January Market Update

The Bay Area concluded 2025 with extraordinary availability compression, with most regions recording 20-40% annual availability reductions as the holiday period intensified a substantial transition toward seller-favorable markets.

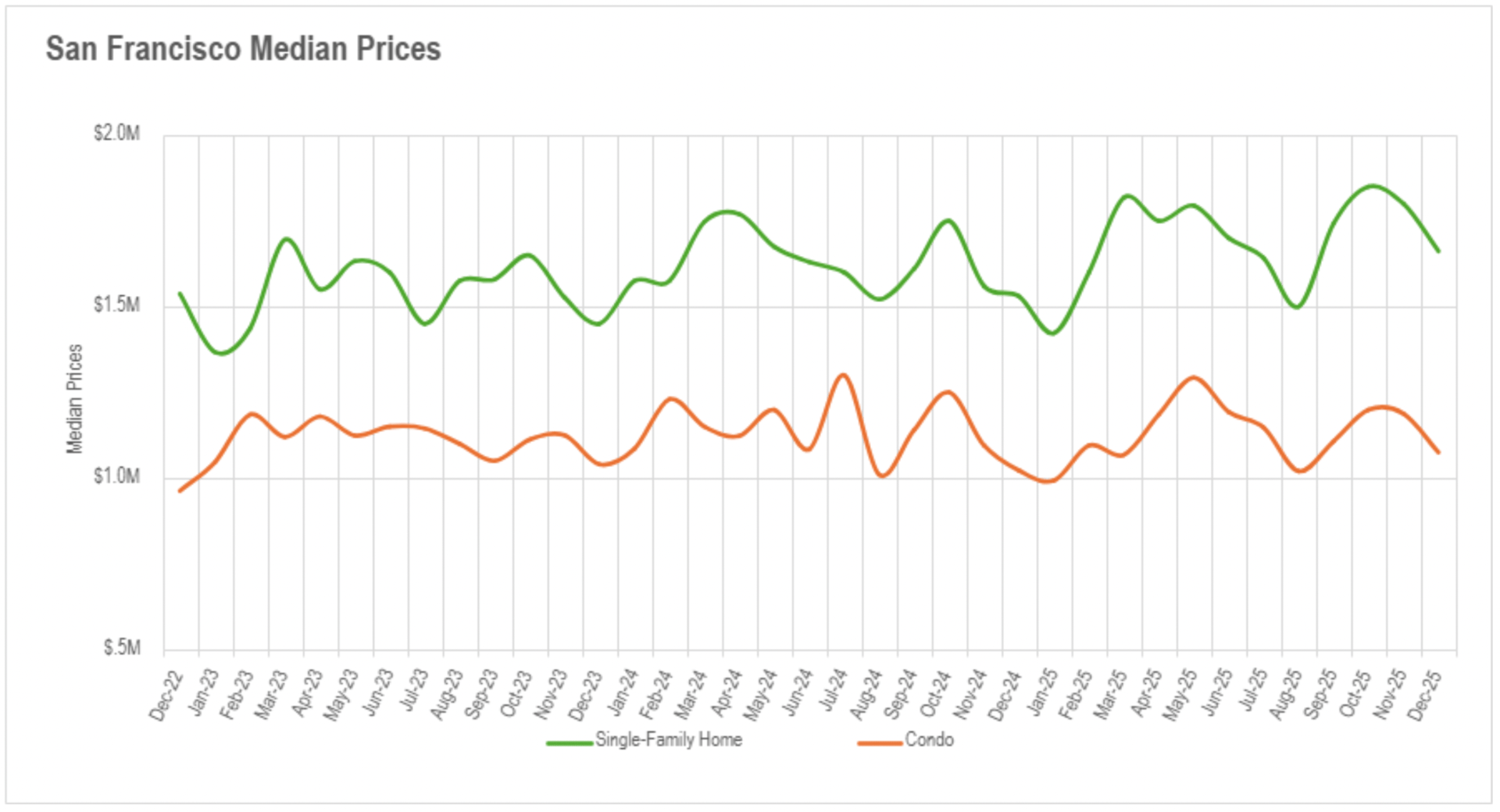

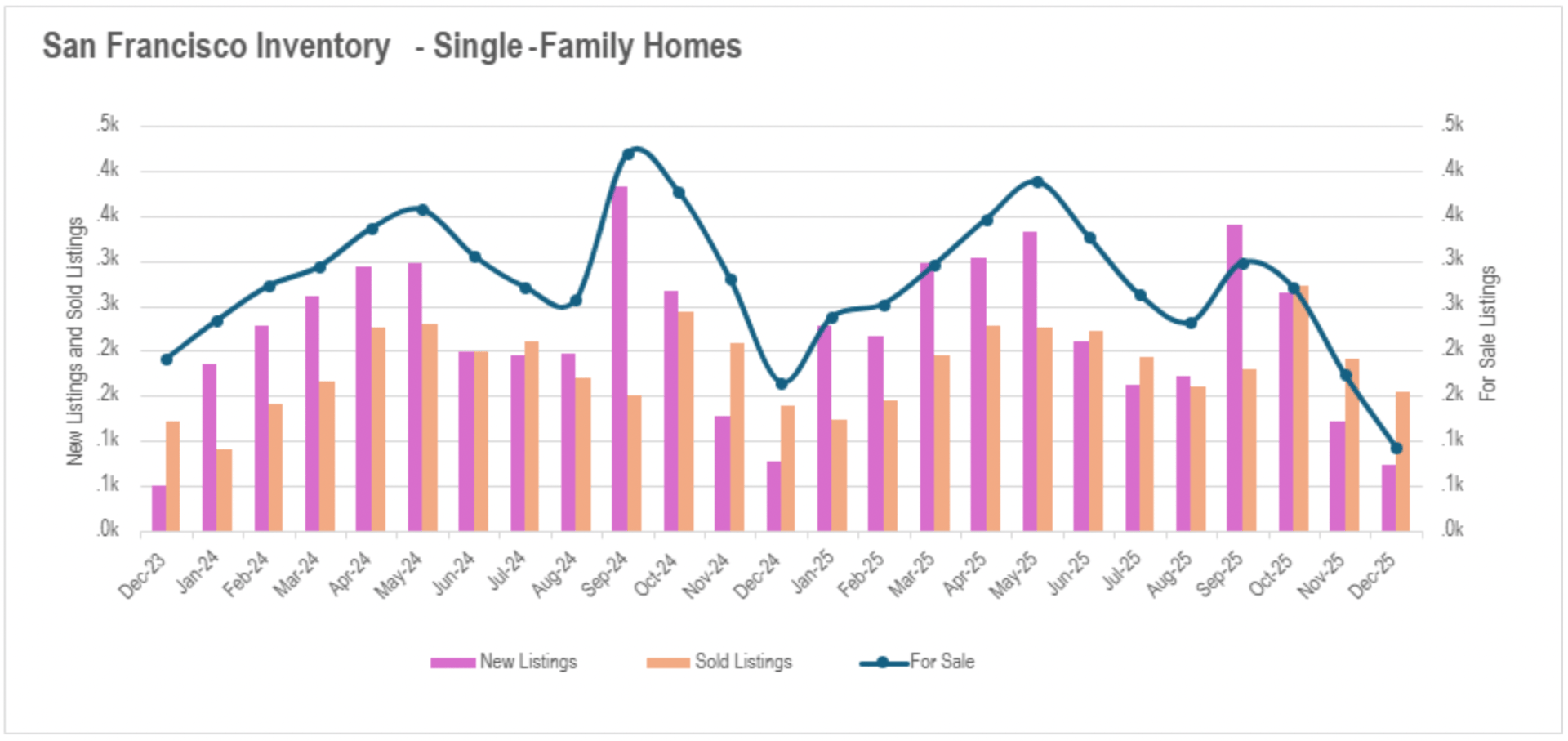

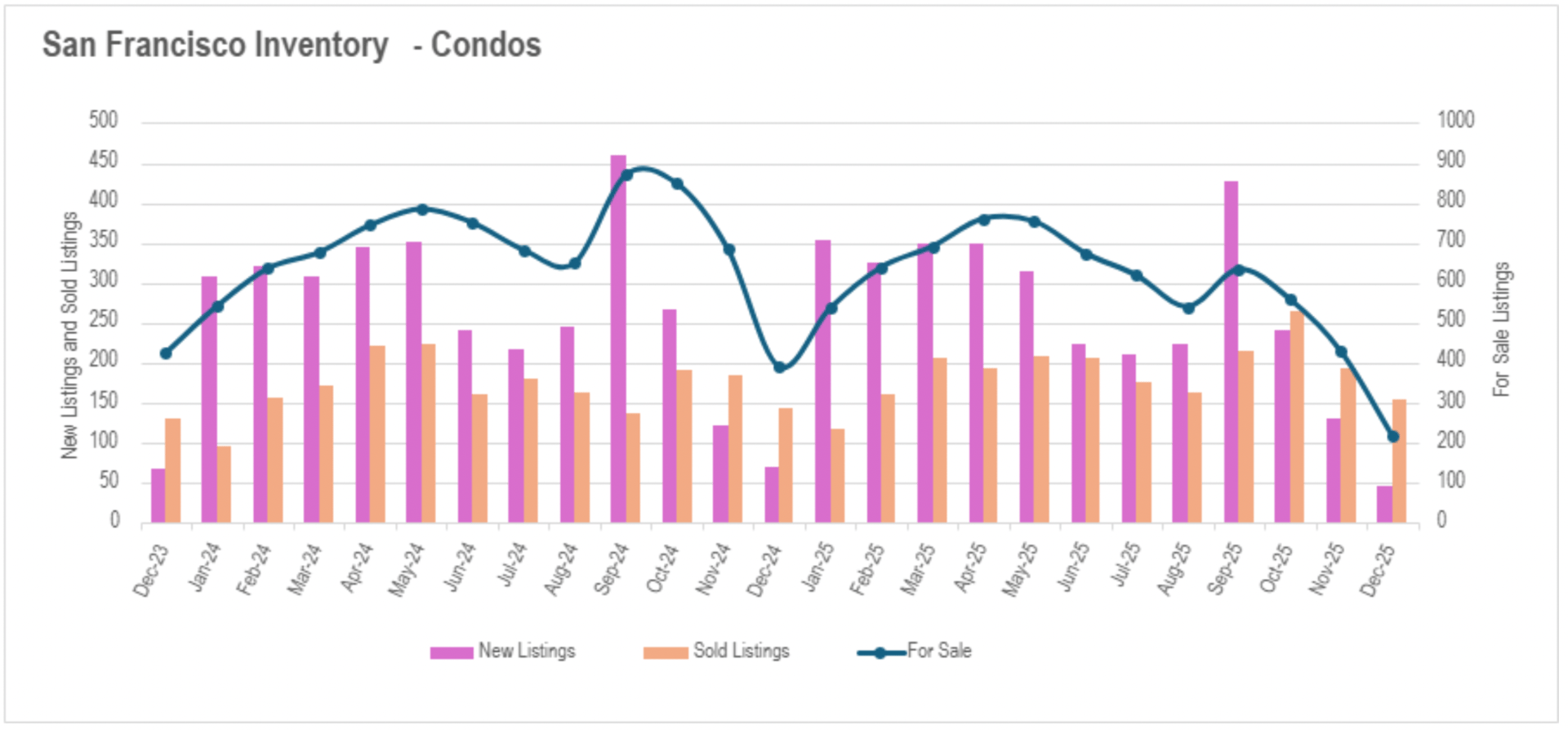

San Francisco commanded regional value appreciation with single-family properties advancing 8.63% and availability achieving historic minimums of merely 93 properties for transaction, while other regions demonstrated more varied outcomes with isolated weakness.

Marketing duration patterns diverged considerably throughout the region, with San Francisco and portions of East Bay markets intensifying while other areas like Santa Cruz County faced meaningful slowdowns despite constrained availability.

The entire Bay Area has transitioned into seller-favorable market territory across nearly all property categories, with several regions achieving extreme supply limitations not documented in years.

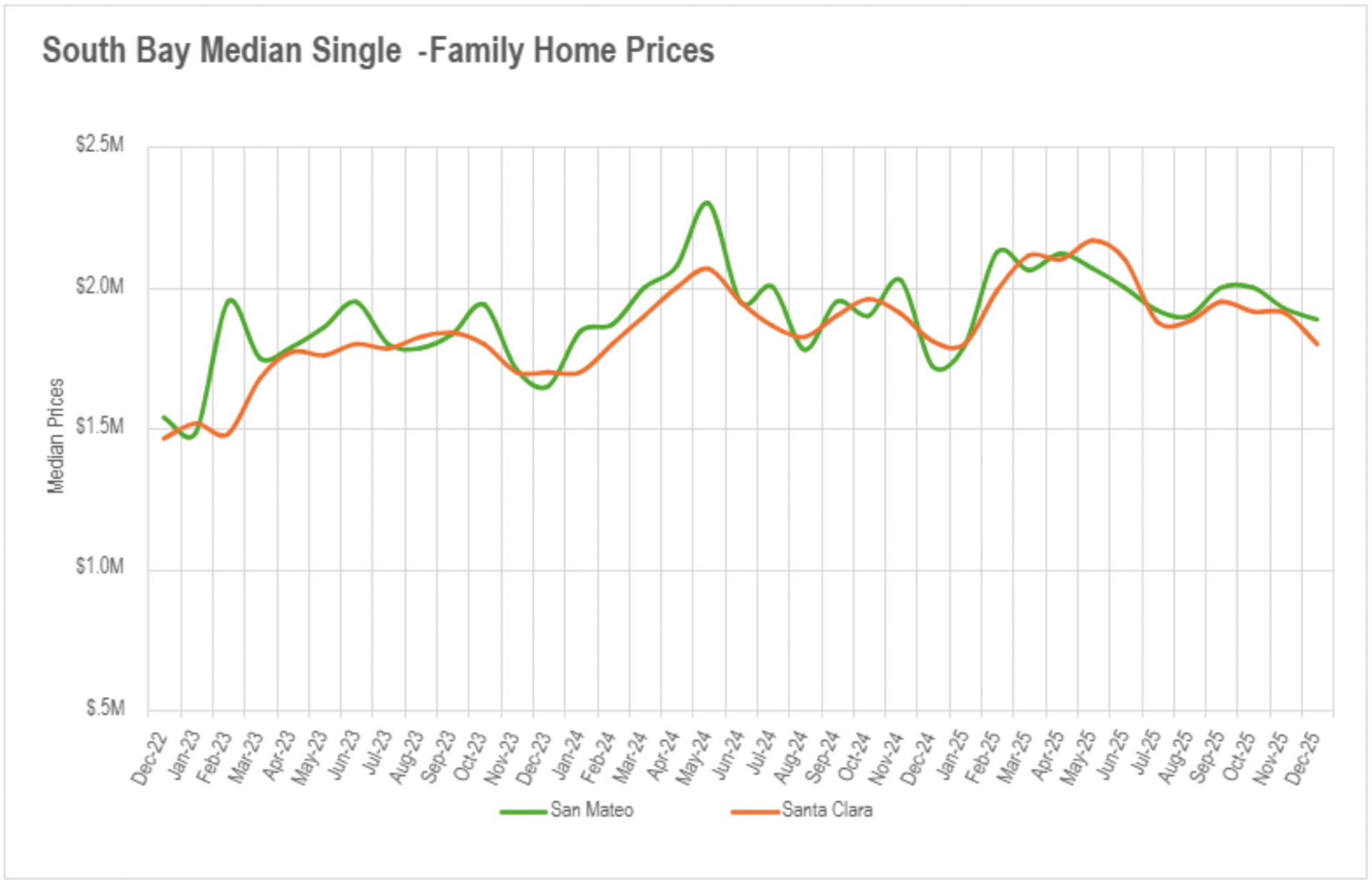

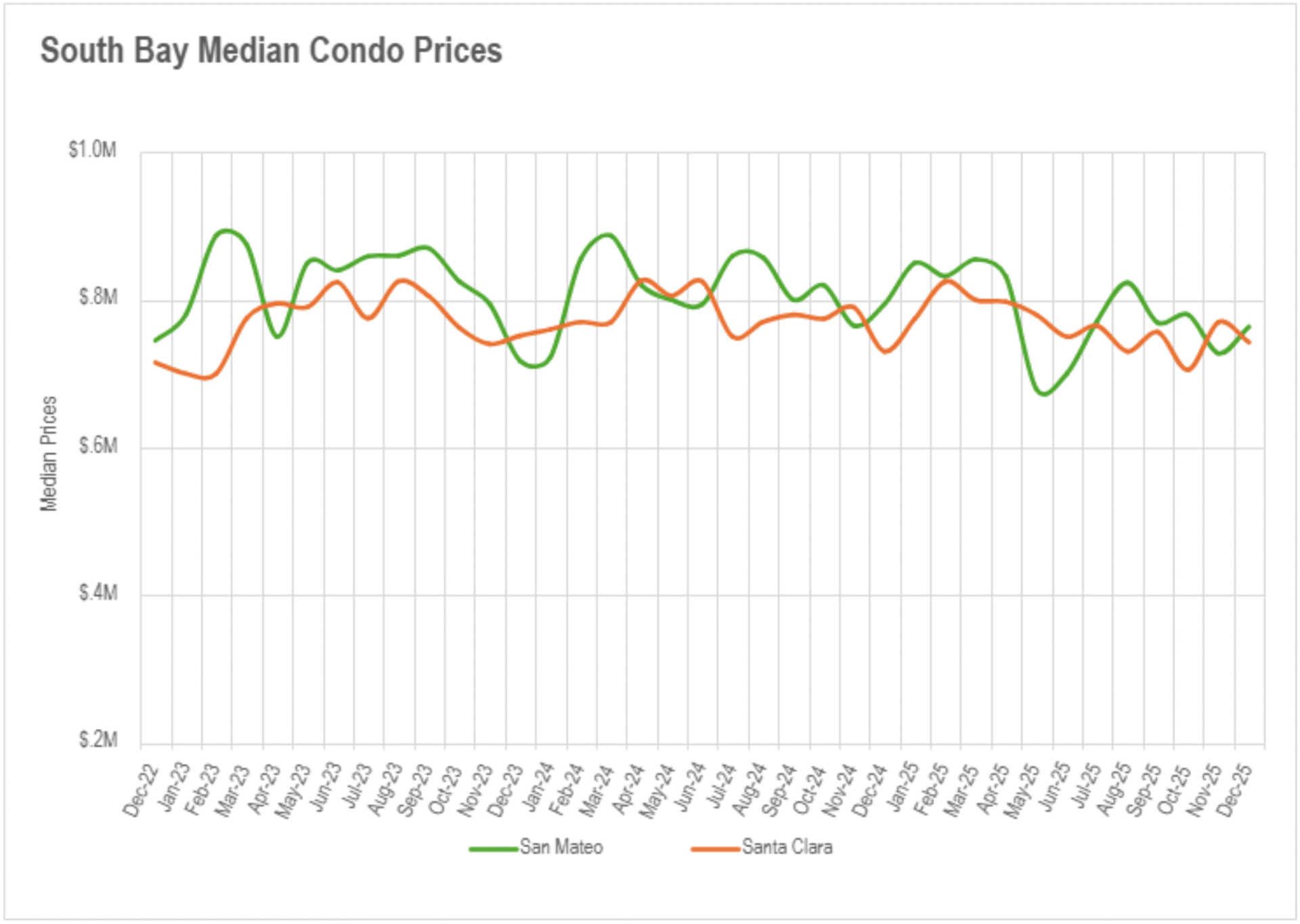

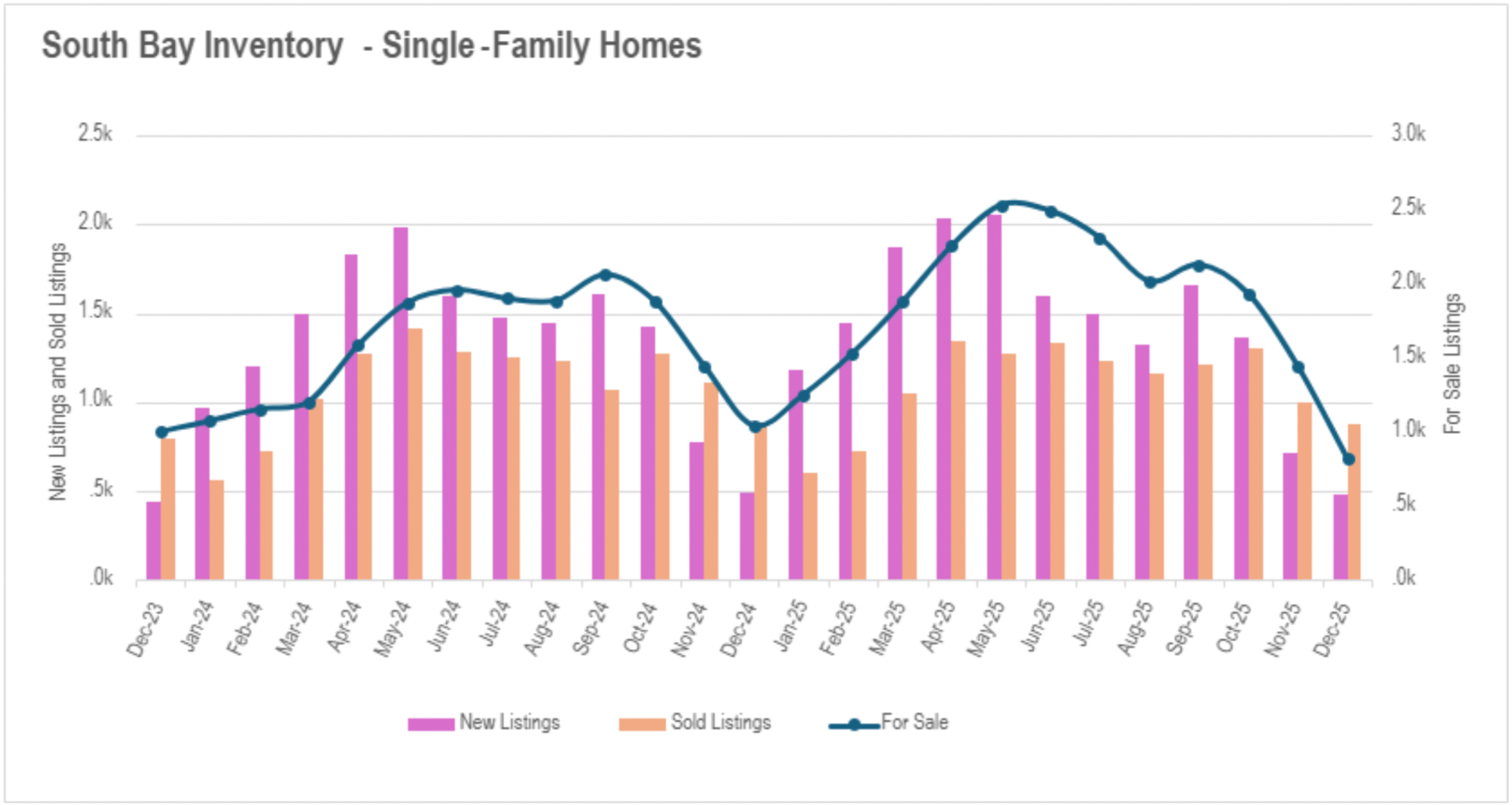

December delivered inconsistent value performance throughout the Bay Area, with San Francisco commanding appreciation while other regions exhibited varying outcomes. San Francisco concluded 2025 on a robust trajectory with single-family properties gaining 8.63% annually to achieve a median of $1,662,000, while condominiums climbed 5.21% to $1,075,000. Single-family properties continue securing substantial premiums, transacting for nearly 13% over asking value. Silicon Valley recorded a December recovery following November's uncommon comprehensive retreats, with San Mateo County commanding at 9.74% annual gains to $1,887,500, while Santa Clara County witnessed a moderate 0.55% decline to $1,800,000 and Santa Cruz remained relatively steady with a 0.79% advance to $1,270,000. Silicon Valley condominiums displayed fluctuation, with San Mateo declining 3.84%, Santa Clara advancing 1.71%, and Santa Cruz surging 10.48%.

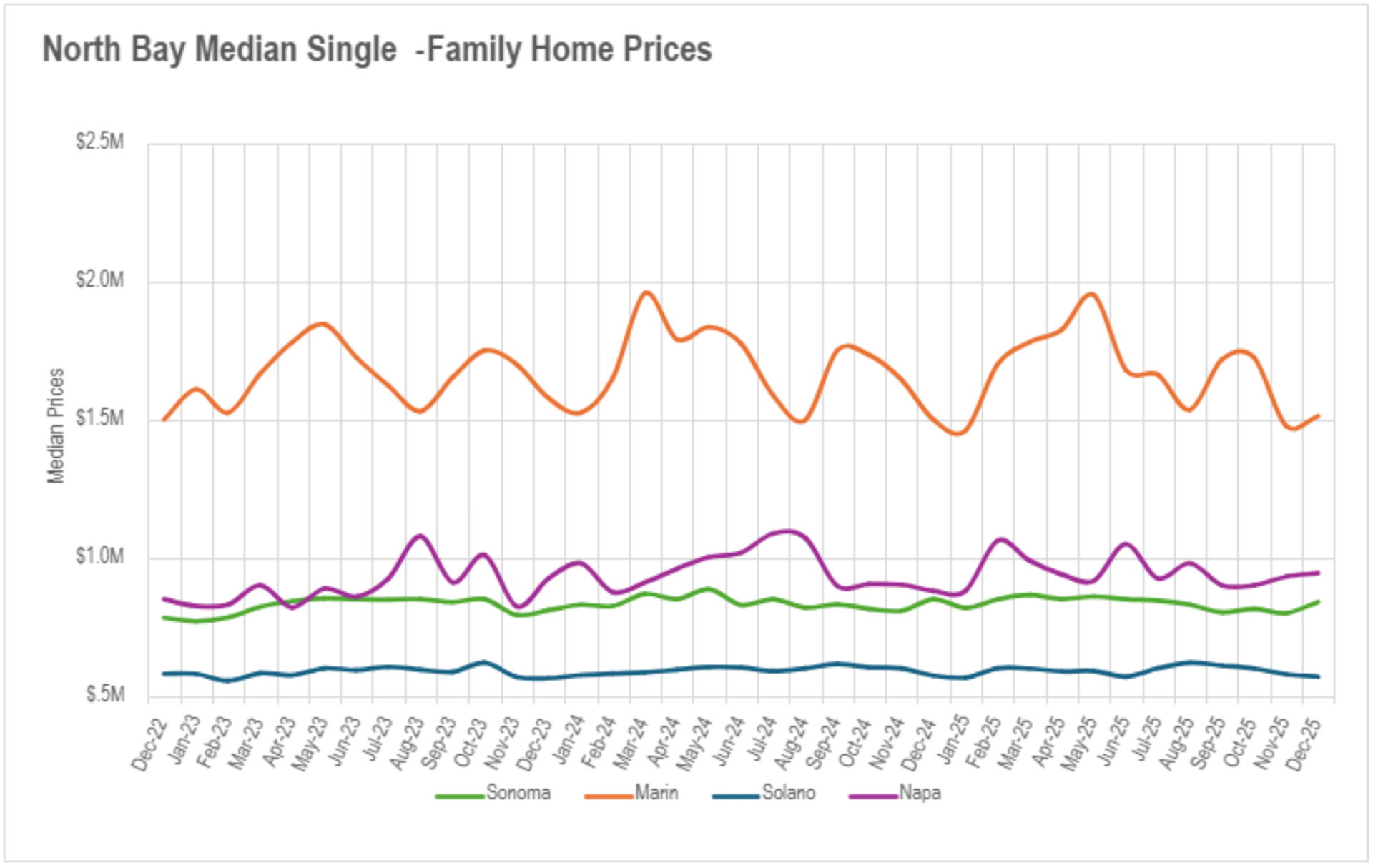

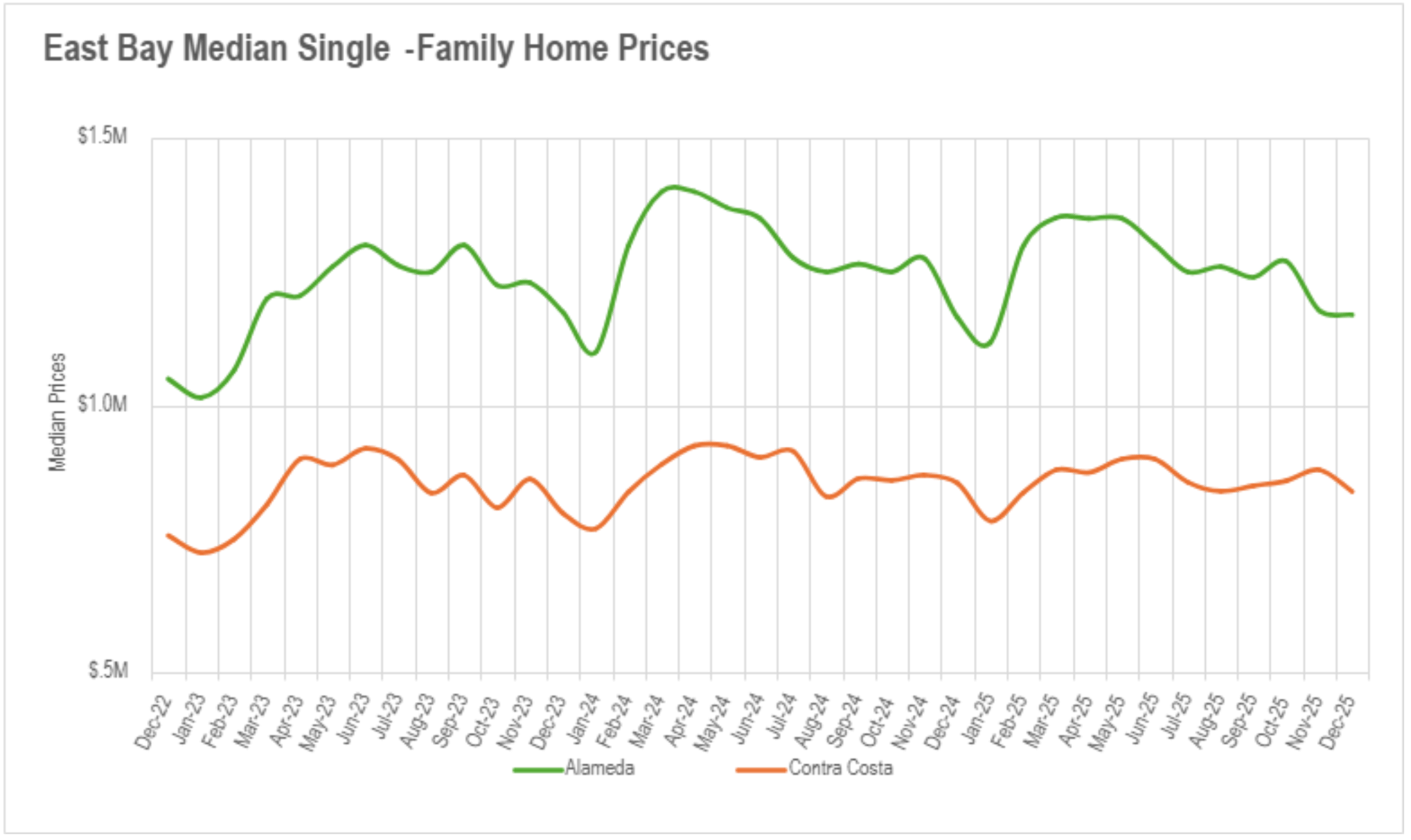

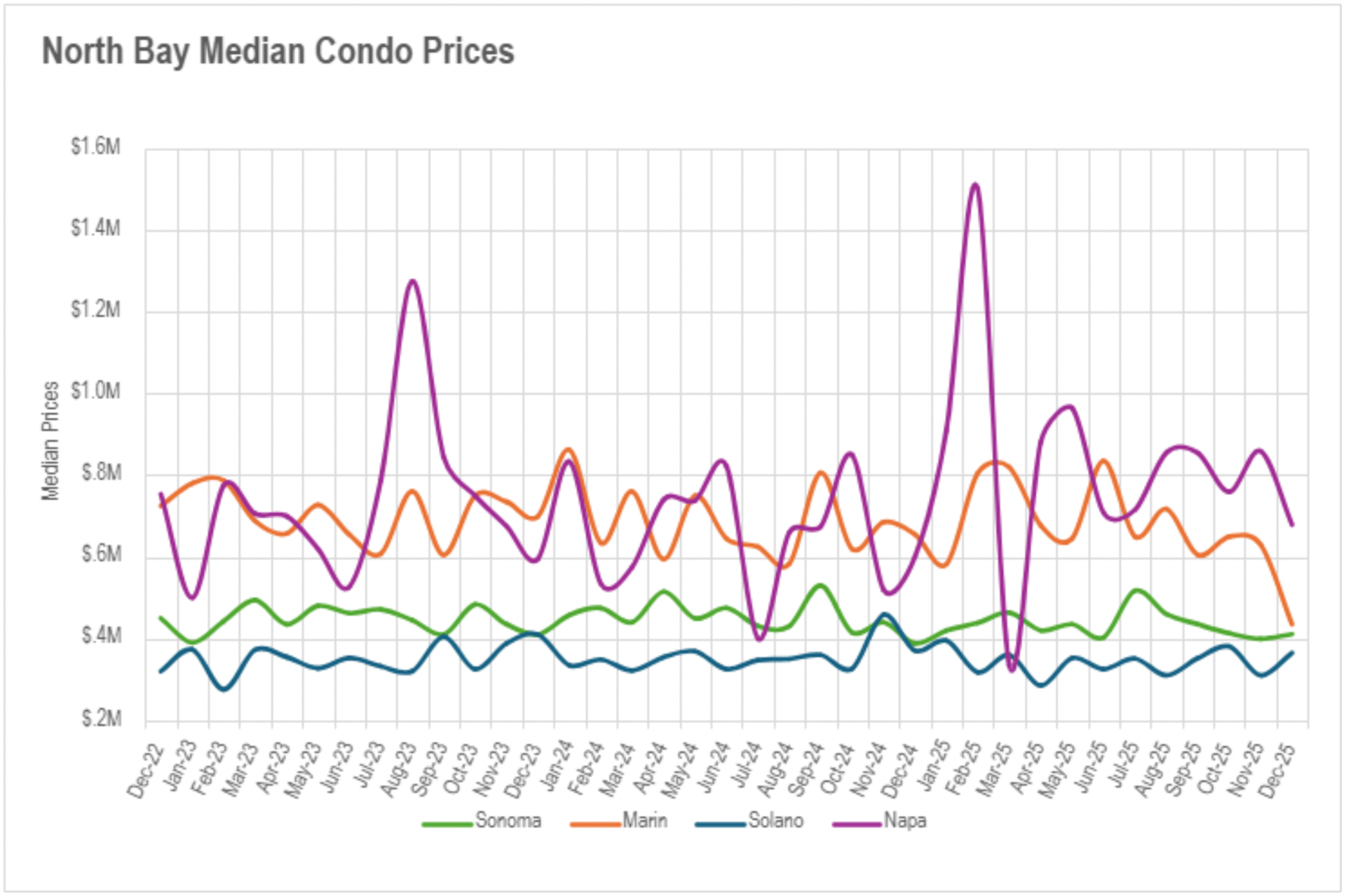

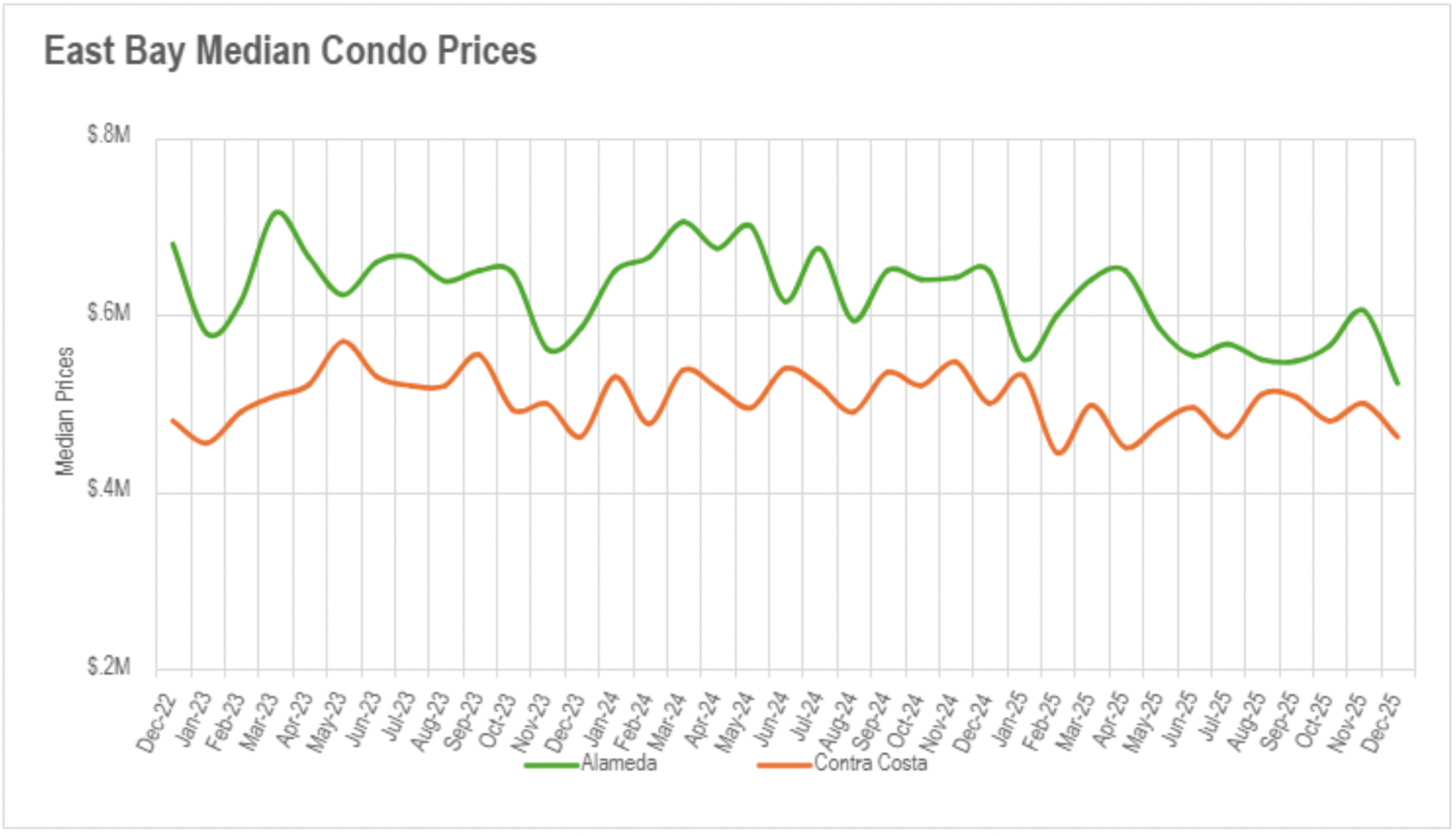

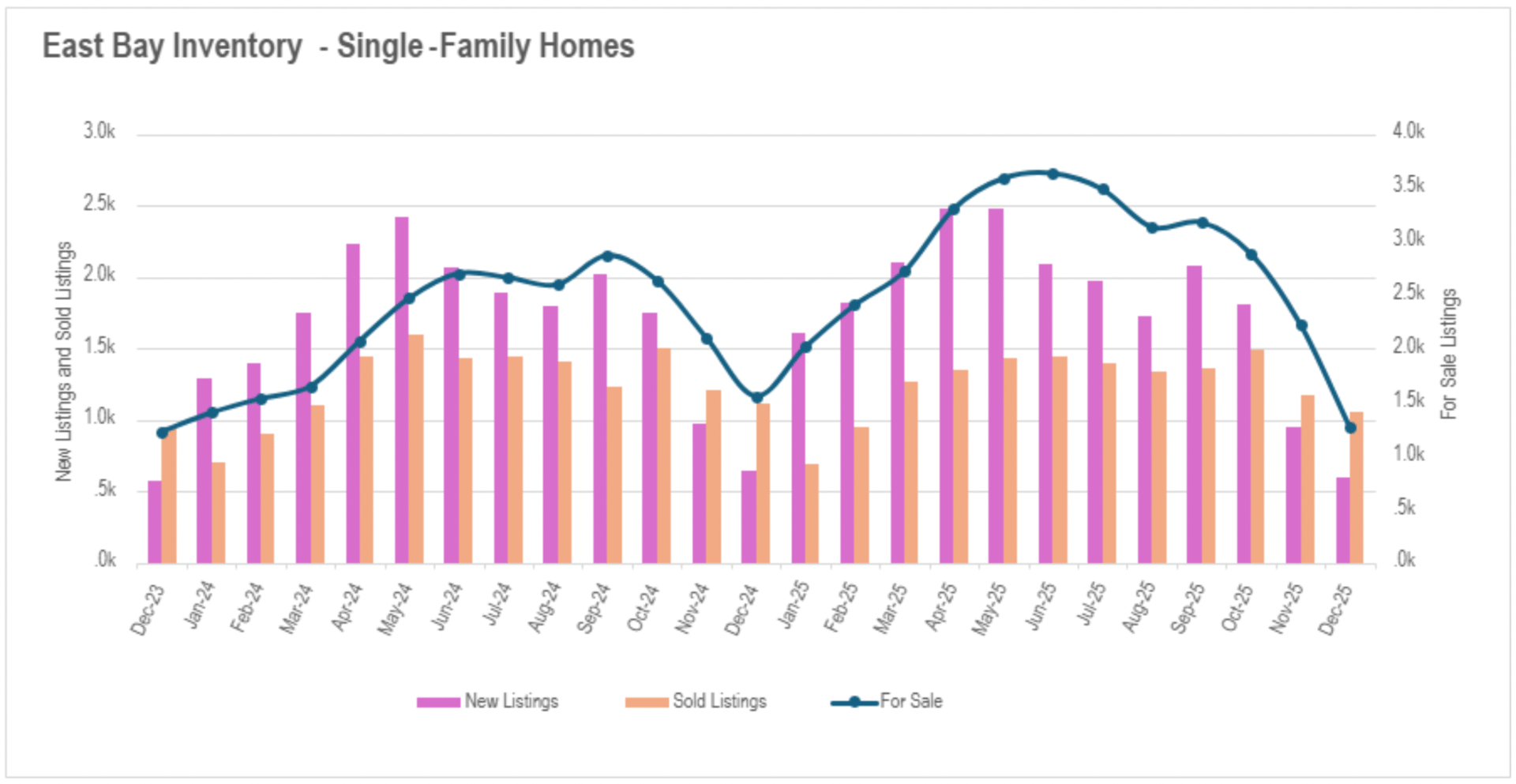

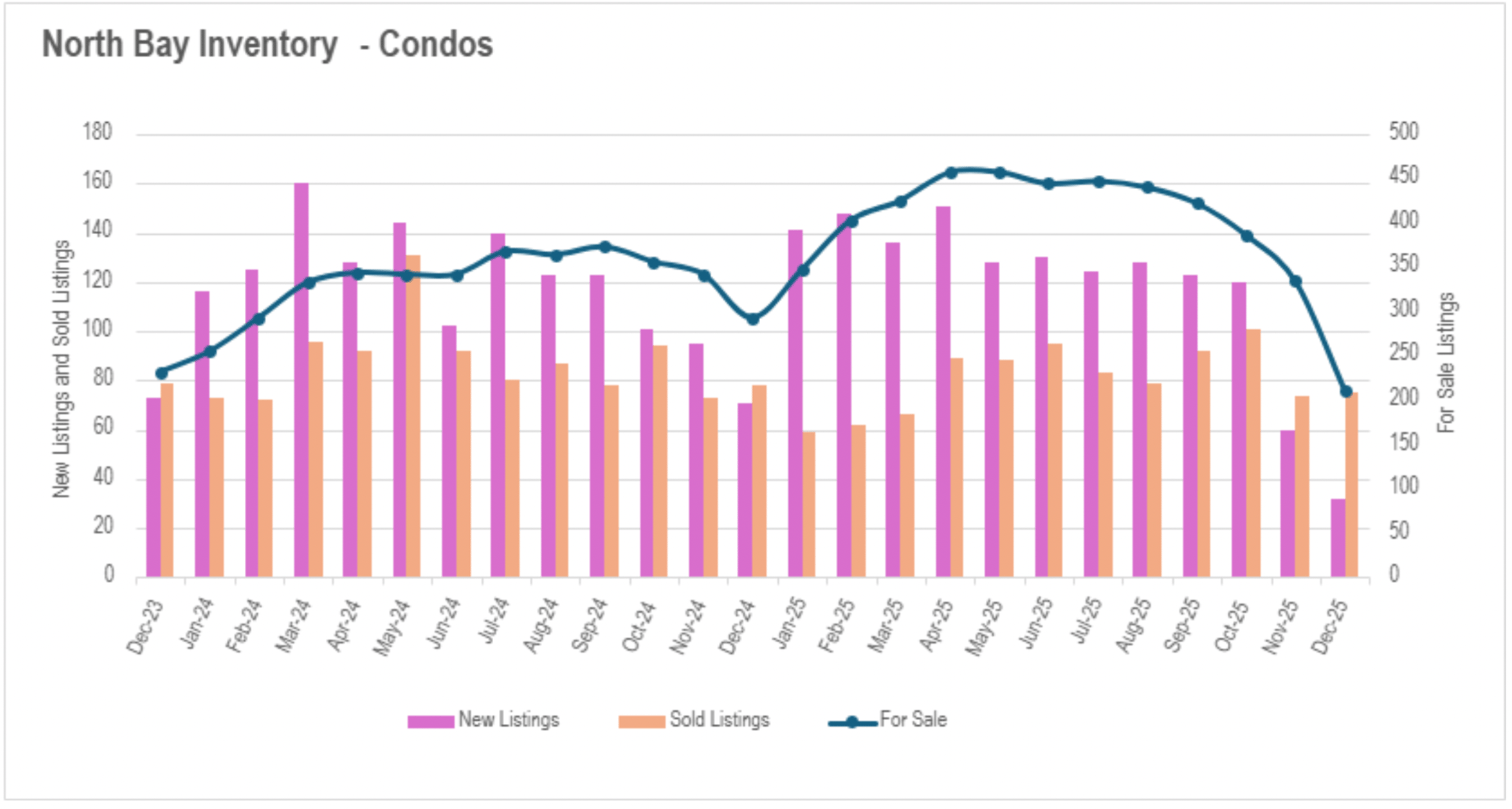

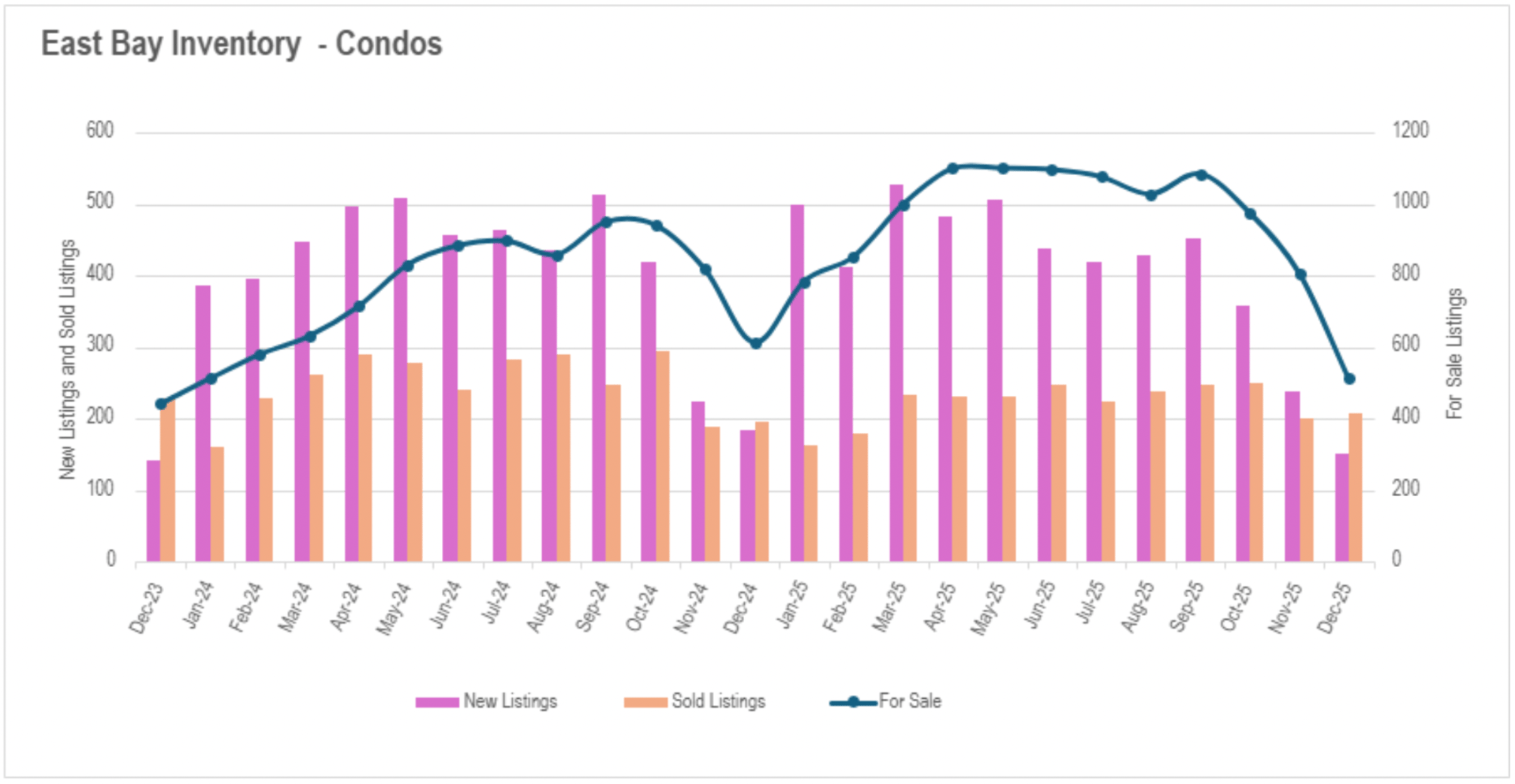

East Bay markets exhibited relative steadiness in single-family properties, with Alameda County advancing just 0.47% to $1,170,000 and Contra Costa declining 1.81% to $839,500, though condominiums perpetuated struggles with Alameda plummeting 19.55% to $522,500 and Contra Costa falling 7.60% to $462,000. North Bay regions presented divergent market conditions, with Napa County emerging as the distinct leader at 7.34% expansion to $944,624 and Marin advancing modestly 0.83% to $1,512,500, while Sonoma and Solano retreated by 1.18% and 0.61% respectively. North Bay condominiums demonstrated extreme fluctuation with Marin collapsing 33.59% while Sonoma climbed 5.86% and Napa gained 13.13%.

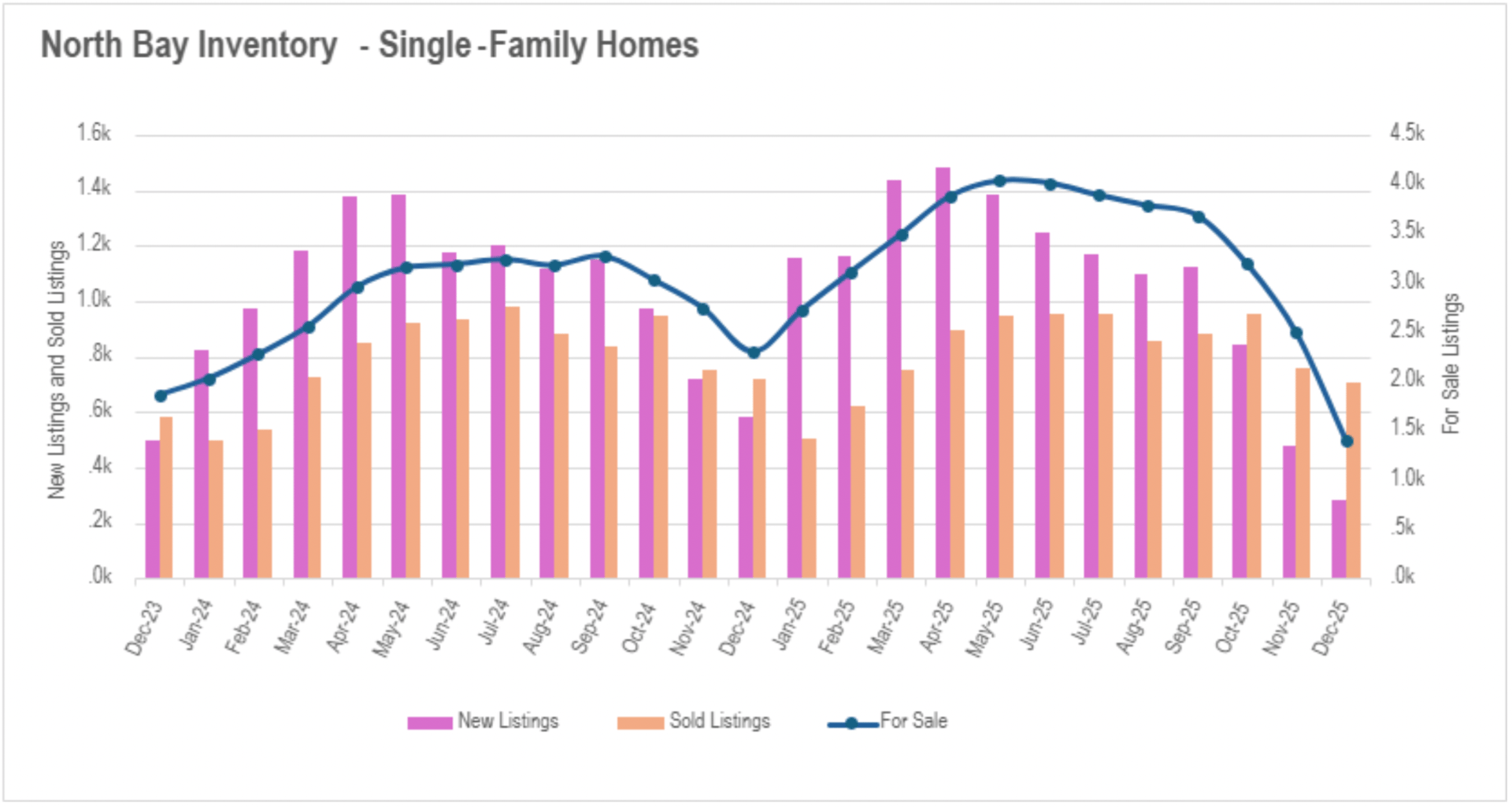

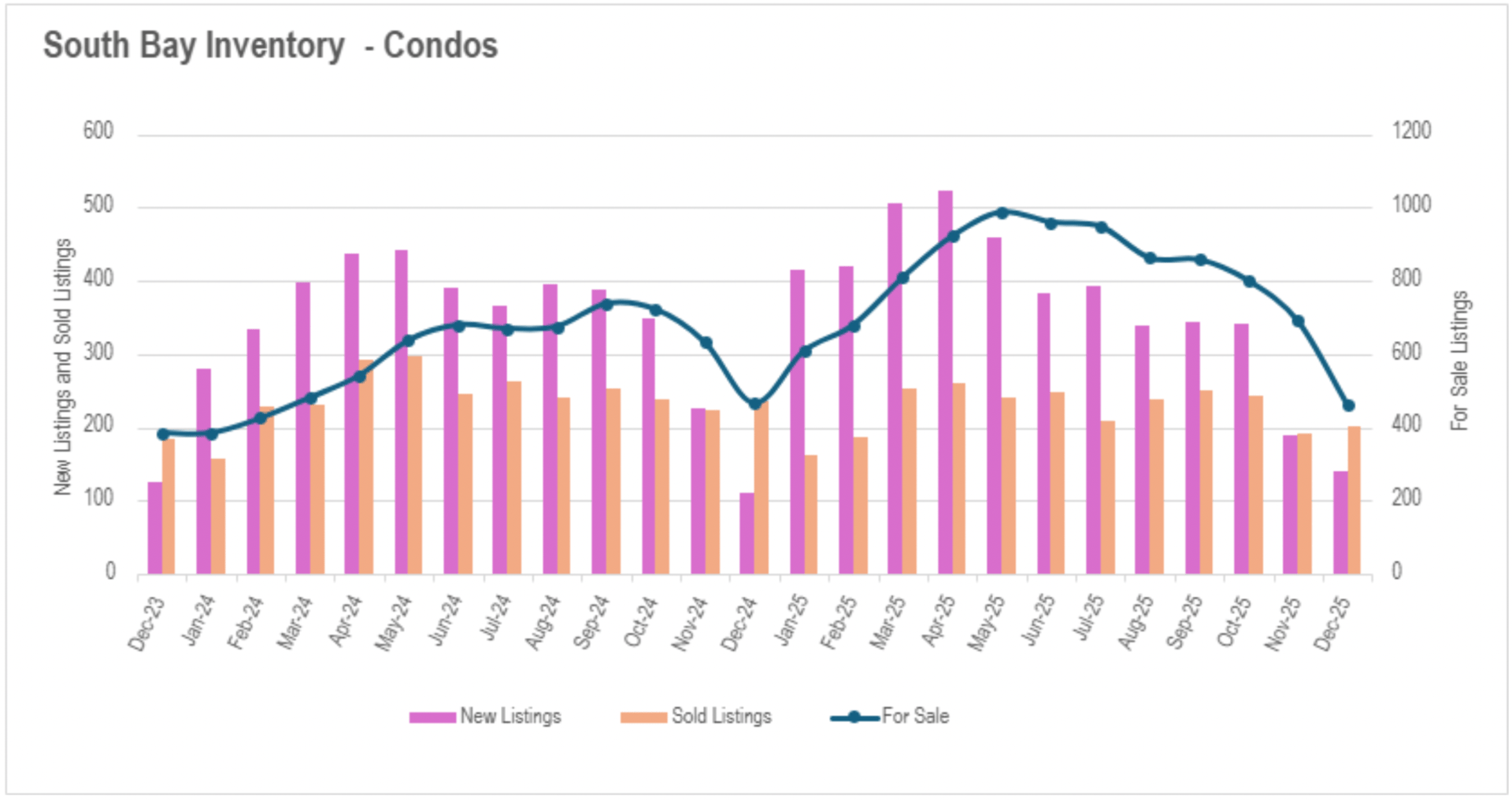

December produced an exceptional availability collapse throughout the entire Bay Area, establishing some of the most constrained supply circumstances documented in years. San Francisco achieved unprecedented levels with merely 93 single-family properties for transaction (declining 43.64% annually) and only 218 condominiums (declining 44.10%), producing a combined total of just 311 properties available in the entire municipality. Silicon Valley experienced similarly substantial compression, with single-family availability plunging 43.01% monthly and 21.02% annually to just 823 properties, while condominium availability declined 33.04% monthly though remained essentially unchanged annually.

North Bay regions witnessed single-family availability crater by 43.56% monthly and 38.85% annually to just 1,407 properties, while condominium availability fell 36.83% monthly and 27.99% annually to merely 211 units. This reduction was intensified by new listings plummeting 51.19% annually for single-family properties and 54.93% for condominiums. East Bay markets displayed relatively moderate but still meaningful reductions, with single-family availability declining 18.70% annually to 1,265 properties and condominium availability falling 16.48% to 512 units. Throughout all regions, the magnitude of availability reduction surpassed characteristic seasonal configurations, indicating that buyers who had been observing throughout 2025 finally commenced engaging, while new listings diminished substantially as sellers withdrew during the holidays.

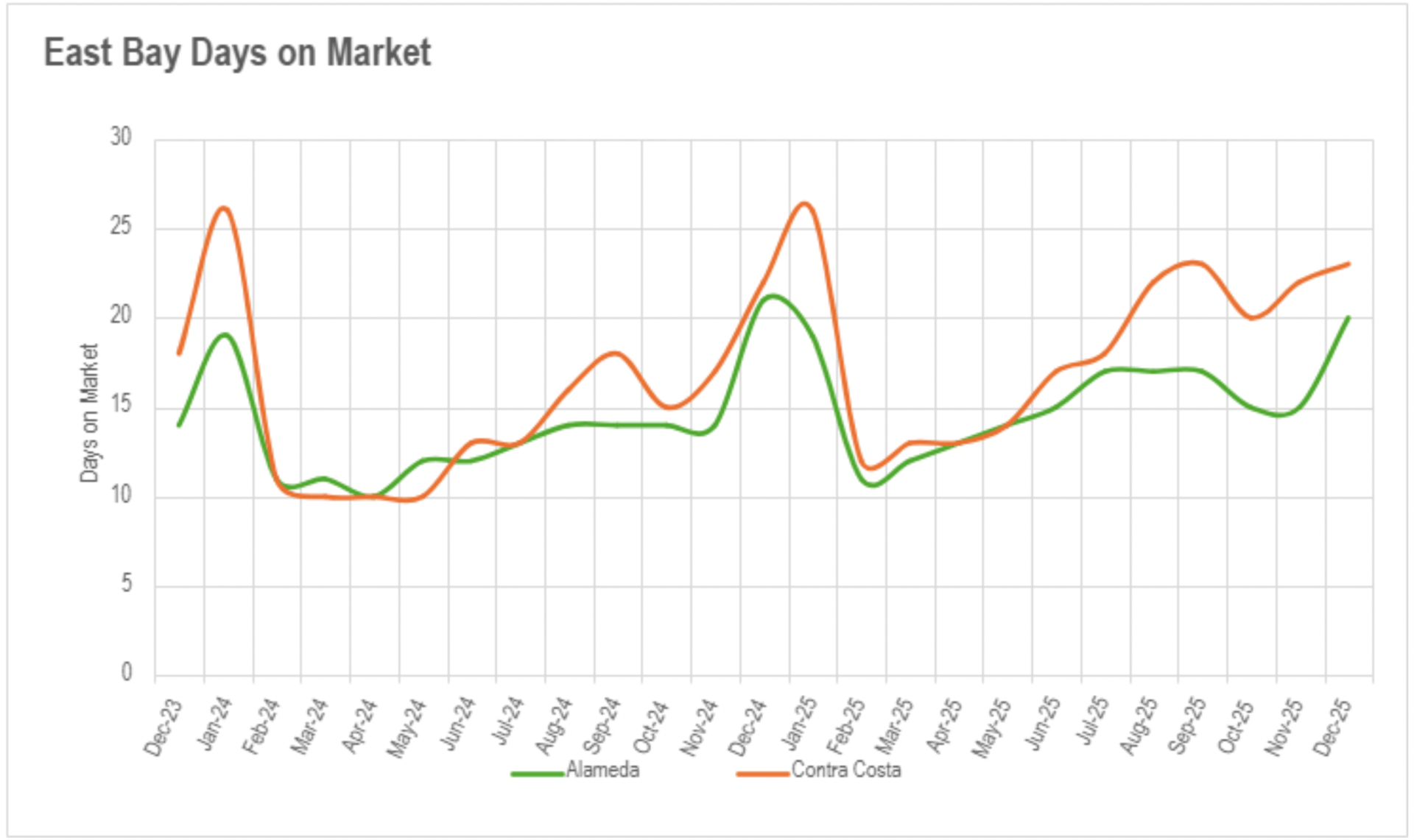

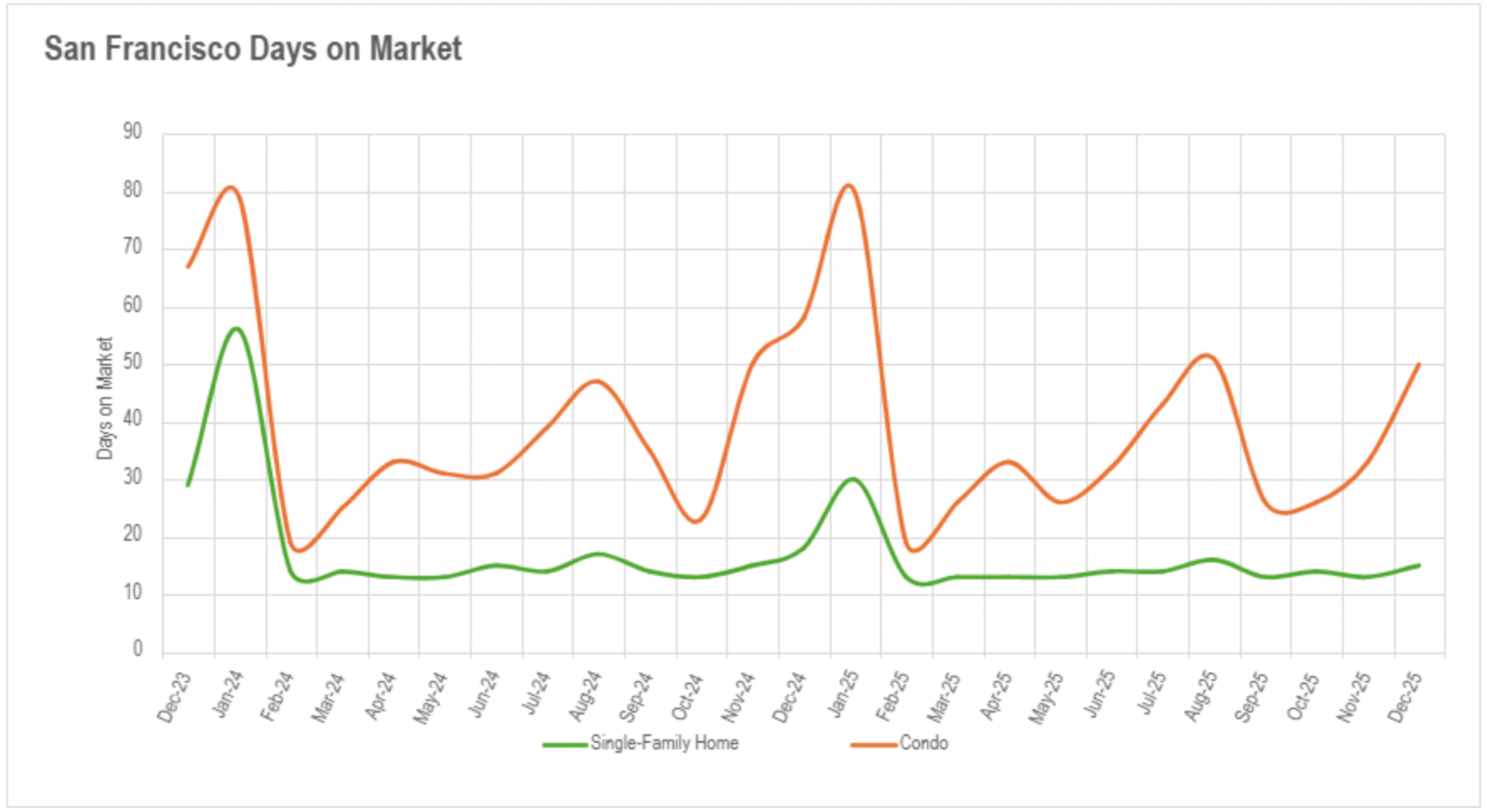

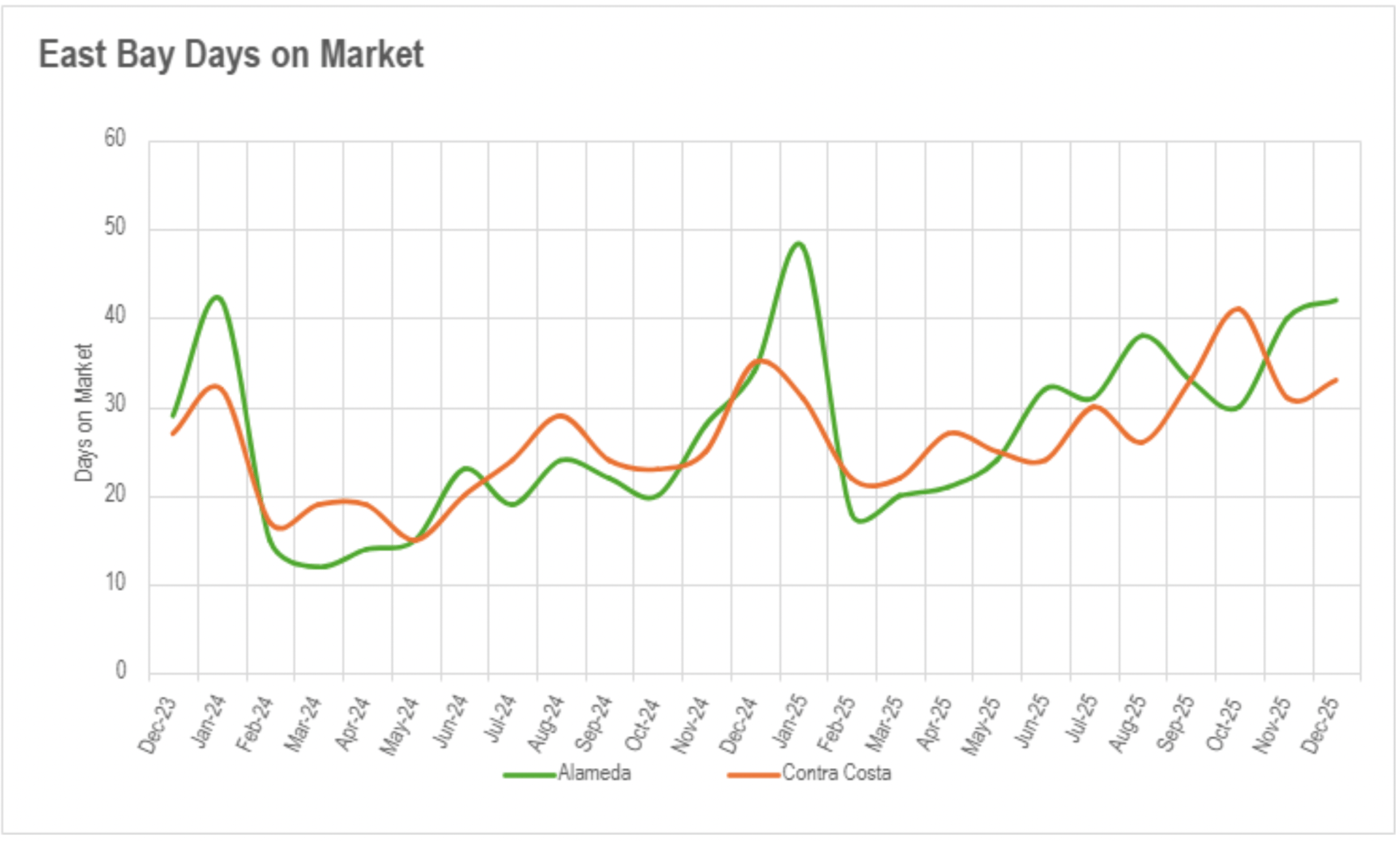

December's marketing duration metrics unveiled pronounced differences throughout regions and property categories, with certain markets intensifying substantially while others decelerated despite constrained availability. San Francisco witnessed the most substantial acceleration, with single-family properties transacting in merely 15 days (declining 16.67% annually) and condominiums moving in 50 days (declining 13.79%), establishing an intensely competitive environment with minimal duration for buyer consideration. East Bay single-family markets also accelerated, with Alameda County properties transacting in 20 days (declining 4.76% annually) and Contra Costa at 23 days, while condominiums decelerated meaningfully with Alameda averaging 42 days (advancing 23.53%) and Contra Costa at 33 days.

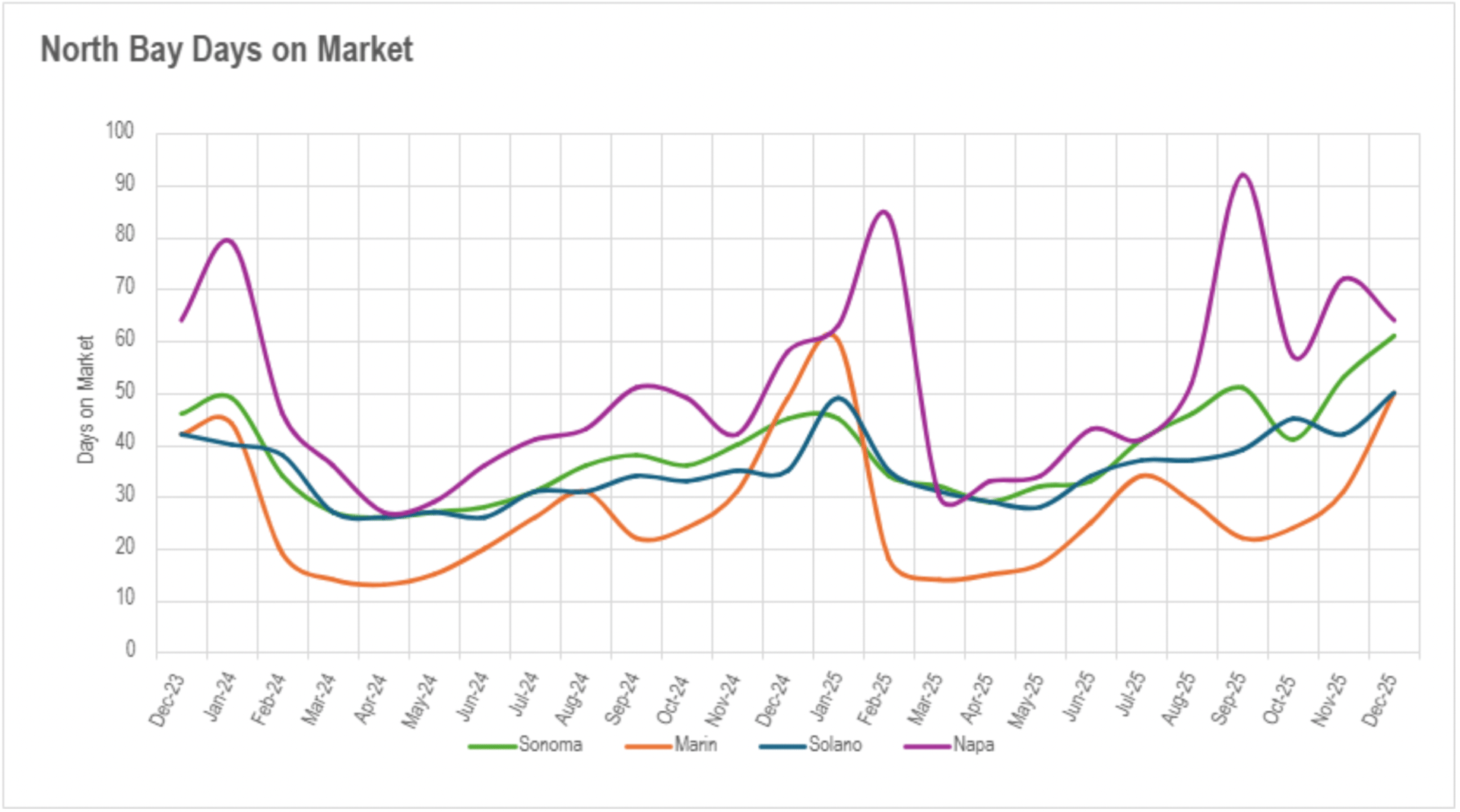

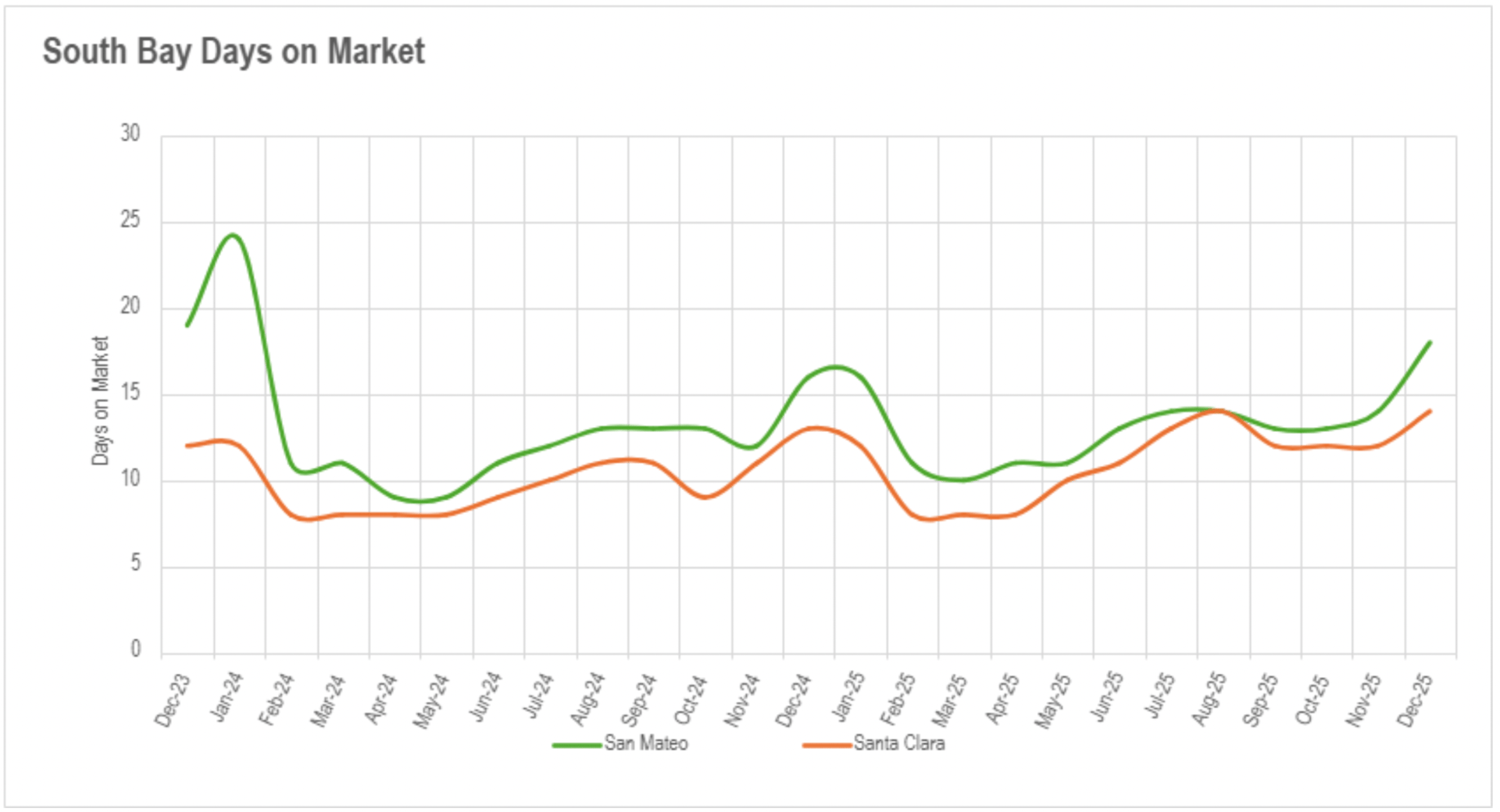

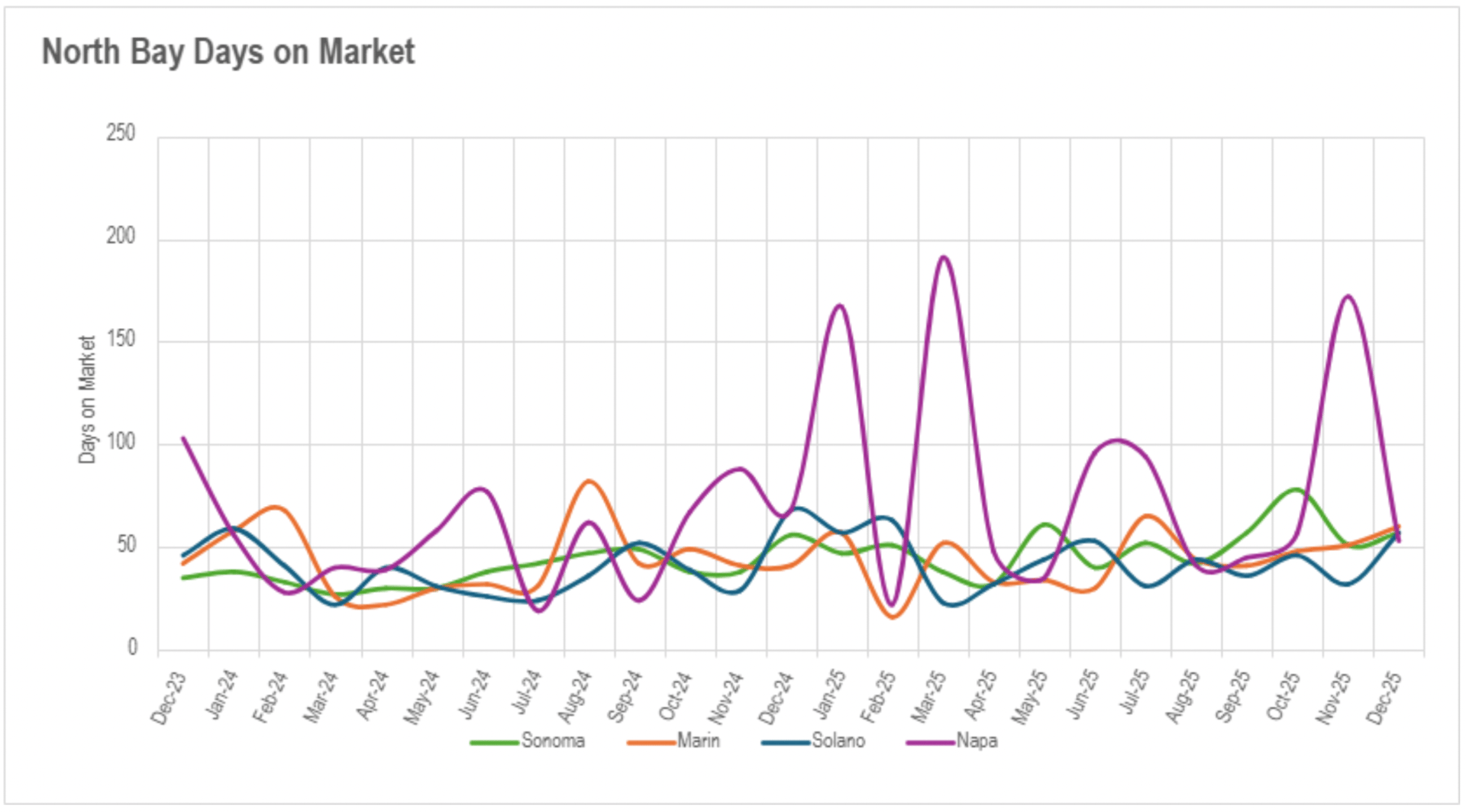

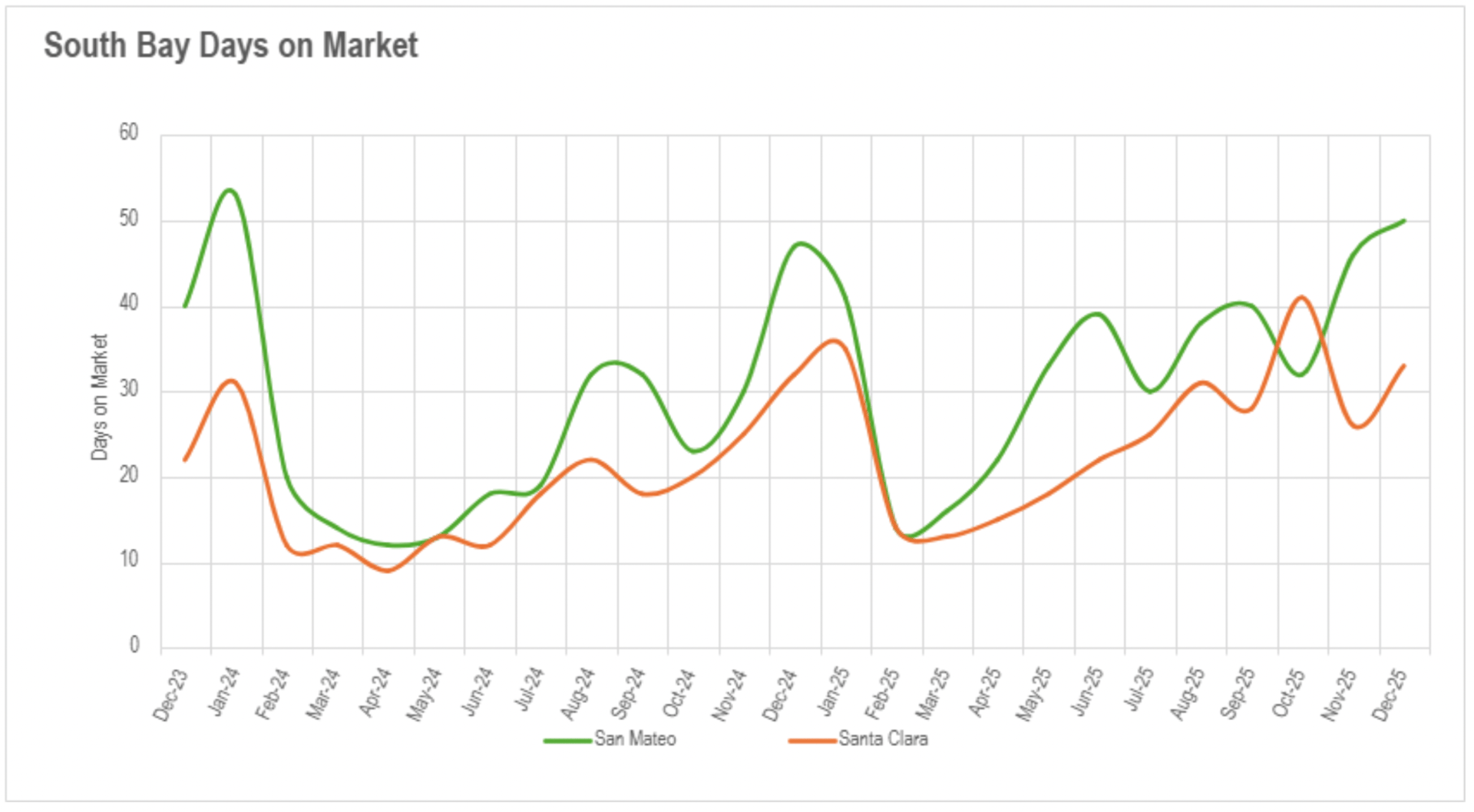

Silicon Valley presented pronounced contrasts by county - San Mateo and Santa Clara sustained relatively expeditious movement at 18 and 14 days for single-family properties (though advancing 12.50% and 7.69% respectively), while Santa Cruz County recorded a substantial slowdown with properties requiring 43 days to transact (advancing 65.38% annually). Silicon Valley condominiums exhibited inconsistent outcomes with modest increases in San Mateo and Santa Clara, while Santa Cruz condominiums actually accelerated with a 16.13% reduction. North Bay regions demonstrated the most extensive slowdown despite availability collapse, with single-family properties in Sonoma requiring 61 days on market (advancing 35.56%), Solano at 50 days (advancing 42.86%), and even Marin increasing modestly by 2.04%. Nevertheless, Napa County condominiums reversed the pattern with a 22.06% reduction in market duration.

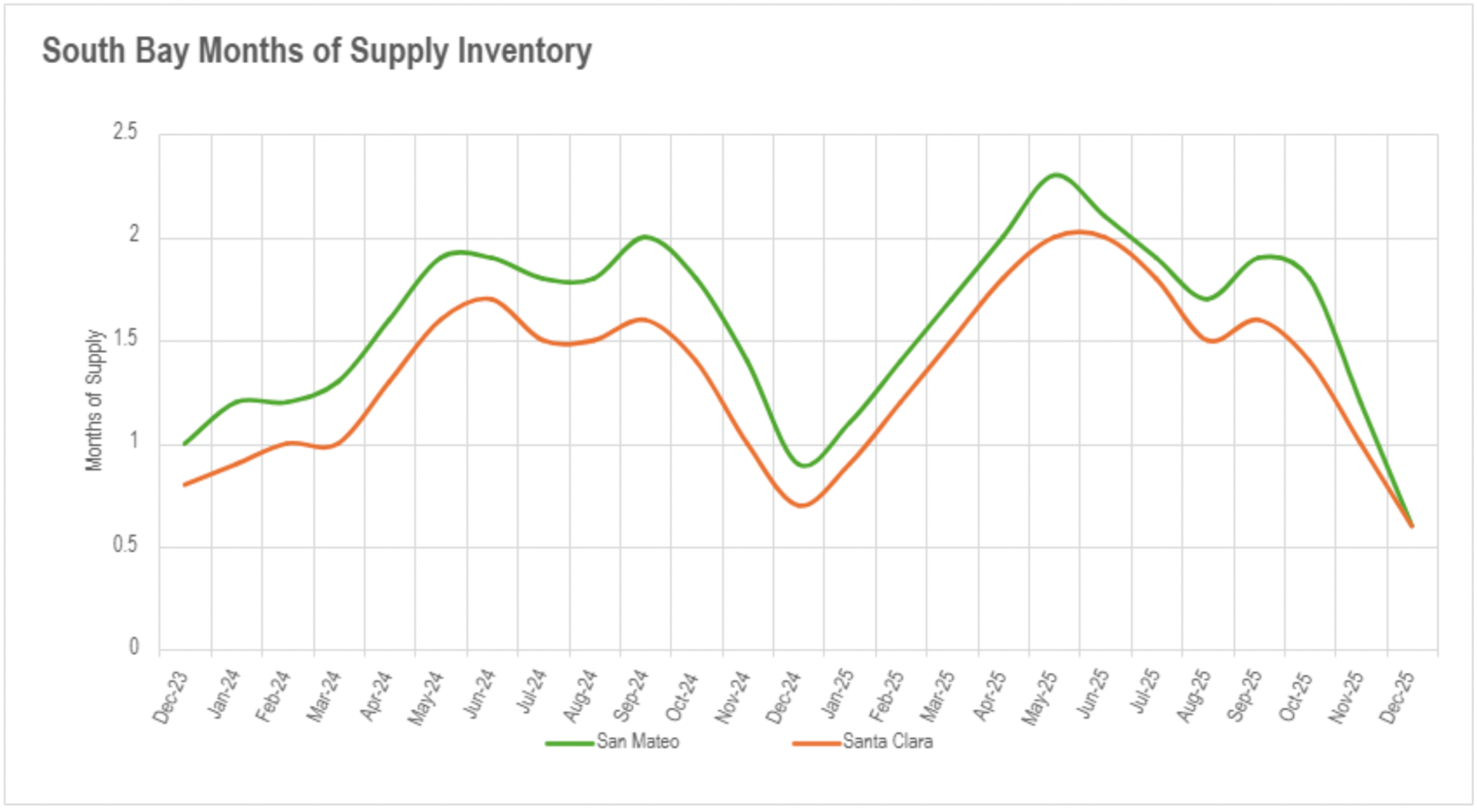

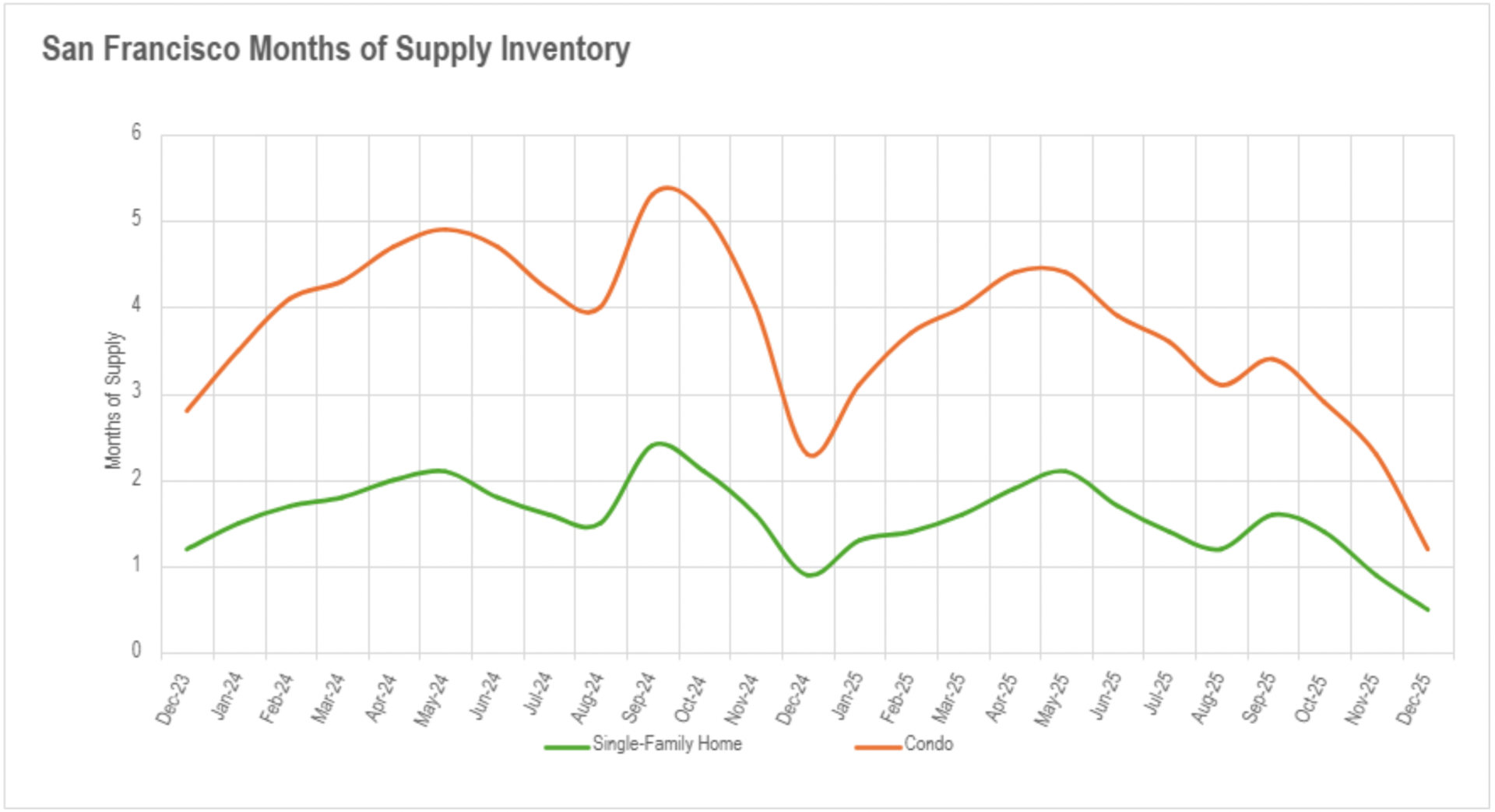

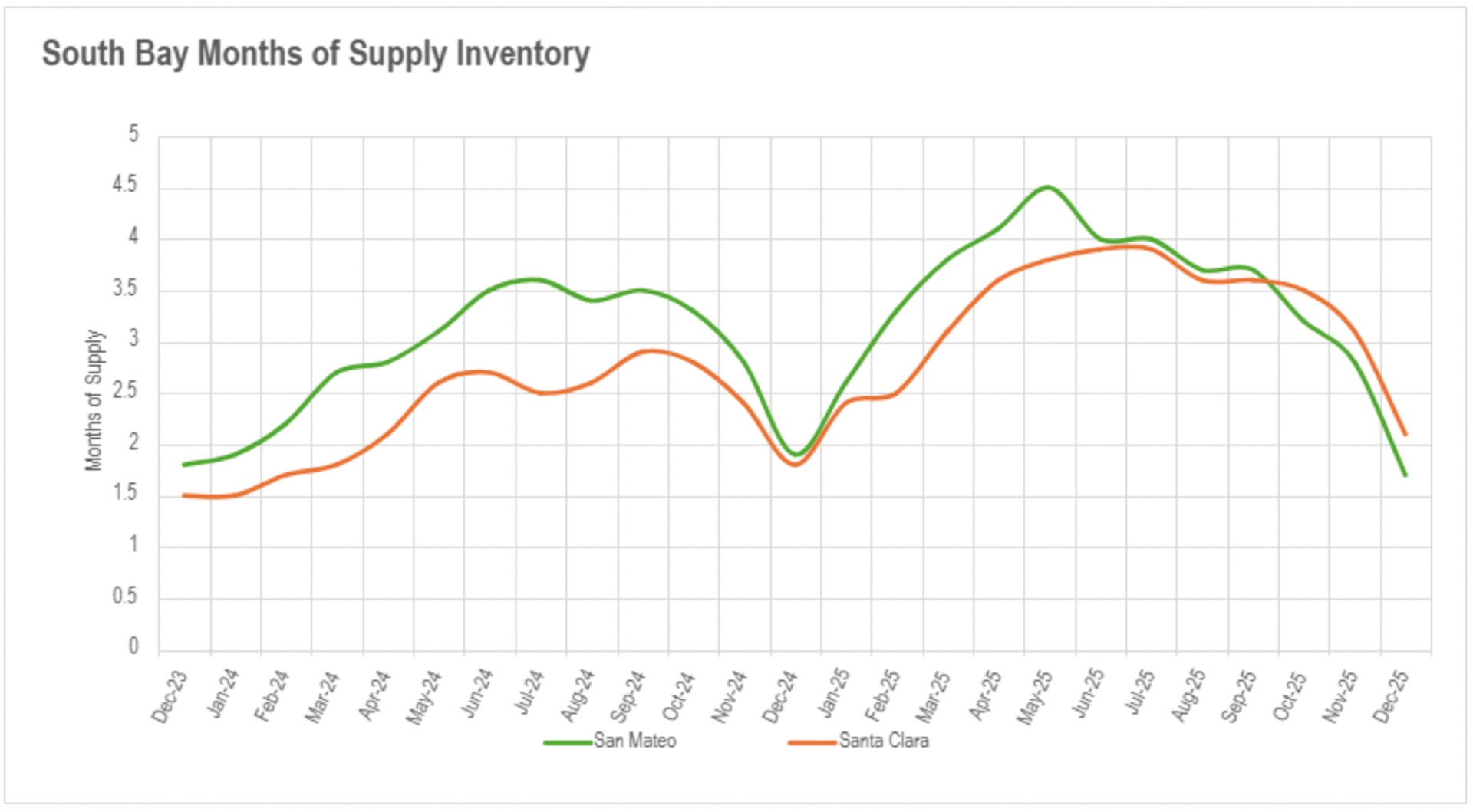

December's availability collapse advanced the entire Bay Area into extreme seller-favorable market territory, with certain regions achieving the most constrained supply limitations in years. San Francisco accomplished the most extreme circumstances in the state with merely 0.5 months of single-family property supply and 1.2 months of condominium availability - some of the minimal MSI figures documented in years with no indication of mitigation. Silicon Valley achieved similarly extreme levels, with San Mateo and Santa Clara Counties both at merely 0.6 months of single-family property supply (declining 33.33% and 14.29% annually respectively), while even Santa Cruz contracted to 2.0 months (declining 28.57%). Silicon Valley condominiums transitioned decisively toward seller-favorable markets with San Mateo at 1.7 months, Santa Clara at 2.1 months, and Santa Cruz at 3.2 months.

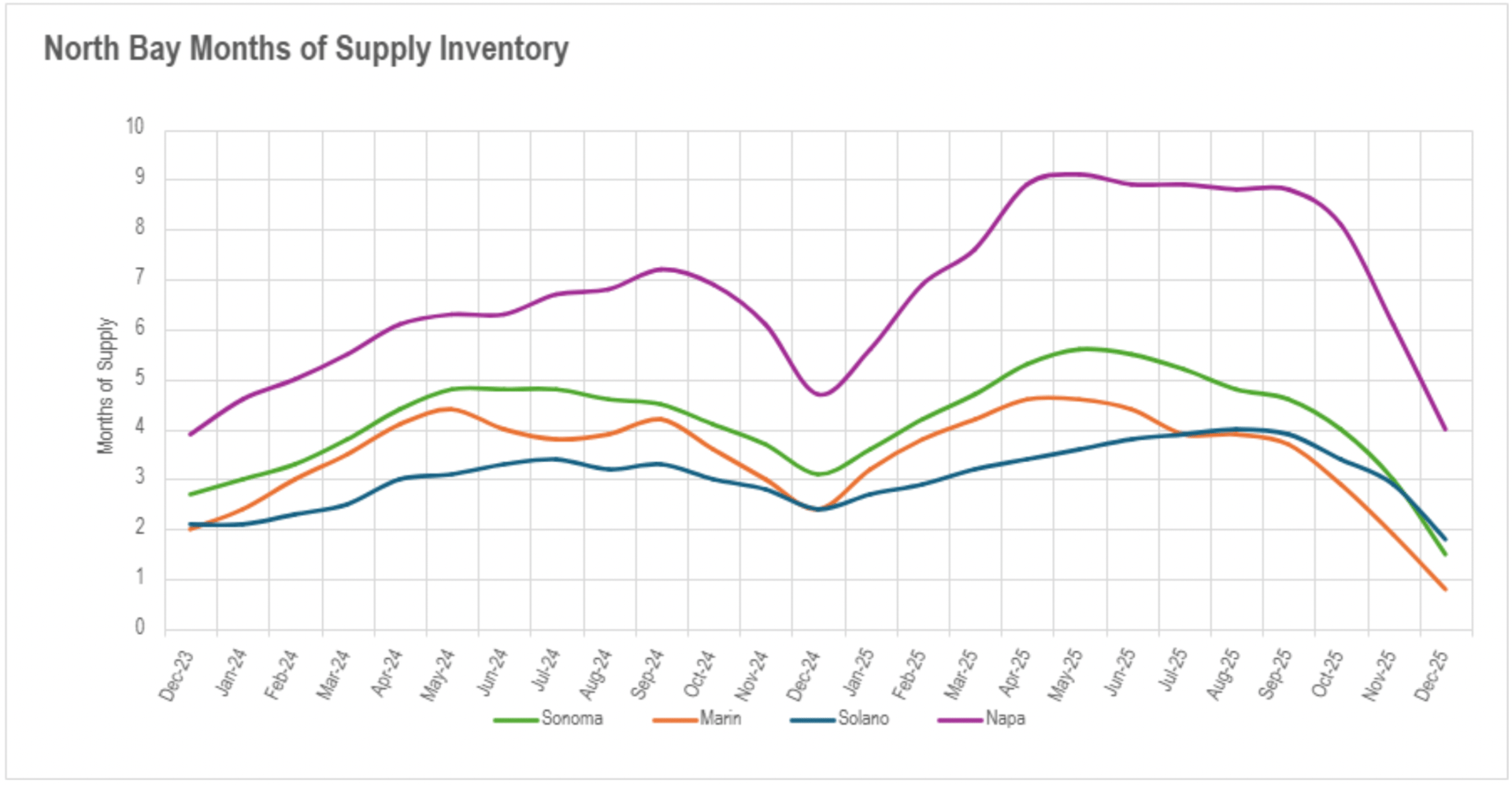

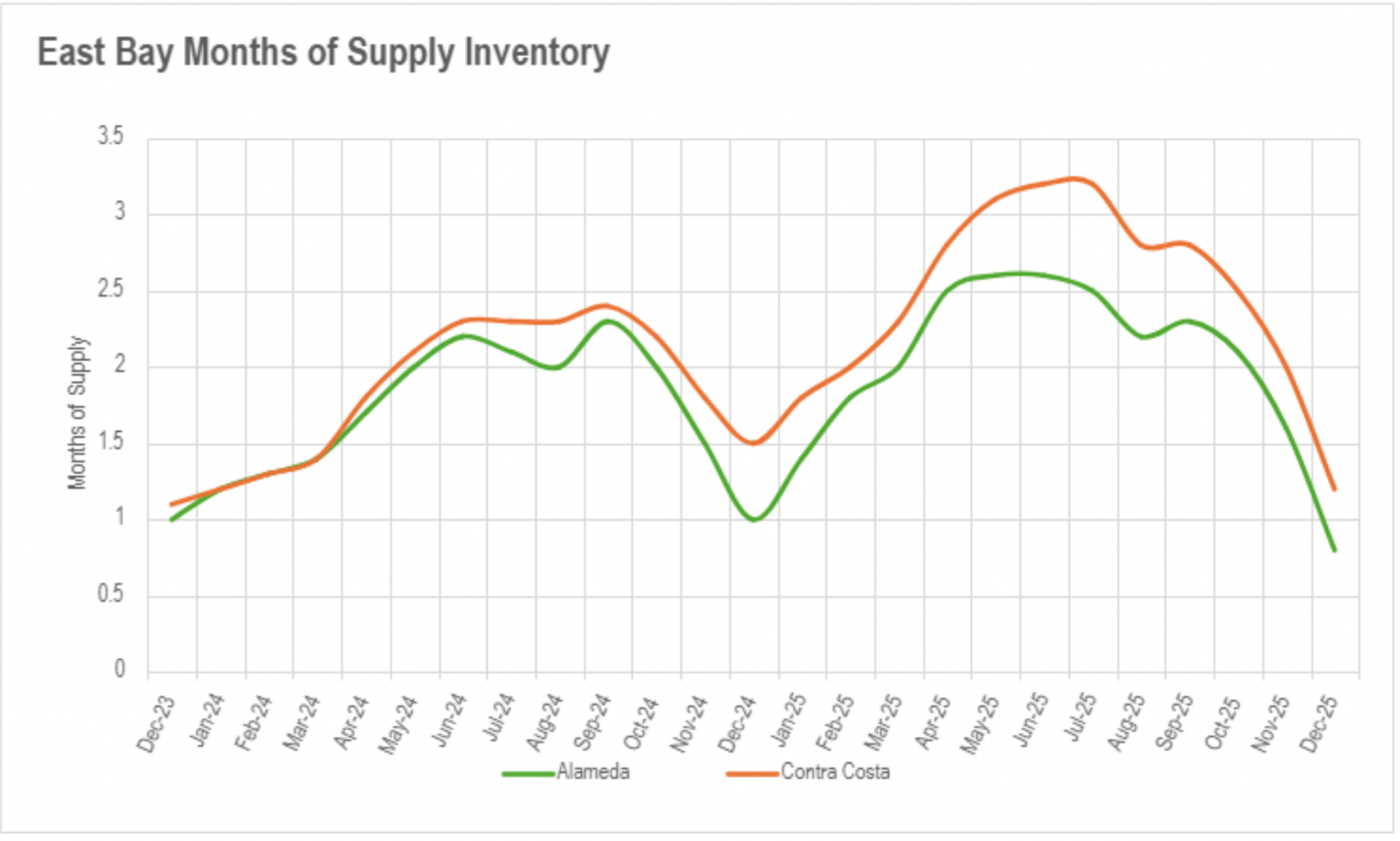

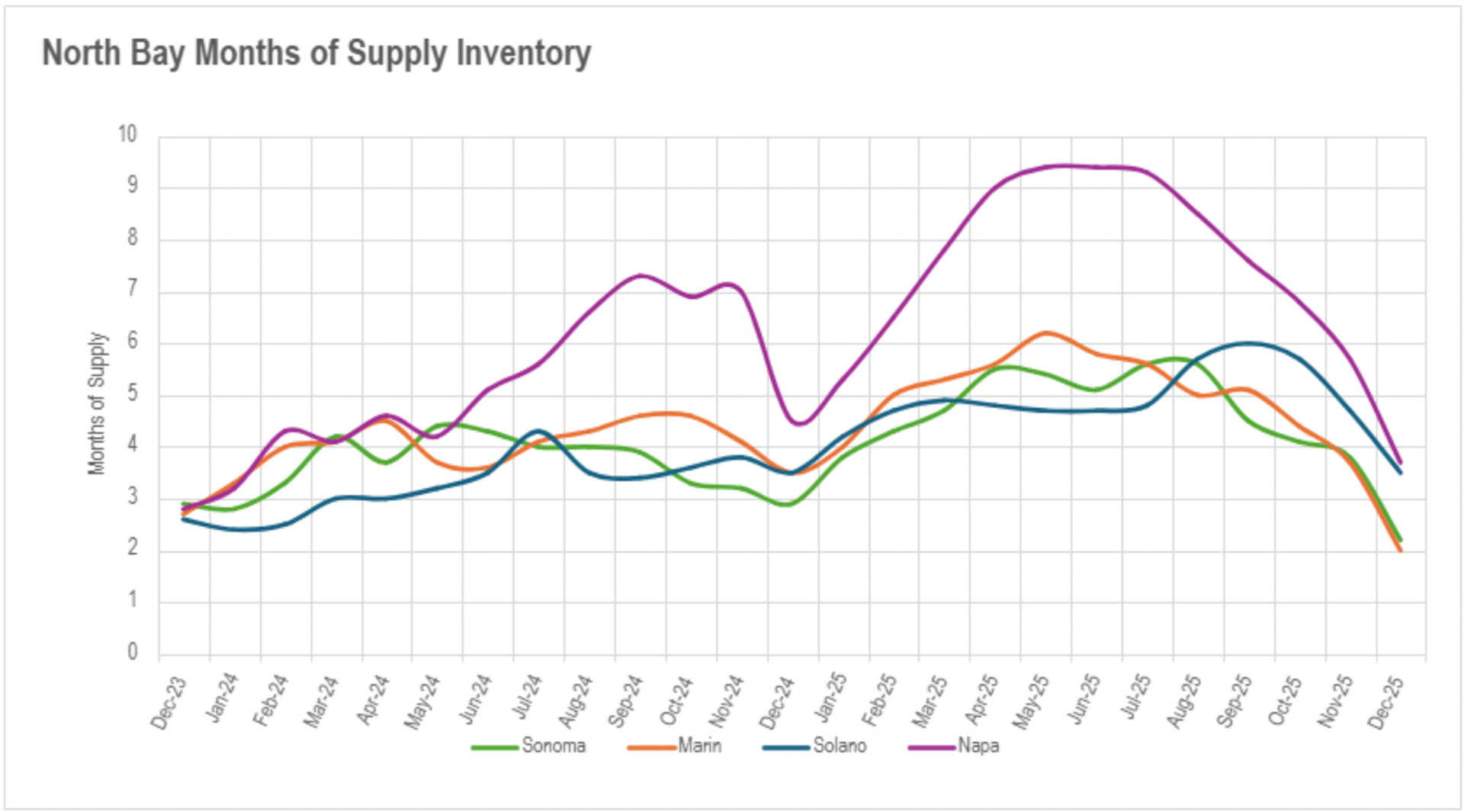

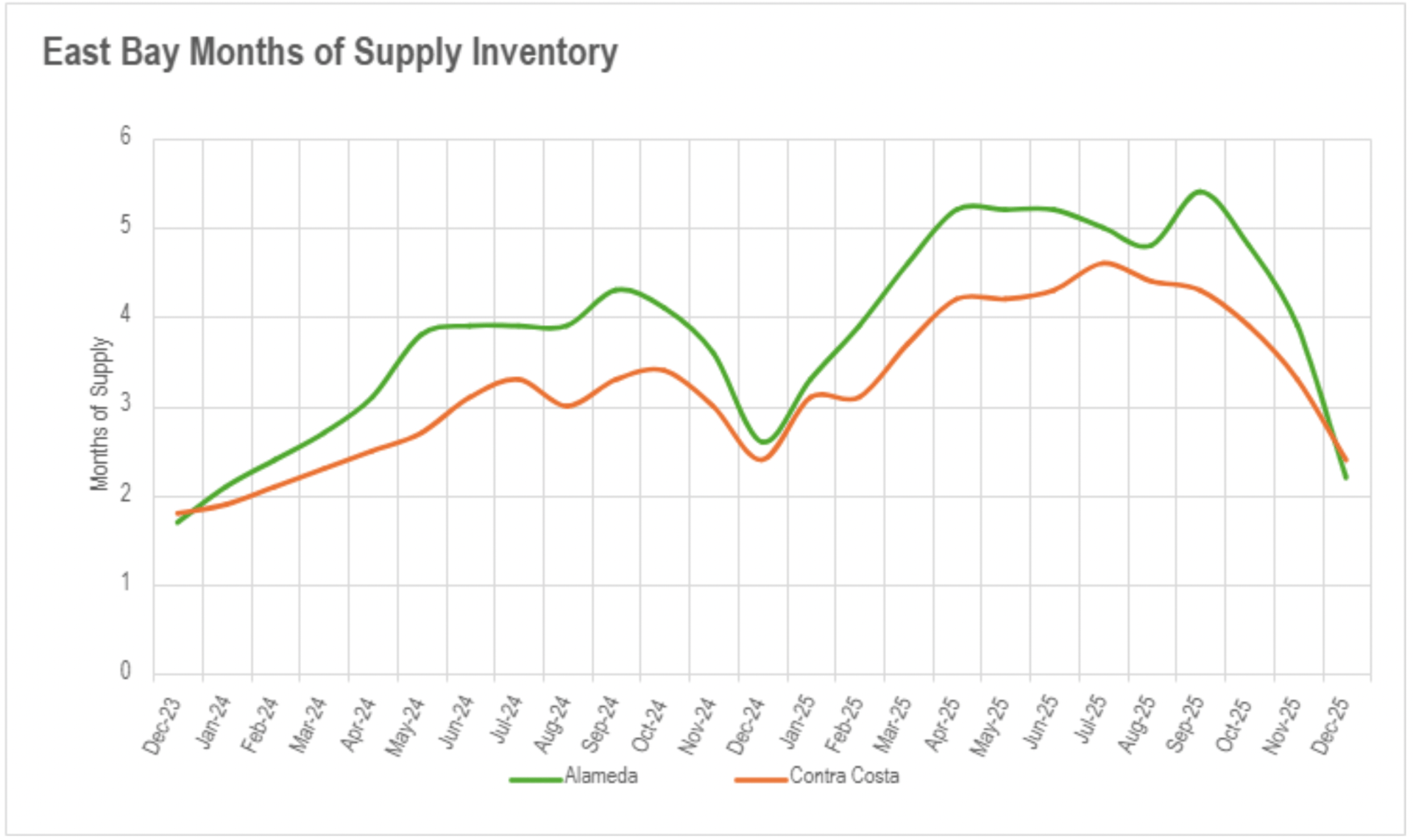

East Bay markets concluded the year with exceptionally constrained circumstances, registering merely 0.8 months of single-family availability in Alameda County and 1.2 months in Contra Costa (both declining 20% annually), while even condominiums transitioned into seller territory at 2.2 and 2.4 months respectively. North Bay regions experienced a substantial holiday period transformation, with Marin County commanding at an extreme 0.8 months of single-family supply (declining 66.67% annually), Sonoma at 1.5 months, Solano at 1.8 months, and even Napa - which had maintained buyer-favorable conditions throughout 2025 - contracting to 4.0 months. North Bay condominiums also compressed considerably with Marin at 2.0 months, Sonoma at 2.2 months, and Solano and Napa at 3.5 and 3.7 months respectively. This regionwide transformation into seller-favorable market territory, combined with historically minimal new listing engagement, indicates intense competition will perpetuate into early 2026 until meaningful new availability enters the market.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

April 24, 2026

April 18, 2026

April 17, 2026

April 11, 2026

March 21, 2026

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

You've got questions and we can't wait to answer them.