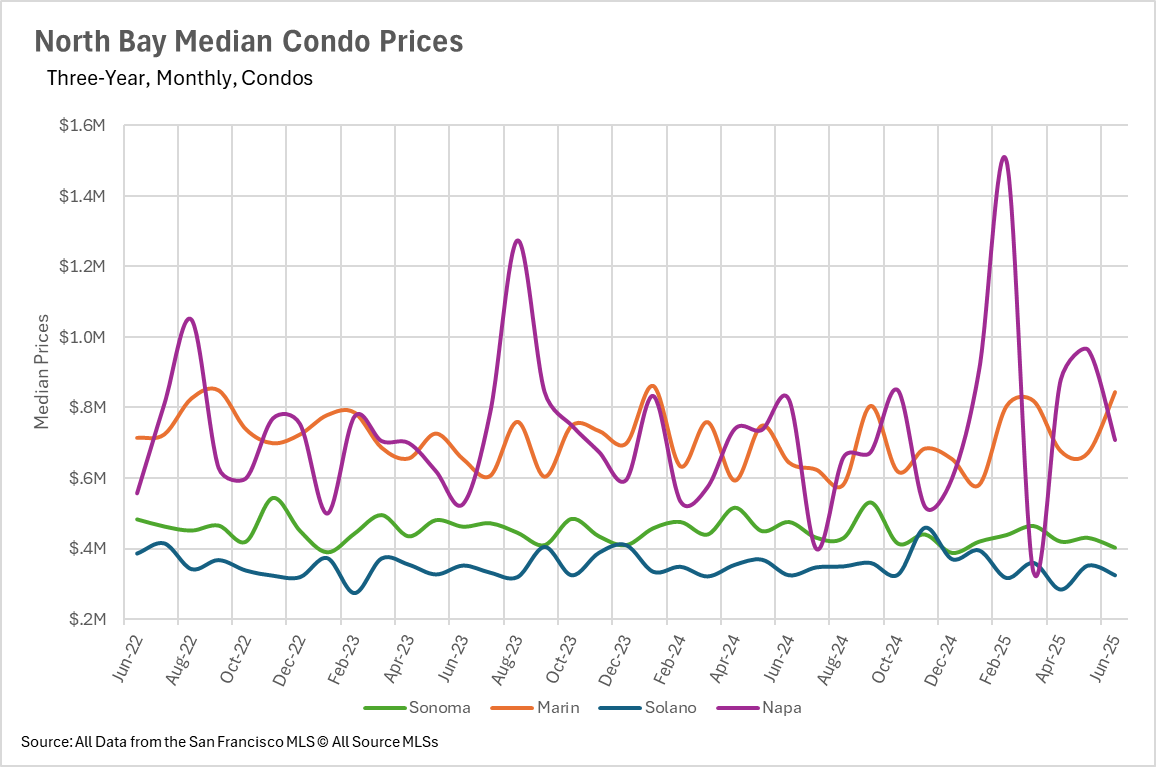

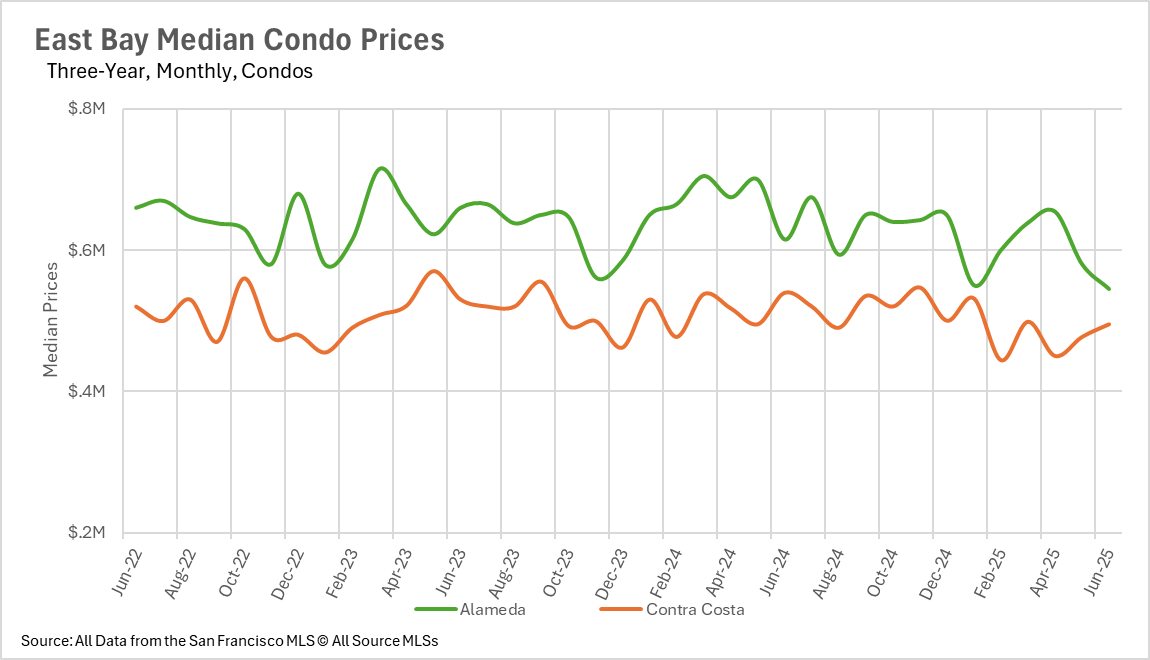

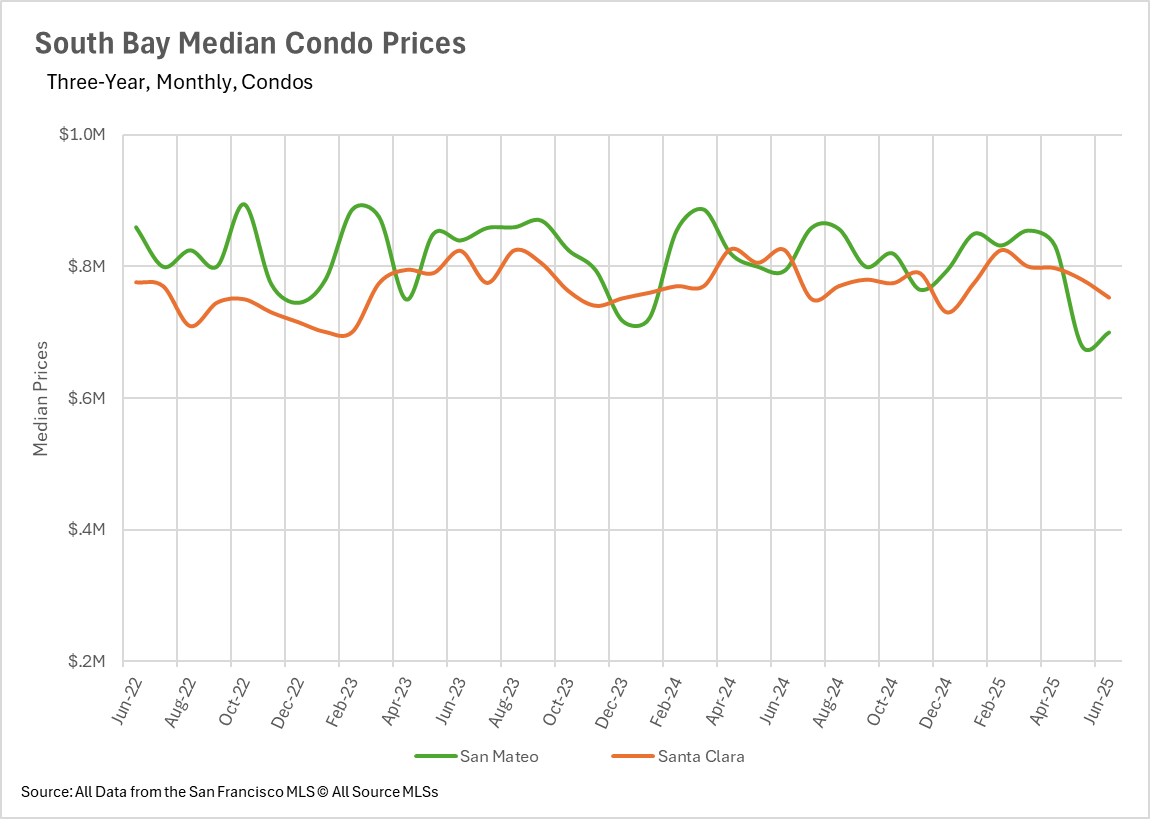

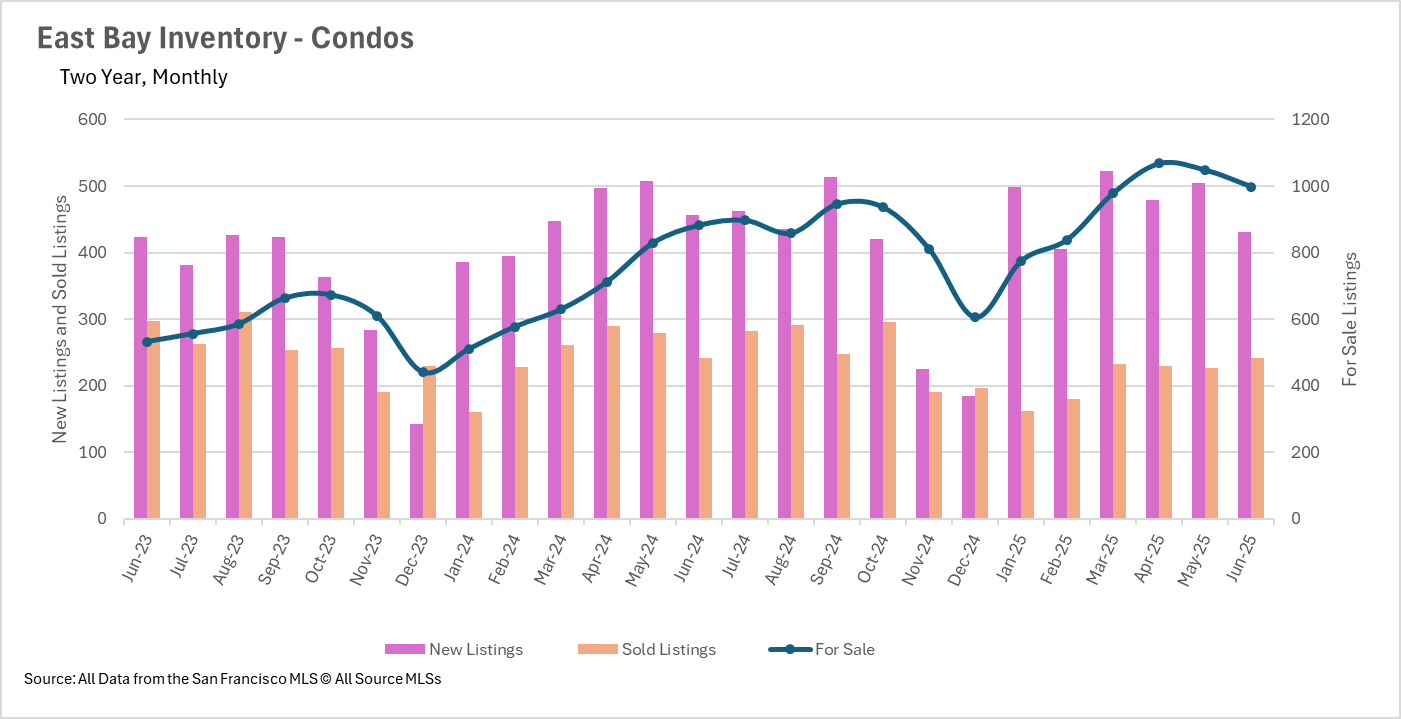

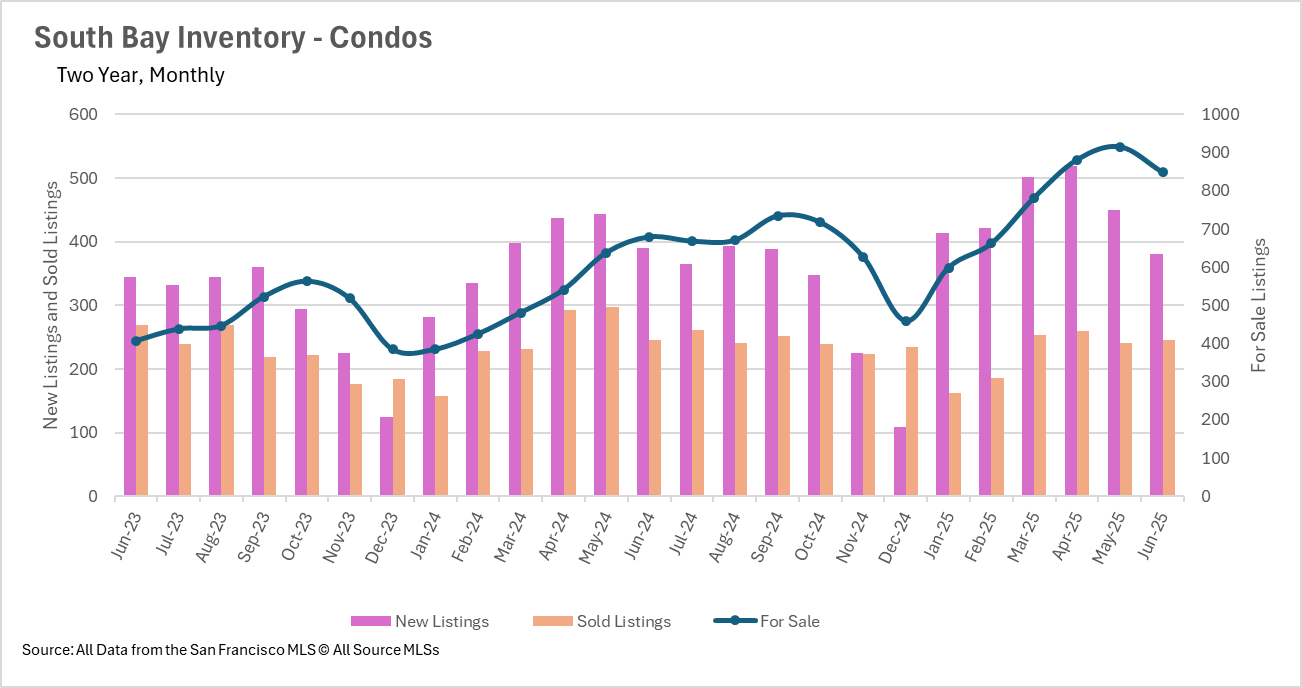

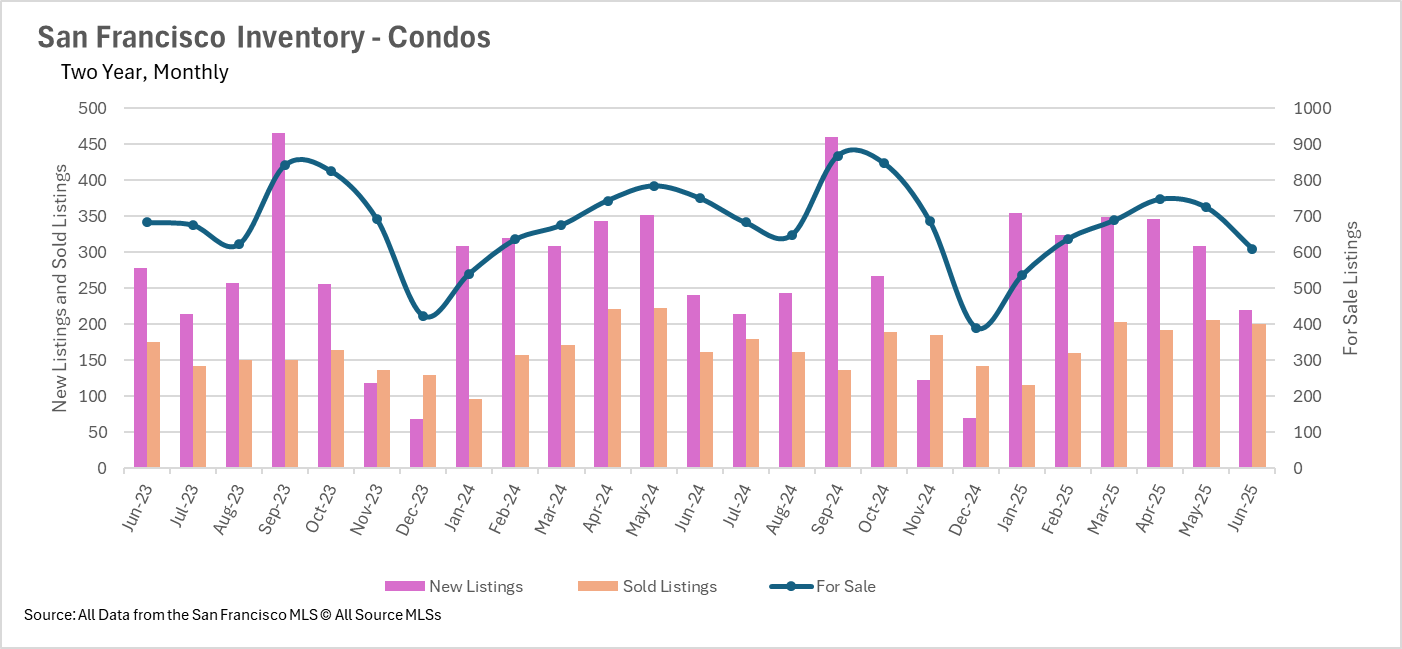

June reinforced San Francisco's position as the Bay Area's price performance leader, with single-family property values advancing 4.42% annually and condominium prices jumping an outstanding 10.52%—continuing over twelve months of sustained appreciation. This performance contrasts sharply with the broader regional landscape, where condominium markets face considerable pressure. The East Bay entered its fifth consecutive month of annual condominium price retreats, with values declining 11.41% in Alameda County and 8.25% in Contra Costa County. Silicon Valley's condominium sector extended its downward trend for the third consecutive month, with Santa Clara County retreating 8.79%, San Mateo County falling 11.84%, and Santa Cruz County posting a severe 13.52% decline.

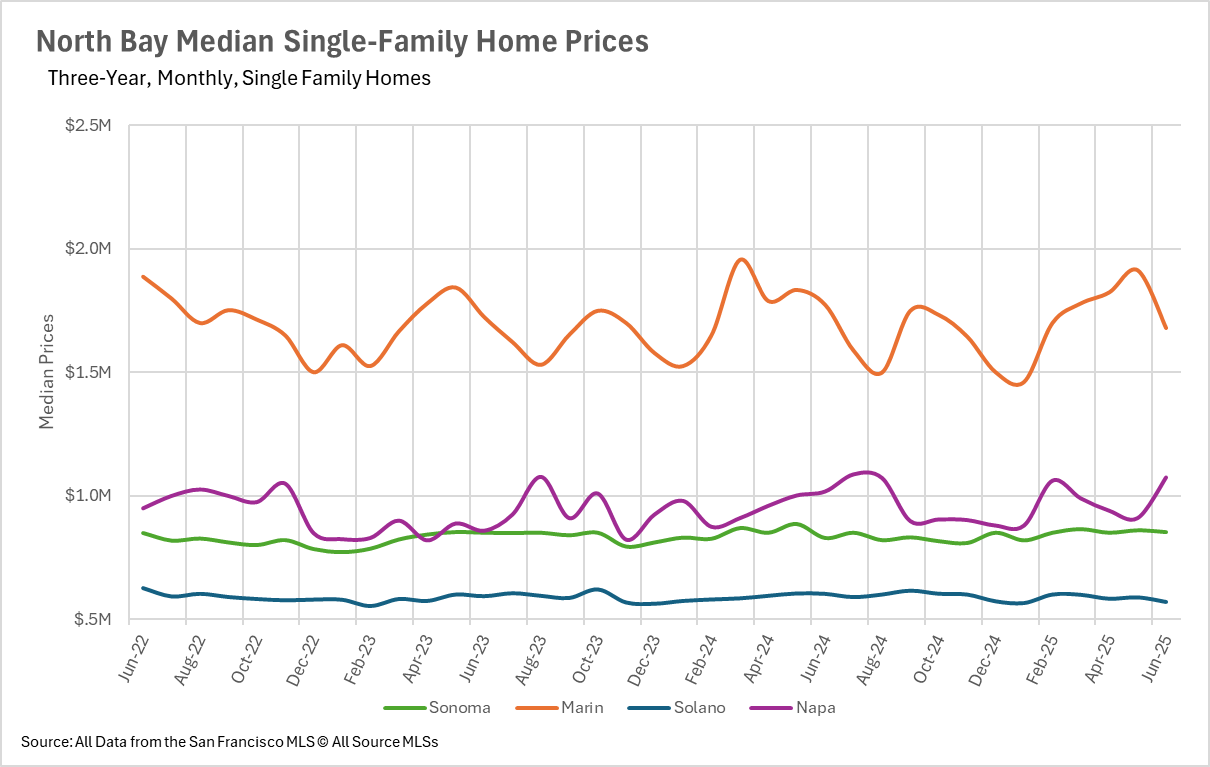

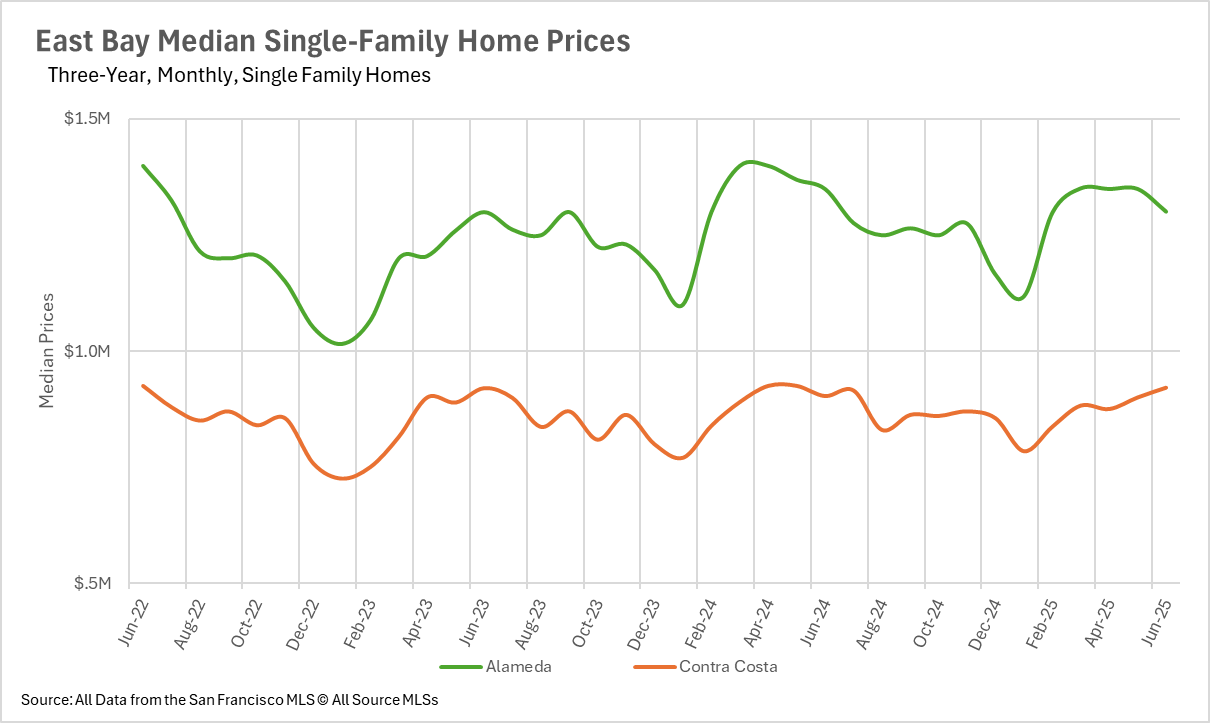

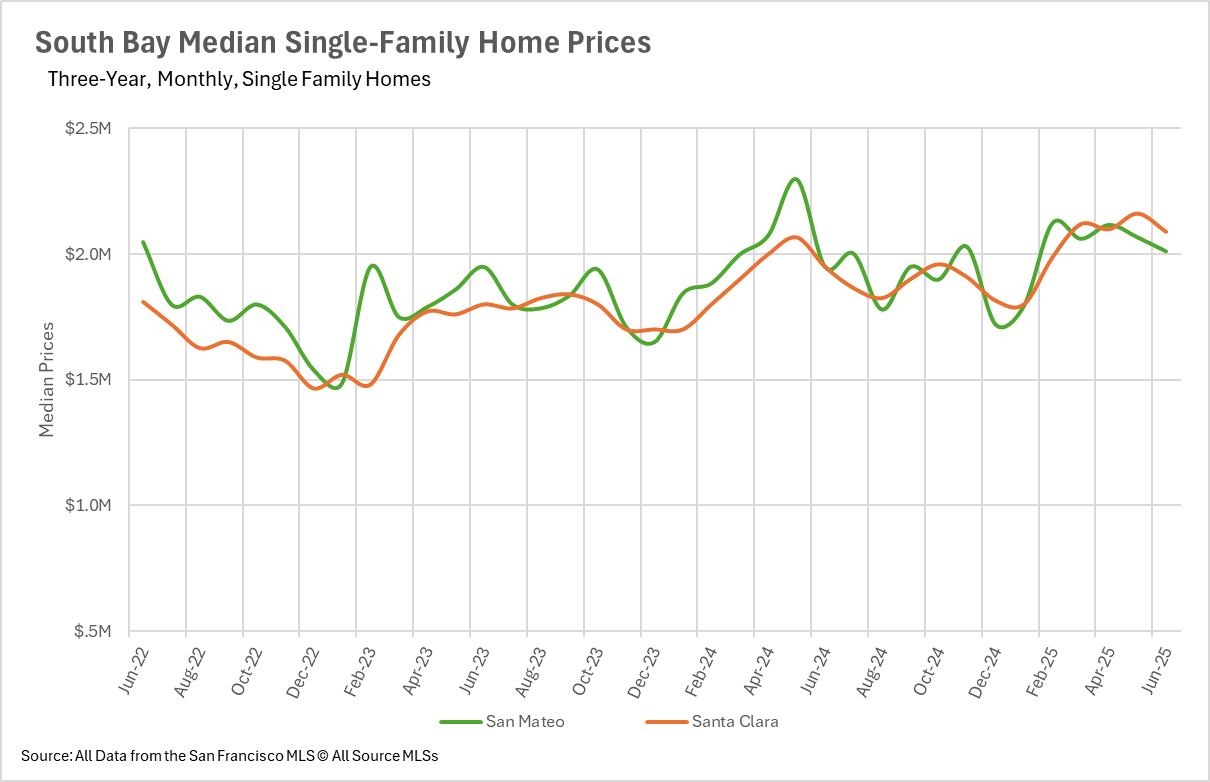

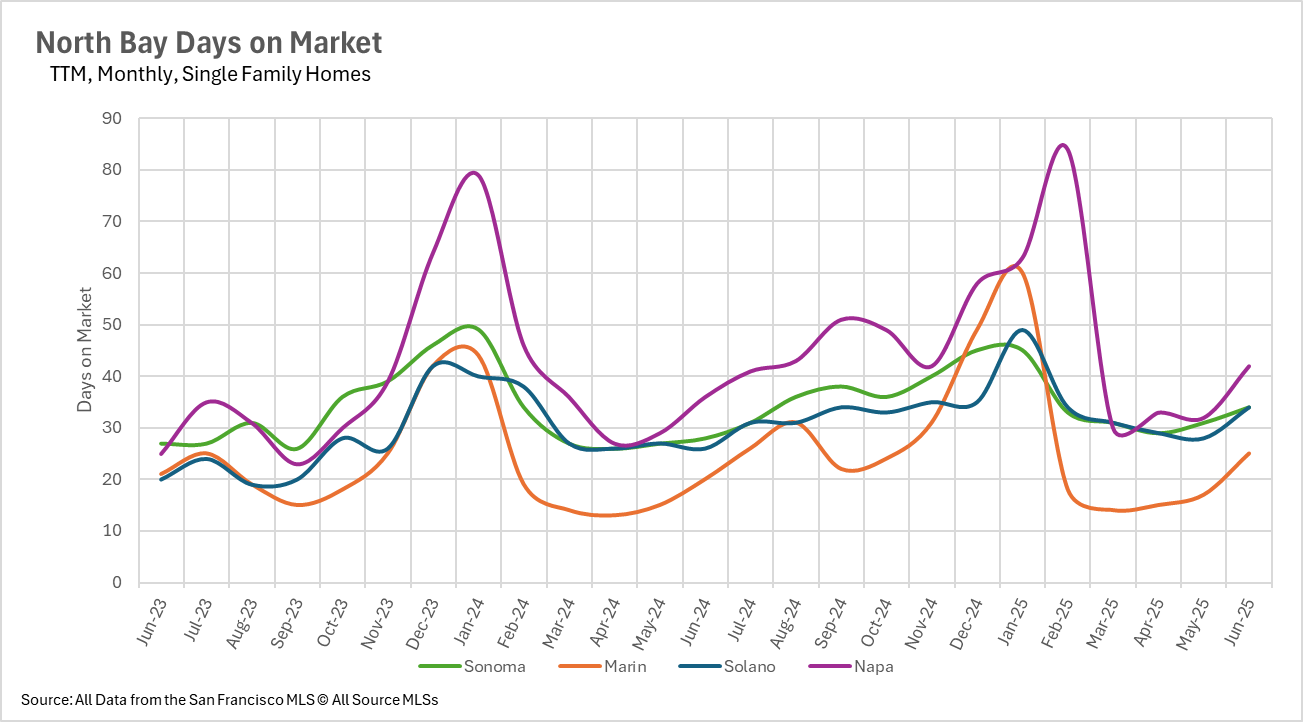

North Bay markets exhibited the greatest single-family stability, with Sonoma County advancing 2.92% and Napa County climbing 5.60%, while Solano and Marin Counties registered declines of 5.23% and 5.35% respectively. Silicon Valley single-family properties showed durability with San Mateo and Santa Clara Counties recording advances of 3.21% and 7.18%, while only Santa Cruz County retreated 4.64%. East Bay single-family conditions displayed varied performance with Contra Costa County achieving a moderate 1.99% gain while Alameda County extended its five-month decline.

June represented a notable transformation in inventory conditions throughout the Bay Area, with most regions recording substantial monthly reductions following local supply peaks in May. North Bay markets experienced among the most dramatic inventory contractions in recent memory, with single-family supply falling 19.34% month-over-month (while remaining down just 7.09% annually) and condominium availability declining 19.76% monthly. San Francisco maintained its extended inventory reduction pattern with single-family supply down 7.87% annually and condominiums posting an even sharper 18.77% retreat.

Silicon Valley and East Bay markets appear to have crested their inventory peaks, with both regions recording June decreases while sustaining considerably elevated levels compared to last year. East Bay markets continue showing single-family inventory 20.05% above year-ago levels and condominium supply 13.15% higher, while Silicon Valley maintains 14.18% more single-family listings and 24.89% more condominium availability than June 2024. The prevailing pattern across all regions shows inventory reductions stemming more from reduced new listing activity rather than enhanced sales volume, indicating seller caution rather than buyer enthusiasm.

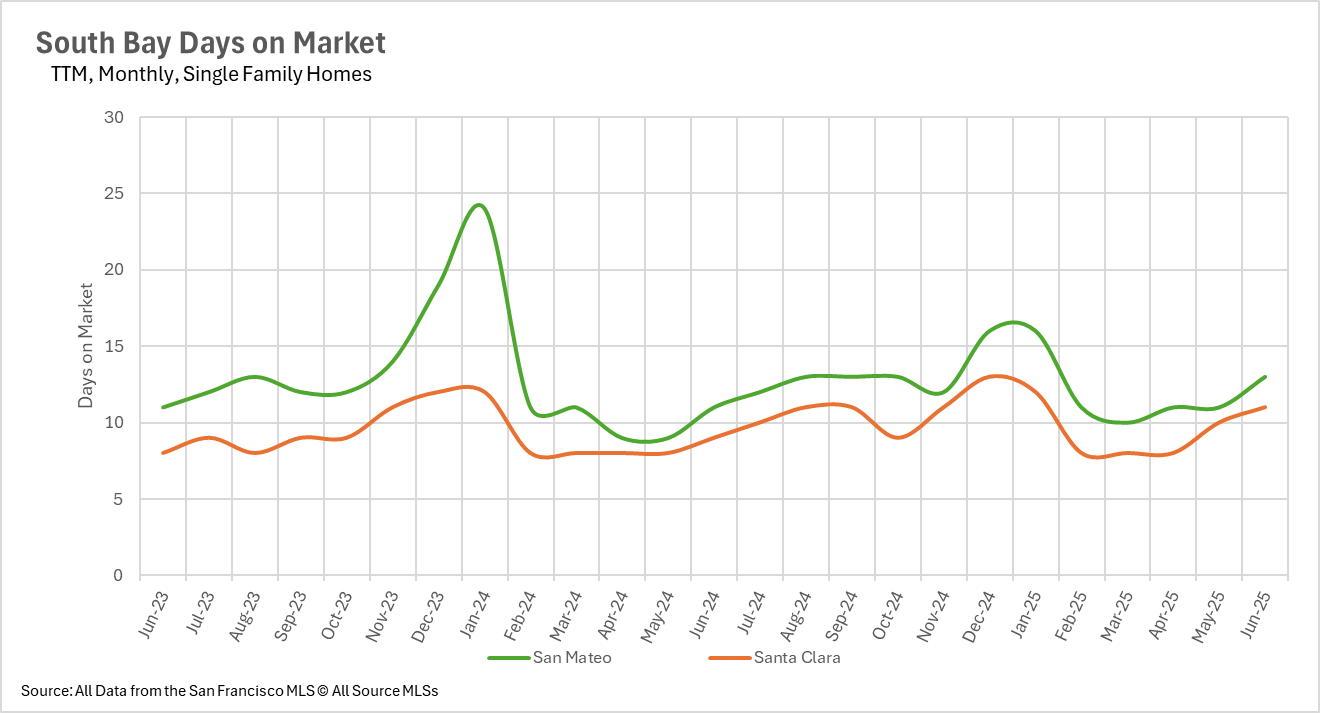

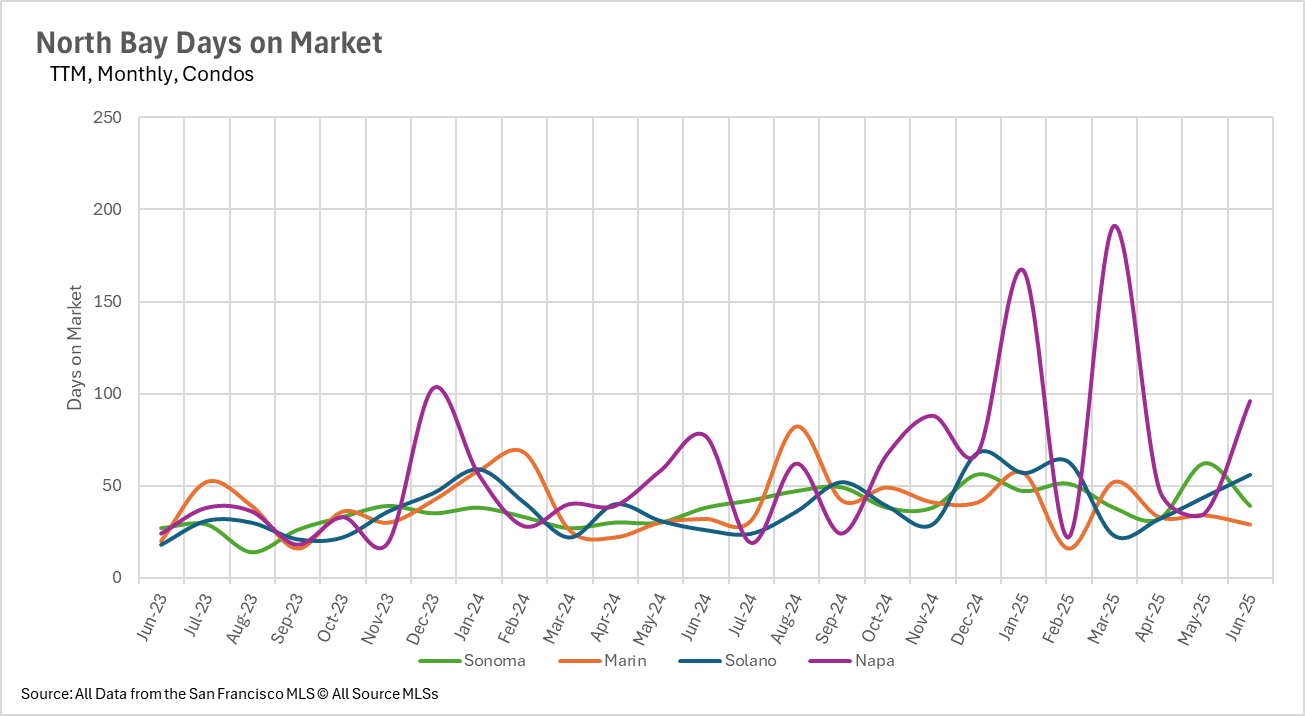

Among June's most notable developments was the significant expansion in marketing timeframes across all Bay Area regions, despite substantial inventory reductions. North Bay markets demonstrated the most uniform pattern with single-family properties requiring 21.43% longer marketing periods in Sonoma County, 25% longer in Marin County, 30.77% longer in Solano County, and 16.67% longer in Napa County annually. Silicon Valley's condominium sector faced the most substantial increases, with Santa Cruz County units spending 245.45% additional time on market, San Mateo County condominiums up 116.67%, and Santa Clara County condominiums rising 83.33%.

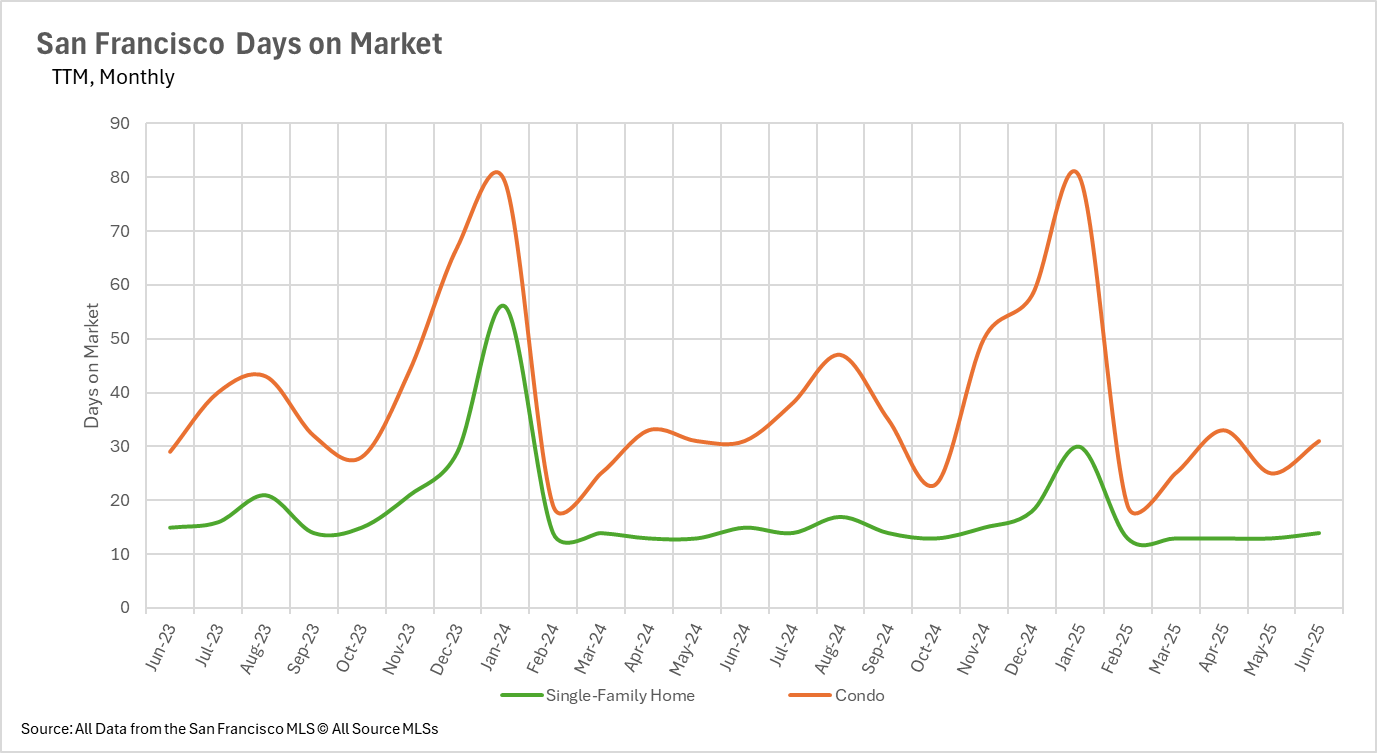

San Francisco, traditionally the Bay Area's most efficient market, recorded single-family properties averaging 14 days (declining 6.67% from last year) while condominiums remained stable at 31 days. East Bay markets showed more moderate yet still meaningful increases of 25-35% longer marketing periods annually, though absolute timeframes remained relatively efficient with single-family properties selling within 15-17 days and condominiums within 25-31 days. This trend indicates that while supply is contracting, buyer discernment is intensifying, establishing a more measured purchasing climate.

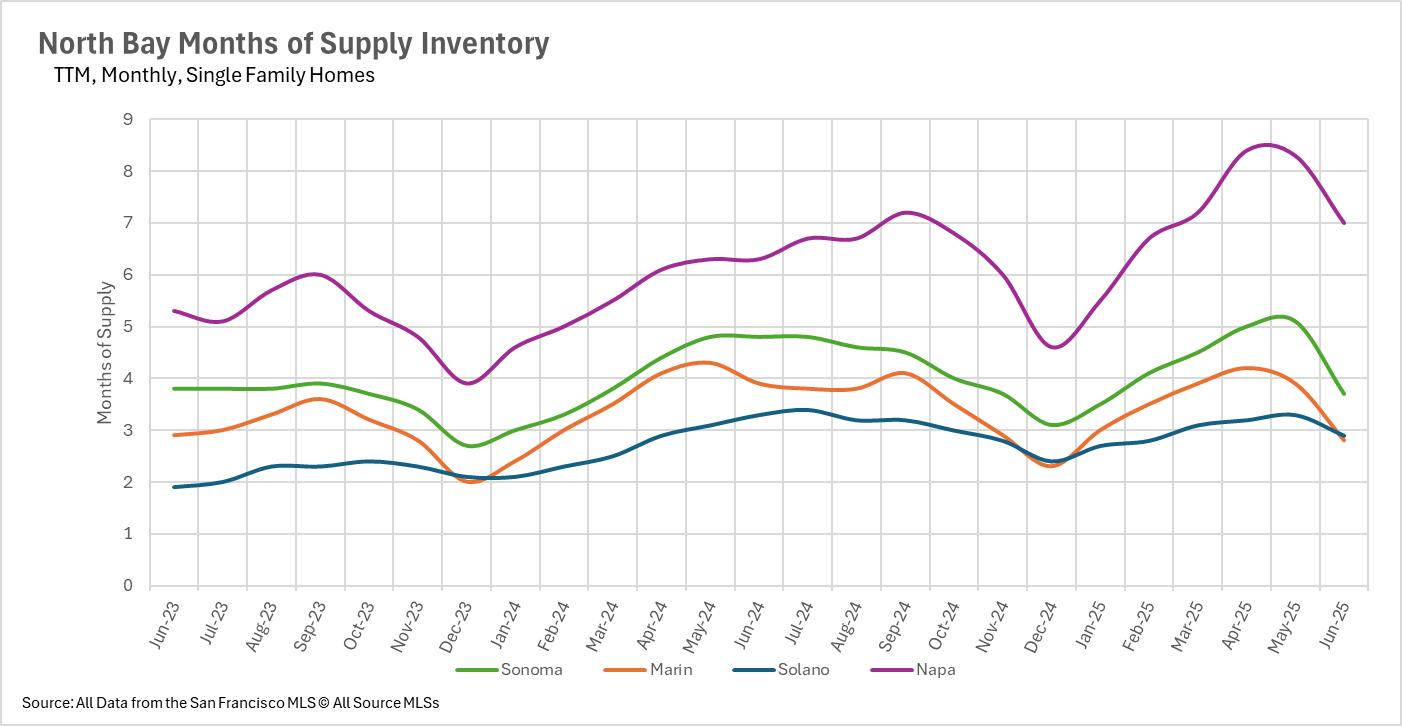

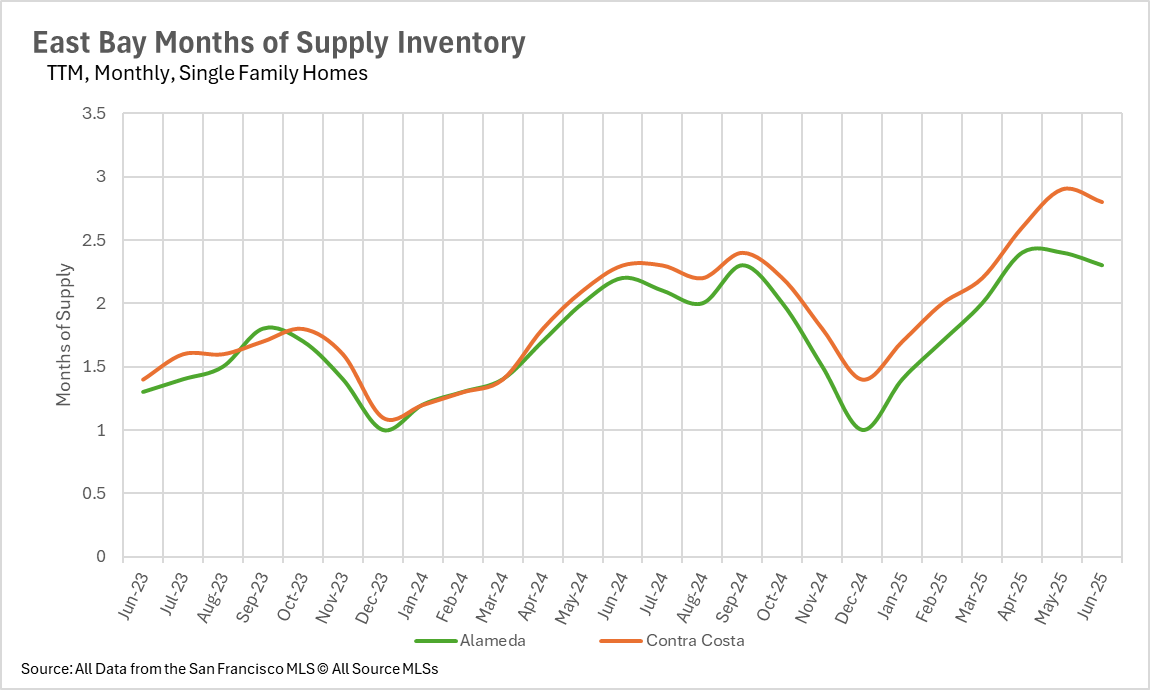

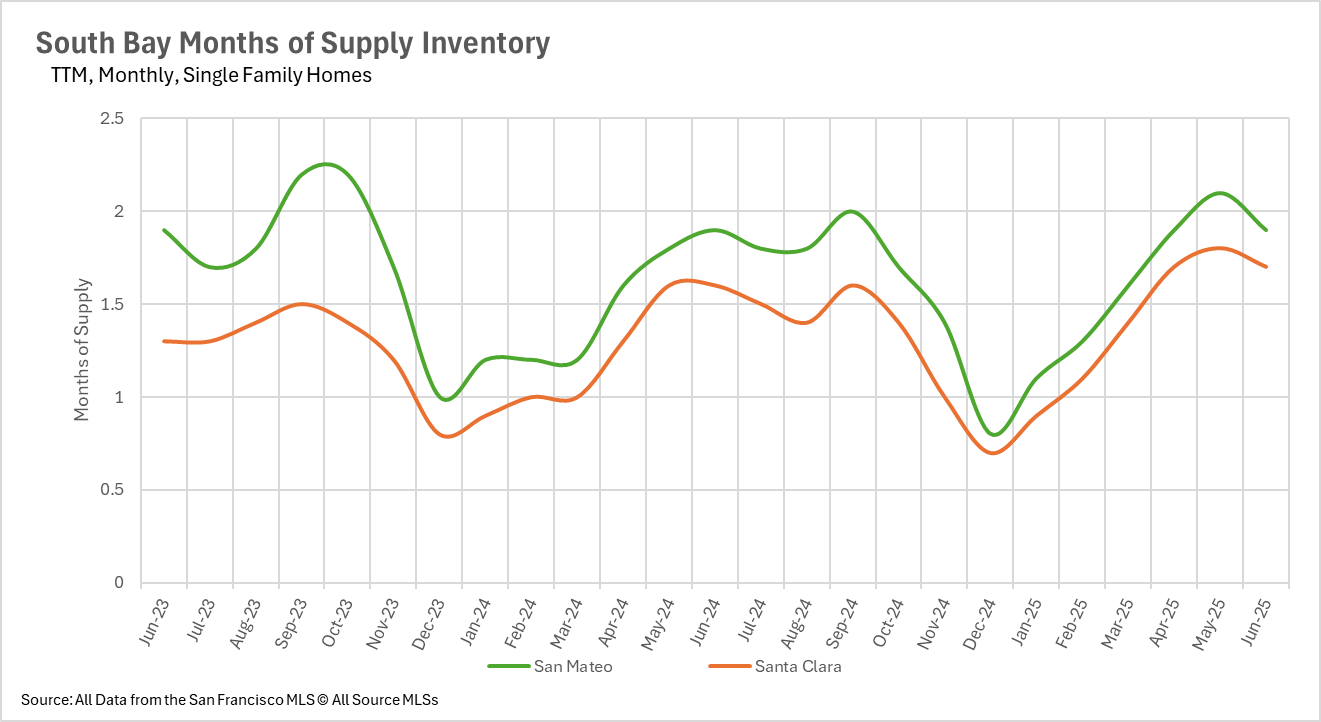

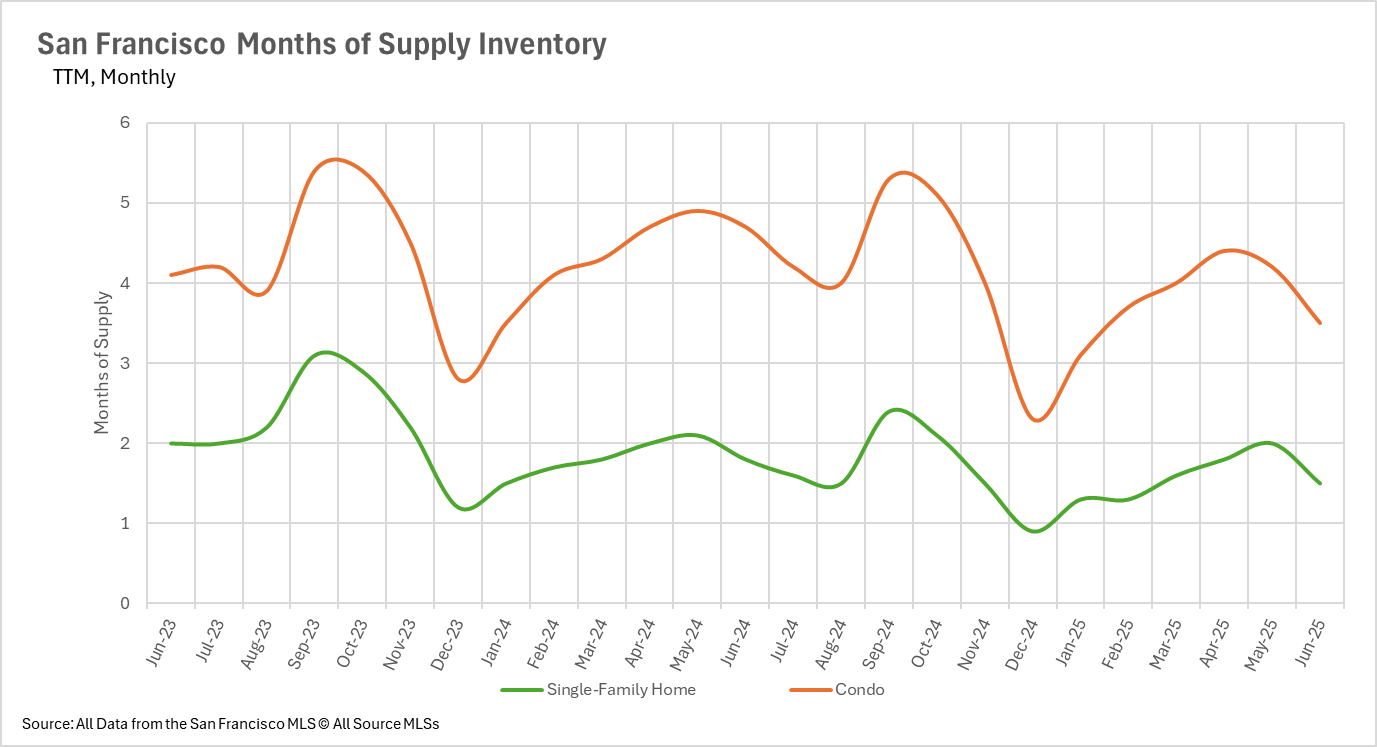

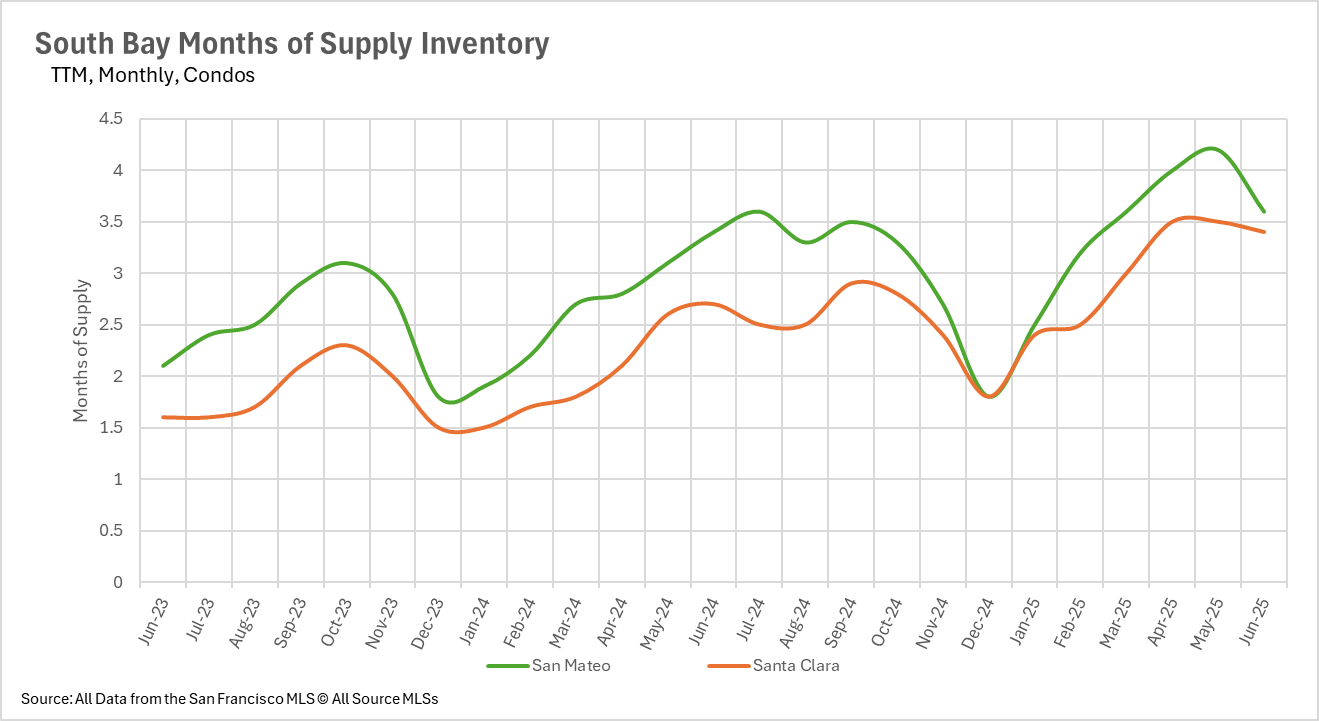

Months of supply inventory analysis demonstrates a uniform Bay Area pattern where single-family properties maintain seller-advantageous conditions while condominiums have moved decisively toward buyer-favorable markets. San Francisco exemplifies this dynamic with single-family homes at 1.5 months of supply (robust seller's market) while condominiums register 3.5 months (buyer's market). Silicon Valley shows San Mateo and Santa Clara Counties preserving seller's markets for single-family properties at 1.9 and 1.7 months respectively, while all three Silicon Valley counties offer buyer's markets for condominiums ranging from 3.4 to 5.5 months of supply.

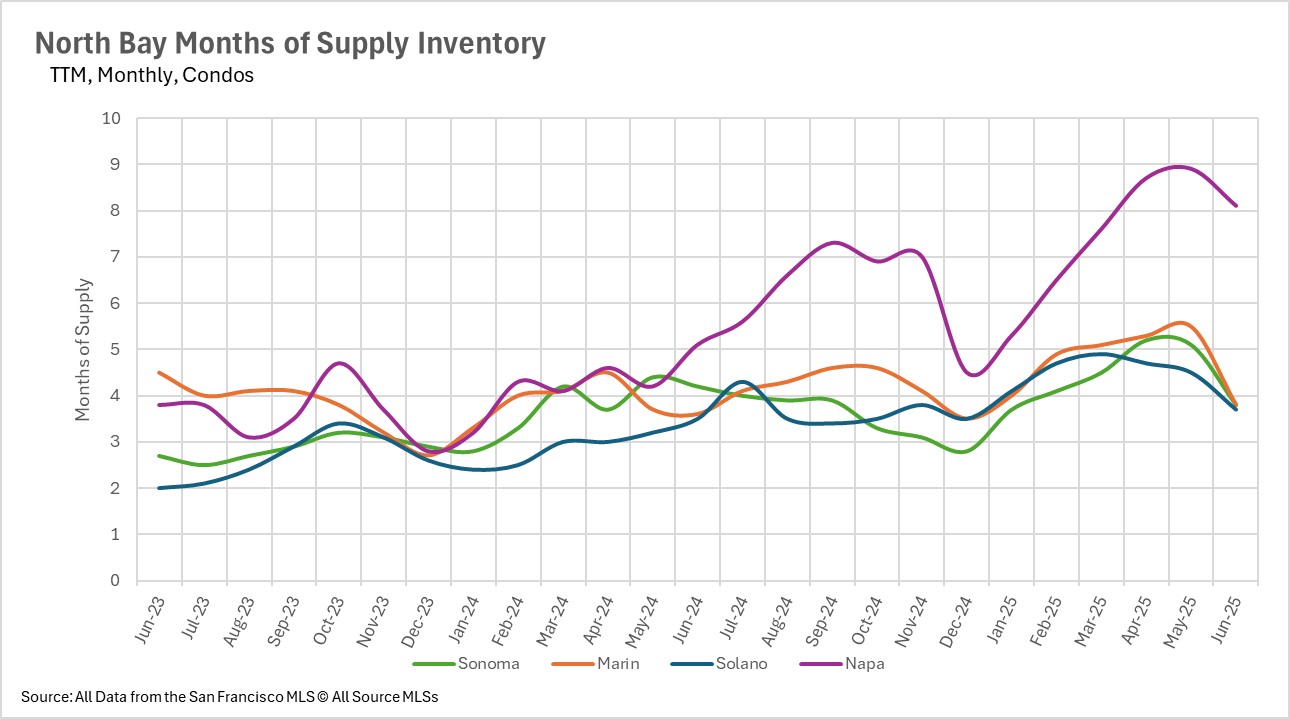

East Bay markets maintain their characteristic division with single-family homes at 2.3 months in Alameda and 2.8 months in Contra Costa (seller's markets), while condominiums support buyers with 4.7 and 3.9 months respectively. North Bay markets demonstrate the greatest diversity, with Marin and Solano Counties approaching equilibrium for single-family properties at 2.8 and 2.9 months, while Sonoma (3.7 months) and Napa (7 months) favor buyers. Nevertheless, all North Bay counties offer buyer's markets for condominiums, with Napa County displaying an exceptional 8.1 months of condominium supply.

This configuration suggests that throughout the Bay Area, single-family properties preserve their desirable positioning and seller benefits, while the condominium market offers increasingly compelling prospects for buyers prepared to manage extended timelines and expanded inventory selections.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

December 4, 2025

November 19, 2025

October 21, 2025

September 24, 2025

September 23, 2025

You've got questions and we can't wait to answer them.