November Market Update

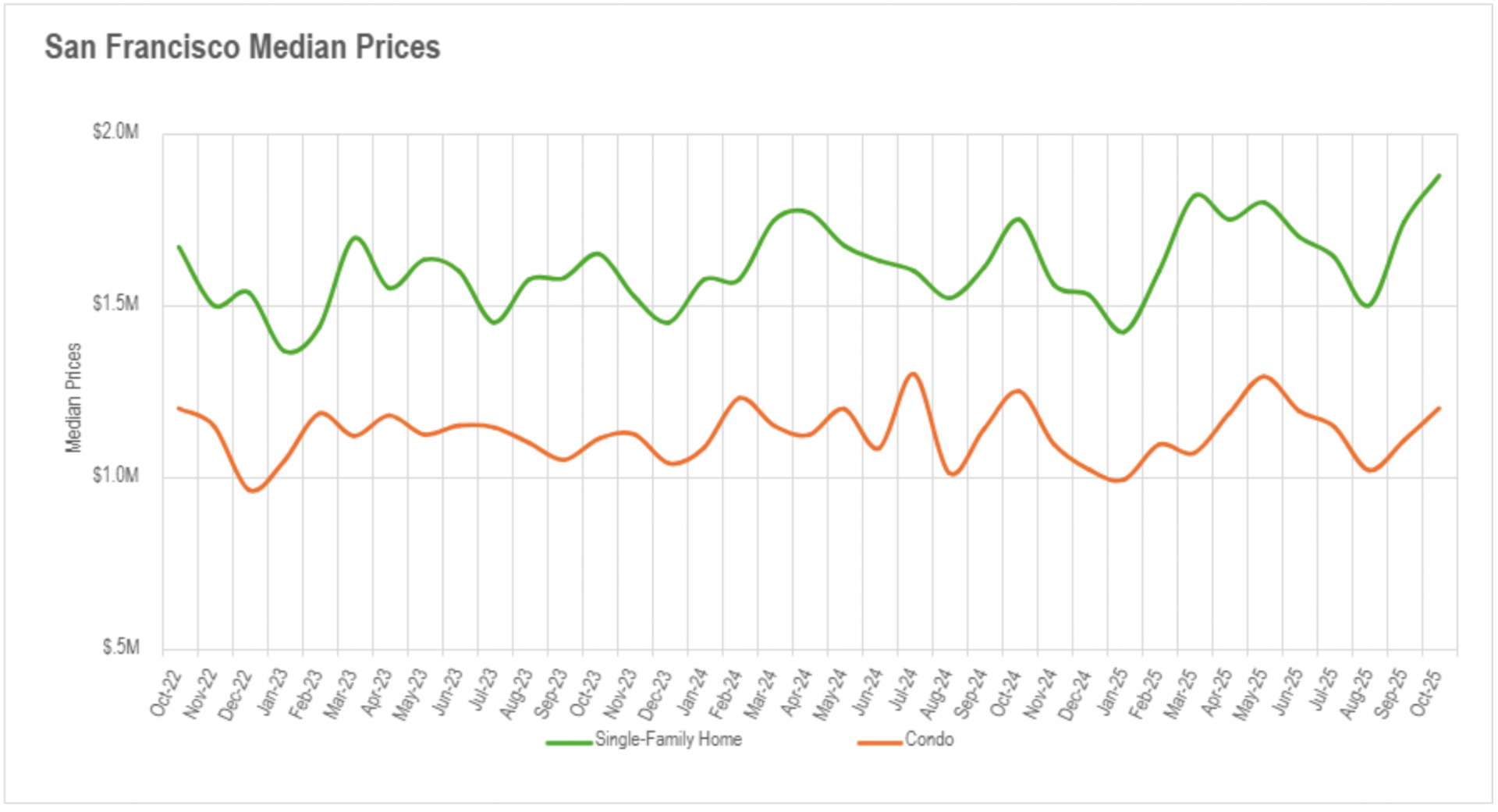

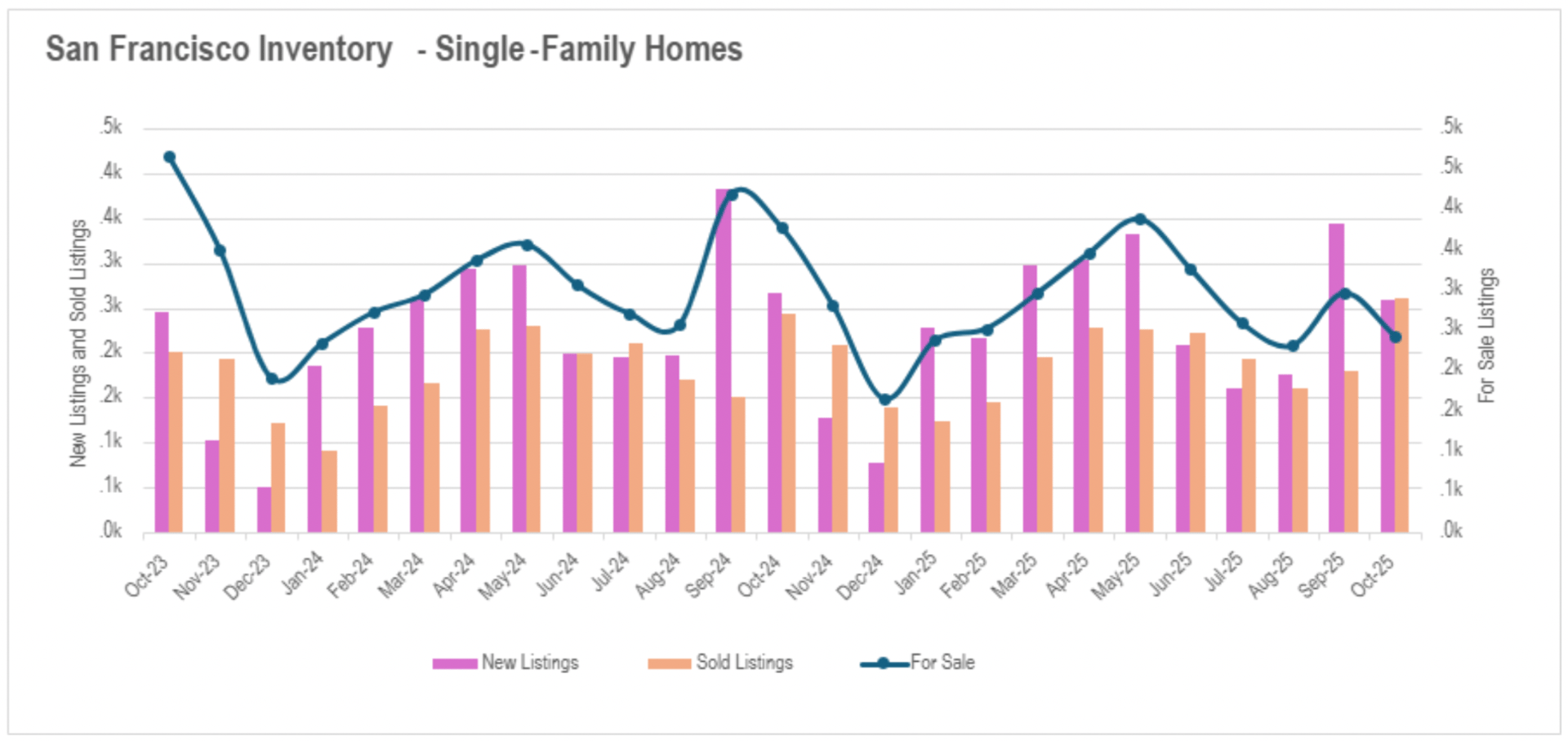

San Francisco attains extraordinary market compression with single-family properties achieving two-year value peaks and availability declining over 35% annually, while both property categories decisively establish seller-favorable status.

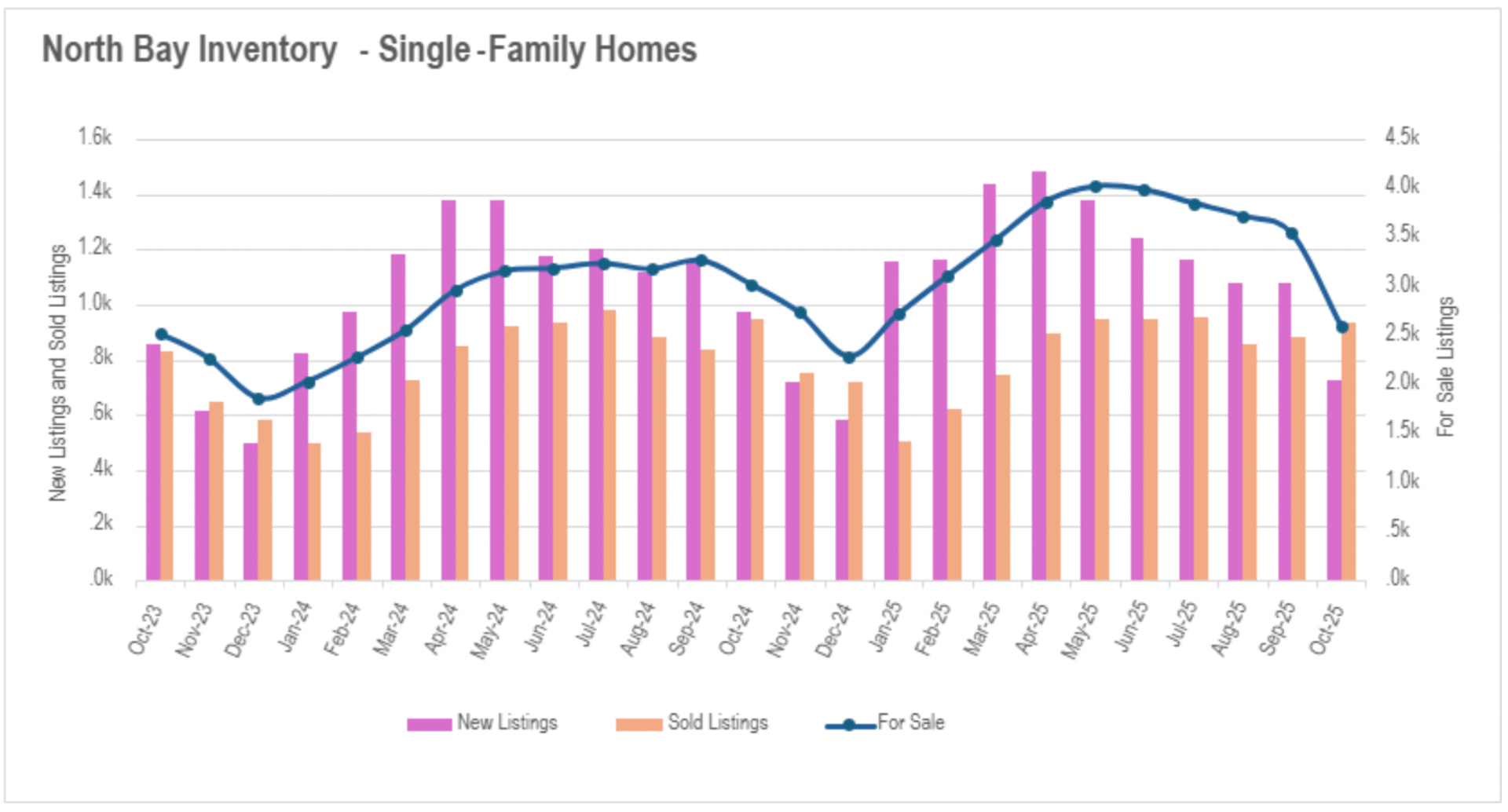

The Bay Area witnesses a substantial "availability overcompensation" in October, with most regions transitioning from elevated summer levels to subnormal supply, propelled primarily by pronounced reductions in new listings rather than enhanced transaction volume.

Condominium sectors throughout the region encounter escalating challenges with extensive value retreats and substantially prolonged marketing periods, particularly in Silicon Valley where certain markets observe listings requiring more than double the previous duration to transact.

The property category distinction amplifies as single-family properties sustain exceptionally competitive environments with expeditious transactions, while condominiums face extended marketing cycles despite advantageous buyer circumstances.

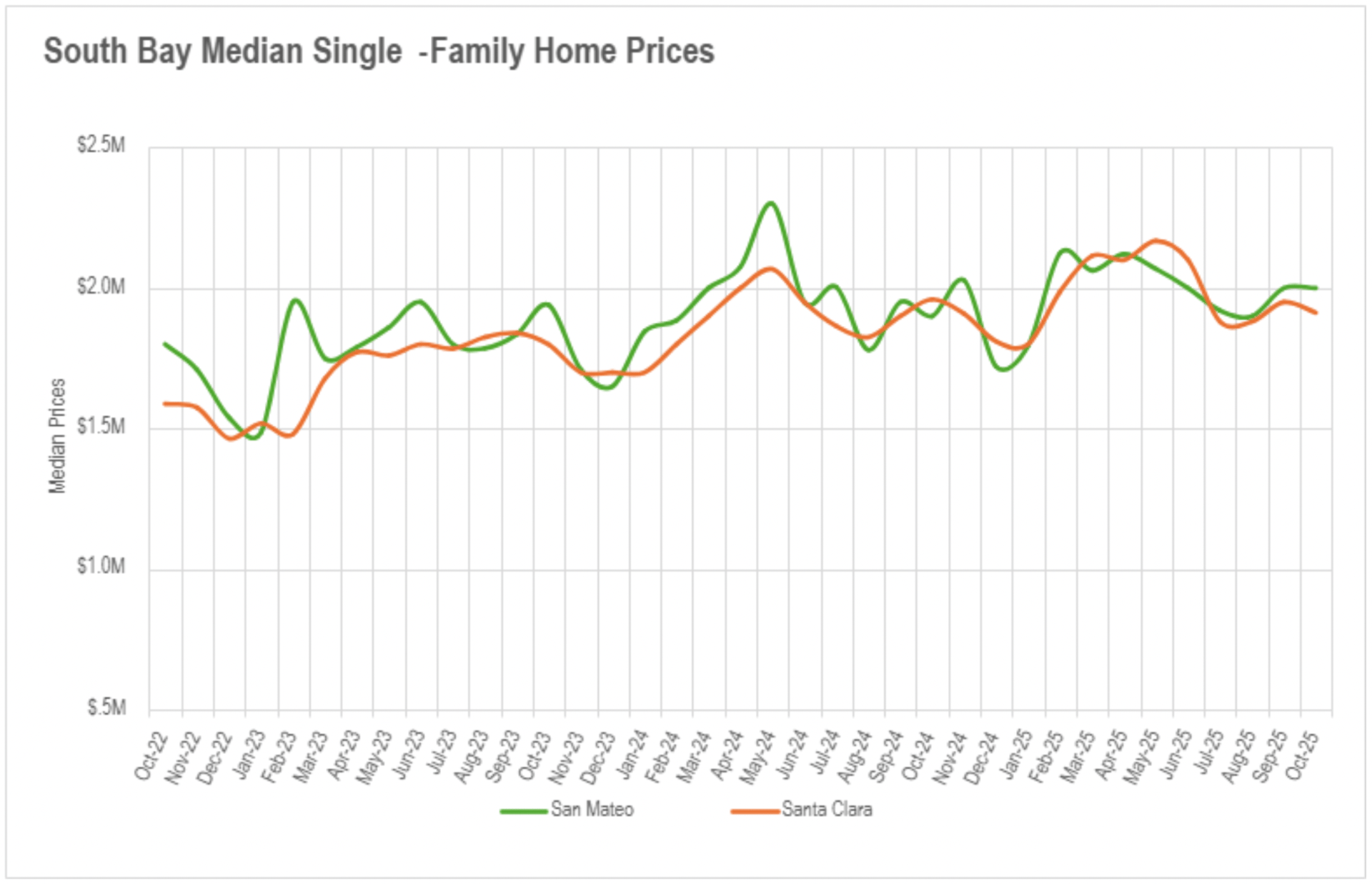

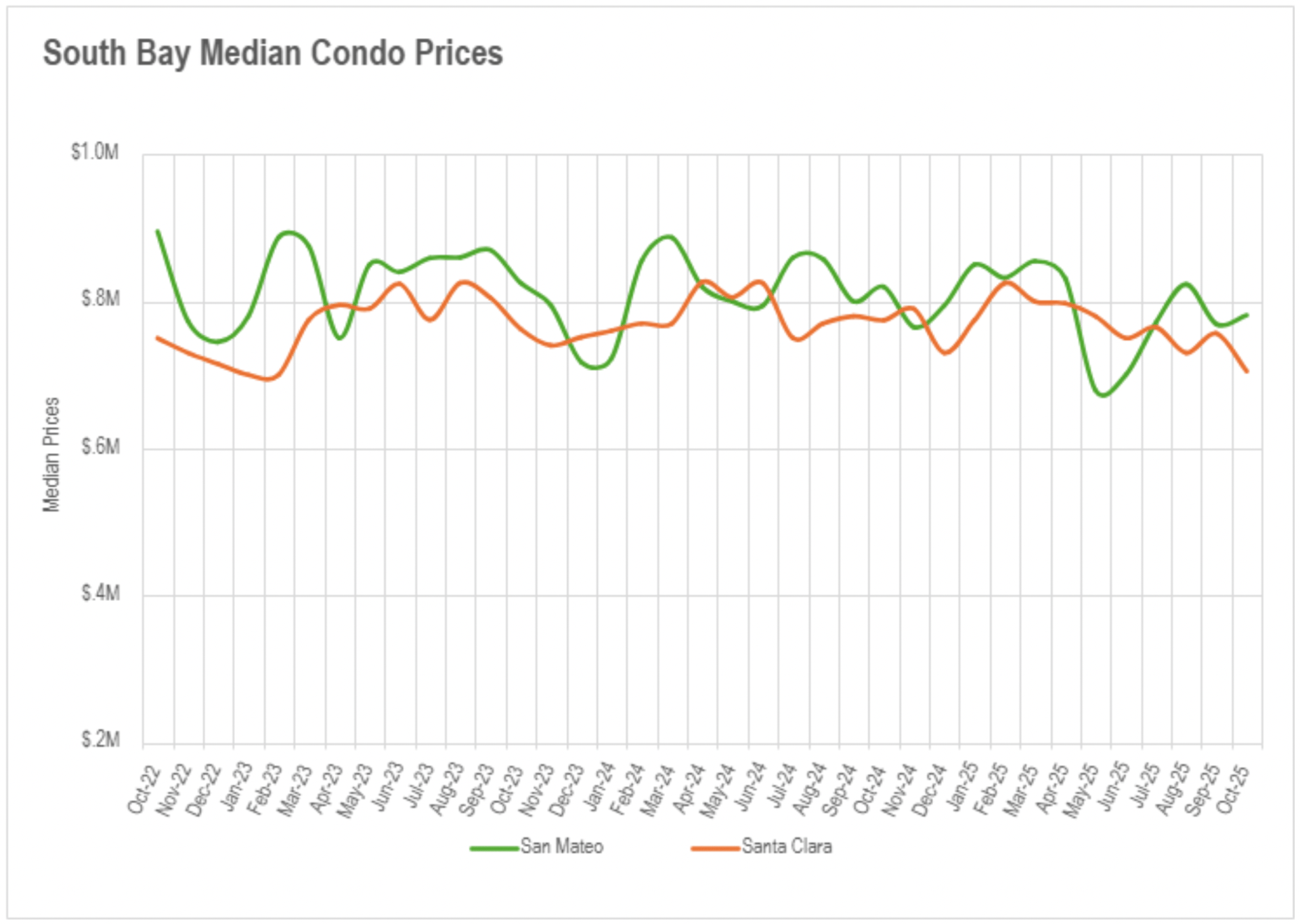

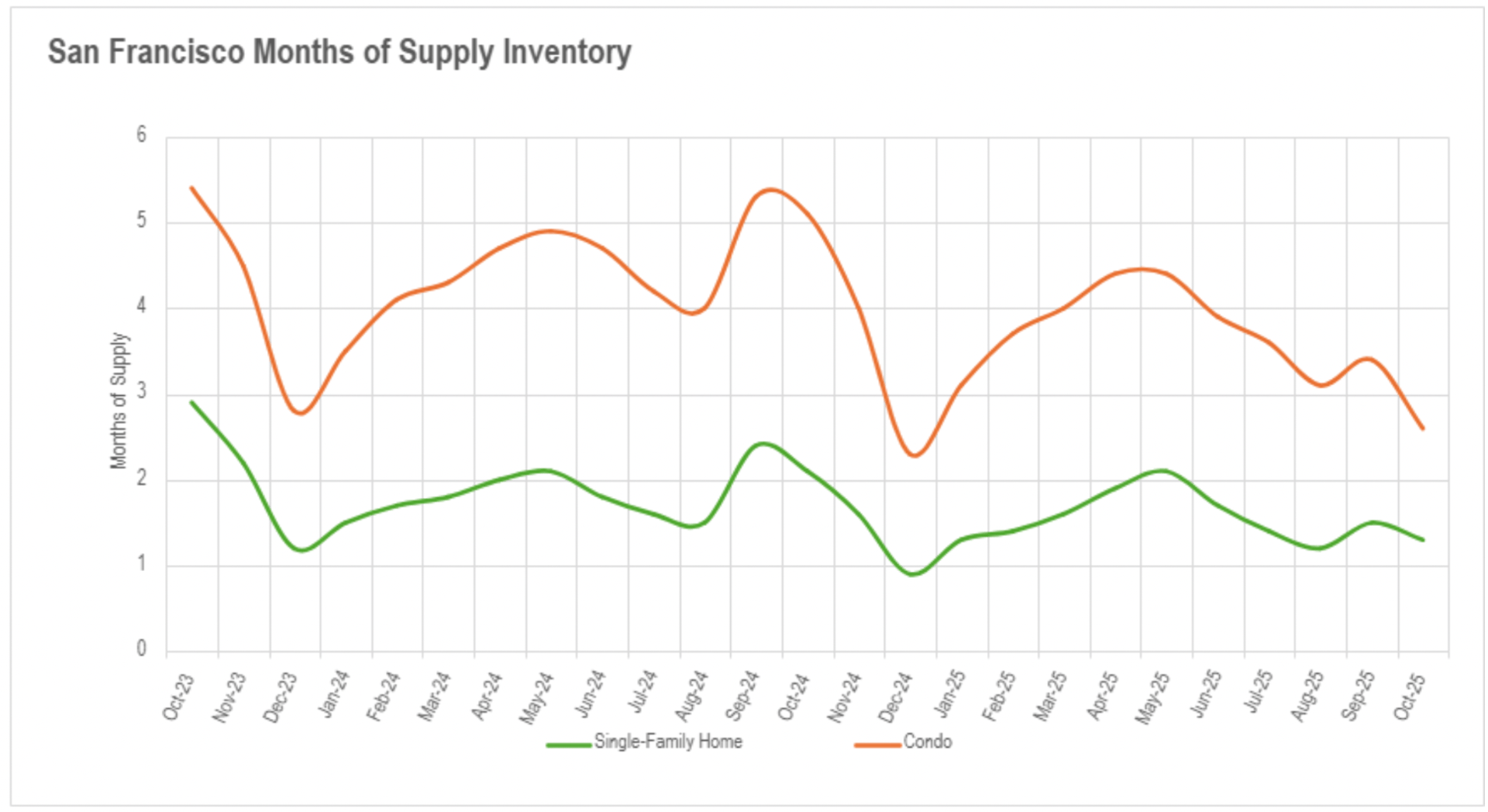

October highlighted San Francisco's exceptional market momentum, with single-family properties achieving their elevated median transaction value in two years, representing a 7.29% annual increase. The typical single-family property transacts for 114.2% of asking value, while condominiums exchange at 101.9% of asking - establishing a significant departure from earlier months. Nevertheless, this San Francisco strength contrasts sharply with extensive condominium vulnerability throughout other Bay Area regions. Silicon Valley recorded especially acute condominium retreats, with San Mateo declining 4.73%, Santa Clara plummeting 8.97%, and Santa Cruz collapsing 18.77% annually.

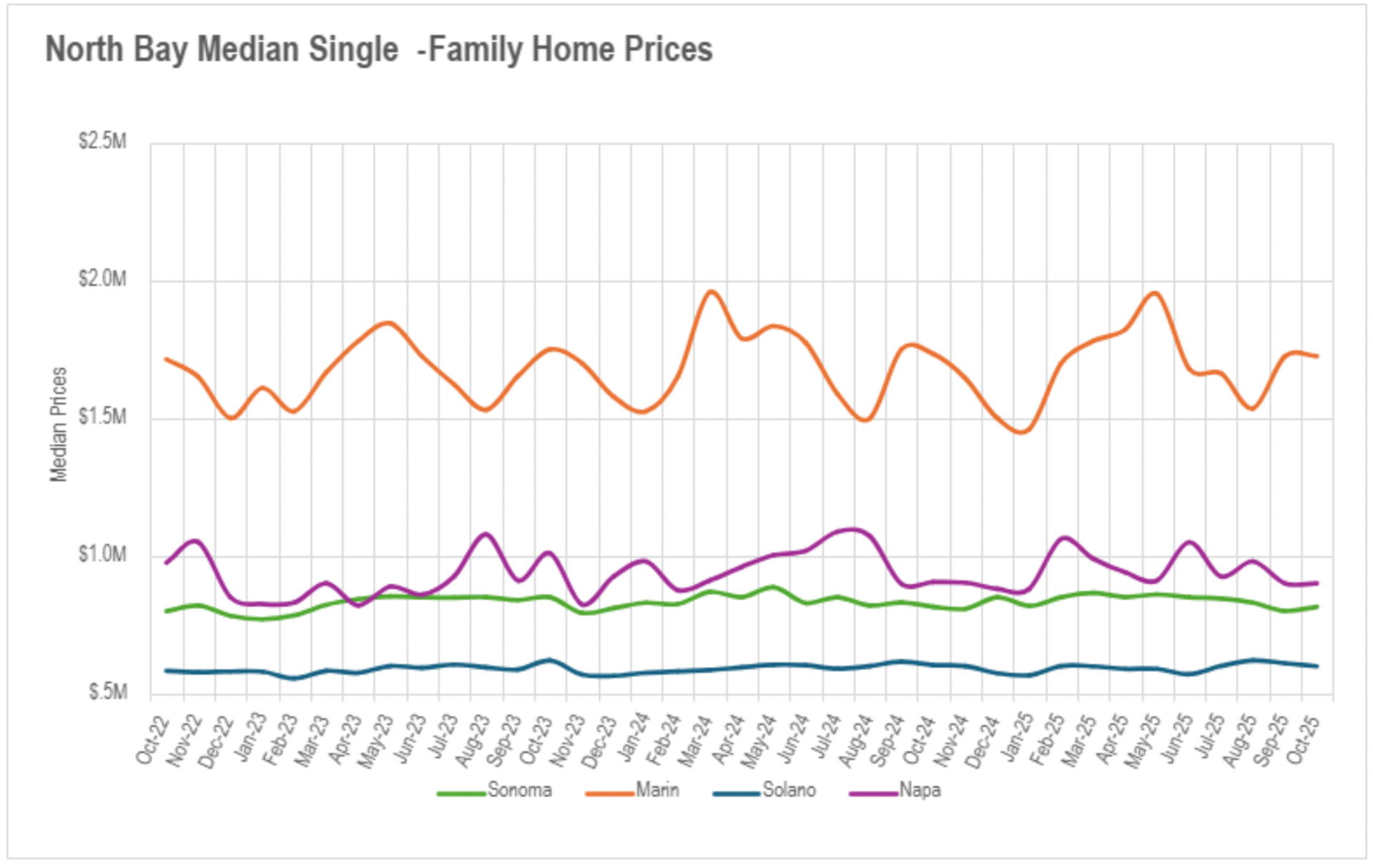

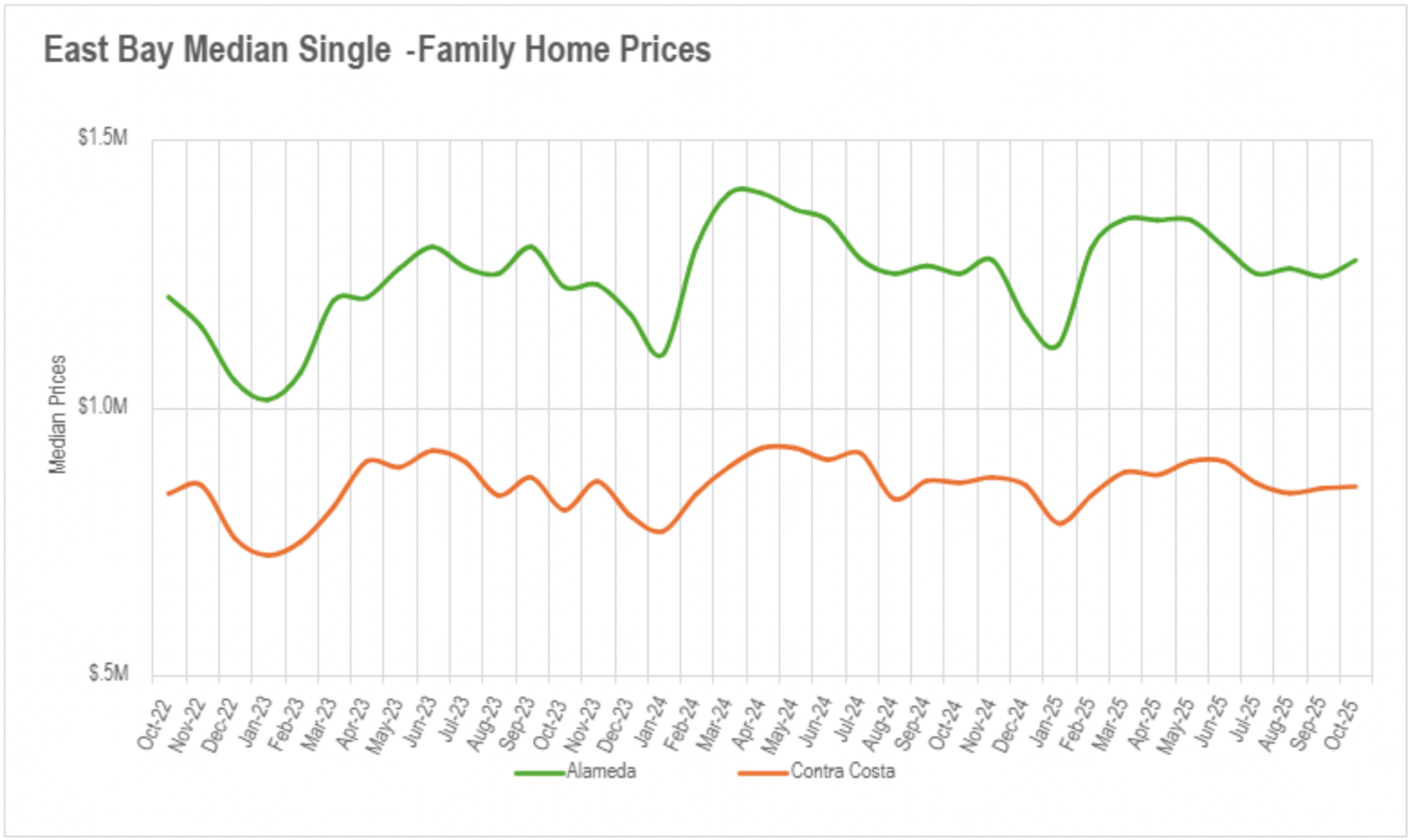

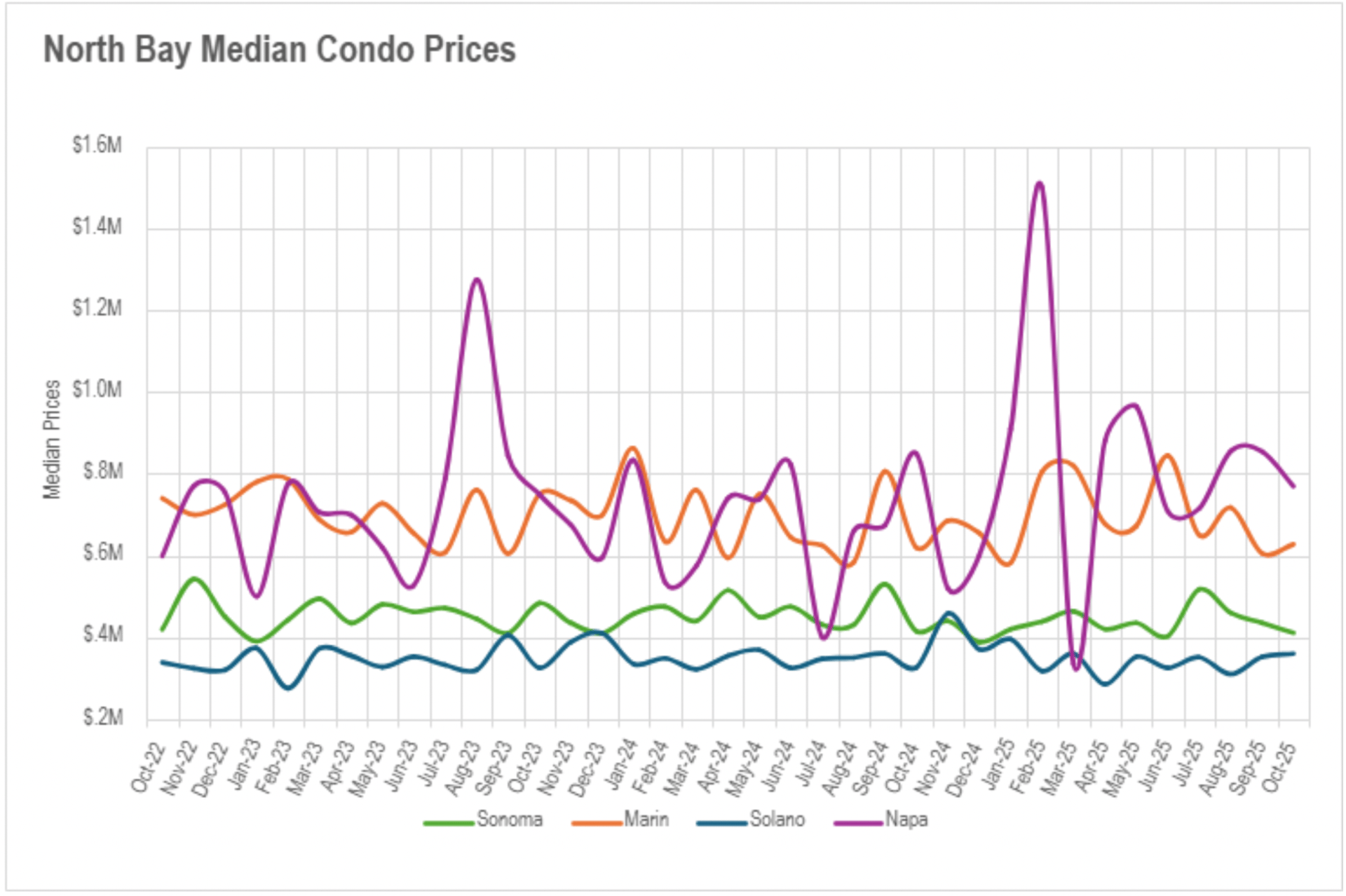

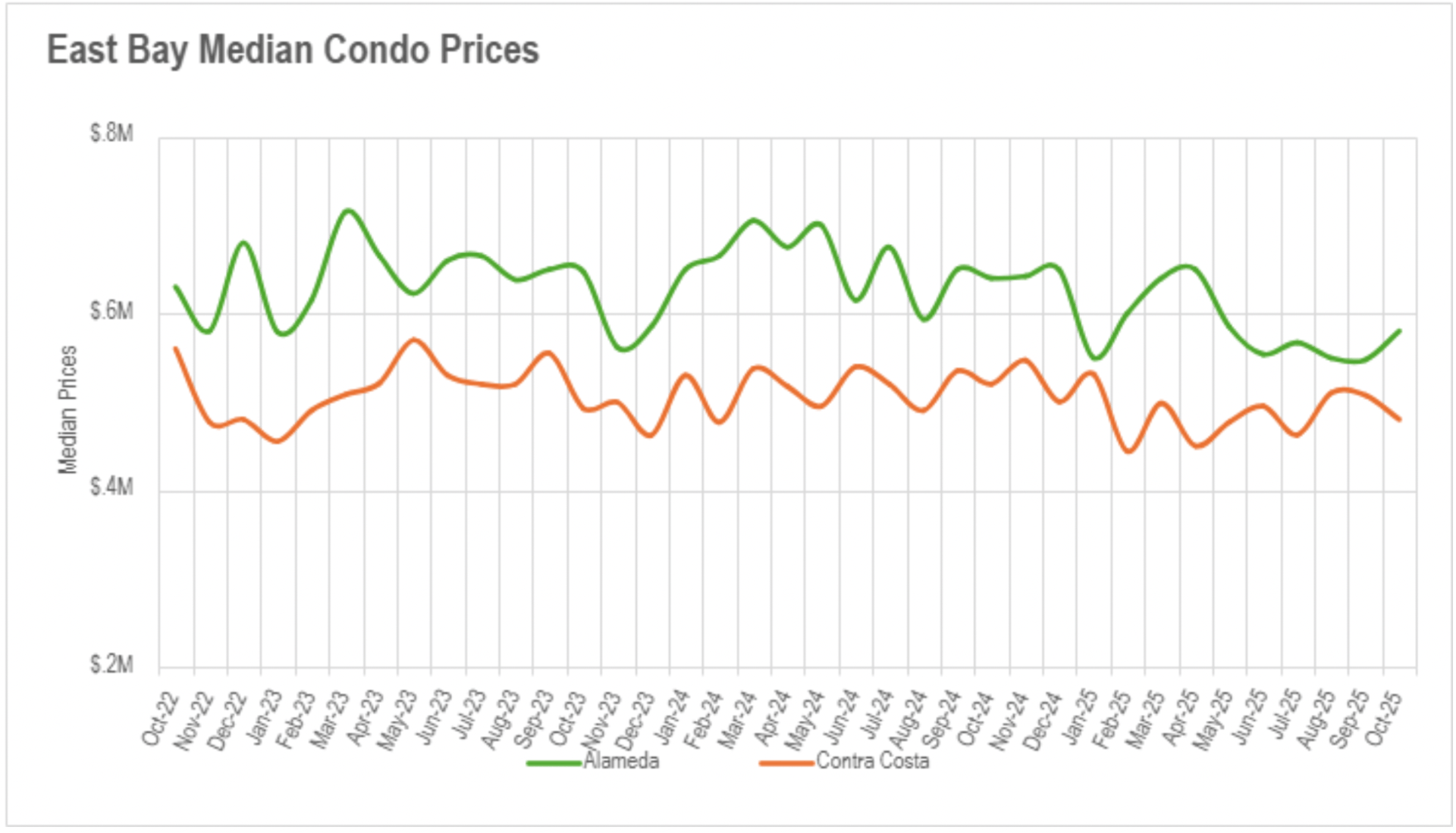

Single-family properties in Silicon Valley exhibited greater steadiness, with San Mateo advancing 5.26%, while Santa Clara and Santa Cruz declined moderately by 2.42% and 3.33% respectively. East Bay markets demonstrated minimal fluctuation in single-family values, with Alameda advancing 2.00% and Contra Costa declining just 0.81%, though condominiums prolonged their declining trajectory with retreats of 9.38% and 7.69% respectively. North Bay regions displayed exceptional value steadiness overall, with single-family properties and condominiums in most counties exchanging within their established parameters, though significant fluctuation materialized in certain condominium sectors - Solano County jumped 10.26% while Napa County declined 9.49%.

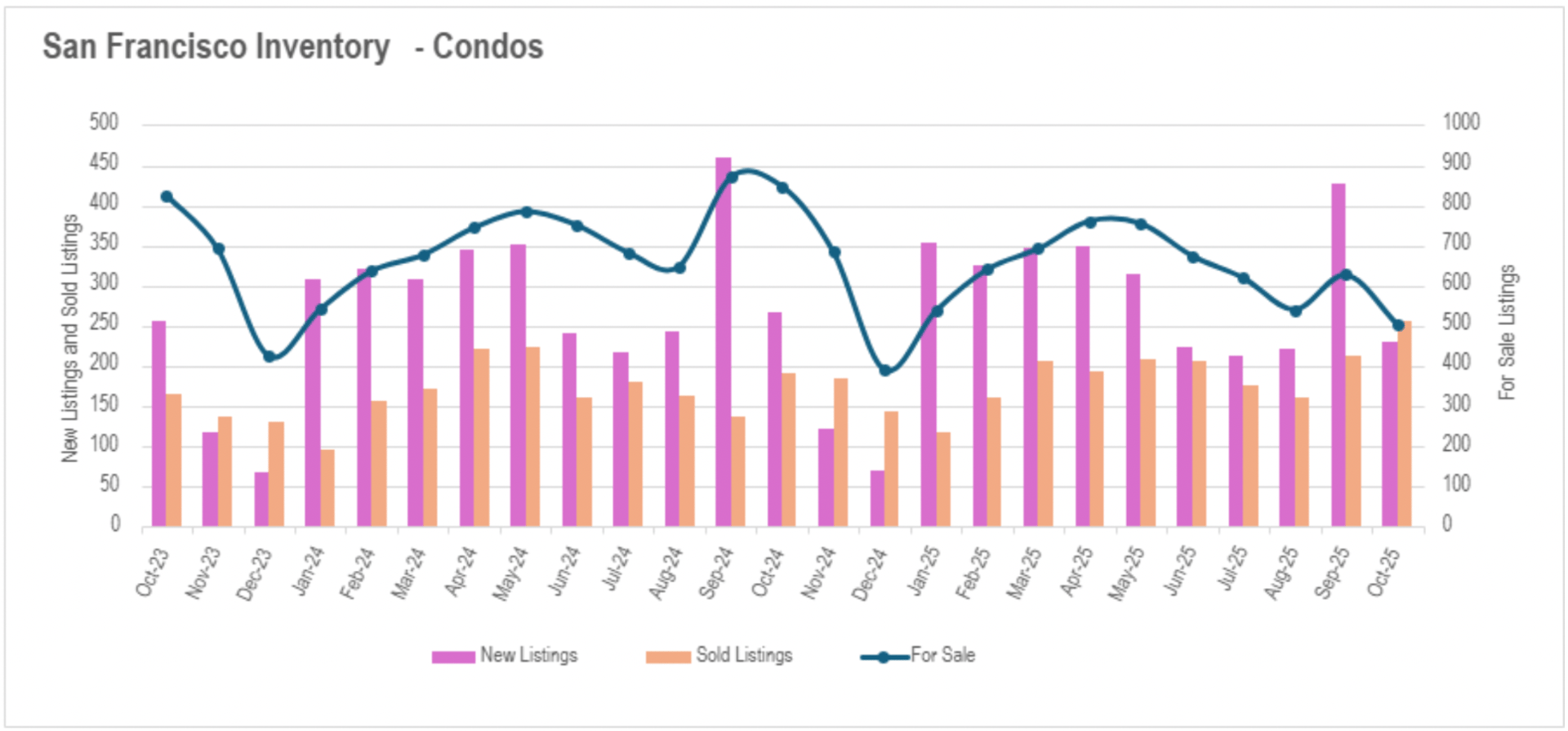

October constituted a pronounced reversal in Bay Area availability trajectories, with most regions transitioning from elevated summer levels to meaningful annual shortfalls. San Francisco commanded this transformation with the most extreme compression, as single-family availability plummeted 35.54% and condominium supply crashed 40.68% below previous year levels. This substantial decline produced months of supply contracting to 1.3 for single-family properties (declining 38.10% annually) and 2.6 for condominiums (declining 49.02%), establishing both property categories decisively into seller-favorable territory for the initial time in recent memory.

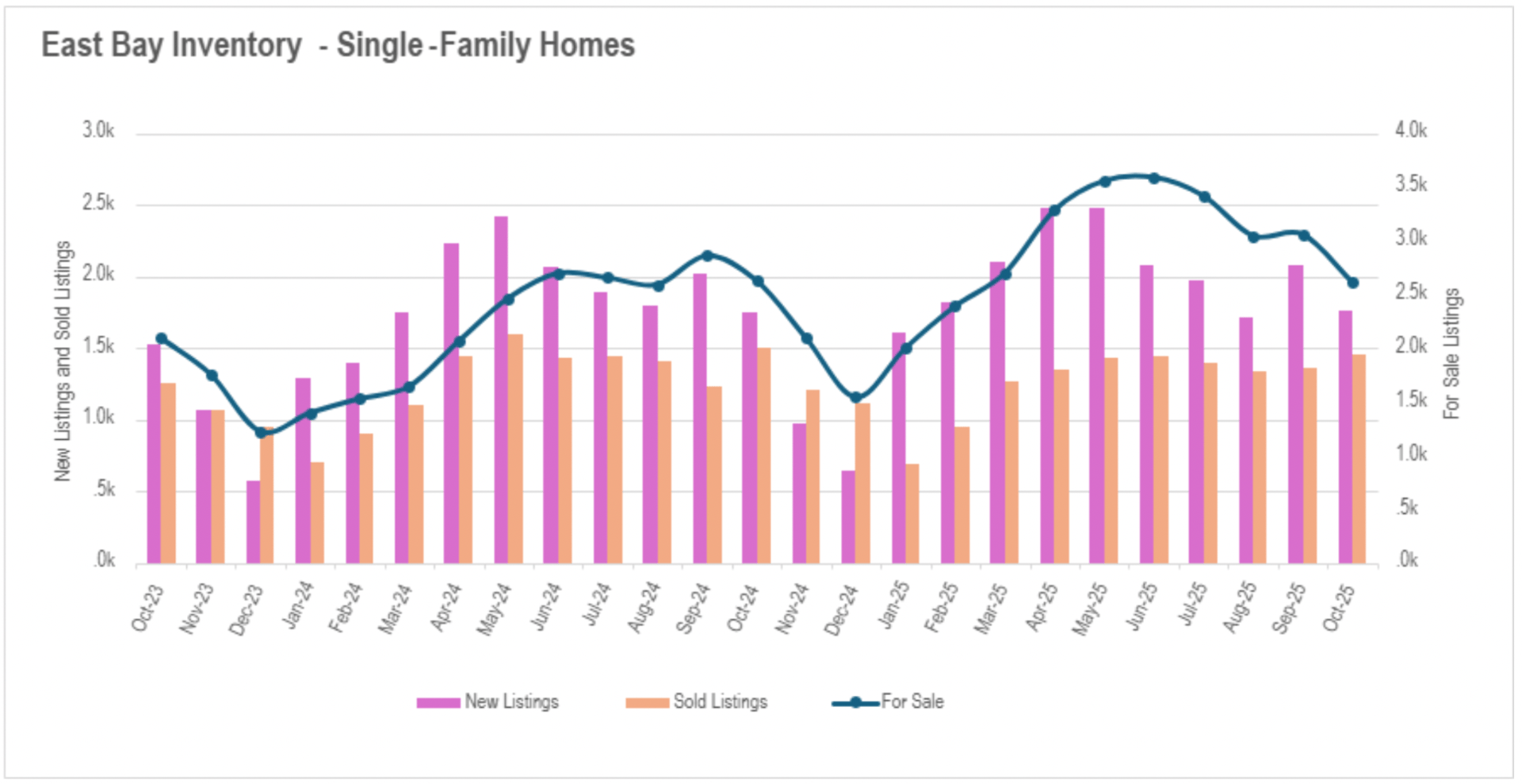

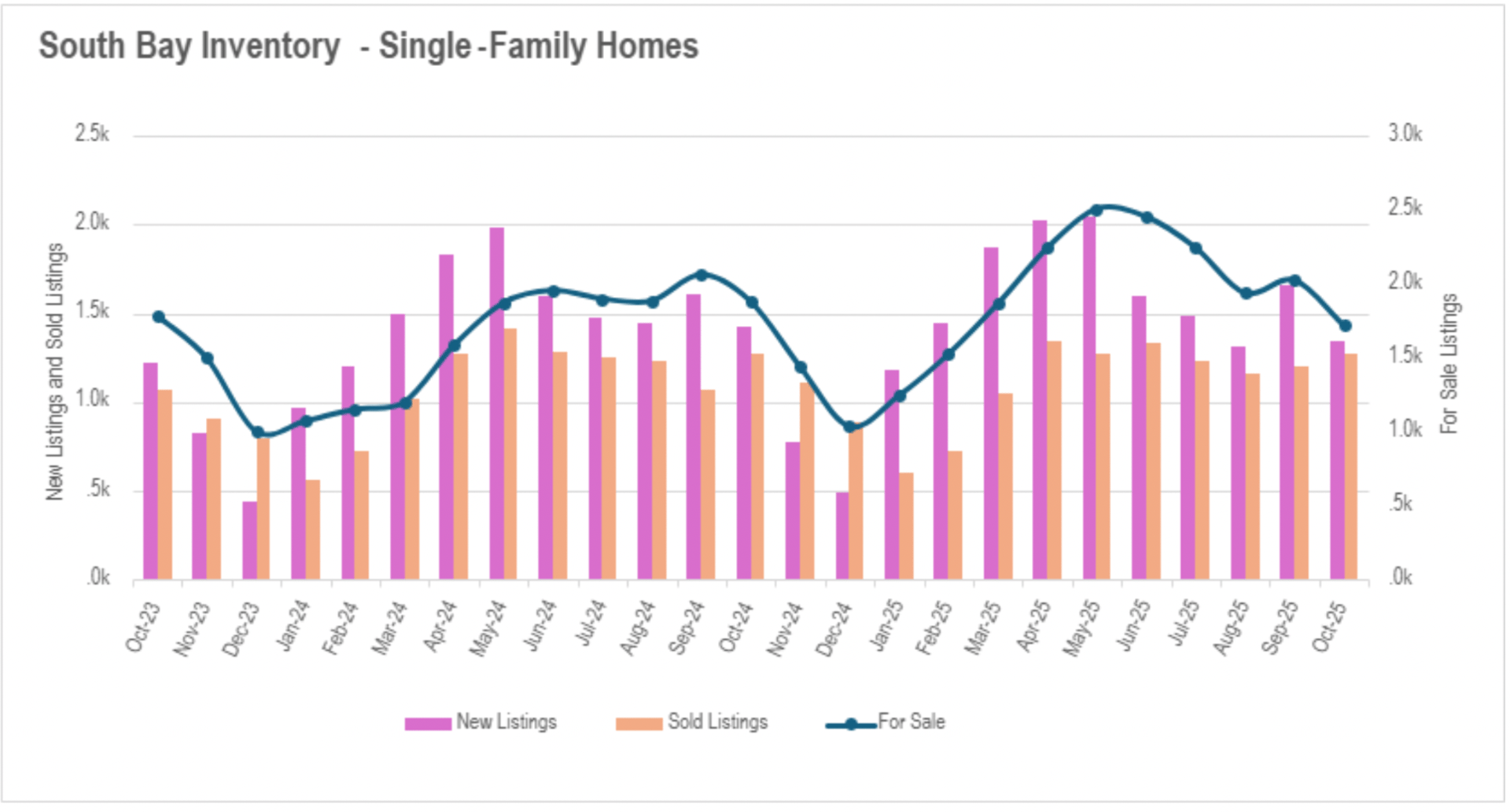

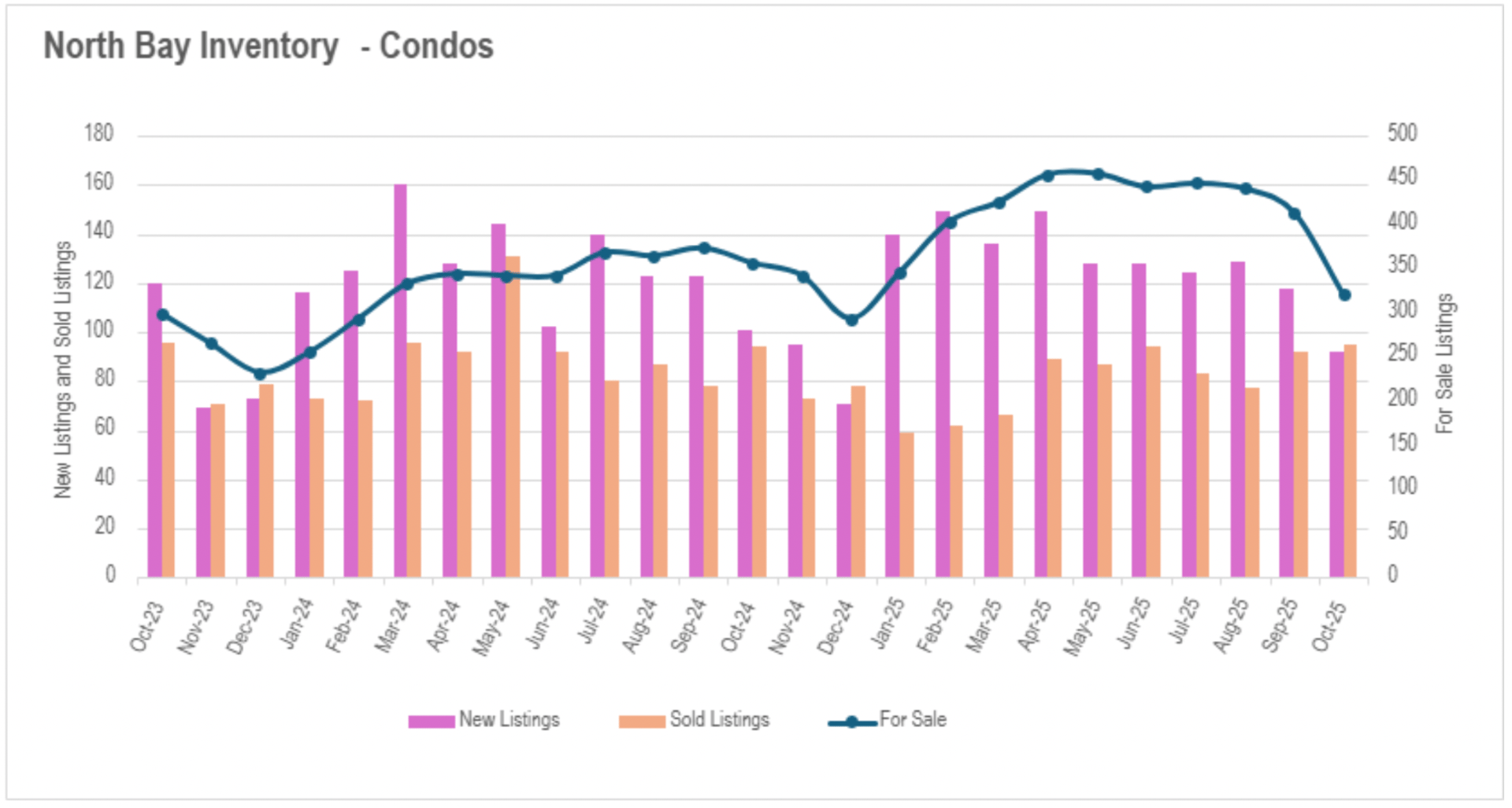

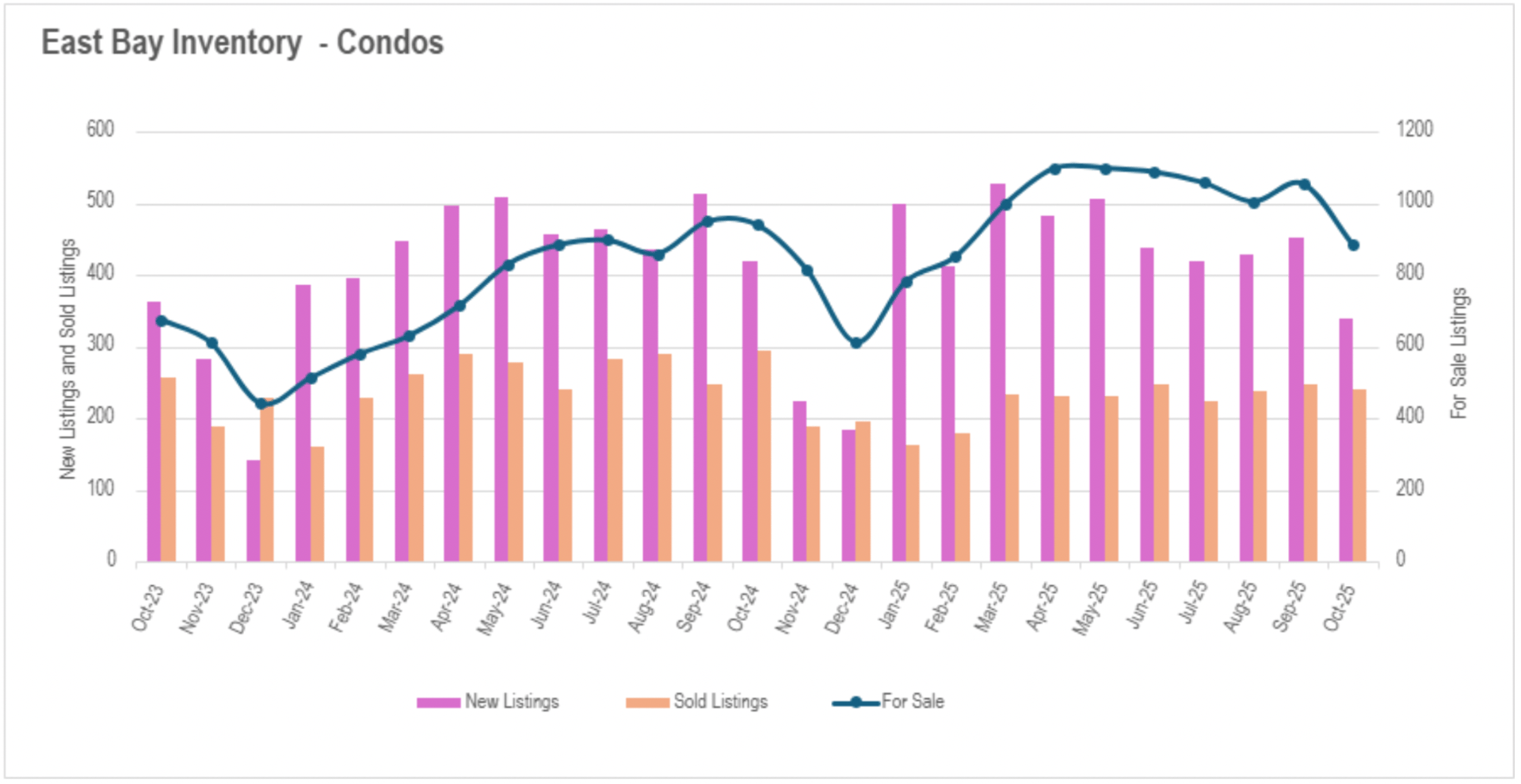

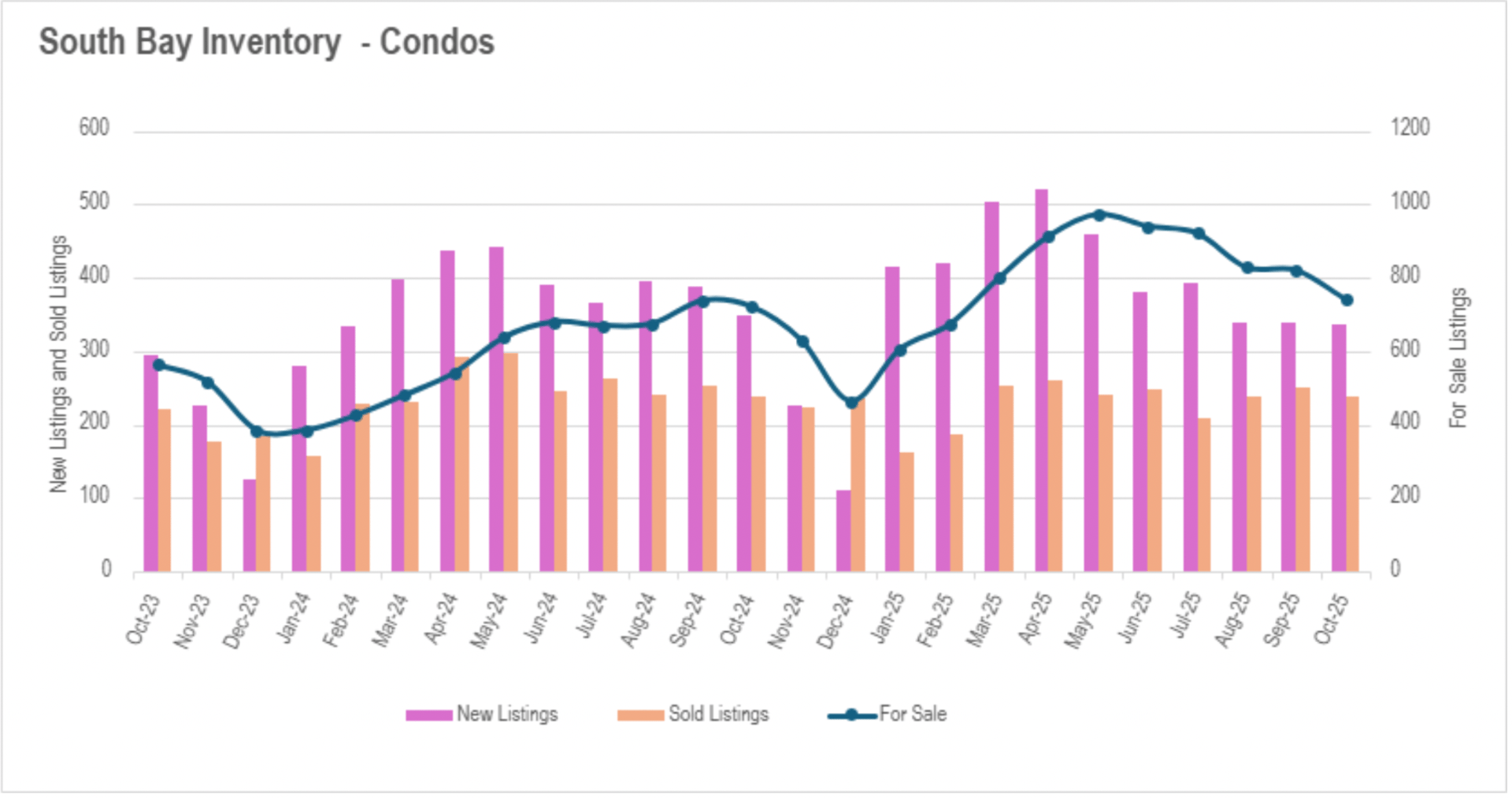

Silicon Valley's single-family sector completed its availability reversal, concluding October with 8.72% reduced active listings than last year and 15.22% reduced than the prior month, propelled by 5.89% reduced new listings entering the market. The condominium sector demonstrated a more moderate adjustment at 2.77% above last year. North Bay regions recorded similarly substantial transitions, with single-family availability declining 14.06% and condominiums declining 10.11% annually, propelled primarily by pronounced 25.41% and 8.91% reductions in new listings for each property category respectively. East Bay markets represented the singular exception with relatively unchanged availability levels, though the condominium sector exhibited compelling developments with 19.05% reduced listings introduced and 5.85% diminished active availability, indicating a potential transition point.

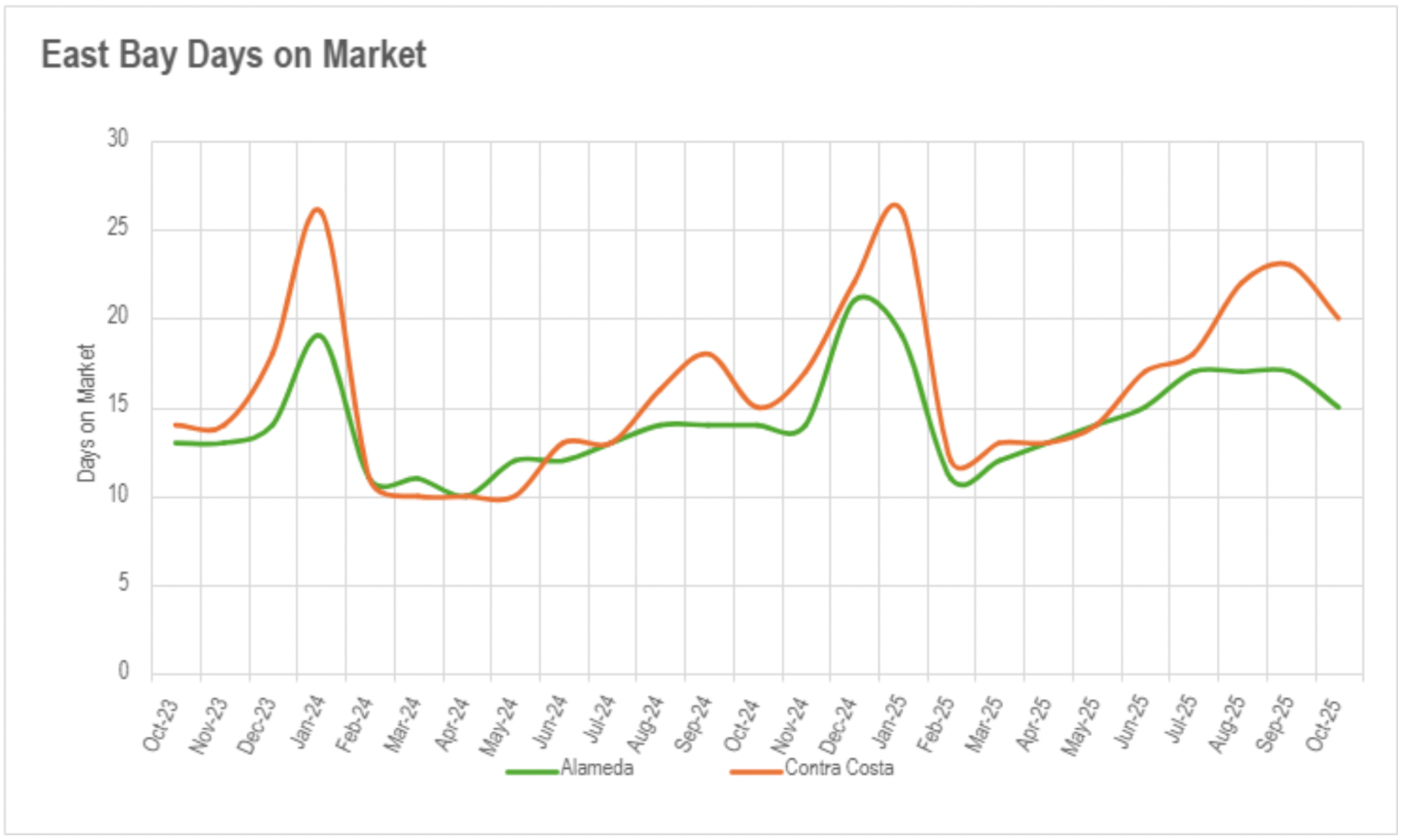

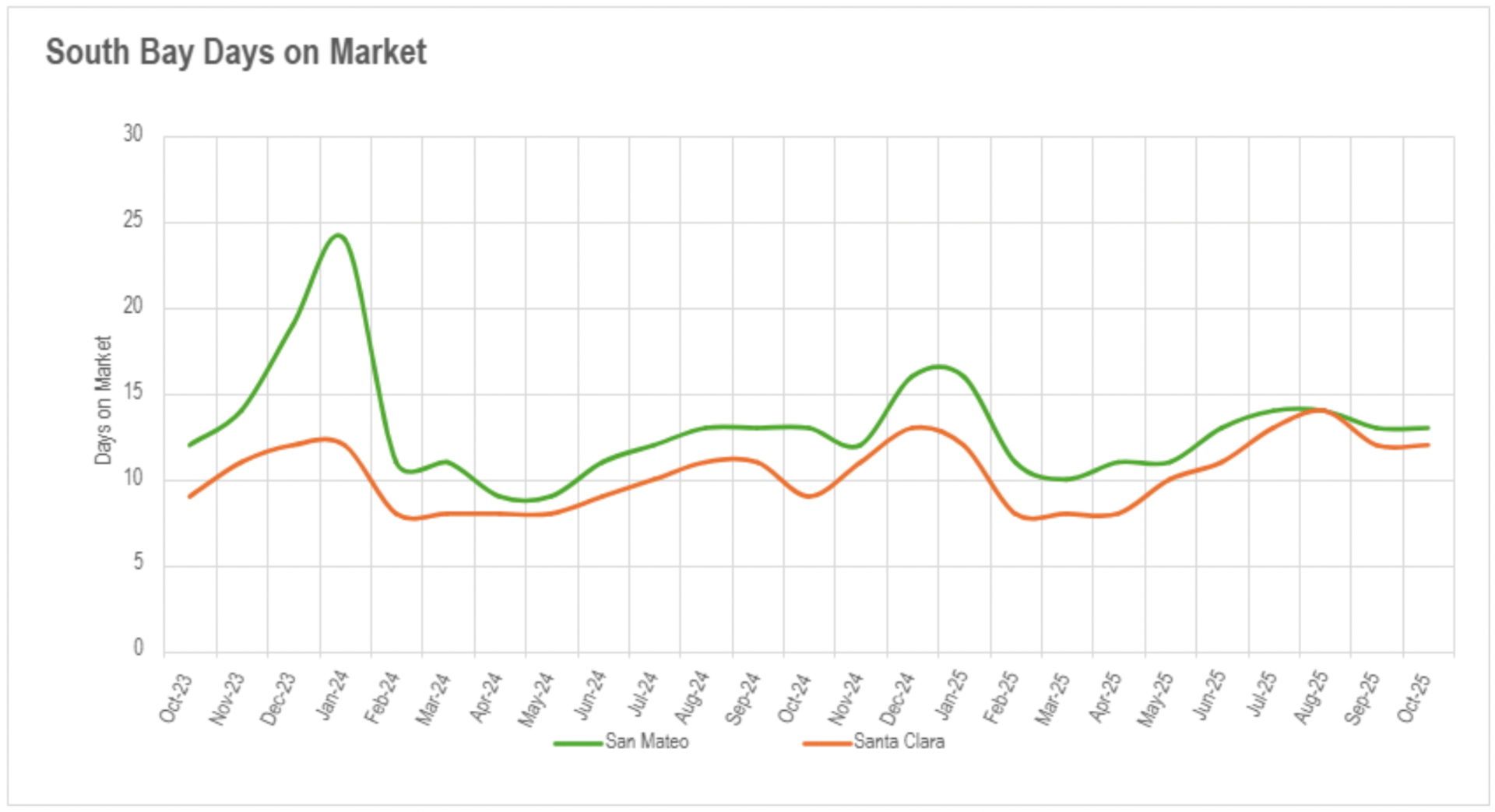

October unveiled a compelling divergence between percentage increases in marketing duration and actual transaction efficiency, with the condominium sector displaying especially substantial extensions. San Francisco sustained relatively expeditious movement with single-family properties averaging 14 days (advancing 7.69% annually) and condominiums at 26 days (advancing 13.04%), though both figures represent modest increases as availability compresses further. Silicon Valley presented the most pronounced contrasts, with single-family properties in San Mateo and Santa Clara transacting in merely 12-13 days while condominiums faced acute delays - San Mateo condominiums now average 32 days (advancing 39.13%), while Santa Clara and Santa Cruz condominiums require 41 and 69 days on market respectively, representing dramatic annual increases of 105% and 155.56%.

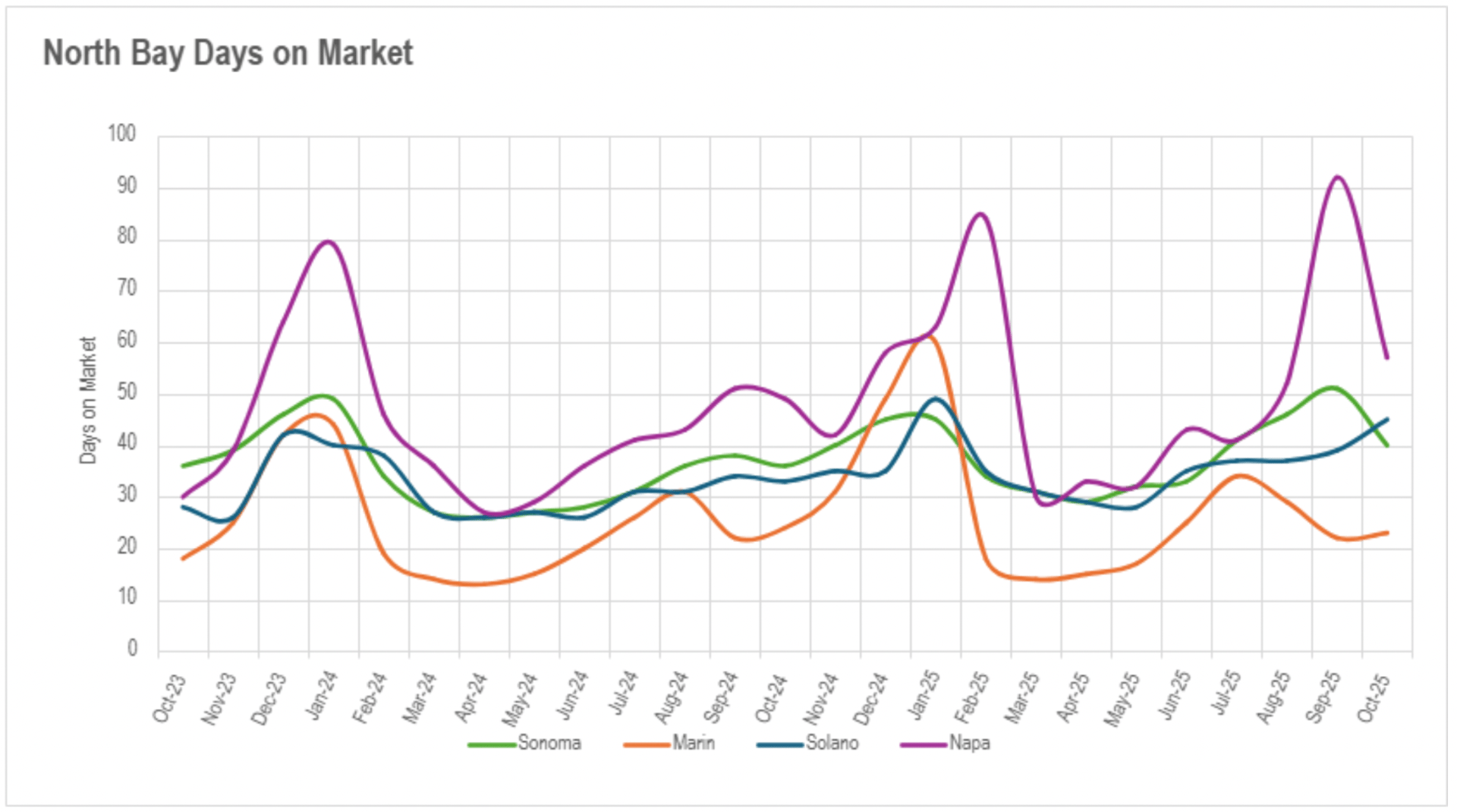

East Bay markets exhibited meaningful percentage increases but preserved relatively expeditious absolute durations for single-family properties at 15 days in Alameda (advancing 7.14%) and 20 days in Contra Costa (advancing 33.33%), while condominiums extended to 30 and 41 days with 50.00% and 78.26% annual increases. North Bay regions displayed the most varied outcomes, with most counties demonstrating moderate increases of 11-36%, though Marin County notably recorded a 4.17% reduction. This configuration indicates that while buyer discrimination has intensified across markets, the tangible influence on transaction efficiency differs considerably by property category and geography.

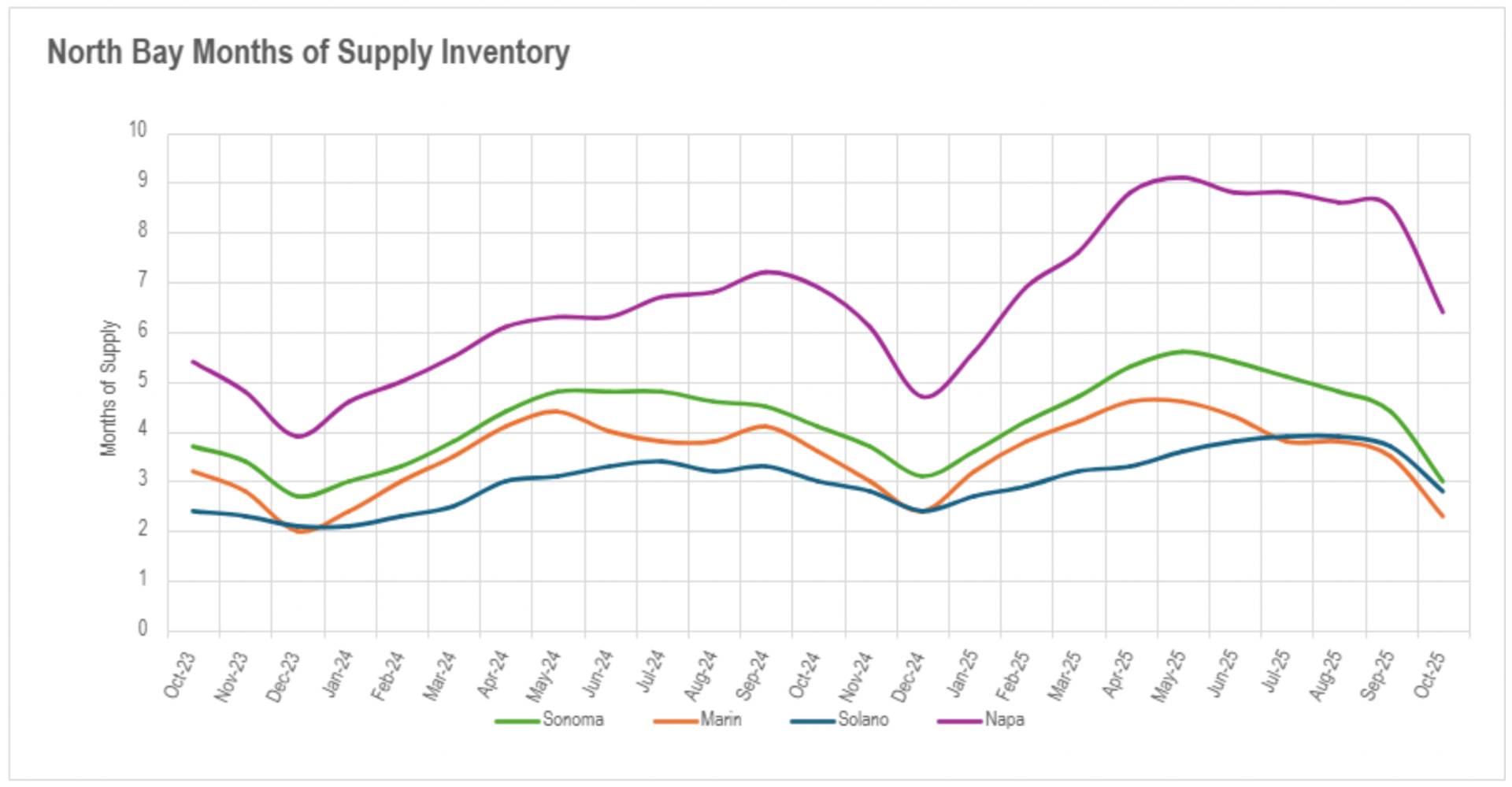

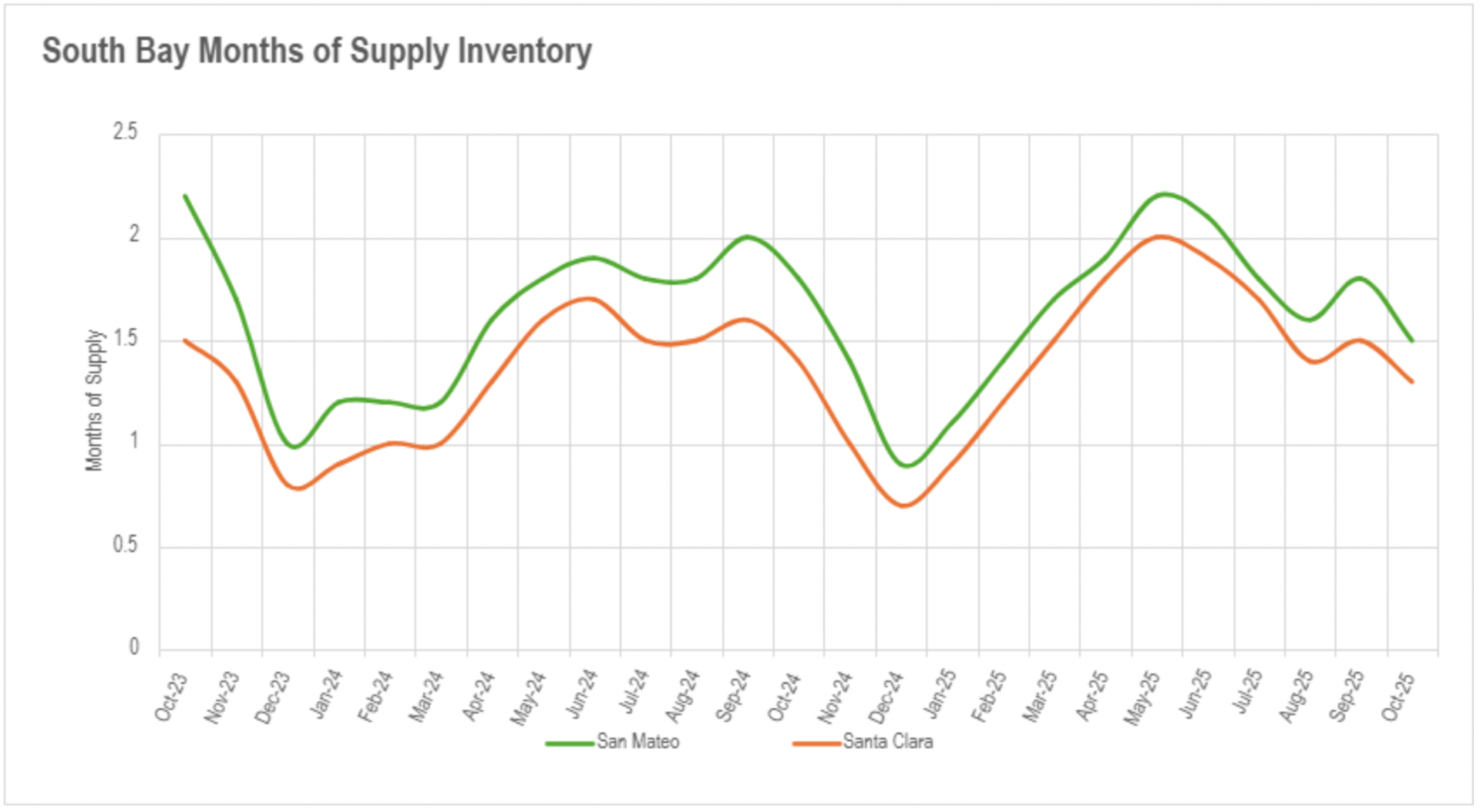

October's availability overcompensation accelerated the Bay Area's substantial transition toward seller-controlled markets, with several regions achieving extraordinary levels of supply limitation. San Francisco accomplished exceptional status with both property categories decisively in seller-favorable territory - single-family properties at an exceptionally minimal 1.3 months of supply and condominiums at 2.6 months, representing the most constrained condominium market San Francisco has documented in recent years. Silicon Valley preserved its conventional exceptionally competitive single-family position with San Mateo at 1.5 months and Santa Clara at an extraordinarily constrained 1.3 months, while Santa Cruz continues progressing back toward balanced conditions at 3.5 months. The Silicon Valley condominium sector displays indications of stabilization, with San Mateo establishing perfect equilibrium at precisely 3.0 months, while Santa Clara (3.2 months) and Santa Cruz (4.2 months) remain in buyer territory but progressing toward balance.

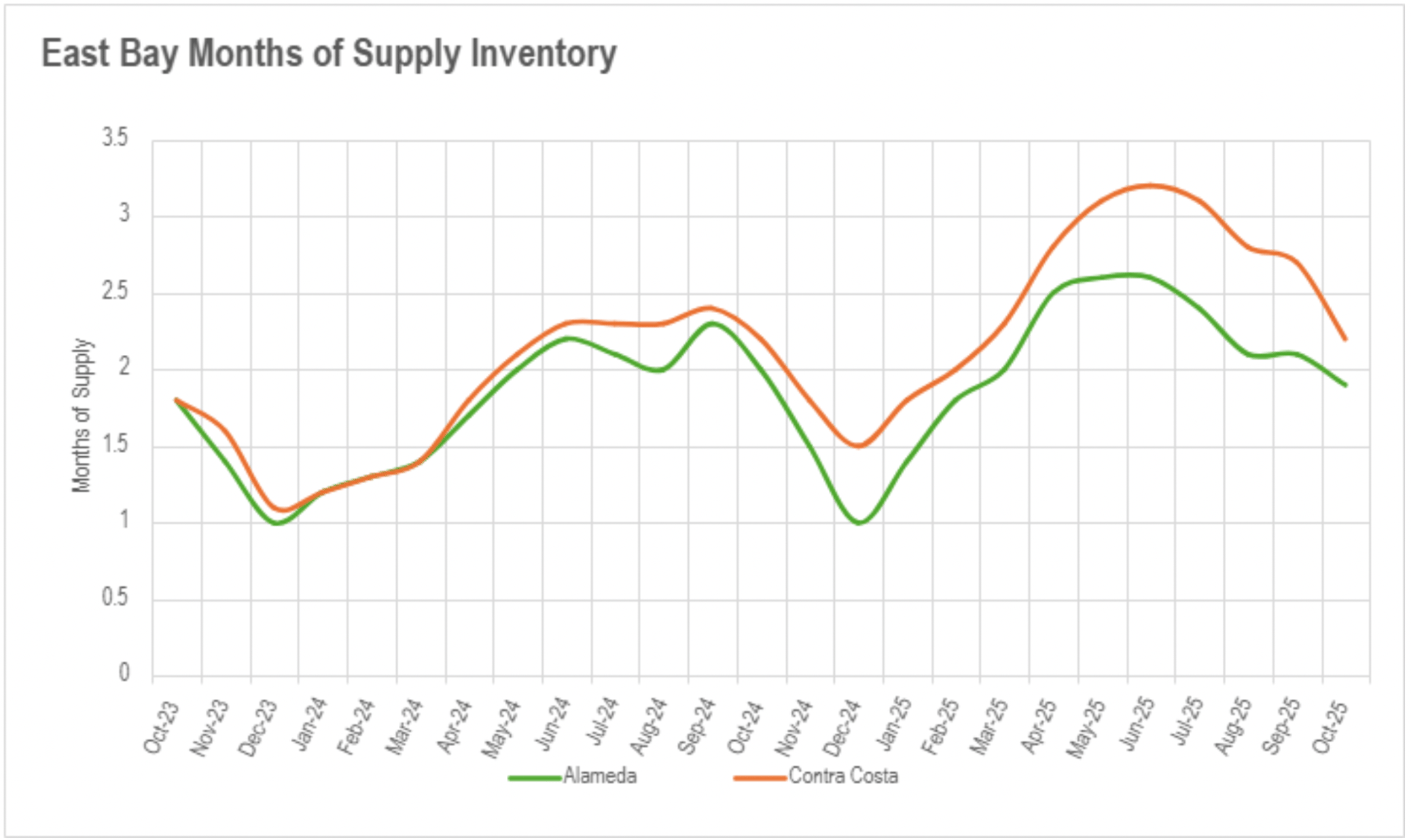

North Bay regions accomplished the most substantial transformation, with Marin and Solano Counties' single-family sectors transitioning to seller-favorable markets at 2.3 and 2.8 months respectively, while Sonoma established perfect equilibrium at 3.0 months and Napa perpetuated its progression toward balance at 6.4 months. North Bay condominiums also transitioned decisively, with Sonoma achieving perfect equilibrium at 3.0 months and other counties advancing consistently in that trajectory. East Bay markets maintained their conventional market architecture with single-family properties supporting sellers at 1.9 months in Alameda and 2.2 months in Contra Costa, while condominiums remained buyer-advantageous at 4.4 and 3.4 months respectively. This regionwide configuration indicates the Bay Area has commenced a renewed phase of supply limitation that could endure through winter months and into 2026.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

June 27, 2026

June 27, 2026

June 20, 2026

June 11, 2026

June 5, 2026

May 23, 2026

May 15, 2026

May 1, 2026

April 24, 2026

You've got questions and we can't wait to answer them.