December Market Update

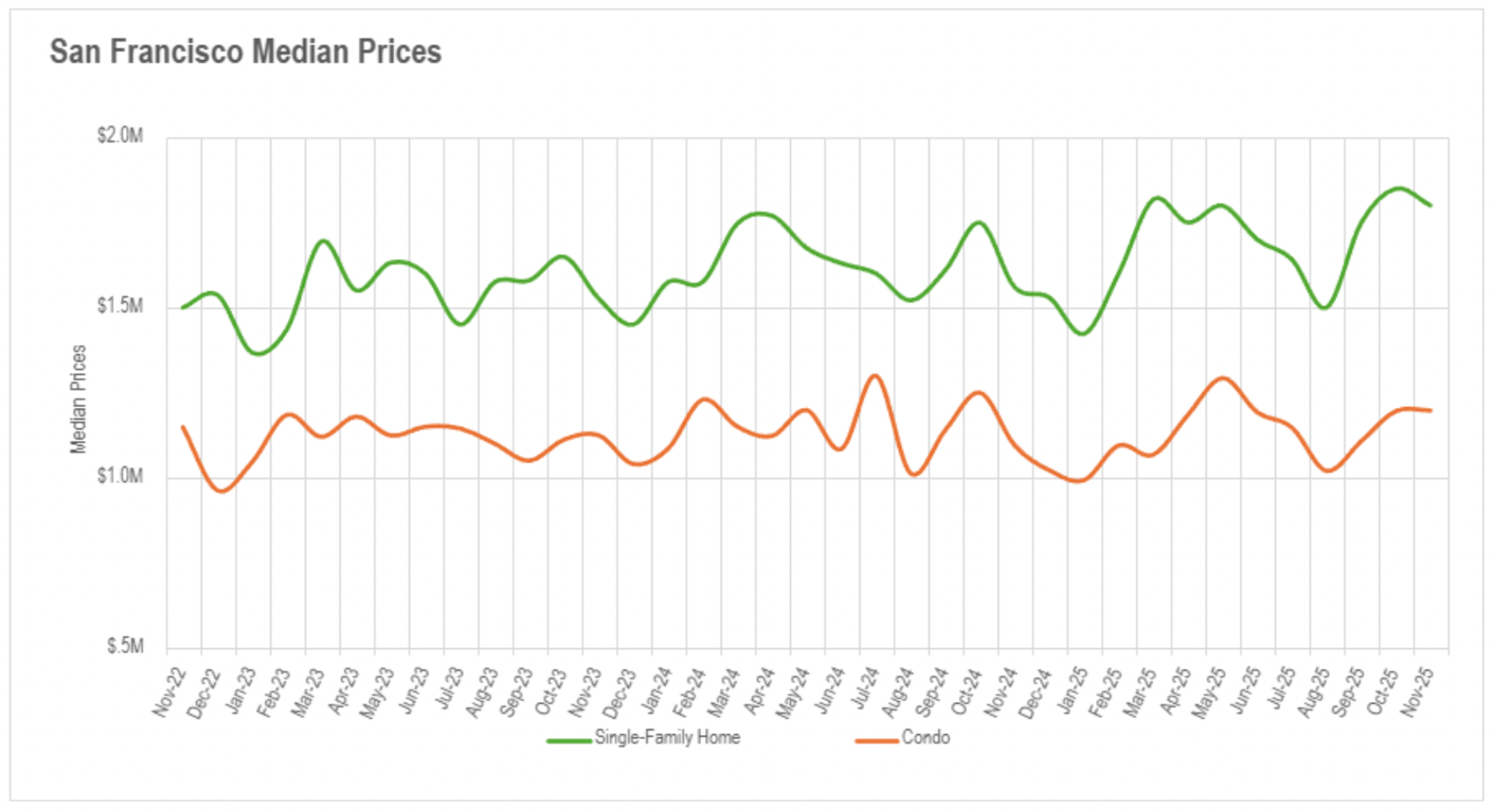

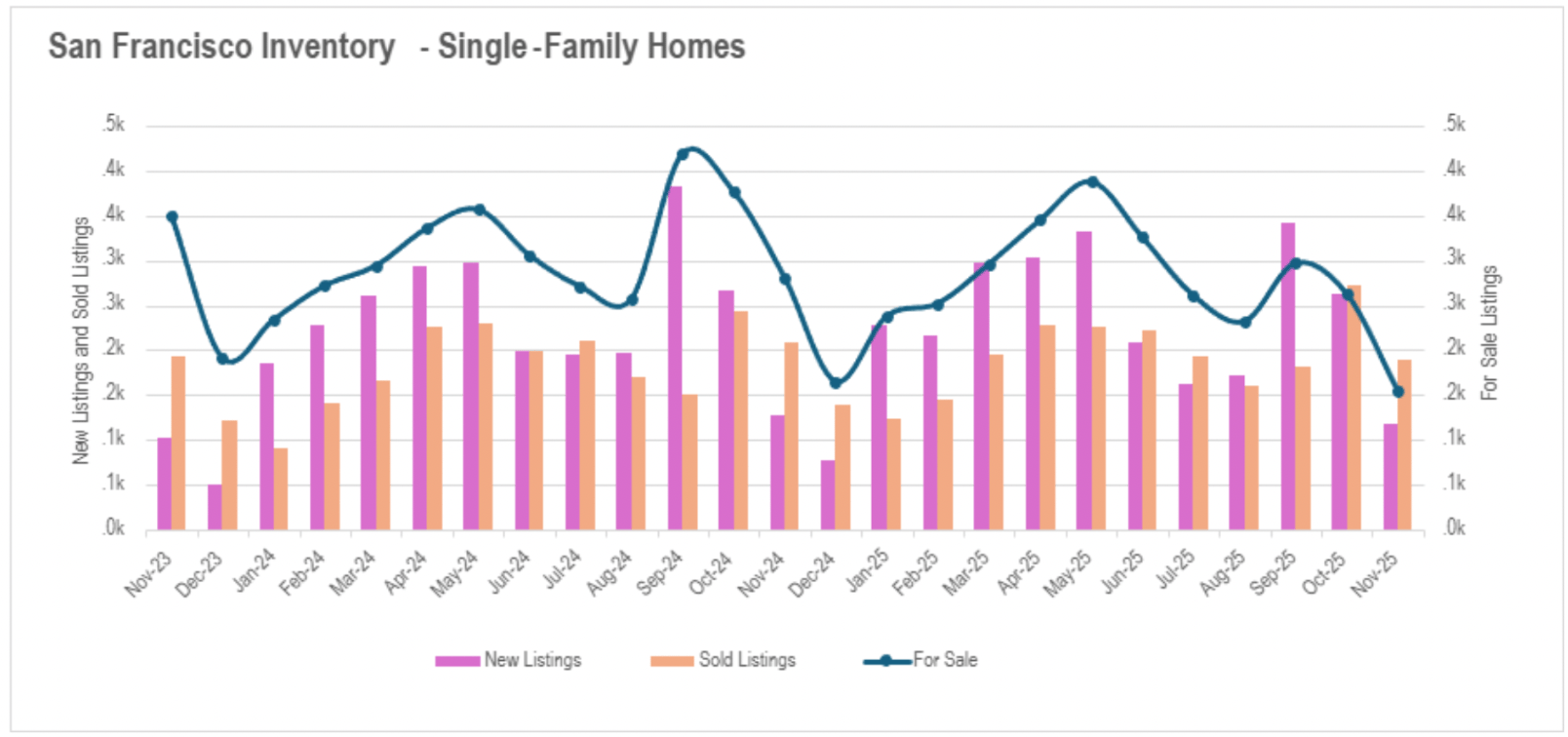

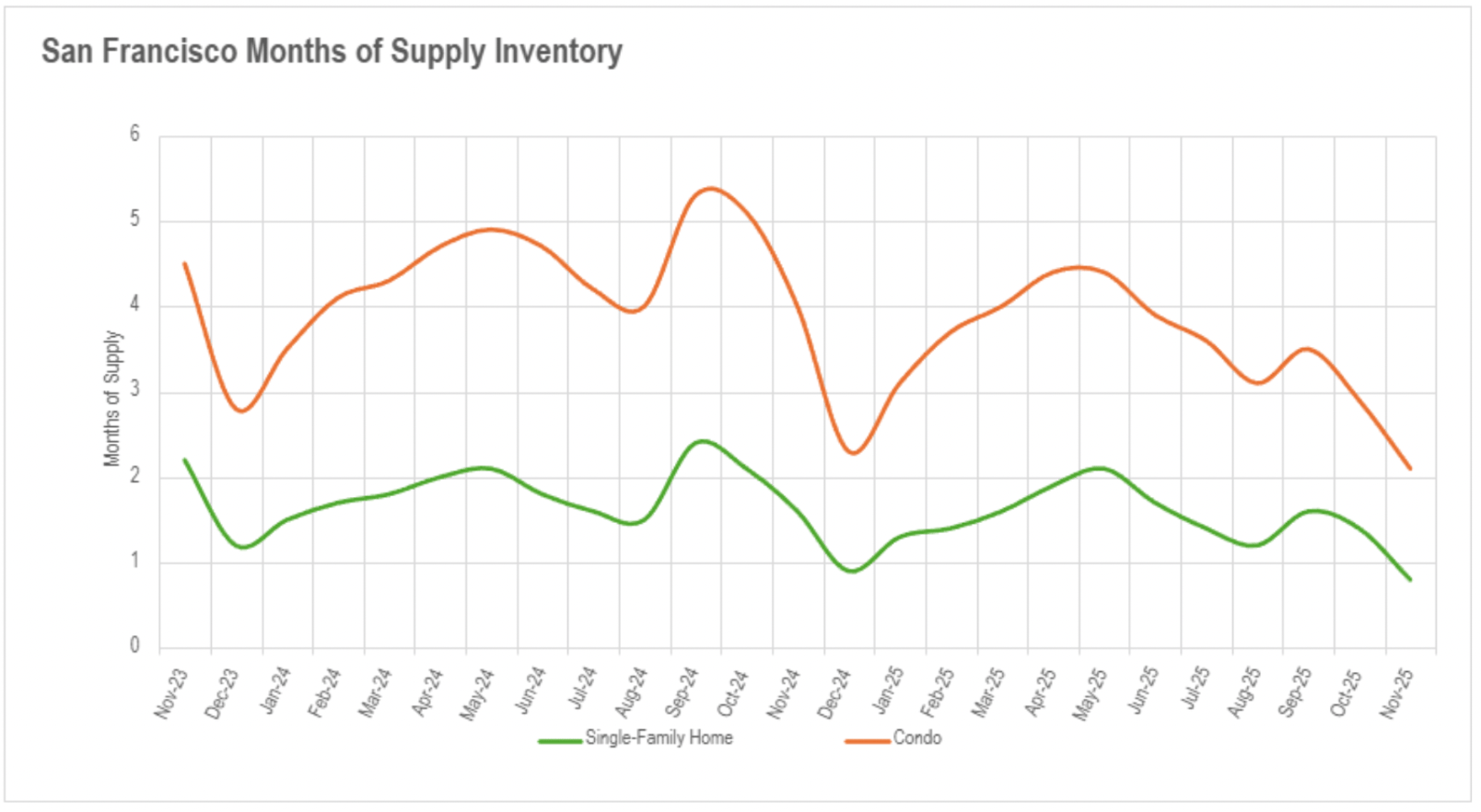

San Francisco records exceptional expansion with single-family properties advancing 15.82% and availability plummeting over 40%, establishing the most constrained market environment in three years with merely 0.8 months of supply.

The Bay Area experiences substantial availability compression in November, with most regions recording 20-30% monthly reductions as the market transitions into its customary winter deceleration.

Value trajectories diverge markedly across regions, with San Francisco ascending to unprecedented peaks while Silicon Valley encounters its initial comprehensive single-family retreats in over a year and East Bay markets witness considerable weakness in Alameda County.

Marketing duration metrics demonstrate extreme regional disparity, with San Francisco intensifying substantially as availability tightens, while other regions face meaningful slowdowns despite diminished availability levels.

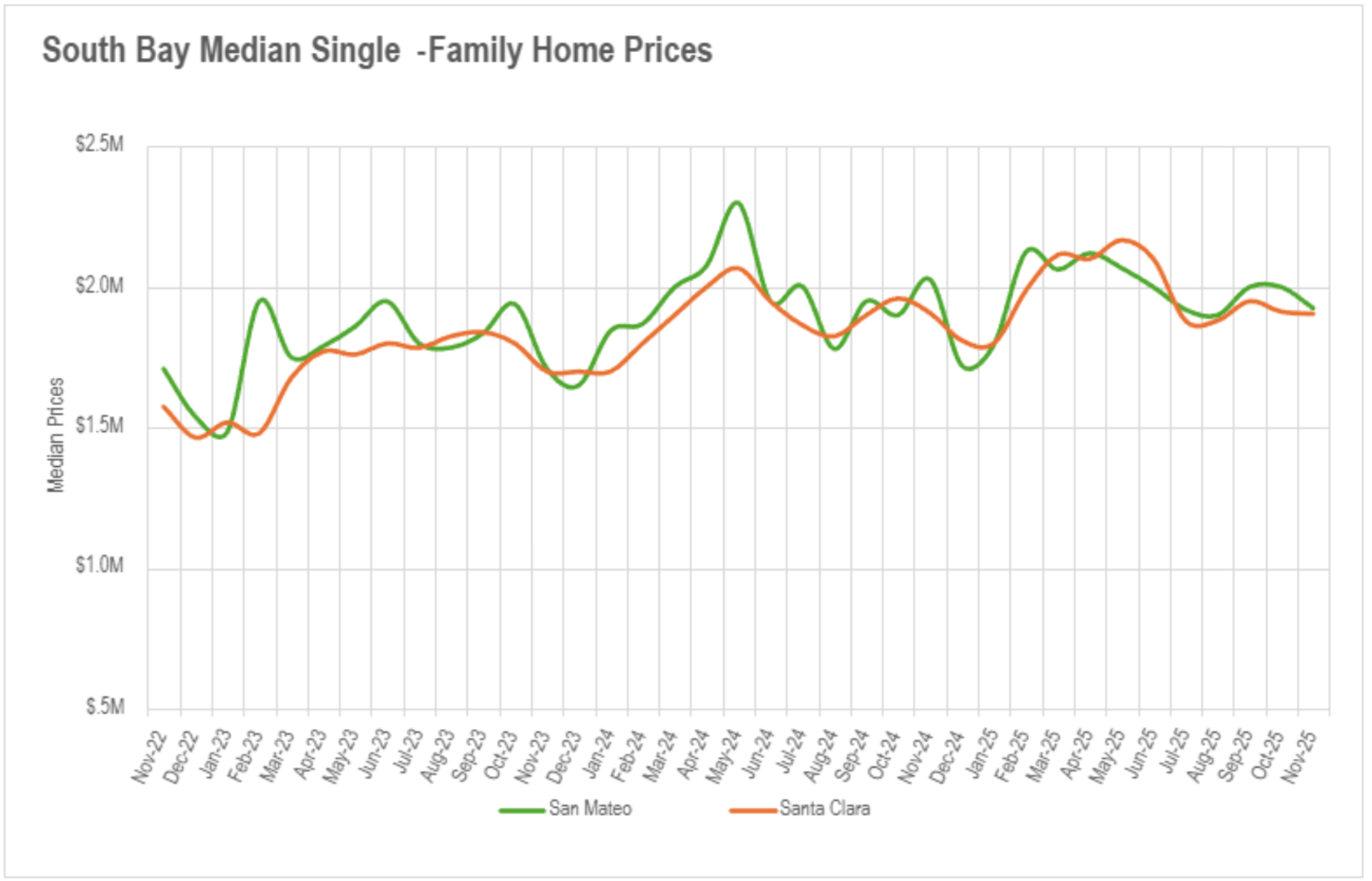

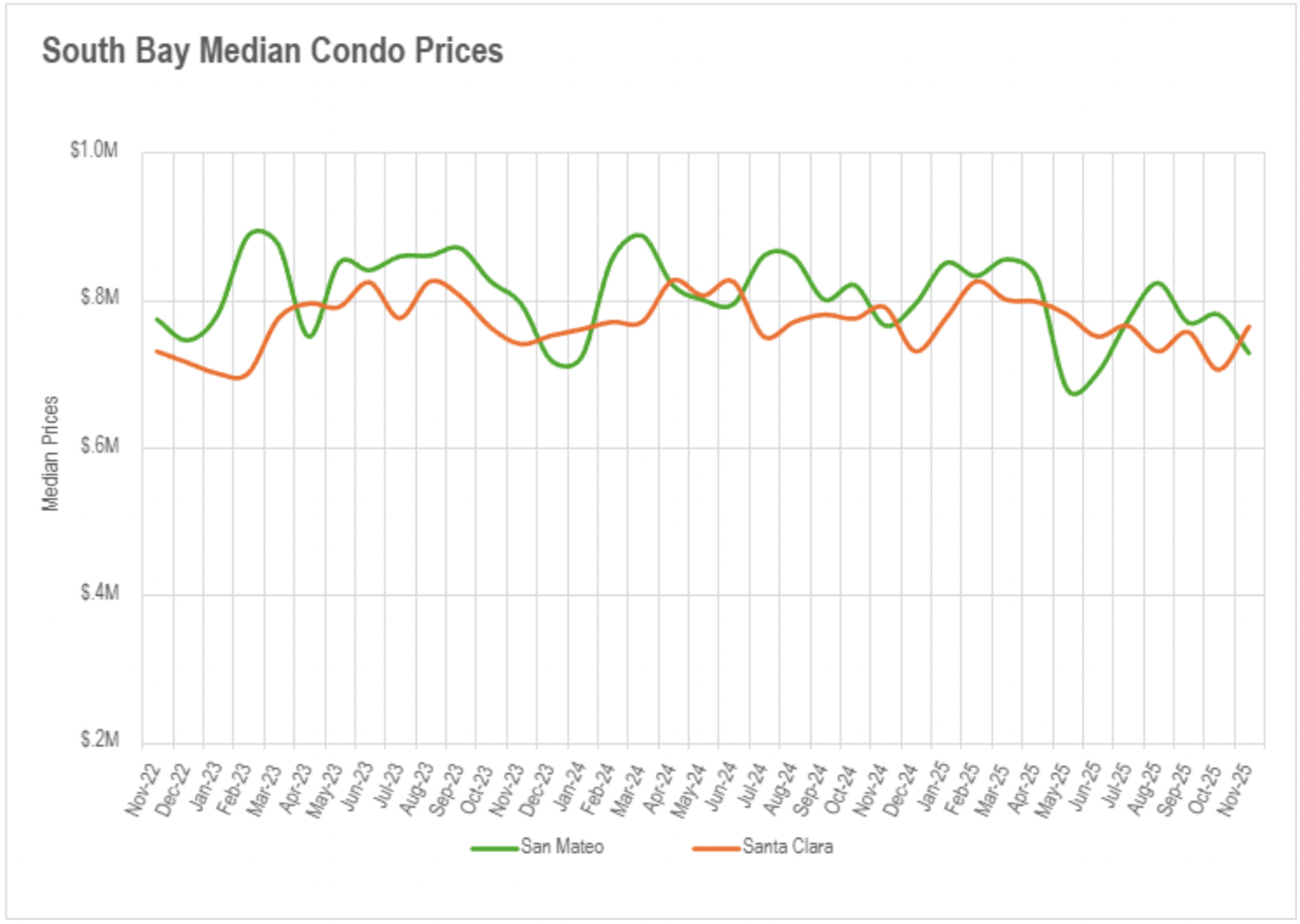

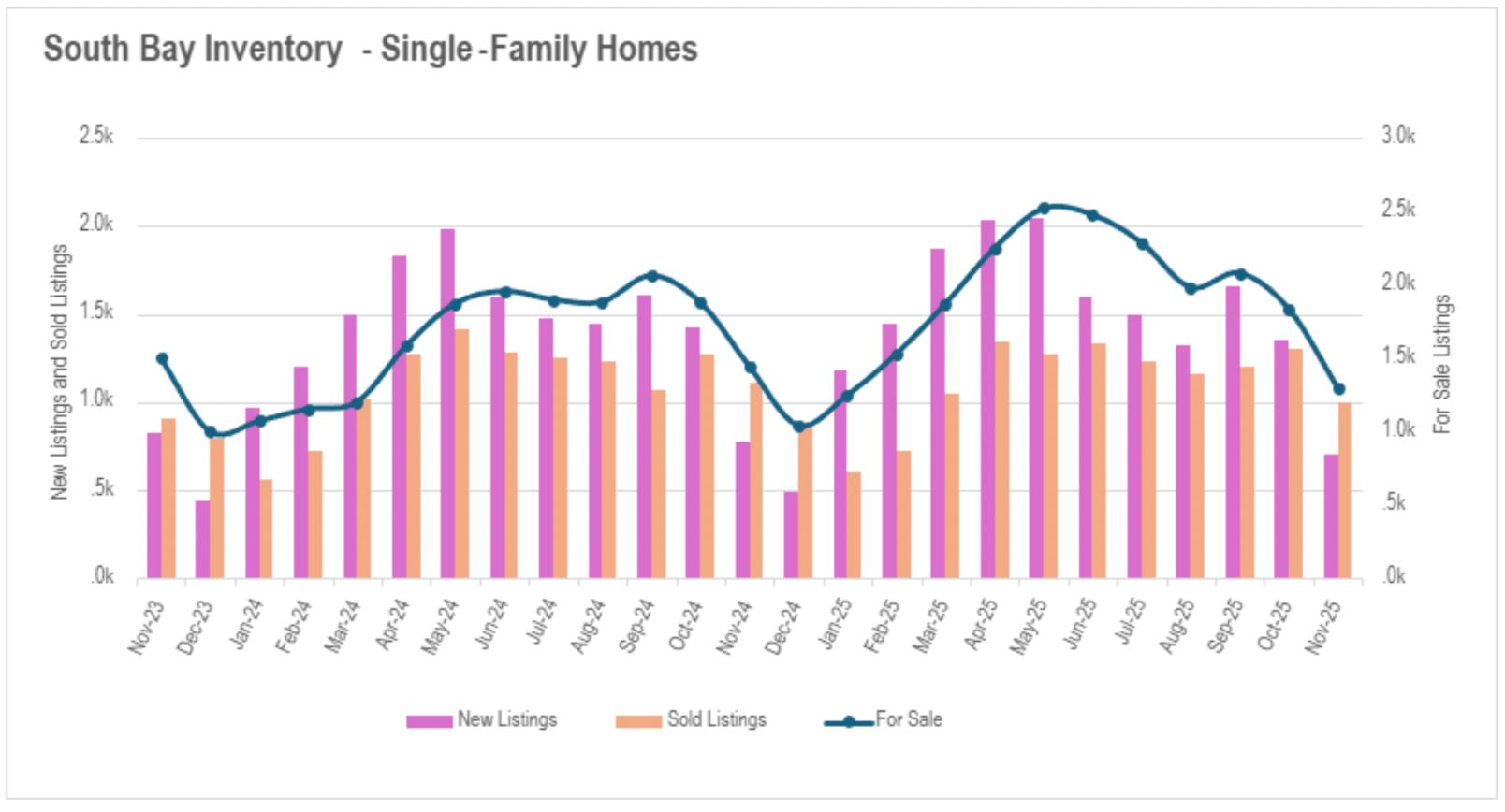

November exposed pronounced regional contrasts in Bay Area valuation patterns. San Francisco recorded exceptional expansion with single-family properties jumping 15.82% annually and condominiums climbing 9.36%, contradicting characteristic seasonal trends with only moderate monthly reductions. Single-family properties are now transacting for an exceptional 16% above asking value - the highest premium in three years. This contrasts dramatically with Silicon Valley, which documented its initial comprehensive single-family value retreats in over a year, with San Mateo declining 5.06%, Santa Cruz falling 1.18%, and Santa Clara retreating 0.16%. Silicon Valley condominiums also weakened with San Mateo and Santa Clara declining 4.90% and 3.28% respectively, though Santa Cruz reversed the pattern with a 5.17% advance.

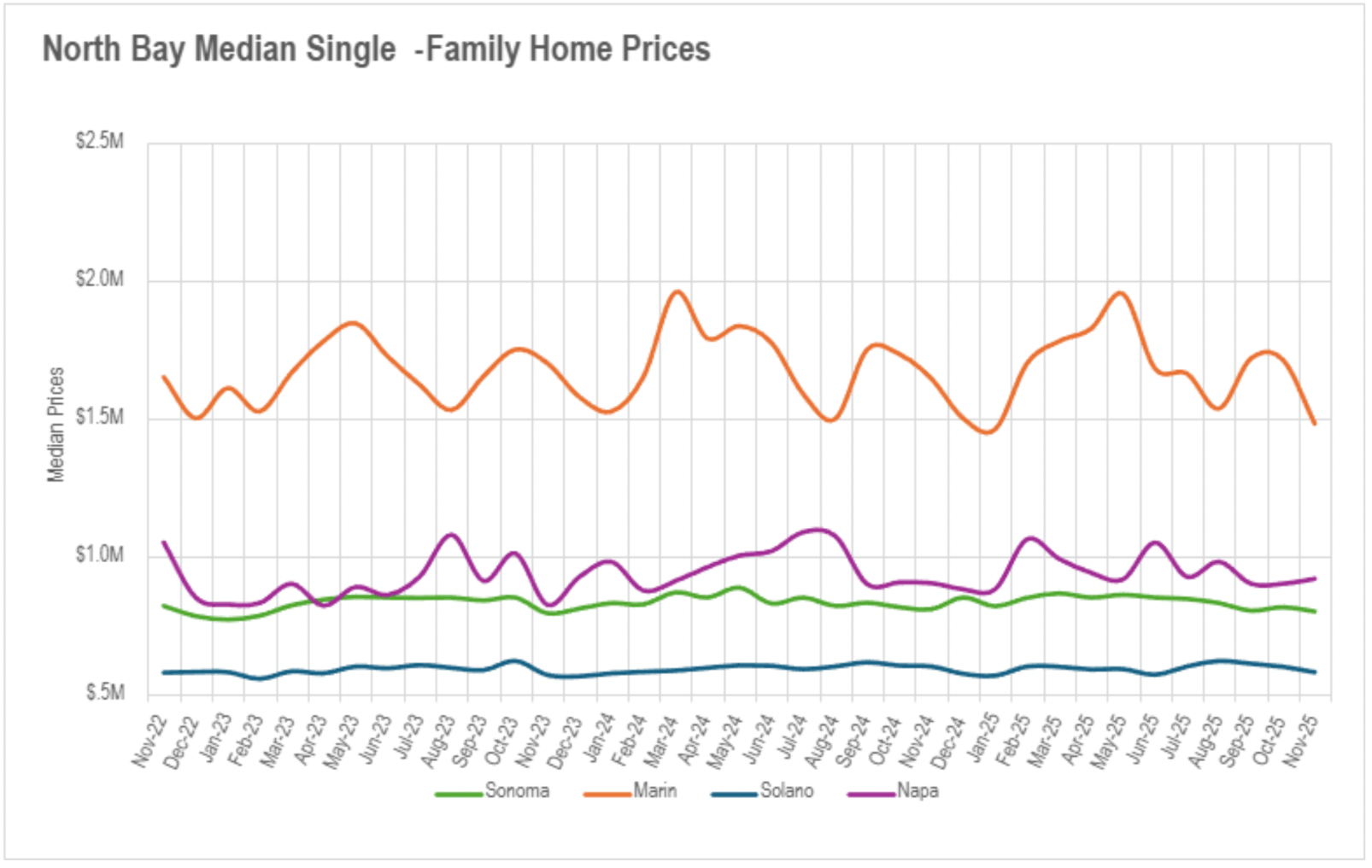

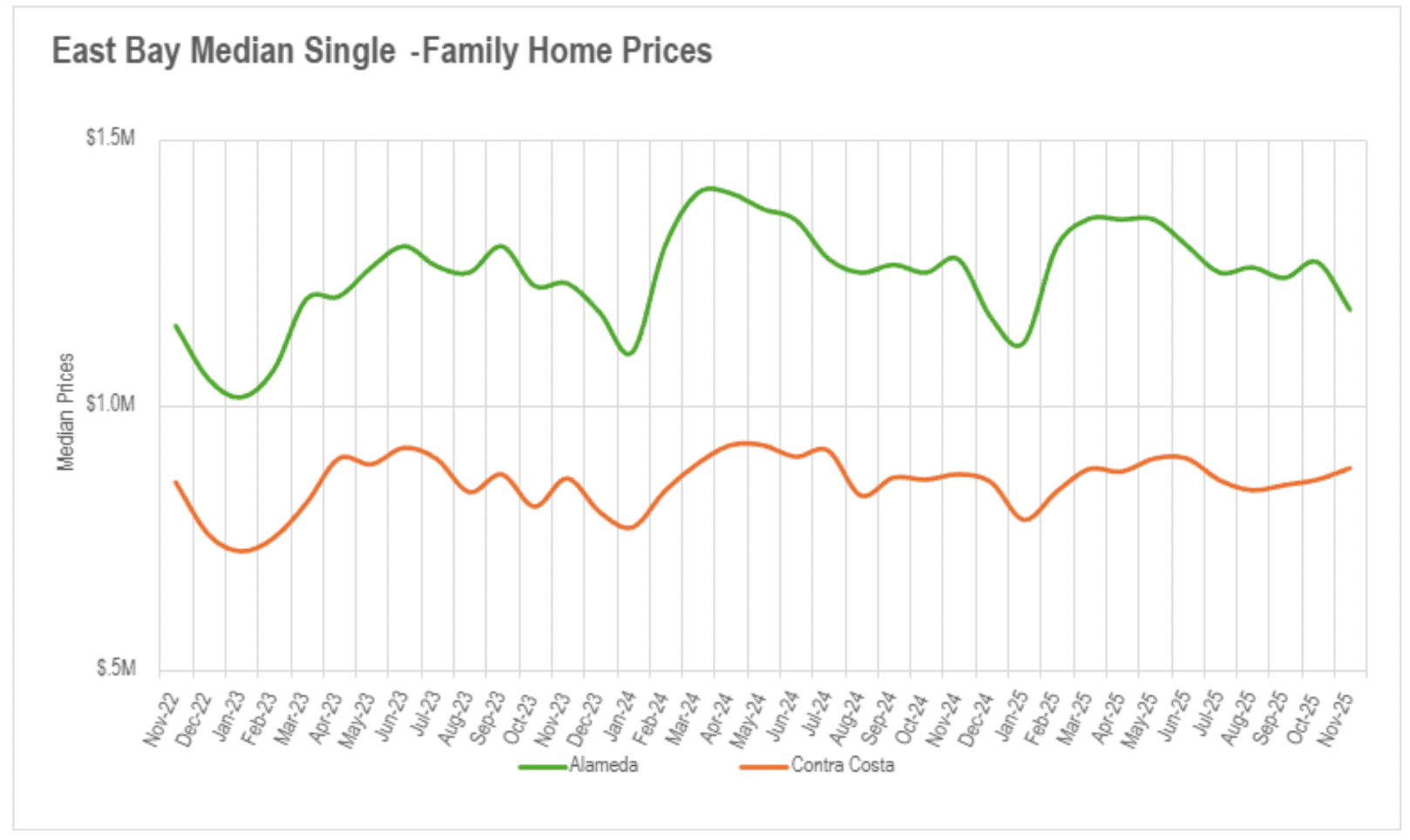

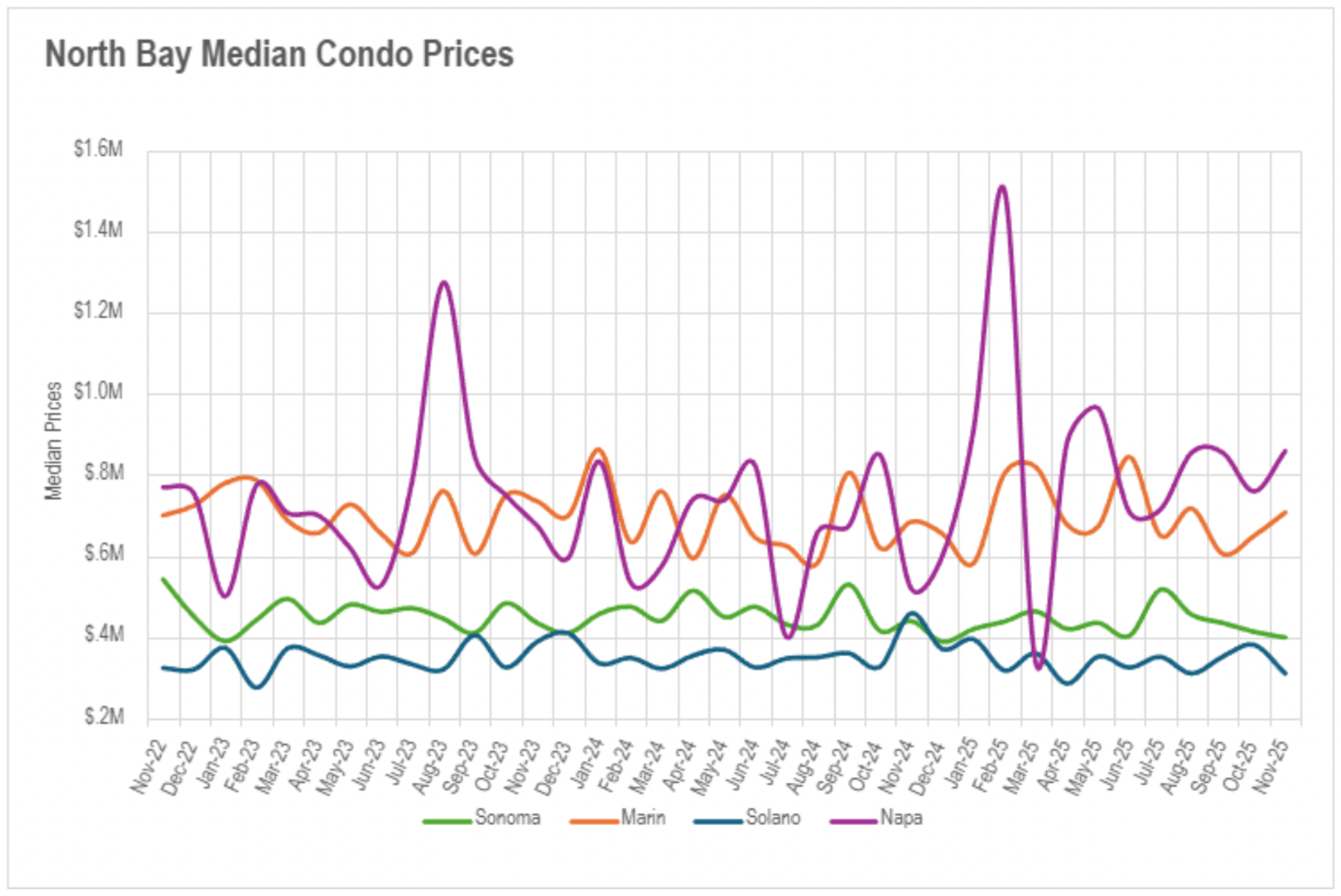

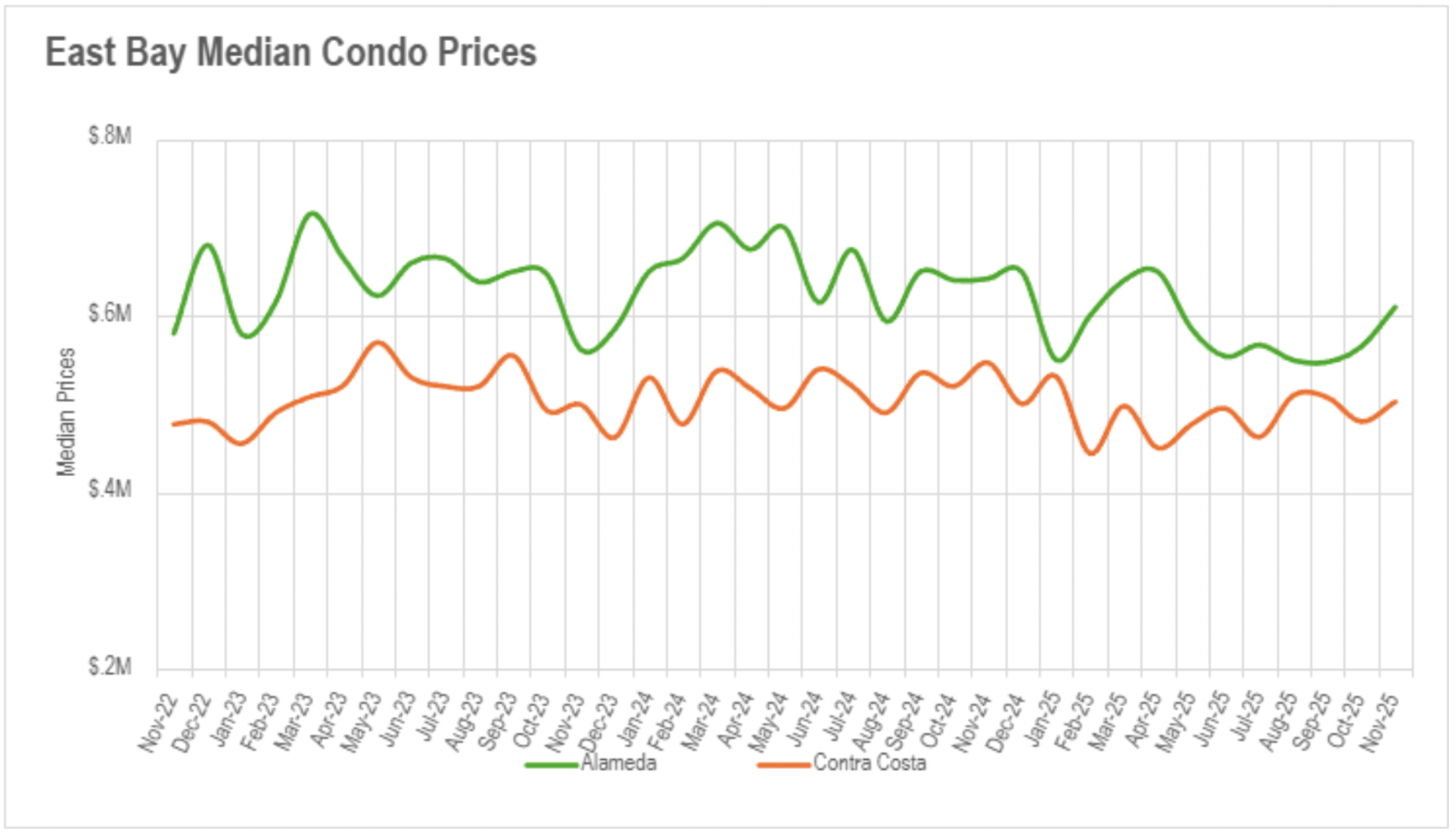

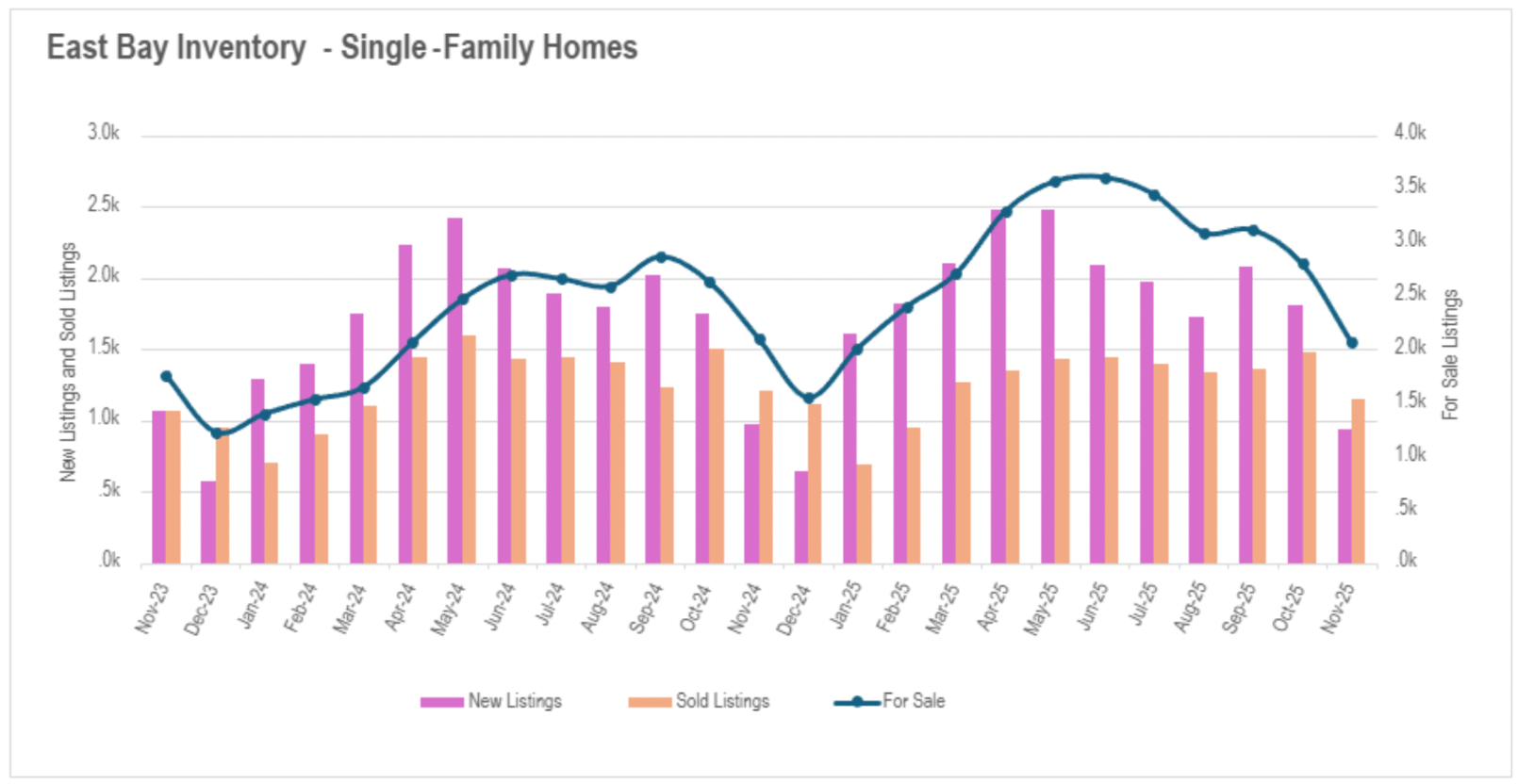

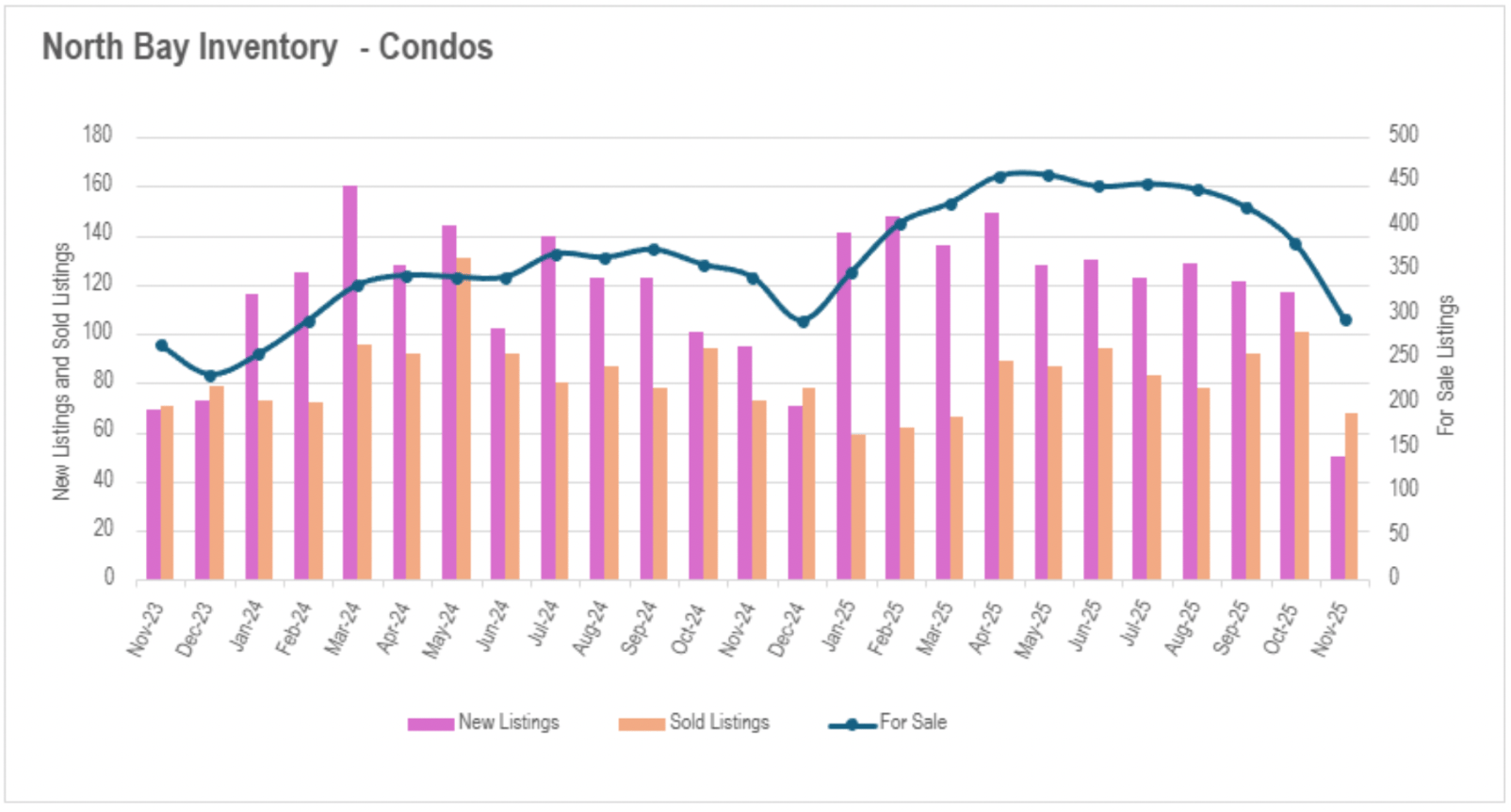

East Bay markets exhibited considerable fluctuation, with Alameda County single-family properties plummeting 7.45% annually while Contra Costa achieved a moderate 1.36% gain. East Bay condominiums declined throughout with 4.98% retreats in Alameda and 8.14% in Contra Costa. North Bay regions demonstrated more restrained movements overall, with single-family properties in Sonoma and Napa relatively steady at -0.99% and +1.72% respectively, though Marin County recorded a substantial 10.03% retreat and Solano declined 3.50%. North Bay condominiums displayed extreme fluctuation with Solano collapsing 32.46% while Napa surged an exceptional 65.35%.

November constituted an exceptional availability contraction throughout the Bay Area, with most regions recording pronounced monthly declines as the market transitioned into its seasonal winter deceleration. San Francisco commanded with the most acute compression, as total availability reached merely 553 properties for transaction - the minimal level in three years. Single-family availability crashed 44.84% annually while condominiums declined 41.90%, establishing unprecedented supply limitations. Silicon Valley's single-family sector experienced a substantial "overcompensation," with availability plunging nearly 30% monthly and 10% annually, nearing the extreme minimums last documented in December 2024. The condominium sector demonstrated greater steadiness with availability essentially unchanged at just 1.11% above last year.

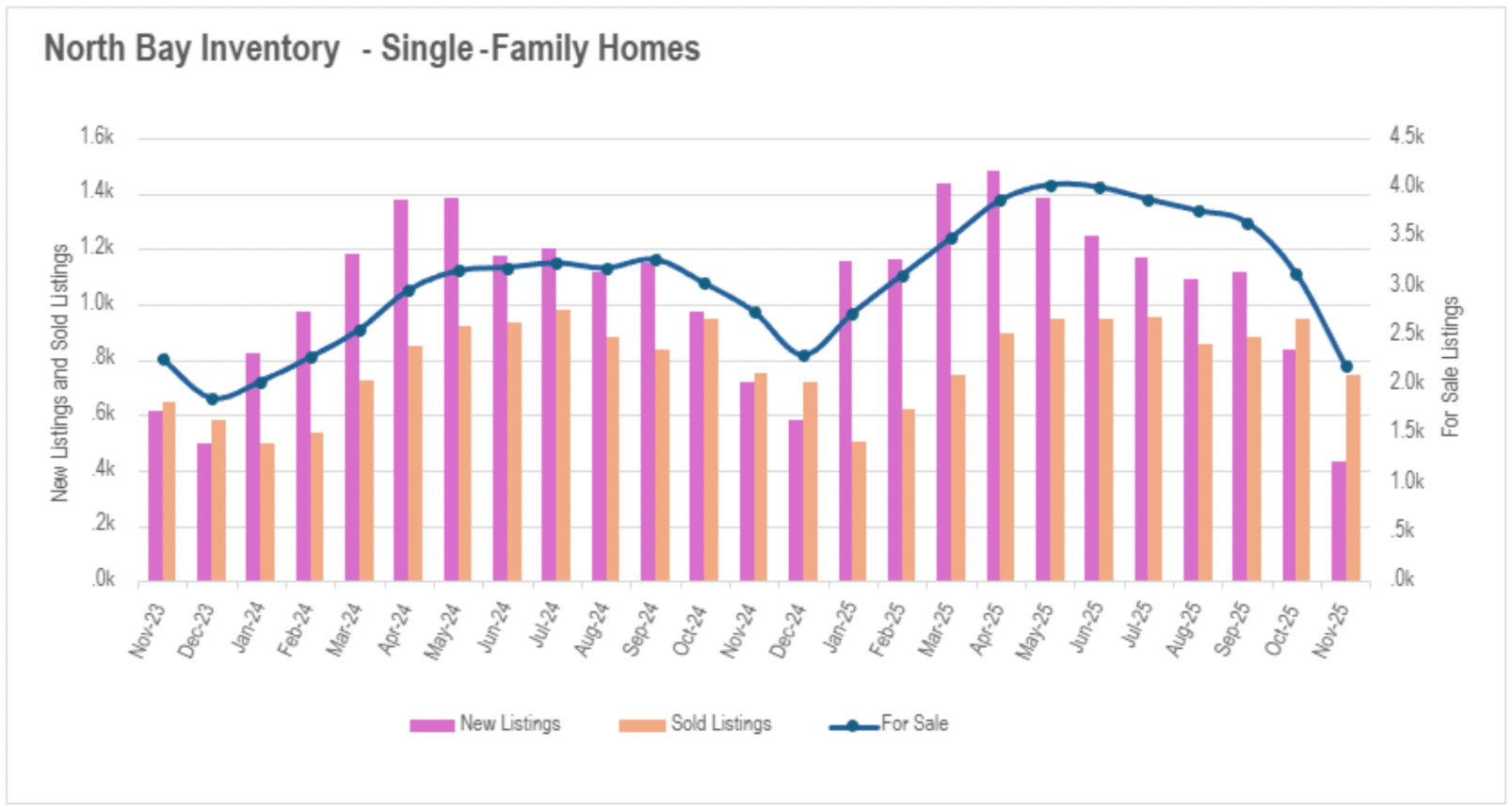

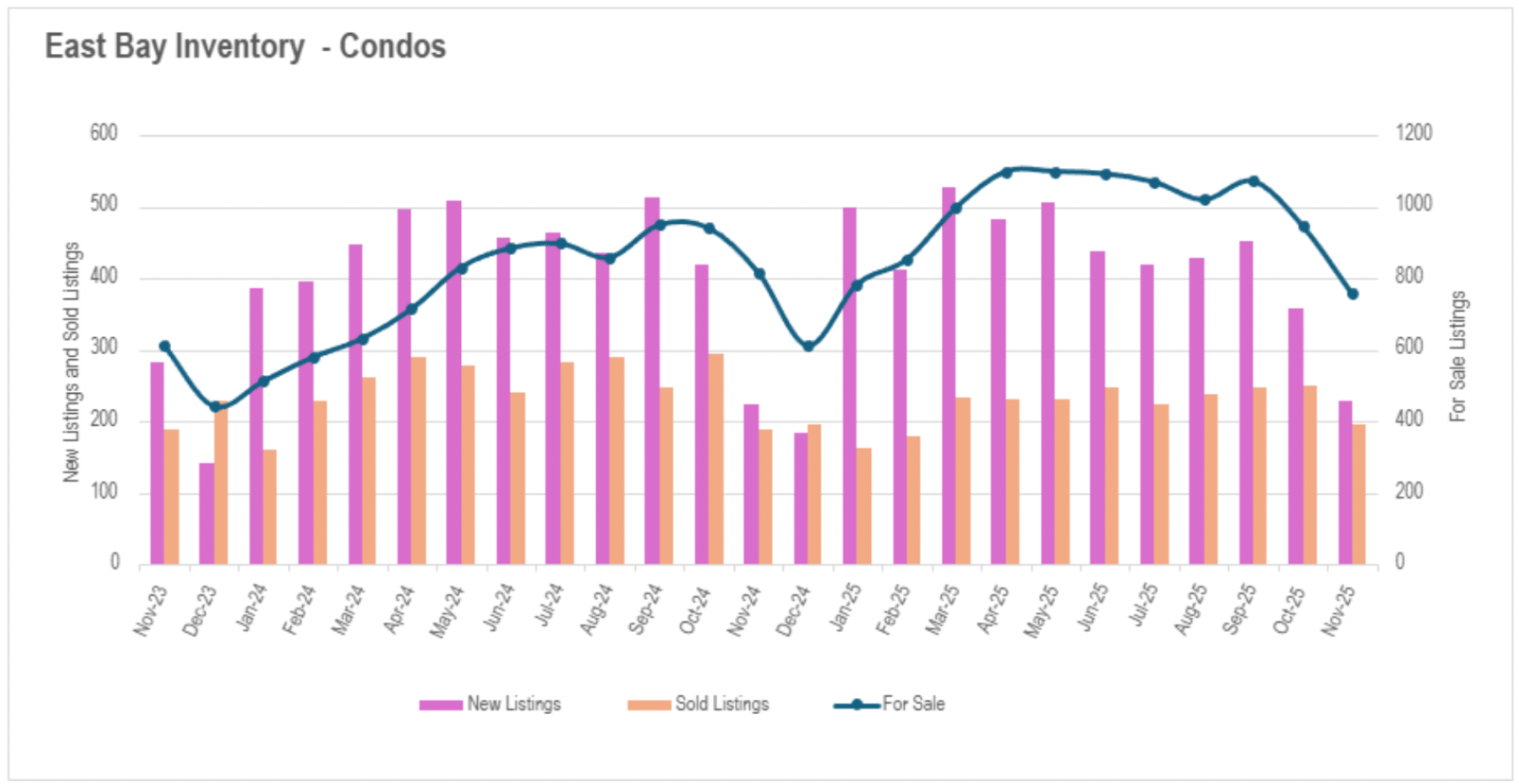

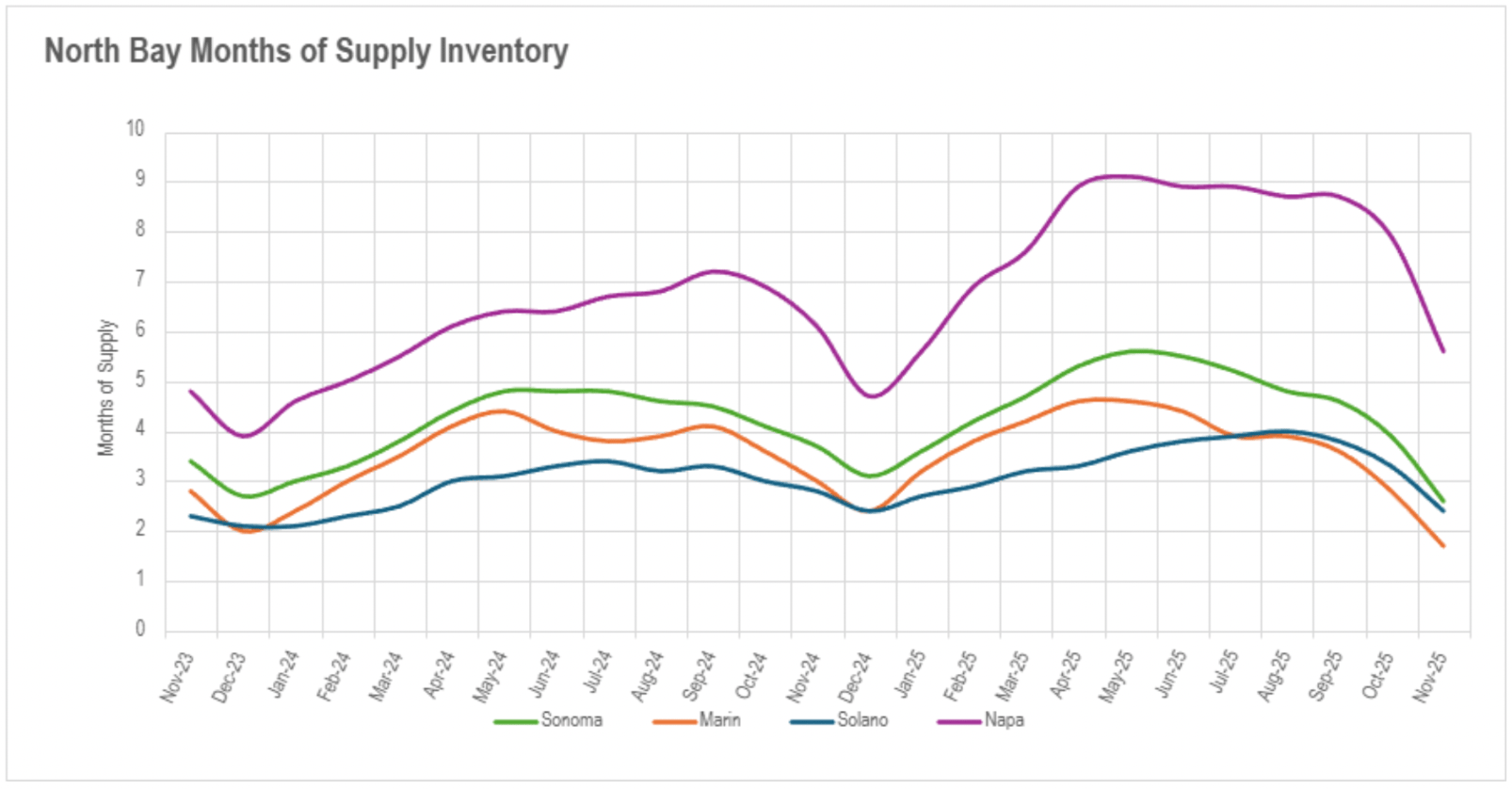

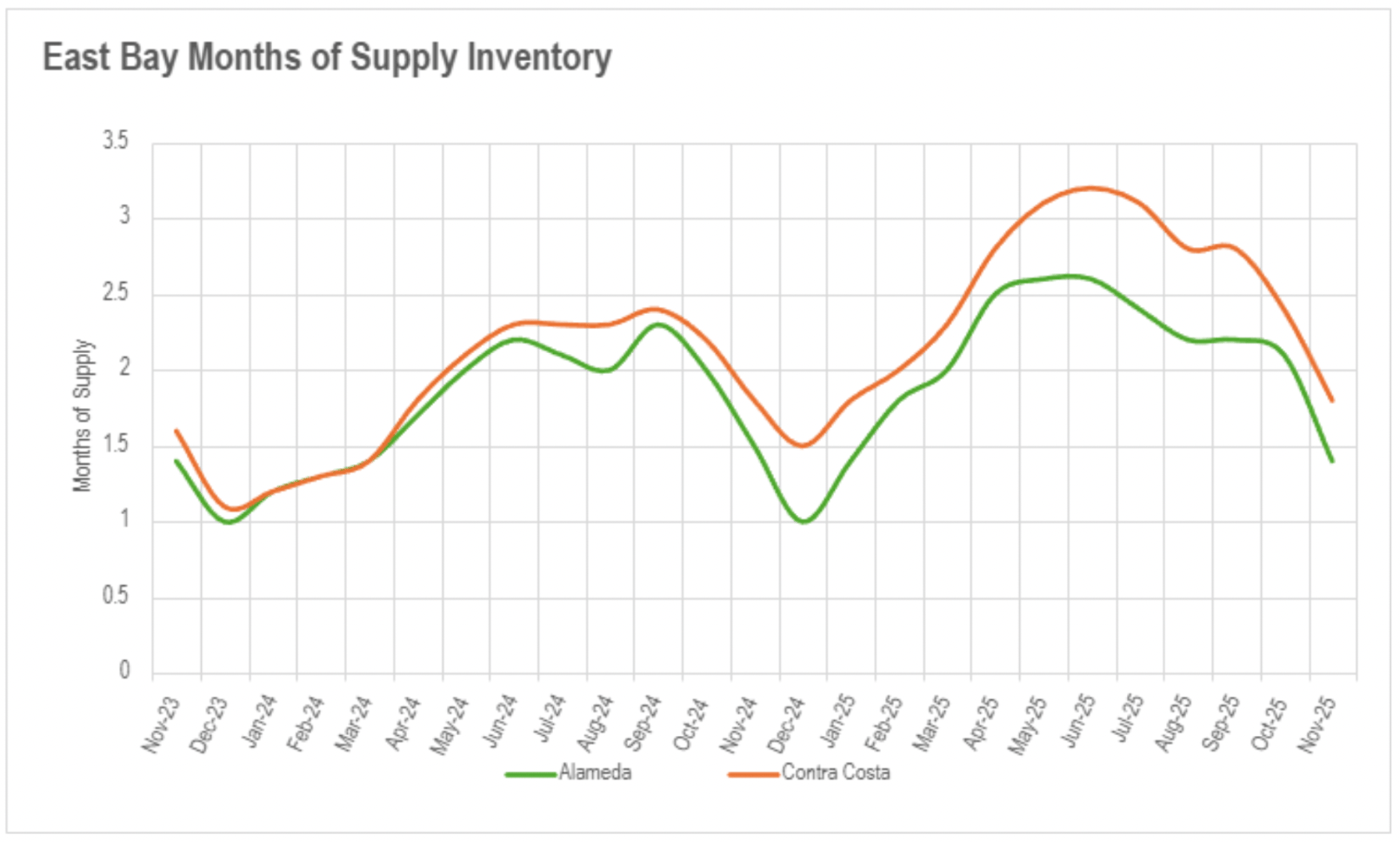

North Bay regions witnessed similarly substantial reductions with single-family availability declining 29.93% monthly and 20.14% annually, while condominiums fell 22.63% monthly and 14.04% annually. Significantly, North Bay availability levels are now beneath December 2024, indicating even steeper reductions may be approaching. East Bay markets represented the singular exception to this trajectory, demonstrating exceptional resilience with availability levels roughly unchanged annually despite the substantial corrections observed elsewhere. This steadiness is especially significant given the considerable availability accumulations the region recorded during late spring and early summer.

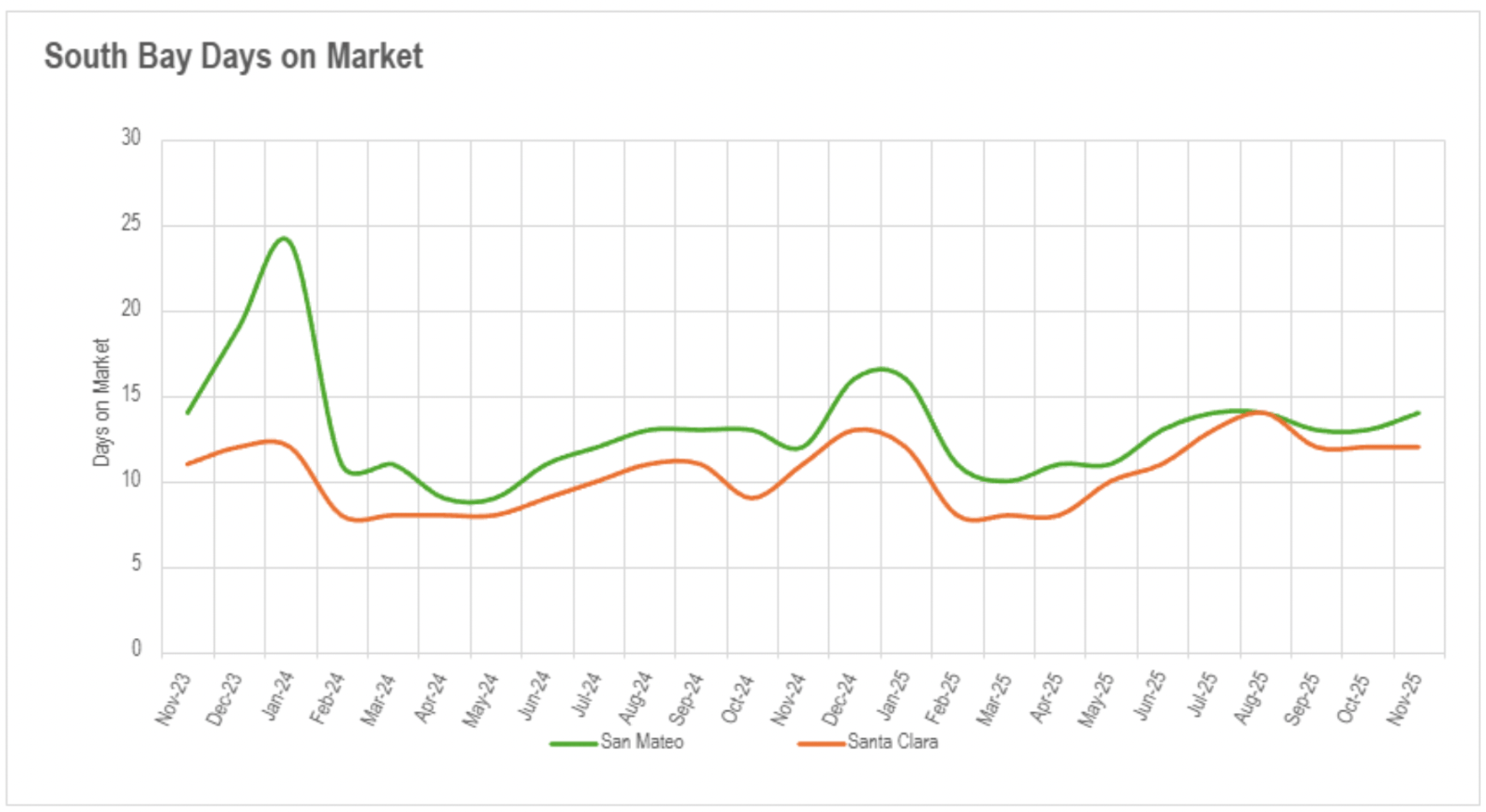

November's marketing duration data unveiled extreme divergence throughout the Bay Area, with San Francisco intensifying substantially while most other regions faced meaningful slowdowns. San Francisco's transaction momentum strengthened as availability compressed, with single-family properties now transacting in merely 13 days (declining 13.33% annually) and condominiums moving in 35 days (declining 30% annually). This acceleration means buyers possess virtually no duration to consider before submitting offers. Silicon Valley presented an inconsistent scenario - San Mateo and Santa Clara Counties sustained their exceptionally expeditious momentum with single-family properties transacting in two weeks or less, but Santa Cruz County recorded a substantial slowdown with single-family properties requiring 109.52% additional market duration than last year. Silicon Valley condominium markets remained difficult throughout.

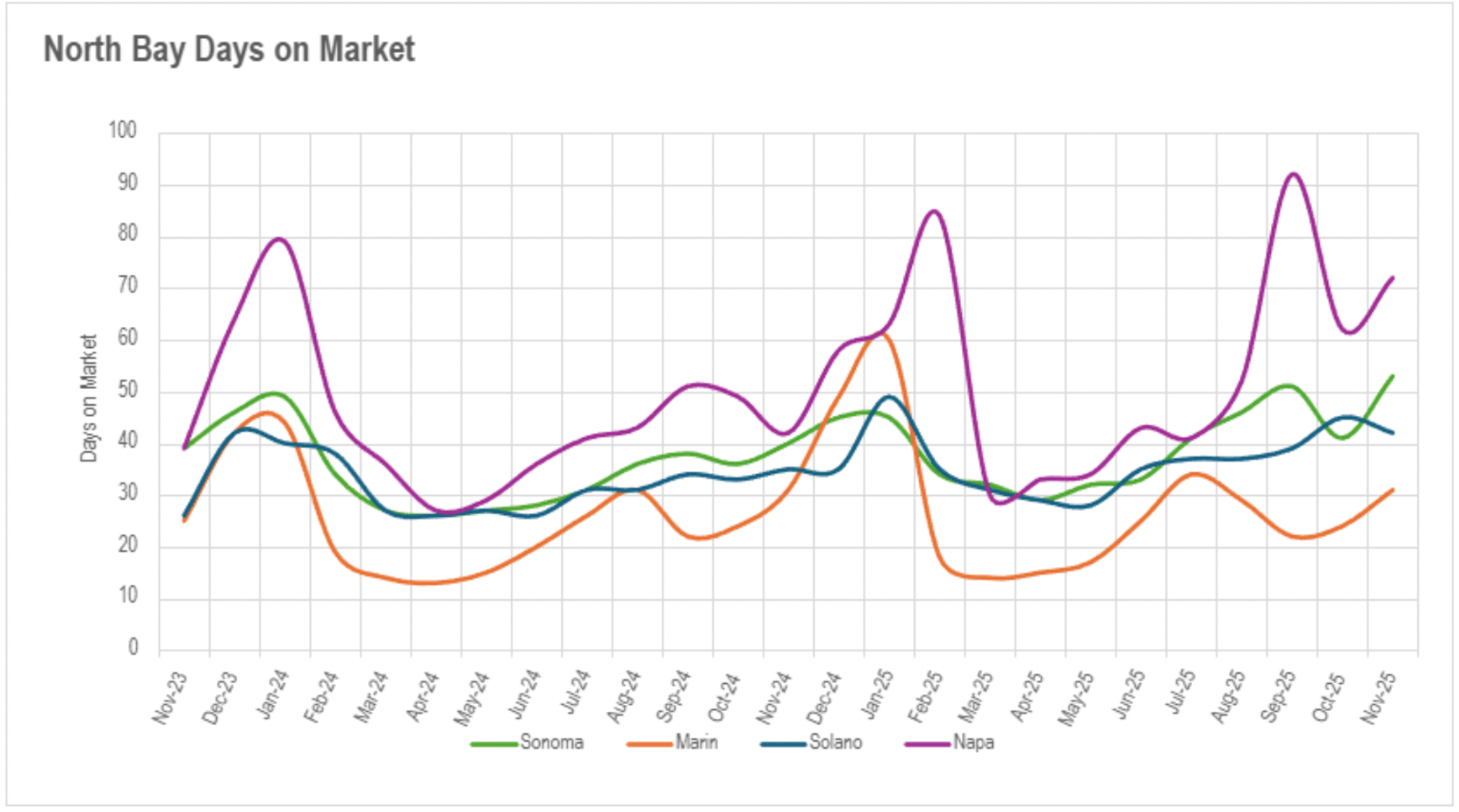

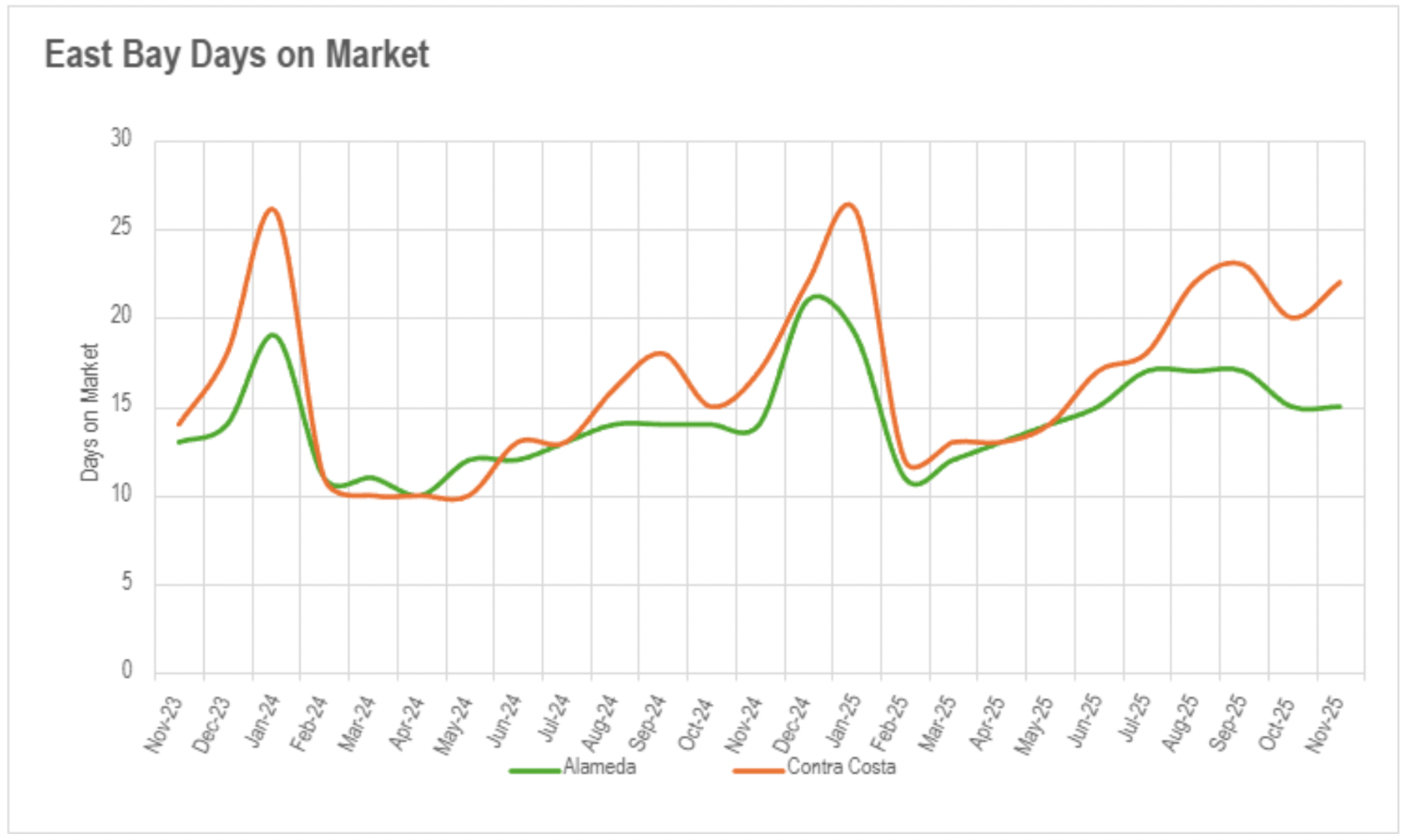

North Bay regions displayed considerable annual increases in most counties, with single-family properties requiring 32.50%, 20%, and 71.46% longer on market in Sonoma, Solano, and Napa Counties respectively, though Marin County remained perfectly unchanged at 31 days in both November 2024 and 2025. Compellingly, Marin condominiums actually accelerated with a 26.83% annual reduction in market duration, while the typical Napa County condominium required nearly half a year (approximately 180 days) on market. East Bay markets perpetuated their year-long configuration of percentage increases obscuring relatively expeditious absolute durations for single-family properties, while condominiums faced more considerable slowdowns with 39.29% and 20.00% increases in Alameda and Contra Costa Counties respectively.

November's substantial availability reductions accelerated the Bay Area's transition toward seller-controlled environments across nearly all property categories and regions. San Francisco accomplished the most extreme seller-favorable market status in the region, with single-family properties at an unprecedented 0.8 months of supply and condominiums at merely 2.1 months - both representing deeply established seller-favorable markets with no mitigation anticipated. Silicon Valley experienced the anticipated seasonal transition toward seller-favorable markets, with single-family properties in San Mateo and Santa Clara Counties achieving exceptionally minimal 1.1 and 0.9 months of supply respectively, while Santa Cruz remained balanced at precisely 3.0 months. Silicon Valley condominiums transitioned decisively toward seller territory with San Mateo at 2.5 months, Santa Clara at 2.9 months (both nearing seller-favorable market parameters), and Santa Cruz at 3.9 months still supporting buyers.

East Bay markets preserved their conventional market architecture but with intensifying seller positioning, as single-family properties achieved exceptionally constrained 1.4 months in Alameda and 1.8 months in Contra Costa, while condominiums remained in buyer territory at 3.6 and 3.1 months respectively. North Bay regions demonstrated distinct seasonal progression toward seller-favorable markets throughout all property categories, with single-family properties in Marin establishing robust seller-favorable market status at 1.7 months, Sonoma and Solano at 2.6 and 2.4 months respectively (seller-favorable markets), and even Napa progressing toward equilibrium at 5.6 months. North Bay condominiums exhibited comparable progression with Marin at 3.0 months (balanced), Sonoma at 3.2 months (nearing balanced), and Solano and Napa at 4.4 and 5.1 months respectively (buyer-favorable markets progressing toward equilibrium). This regionwide configuration indicates the Bay Area has commenced a period of extreme supply limitation that will likely strengthen through December's characteristically minimal-availability holiday season.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

May 23, 2026

May 15, 2026

May 1, 2026

April 24, 2026

April 18, 2026

April 17, 2026

April 11, 2026

March 21, 2026

March 5, 2026

You've got questions and we can't wait to answer them.