February Market Update

Single-family property values are accelerating in San Francisco and portions of North Bay markets, with annual advances exceeding 16% and 19% in San Francisco and Marin County, respectively, while other segments of the region record moderate retreats.

Availability levels have contracted throughout the Bay Area, with single-family property availability declining by double digits in every submarket on an annual basis.

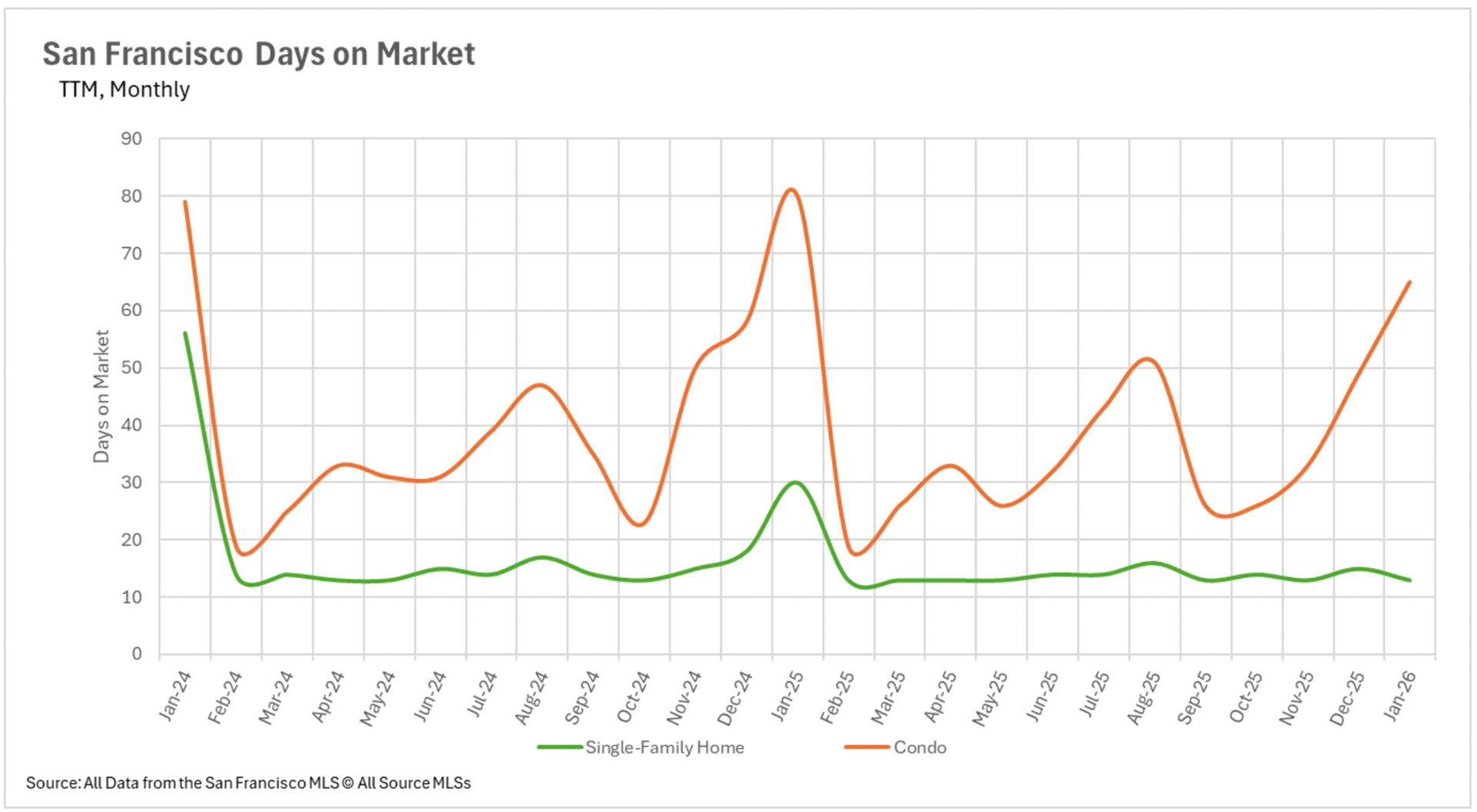

Condominiums perpetuate challenges with valuation and extended marketing periods, while single-family properties are transacting rapidly in numerous areas.

Nearly every single-family property market in the Bay Area maintains decisively seller-favorable territory, with several counties registering at or beneath one month of supply.

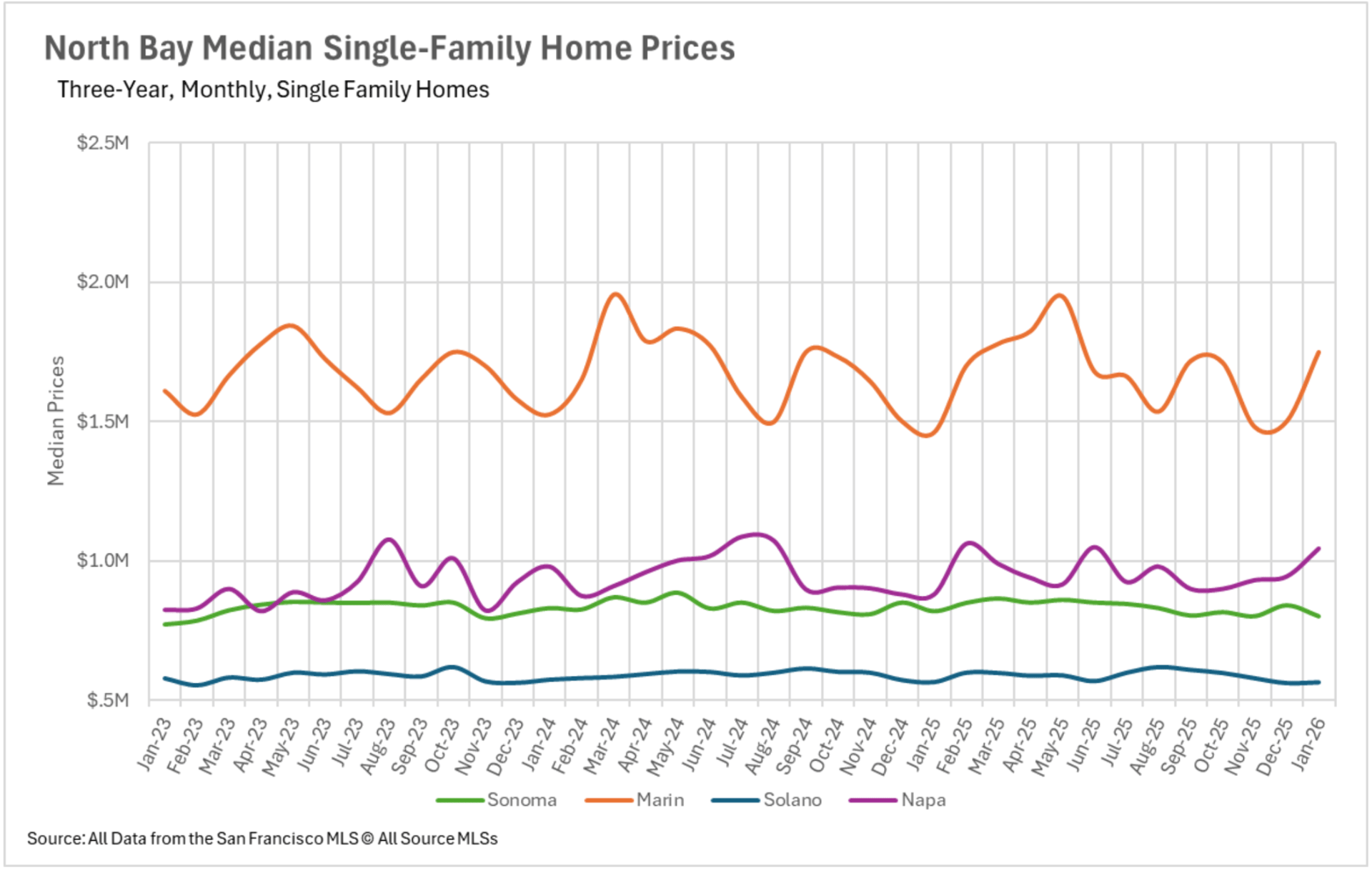

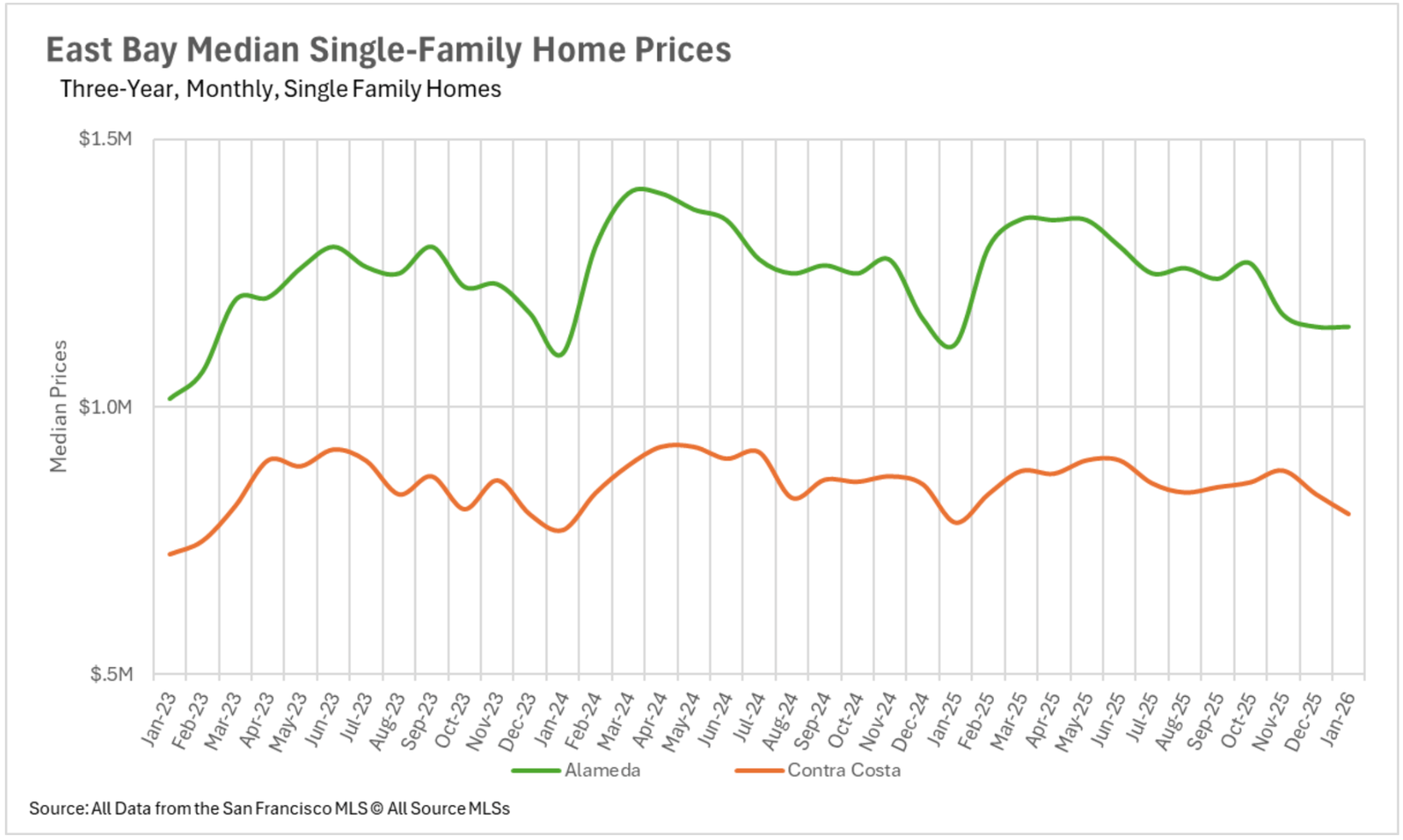

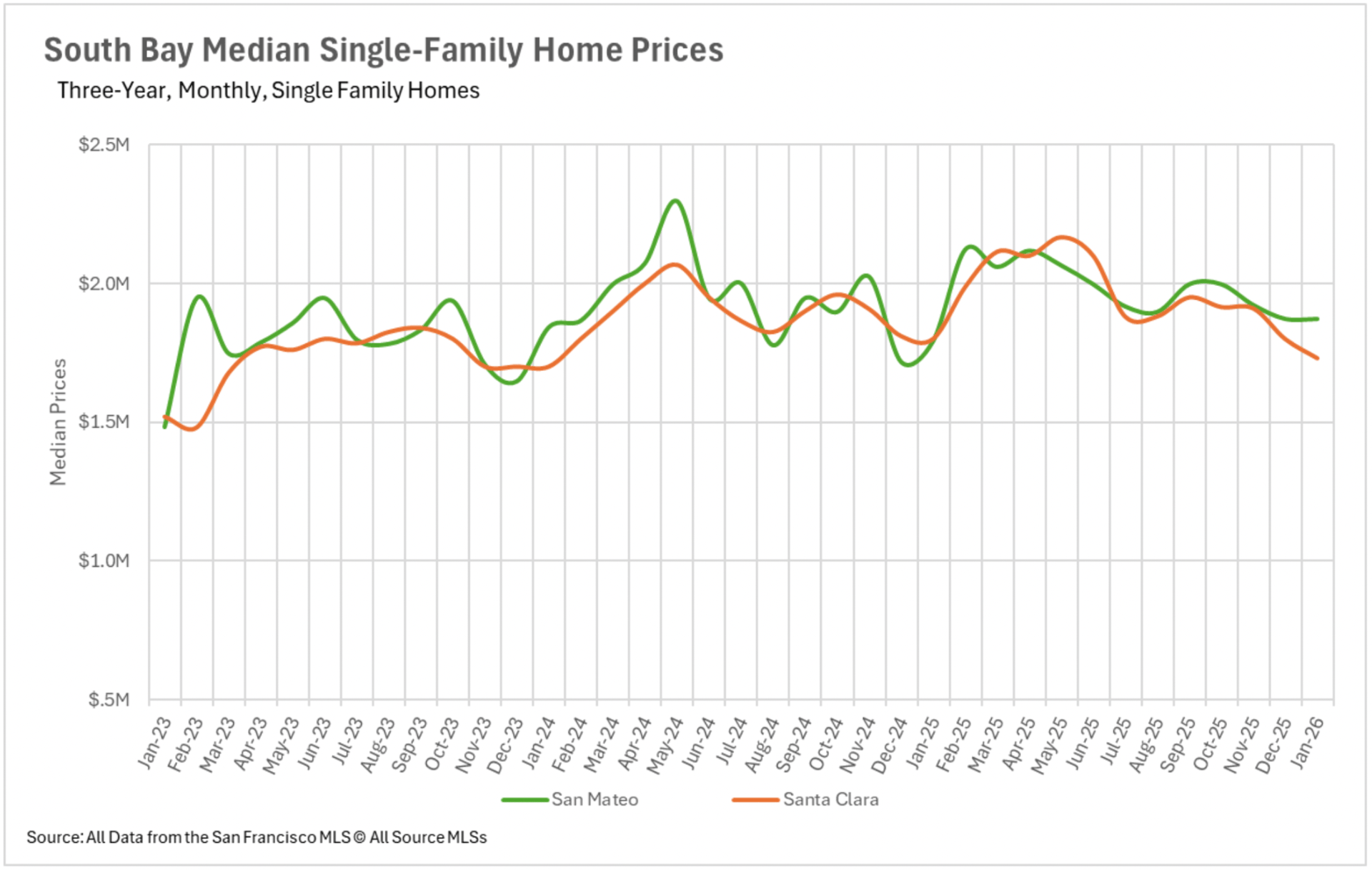

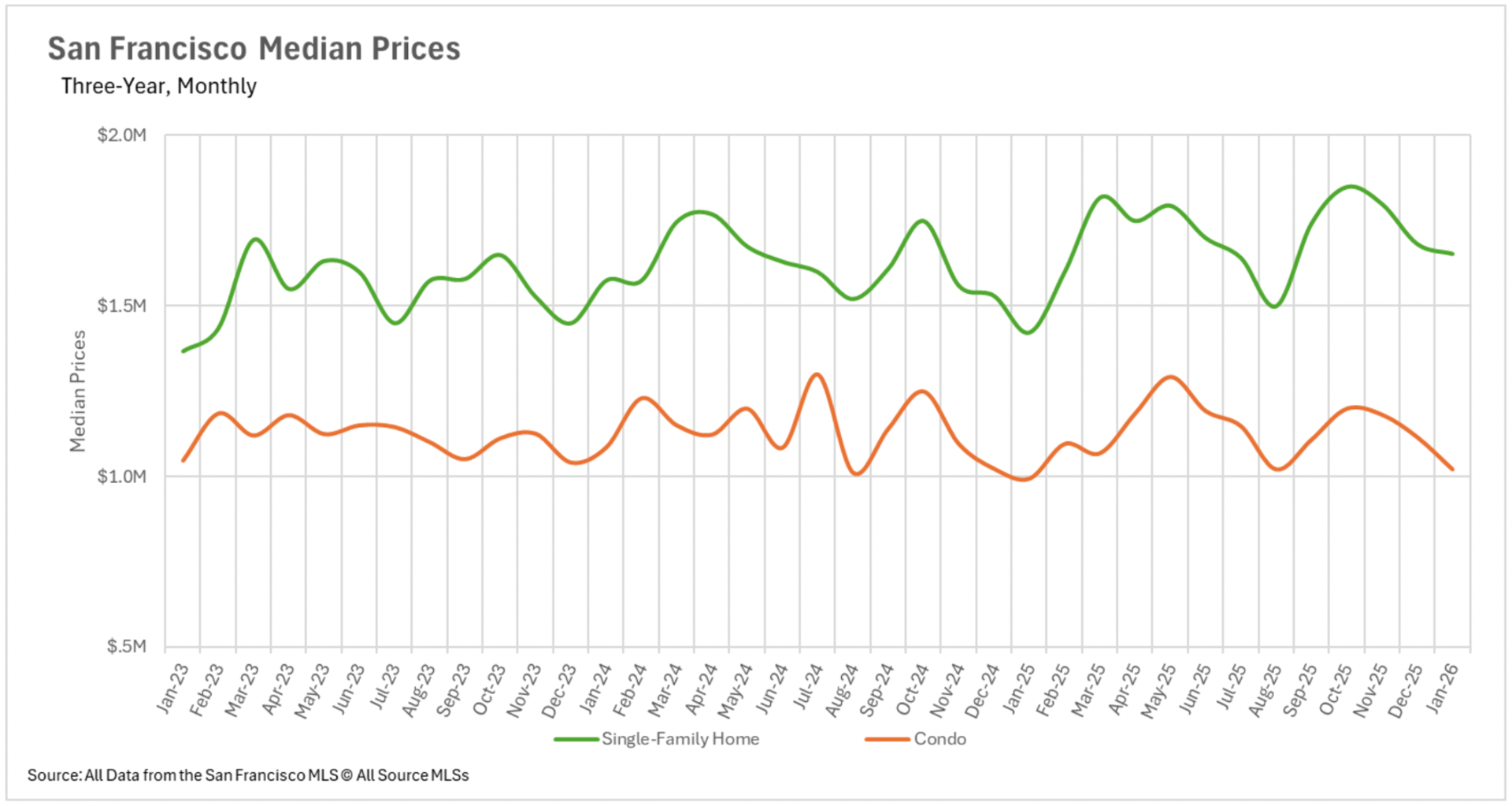

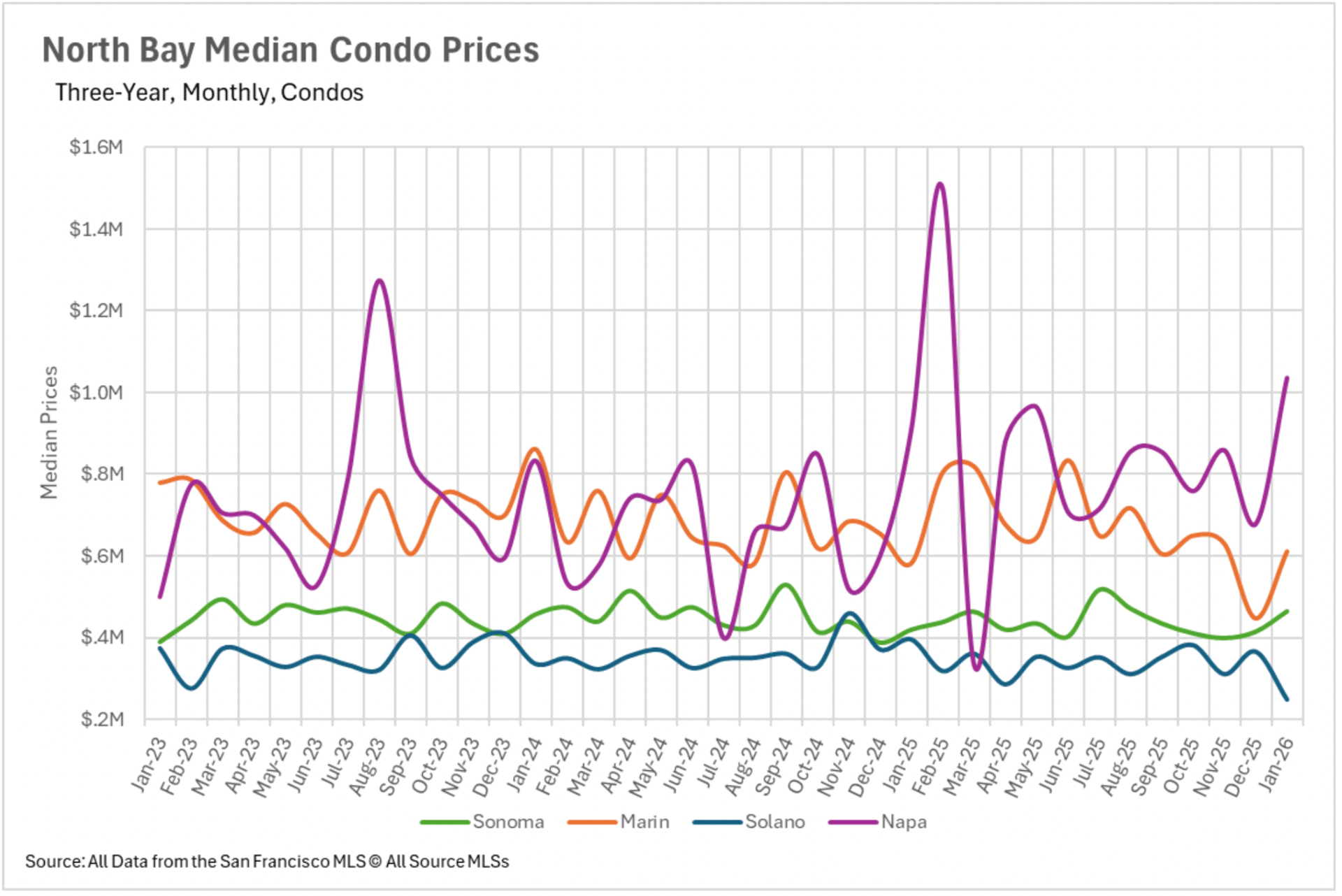

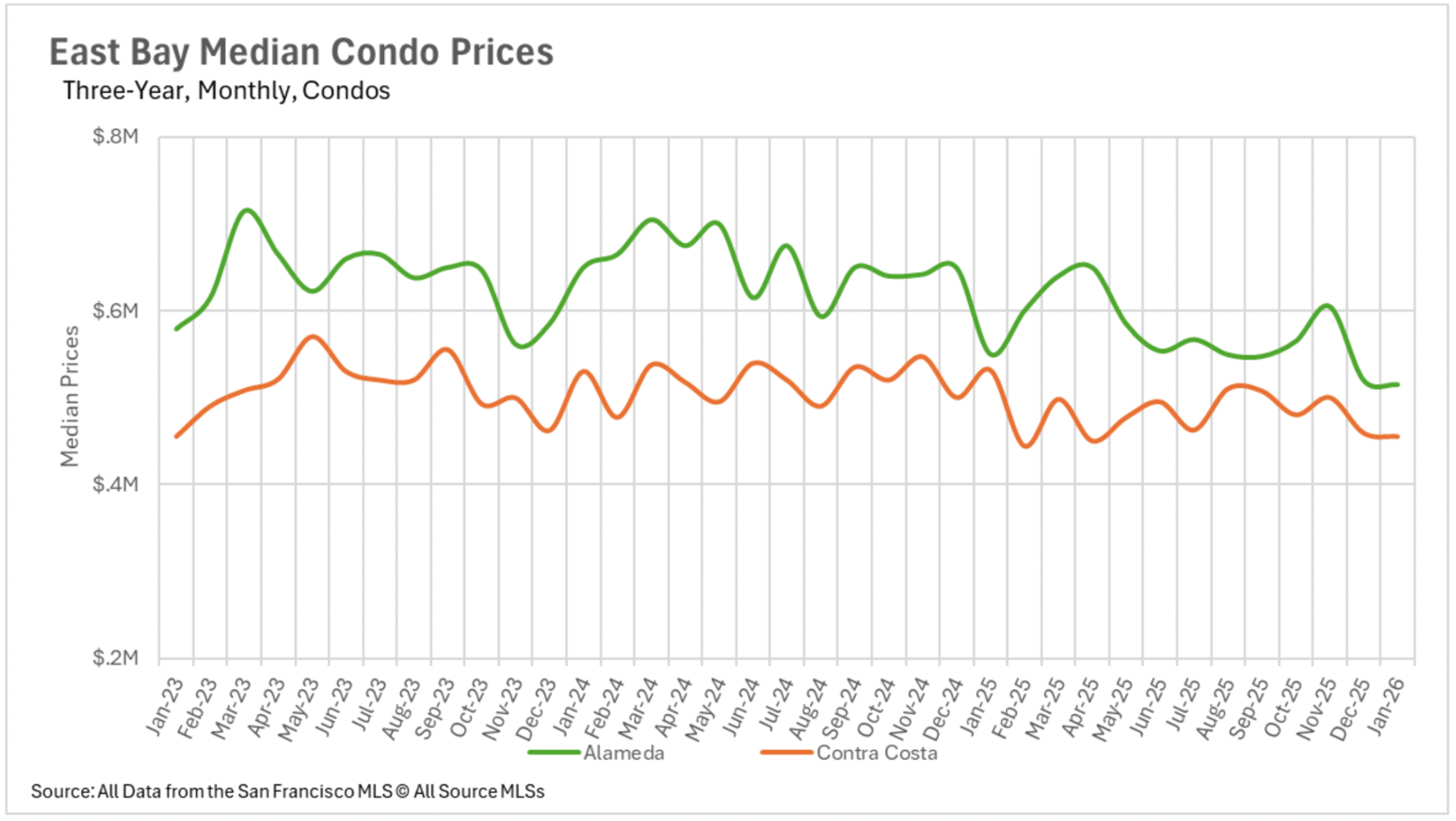

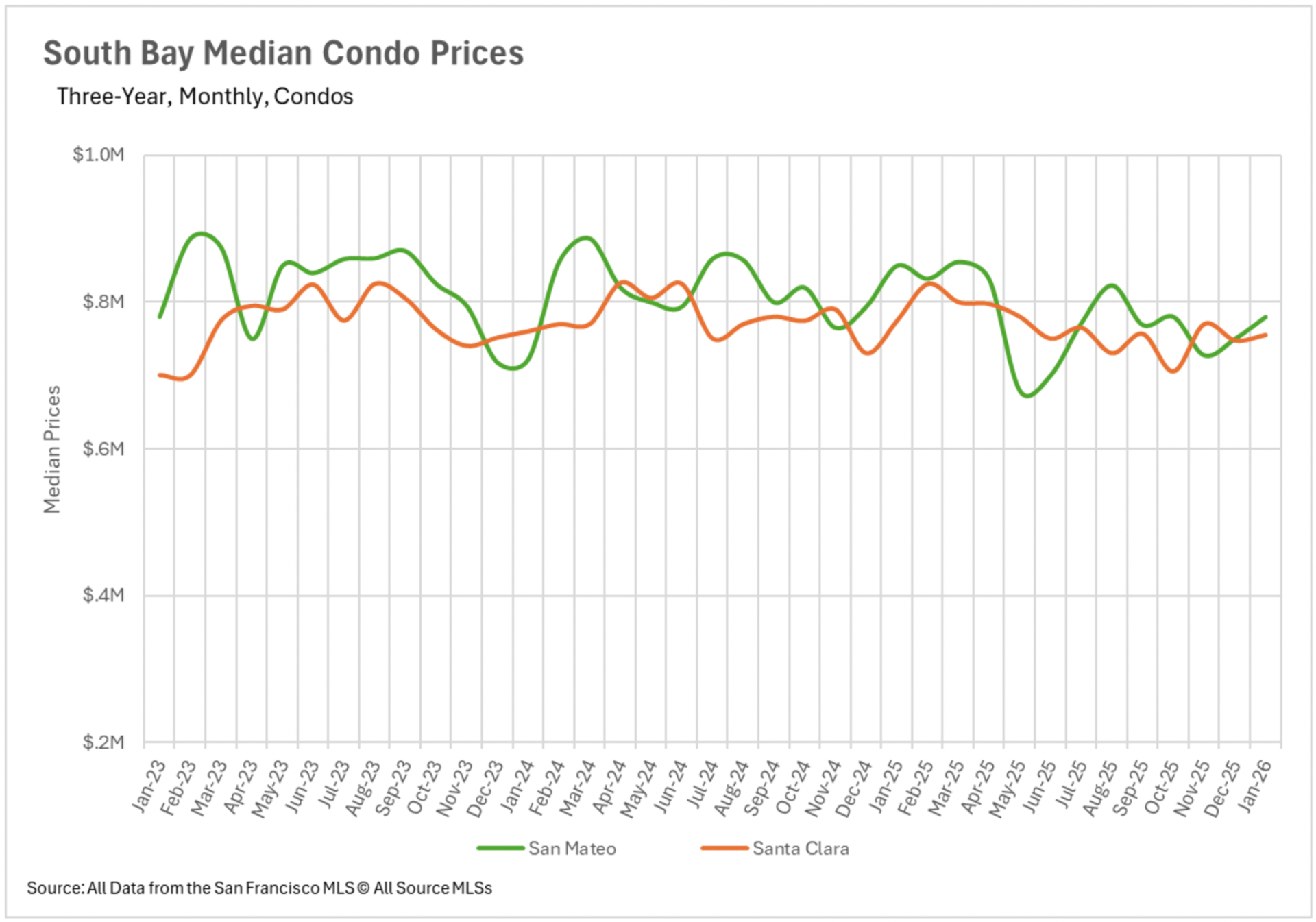

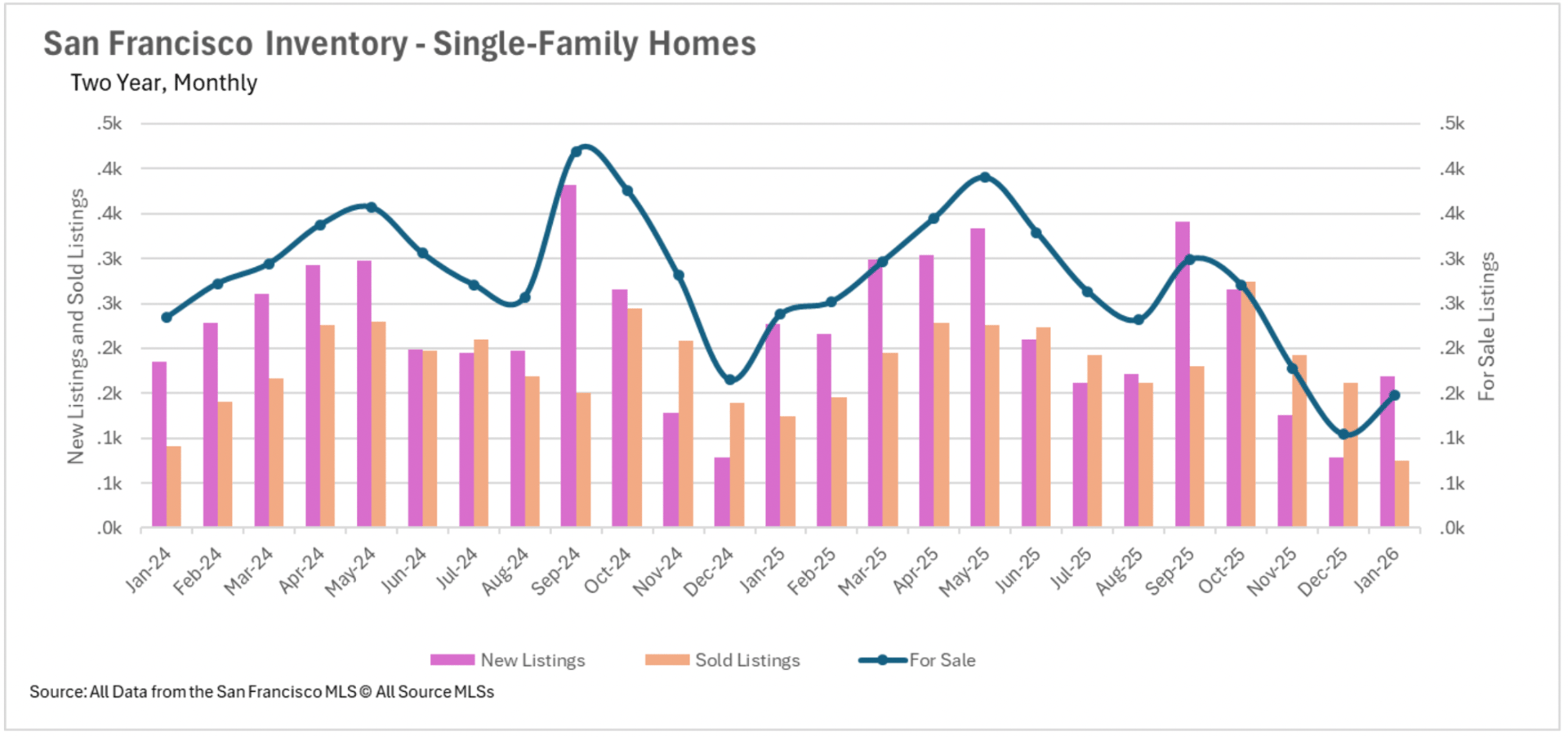

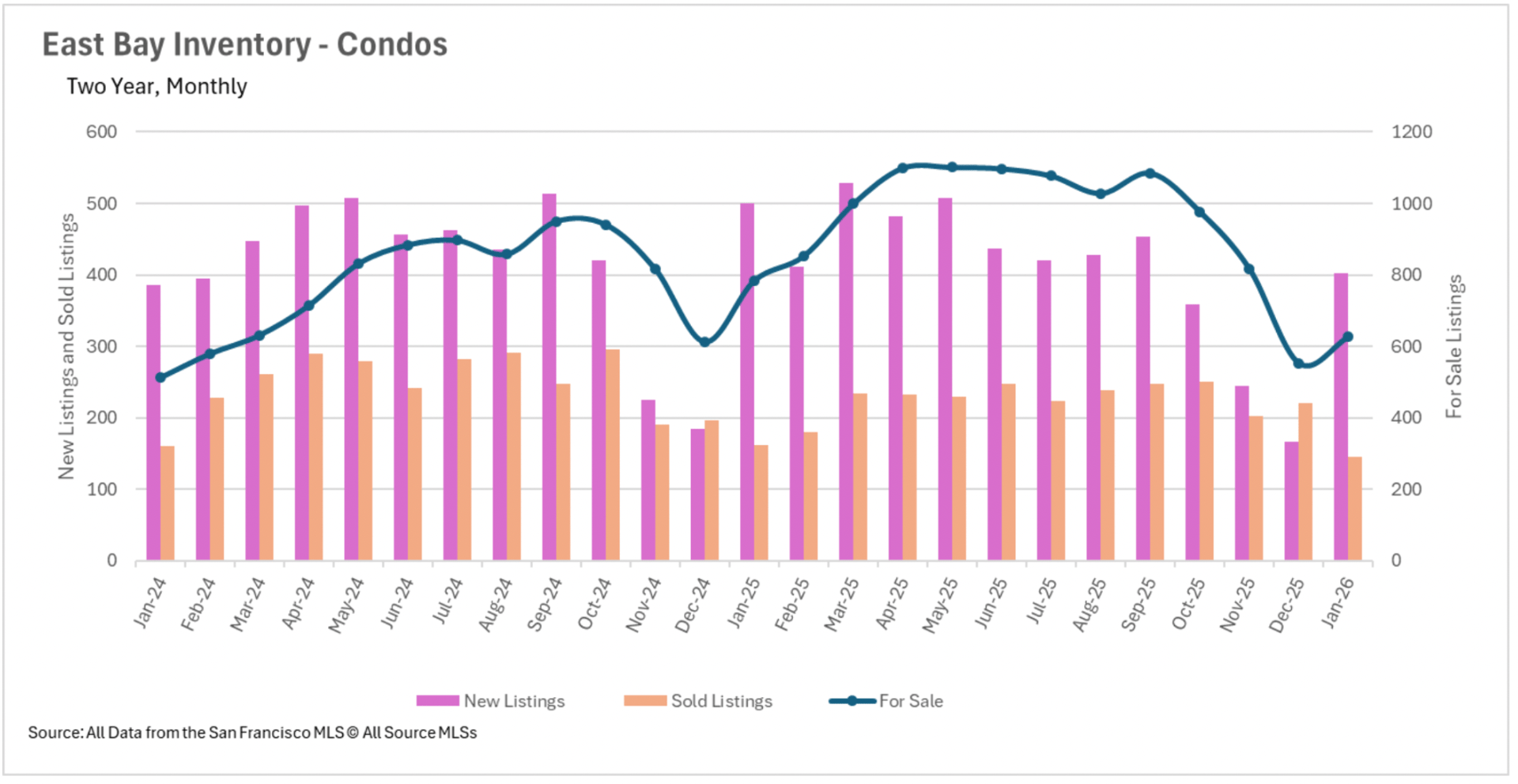

The Bay Area commenced 2026 with particularly striking value appreciation in several primary markets. San Francisco's single-family property sector recorded an impressive 16.23% annual increase in median transaction value, with the median property transacting for $1,653,325. Matching this momentum, Marin County witnessed its median single-family property transact for $1,750,000, a 19.86% annual advance. Napa County also registered substantial gains, with single-family properties advancing 18.75% to a median of $1,045,000. Nevertheless, not every market is recording this magnitude of expansion. Santa Clara County witnessed its median single-family property value decline by 3.89%, while Sonoma and Solano Counties also registered modest annual retreats. The condominium sector continues presenting a substantially different narrative, with retreats throughout Silicon Valley and meaningful weakness in Contra Costa County, where the median condominium transacted for 14.39% less than it did last January. San Francisco condominiums provided a positive development, registering a moderate 2.77% annual gain.

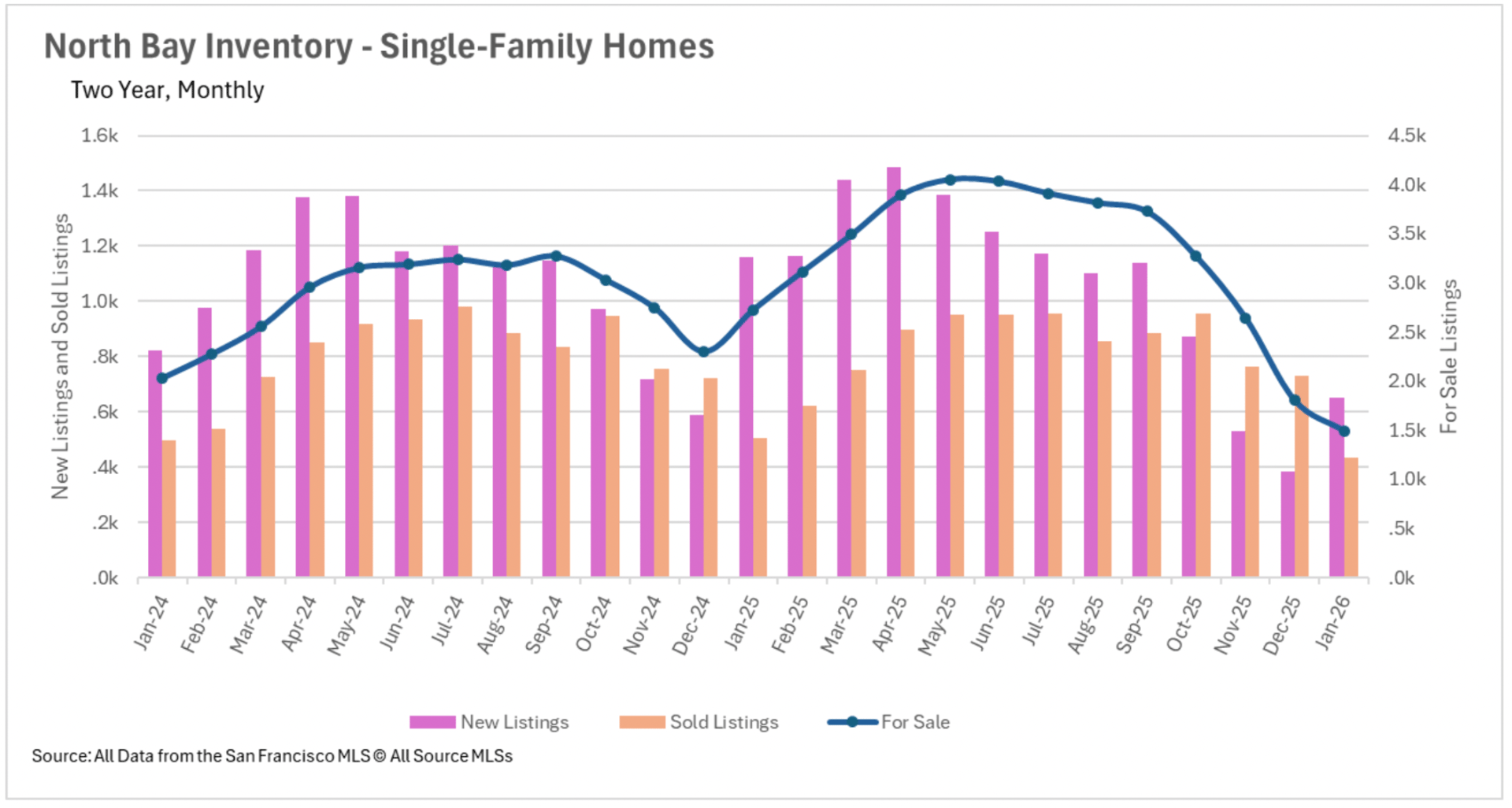

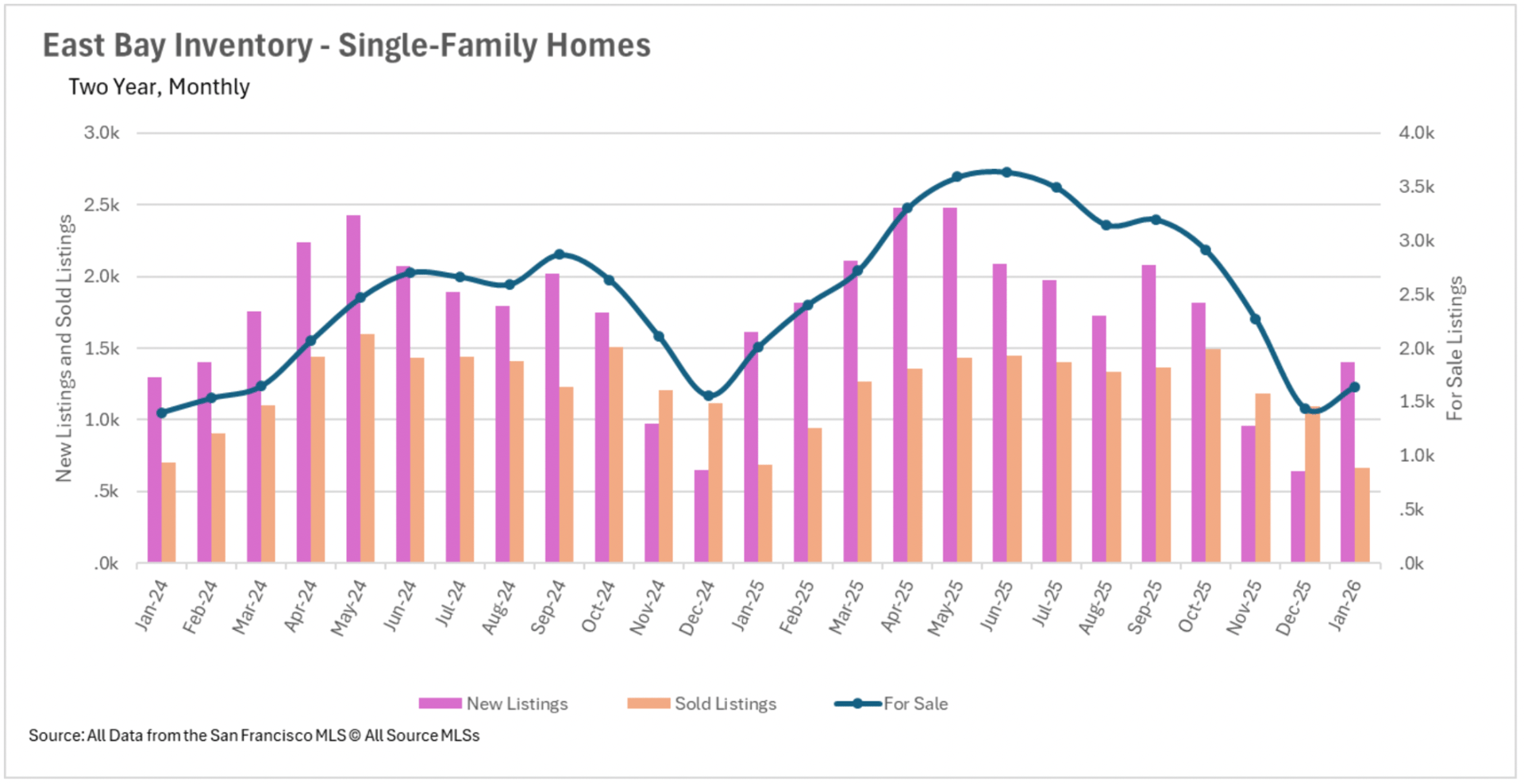

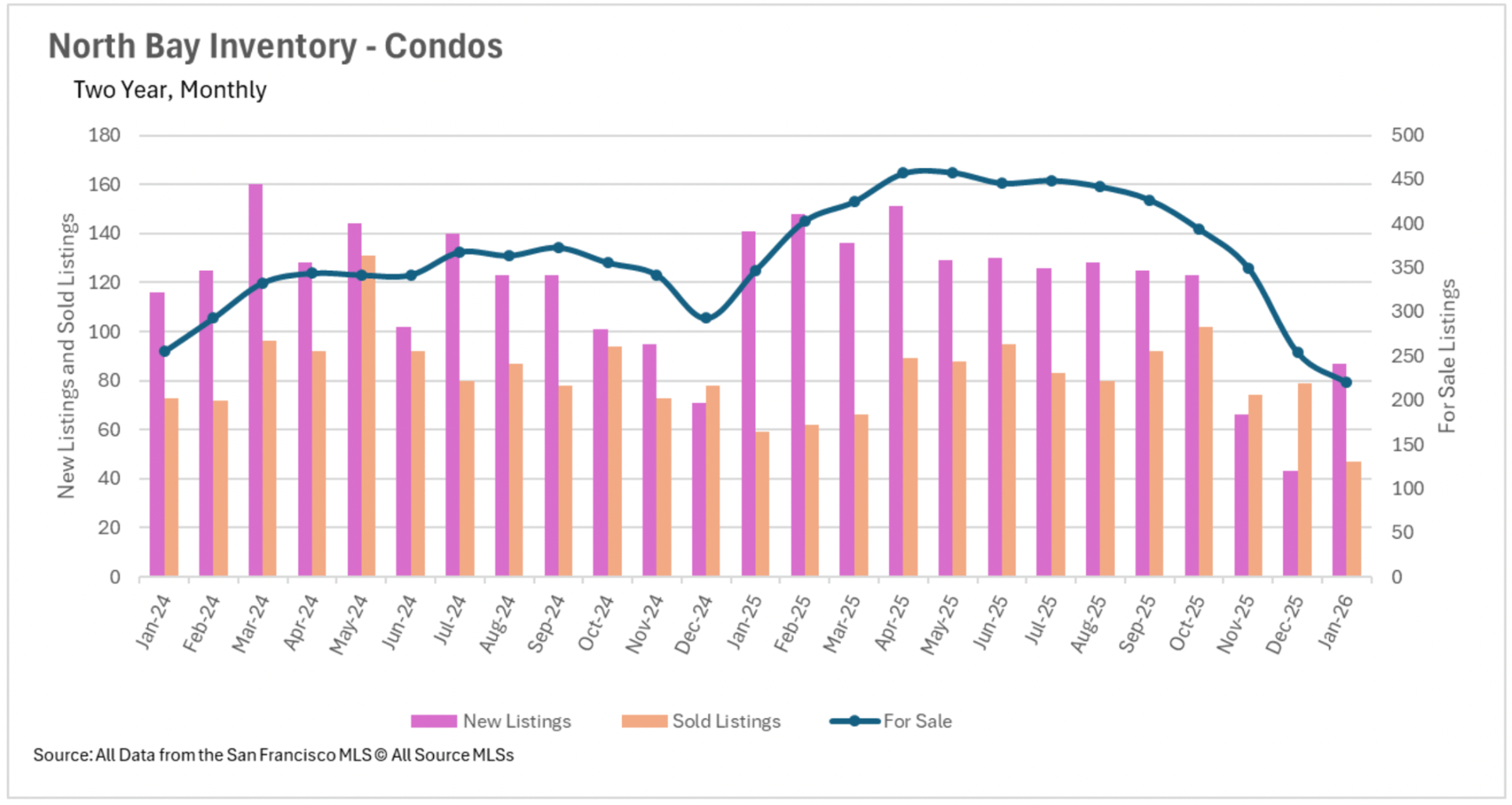

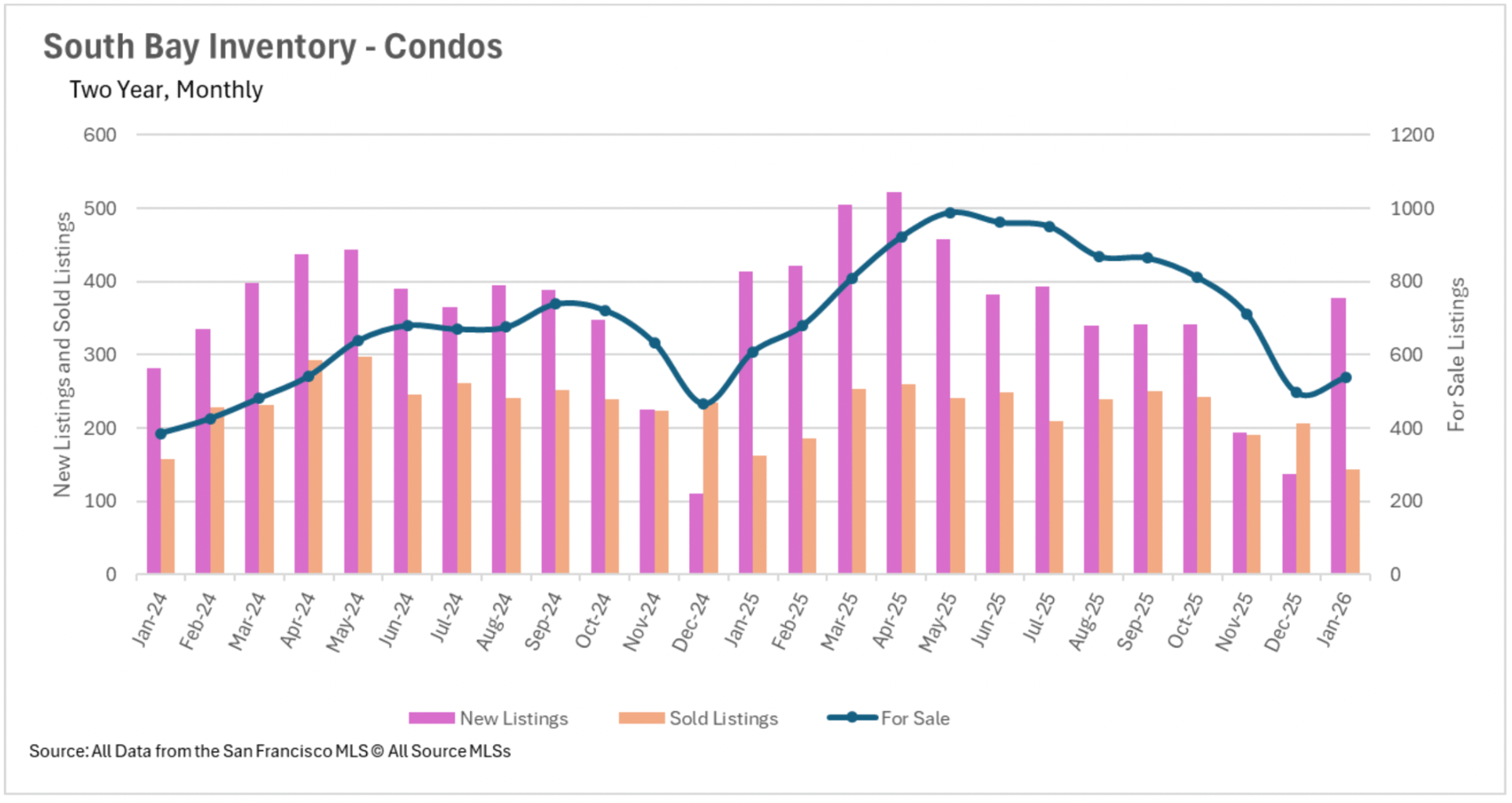

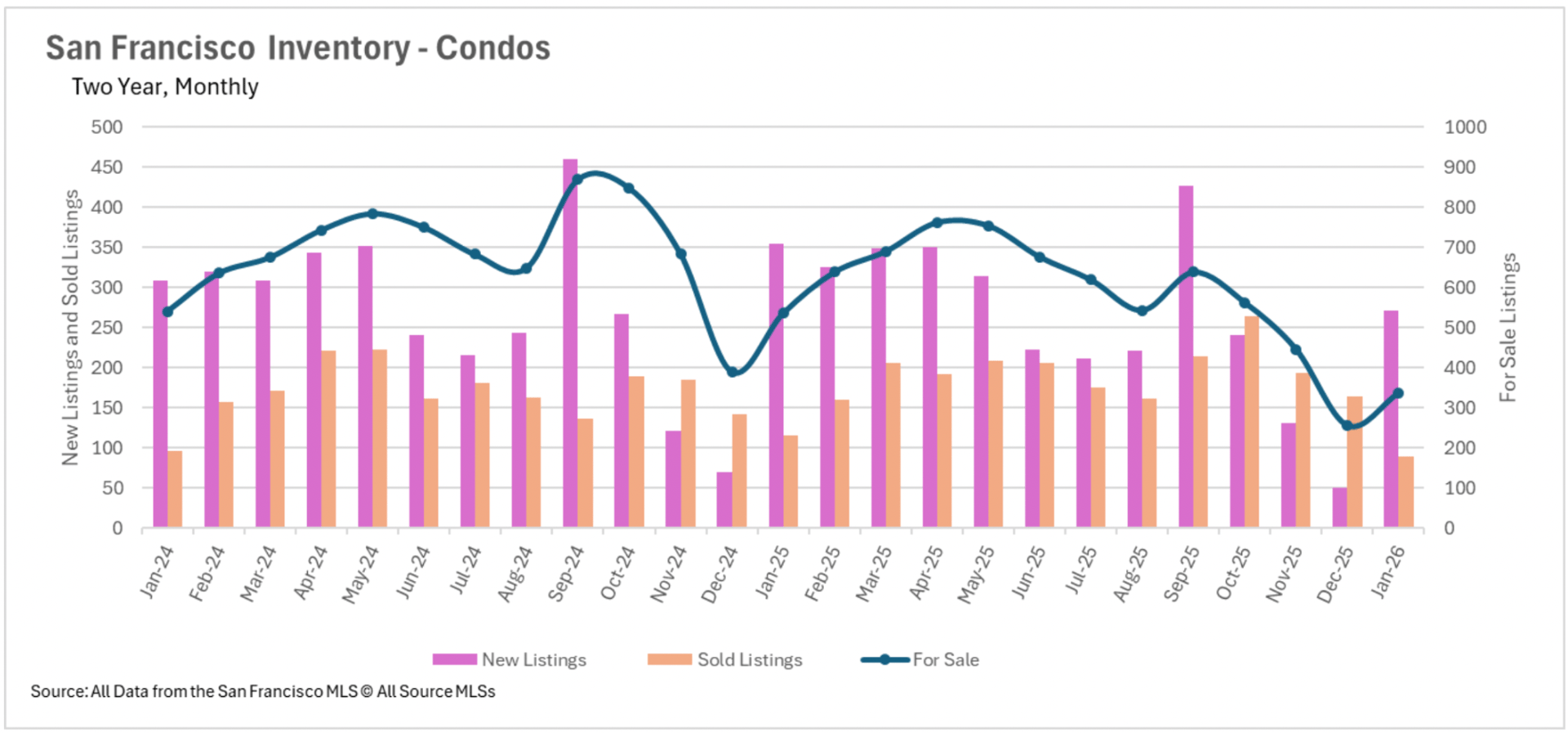

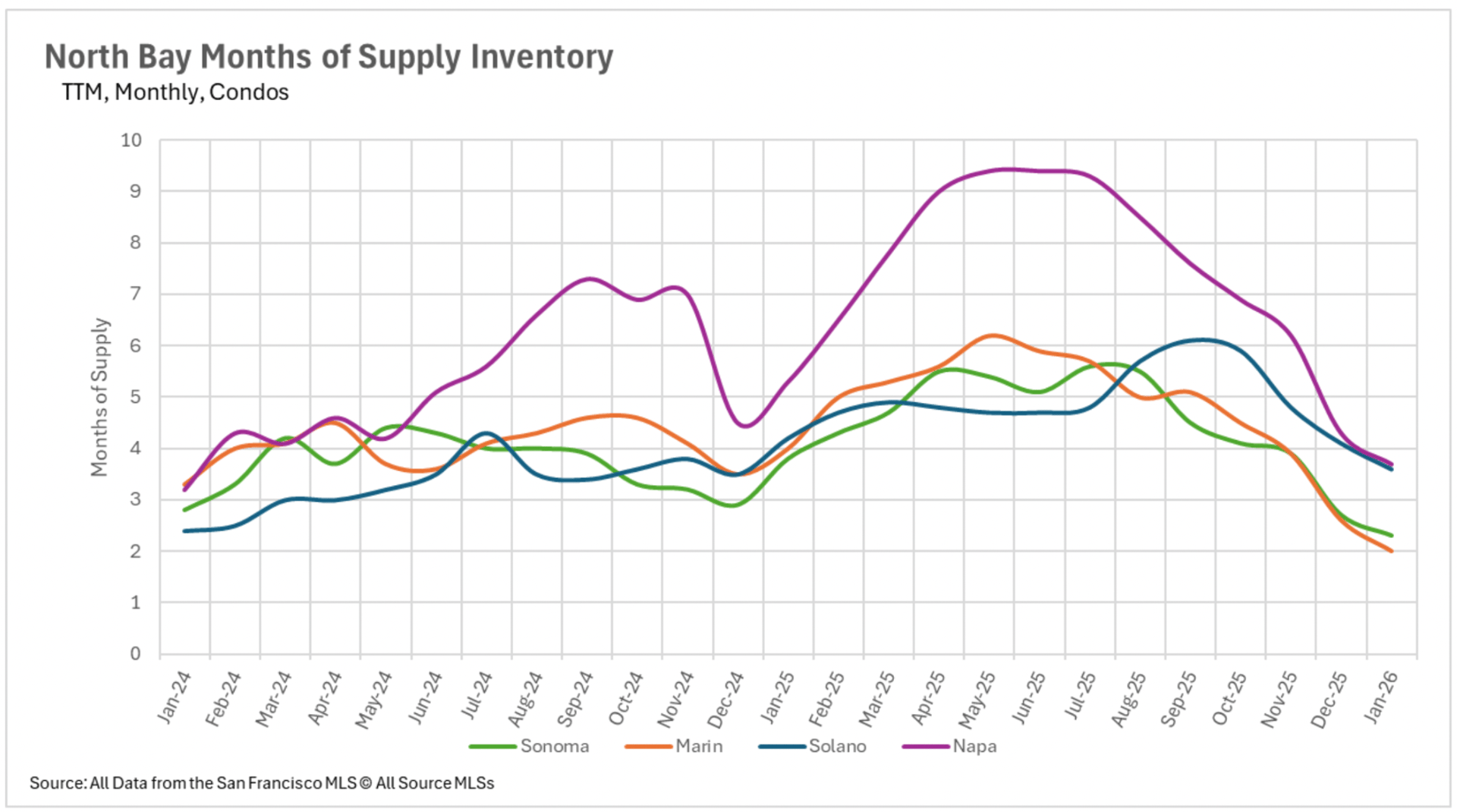

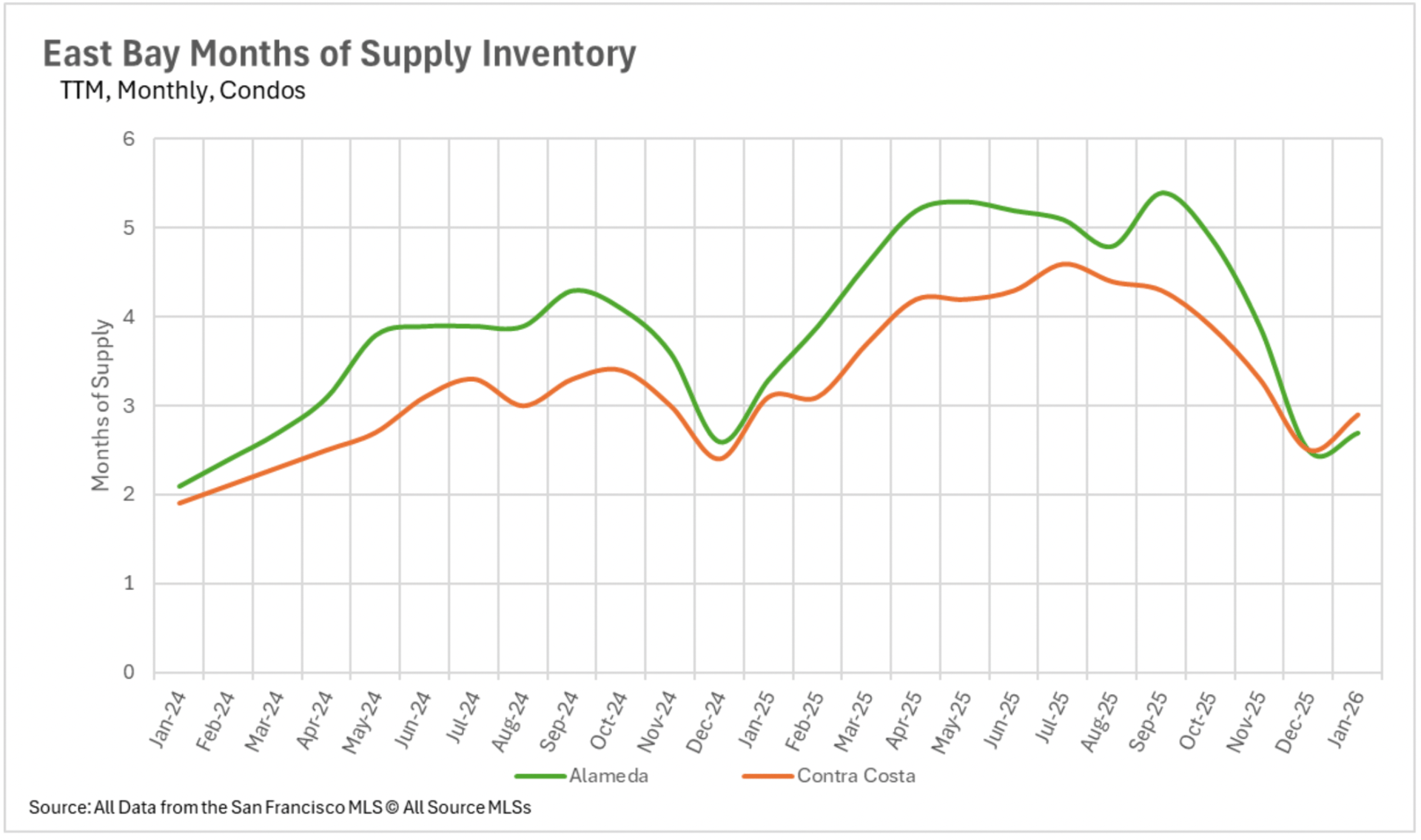

Among the most significant developments heading into 2026 is the substantial reduction in availability across the Bay Area. Following availability accumulations throughout the spring and summer of 2025, the adjustment has been expeditious and pronounced. North Bay regions witnessed the most substantial compression, with single-family property availability plummeting 45.19% on an annual basis and condominium availability declining 36.60%. San Francisco trails closely, with single-family availability declining 37.82% and condominium availability declining 36.94%, producing fewer than 500 properties available for transaction in the entire municipality. East Bay markets witnessed reductions of 18.58% for single-family properties and 20.03% for condominiums, while Silicon Valley's single-family availability declined 12% annually. New listings are commencing recovery following the holiday deceleration, but they remain substantially beneath last year's levels in most markets. Until sellers commence entering the market in greater volumes, buyers will perpetuate facing exceptionally constrained options.

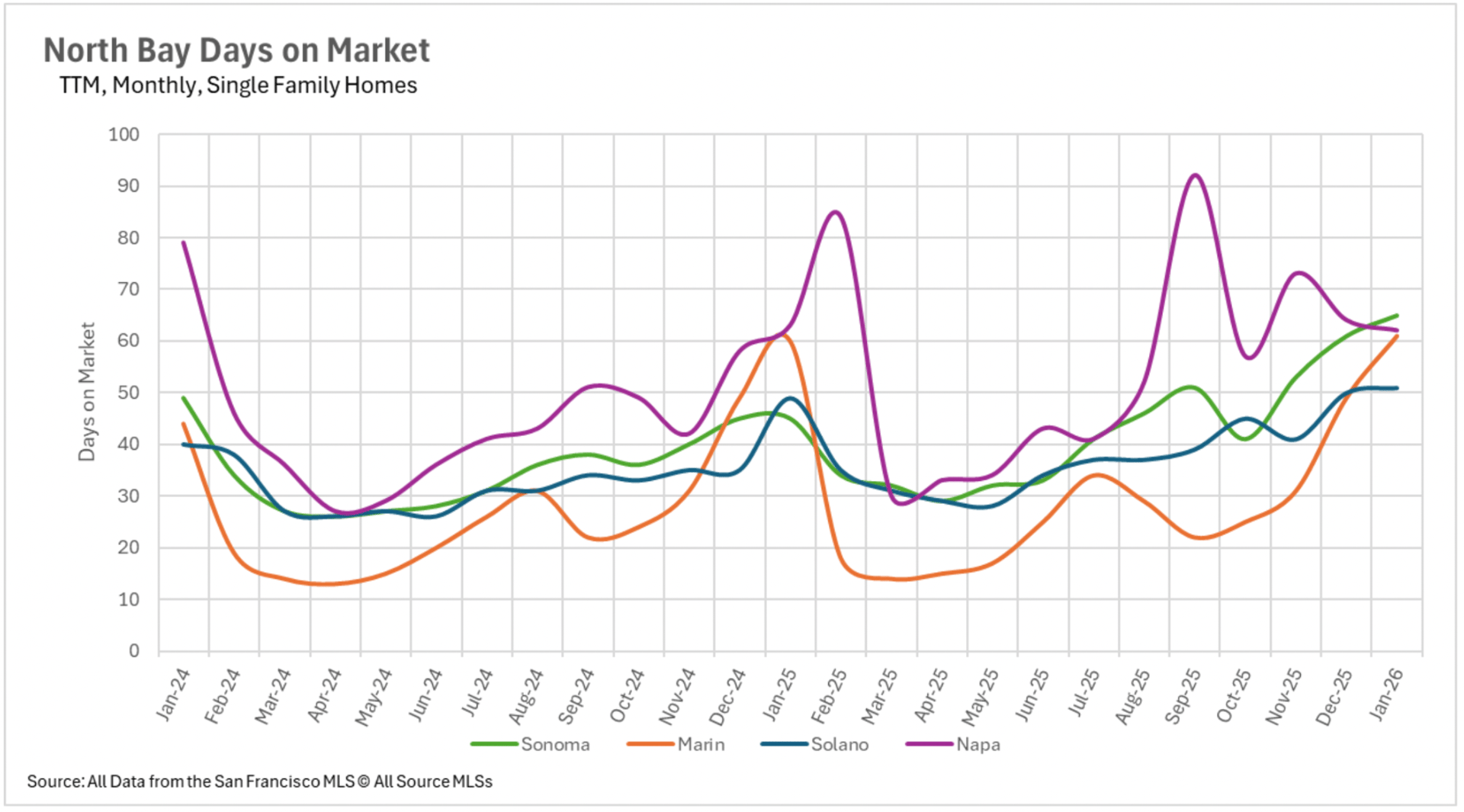

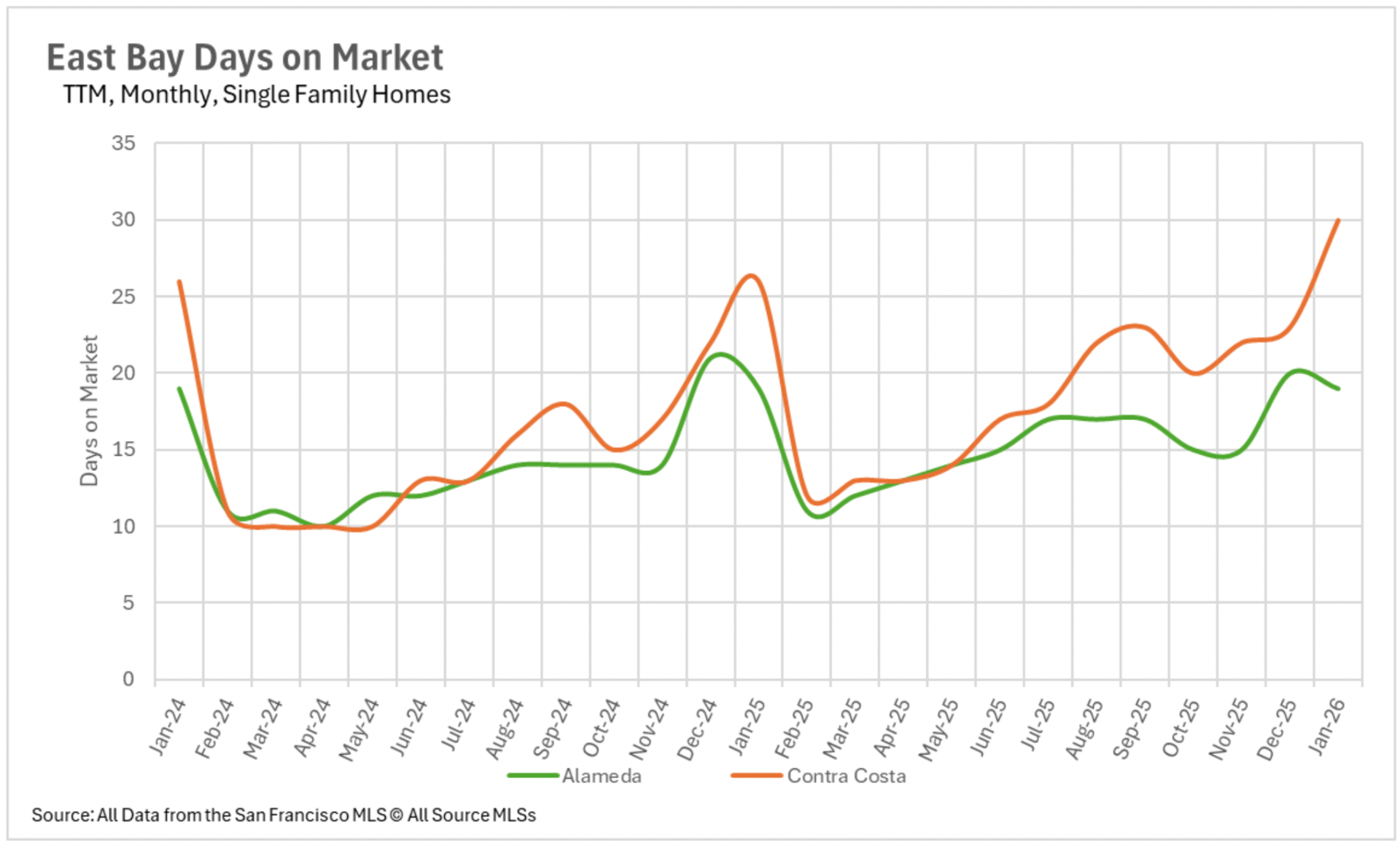

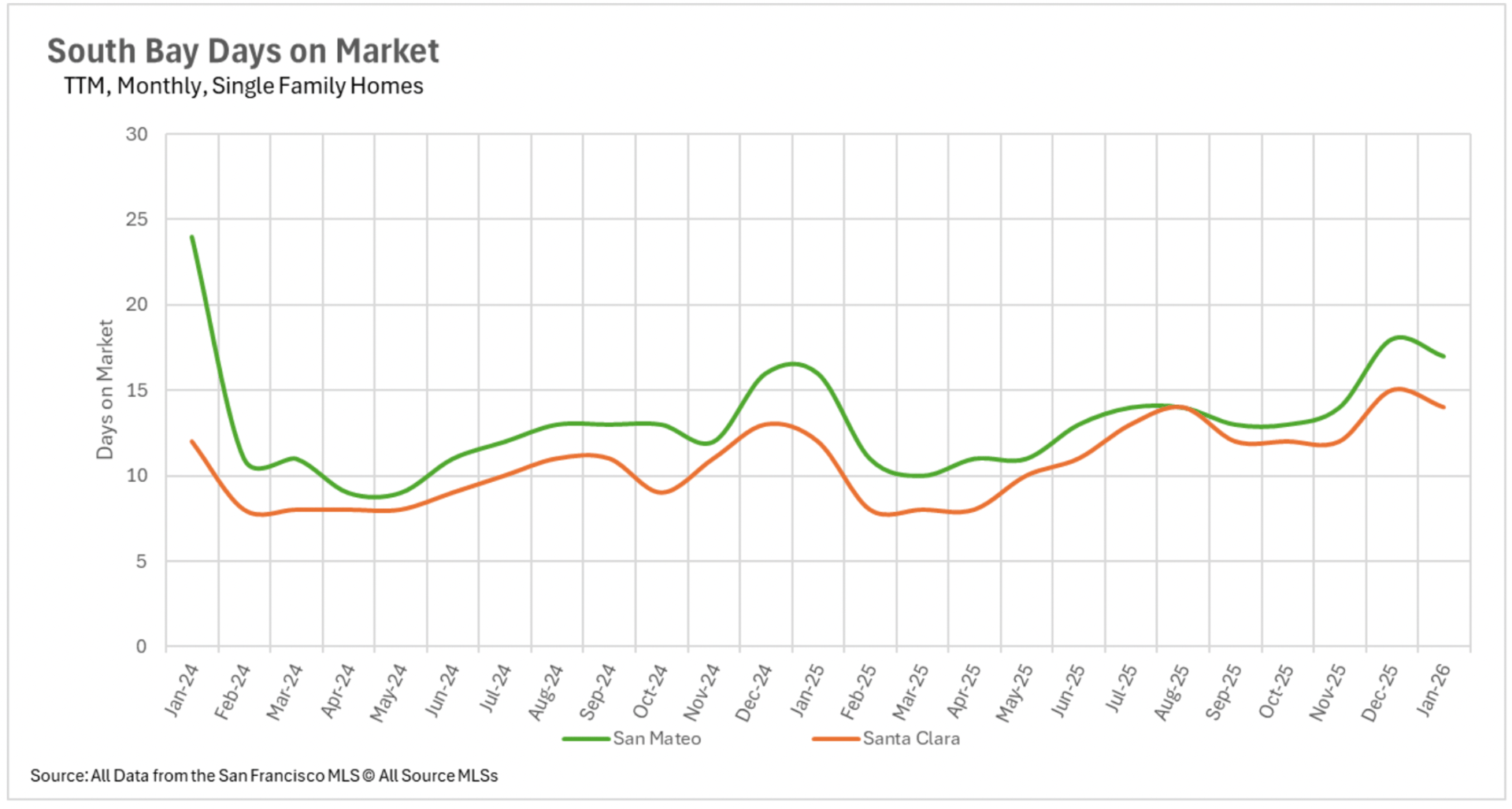

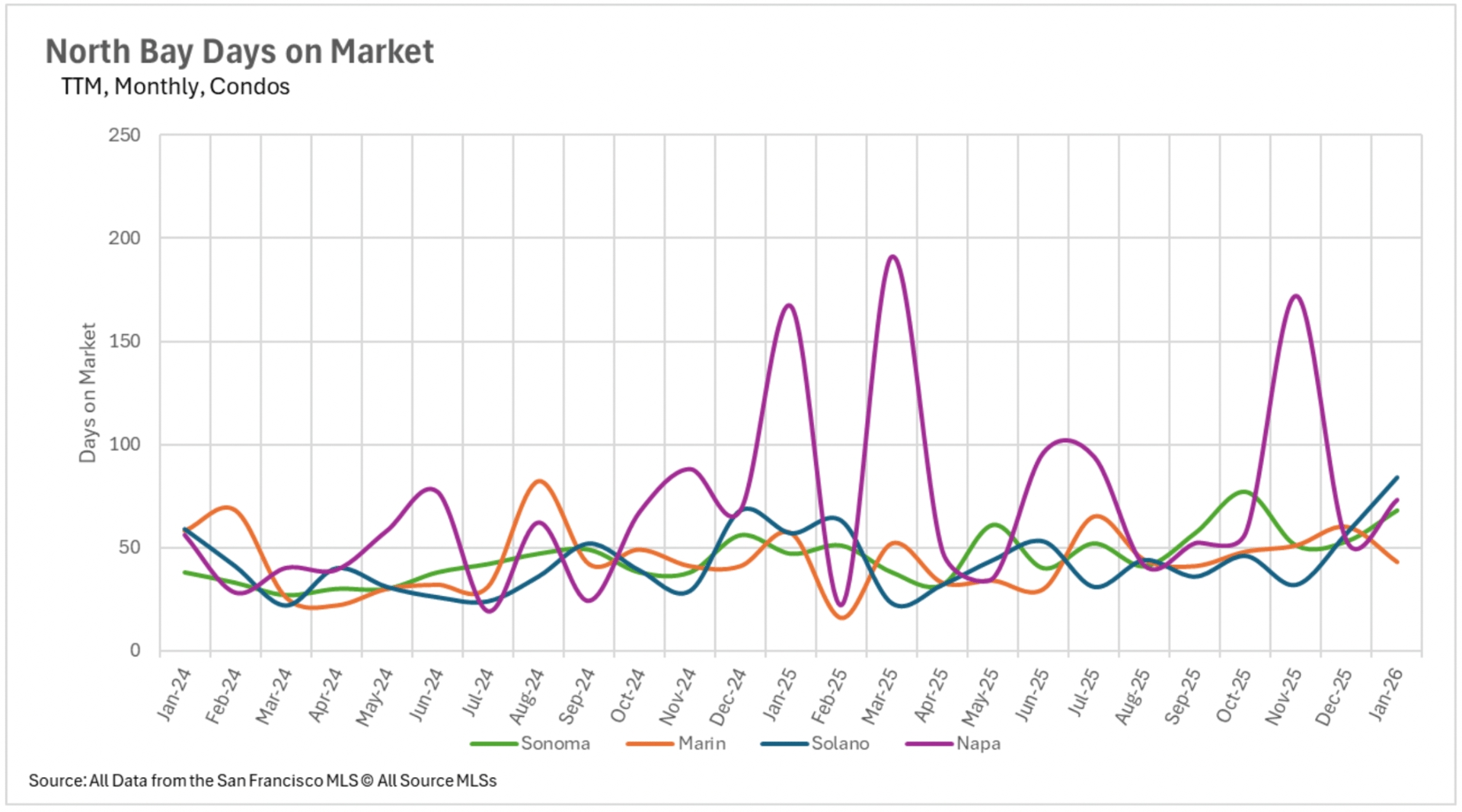

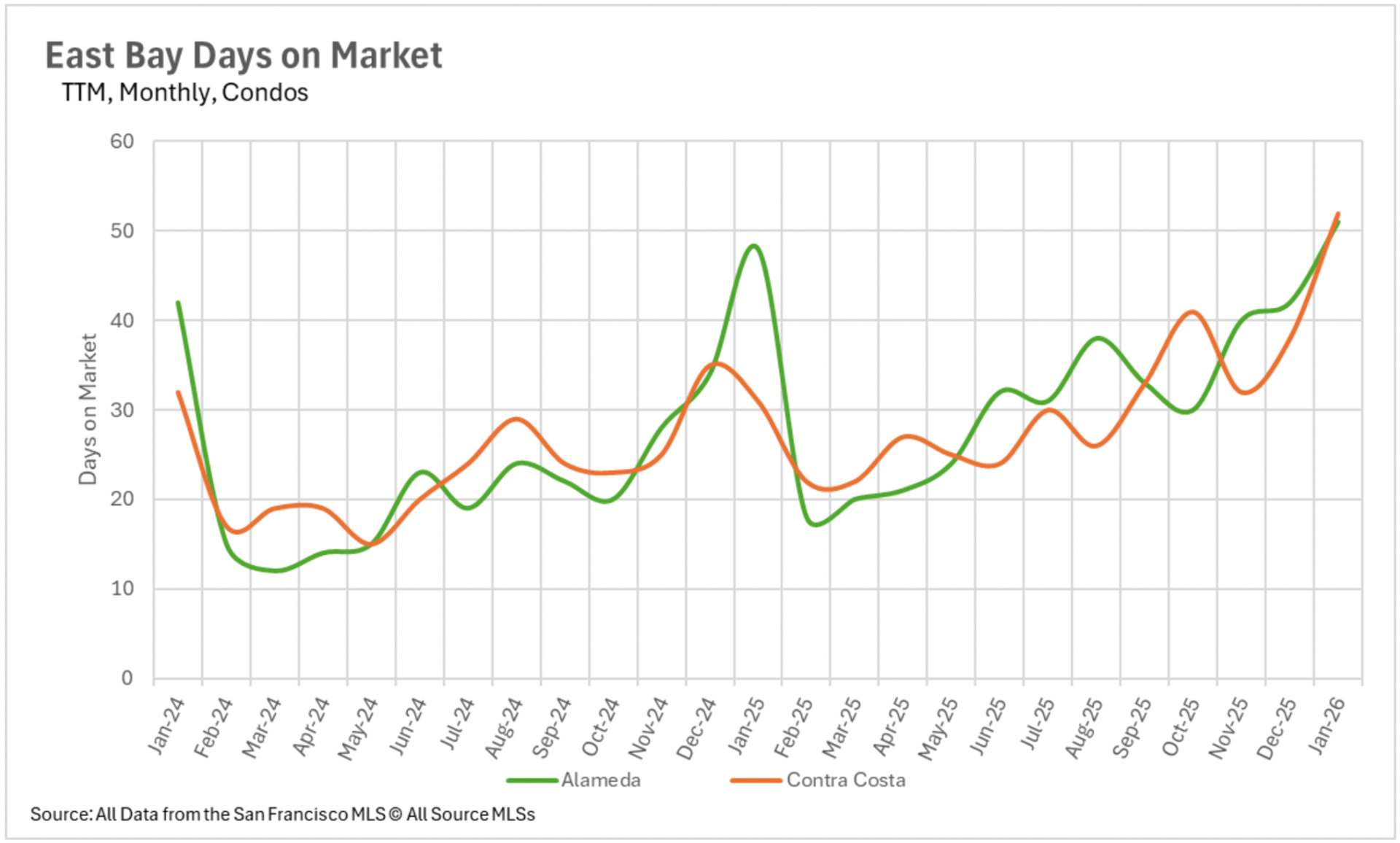

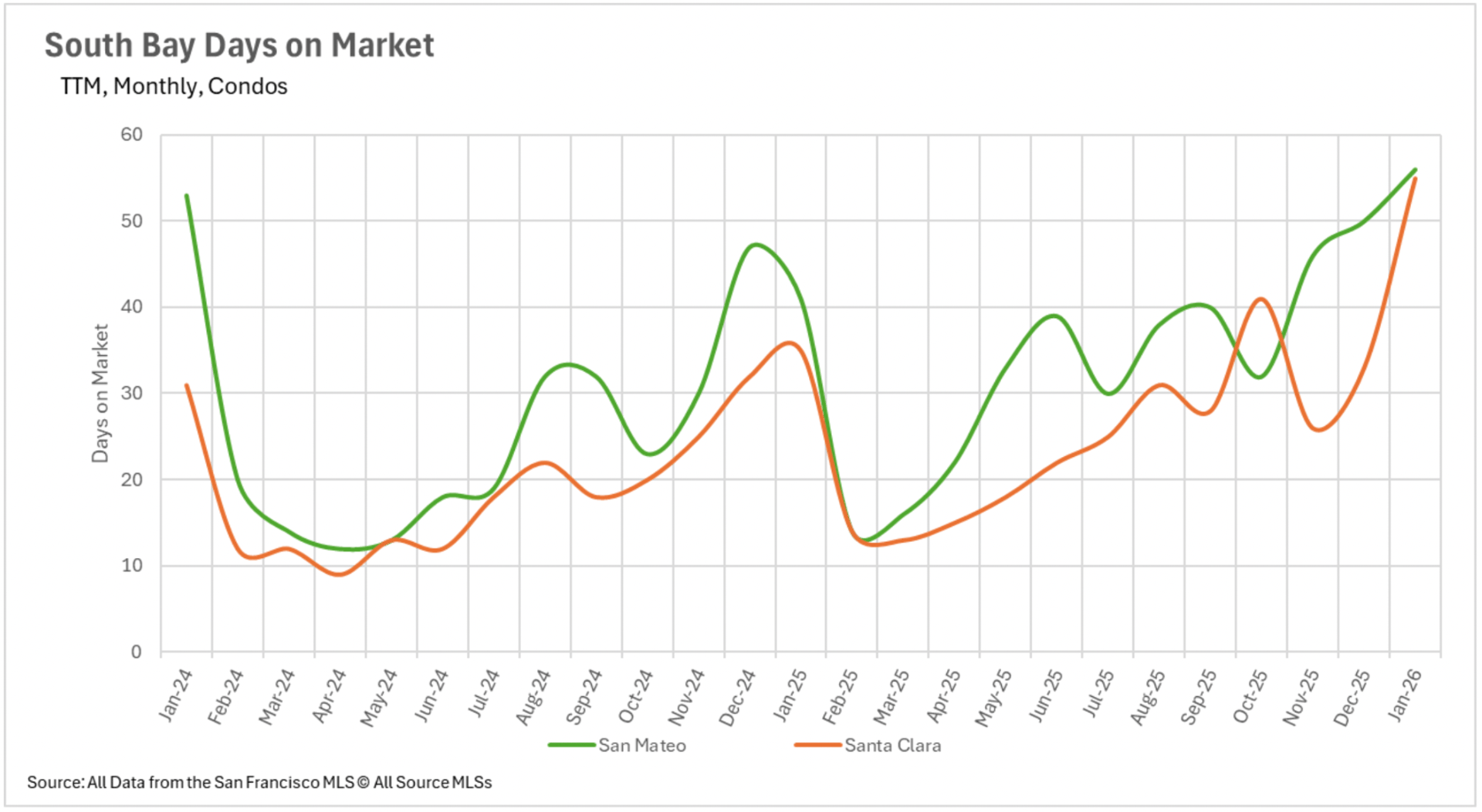

The divergence between the single-family property market and the condominium market continues expanding regarding marketing duration. In San Francisco, the typical single-family property is transacting in merely 13 days, a 56.67% reduction compared to last January. Alameda County single-family properties are also moving at an efficient momentum, transacting in just 19 days on average. Nevertheless, the condominium sector presents a completely different scenario. Santa Clara County condominiums are requiring an average of 55 days on the market, a 57.14% annual increase, while Santa Cruz County condominiums are requiring 67 days, more than double what we documented in January 2025. In North Bay markets, Sonoma County single-family properties are requiring 44.44% additional market duration despite plummeting availability levels, indicating that even in a constrained market, buyers are exercising caution and deliberation with their offers.

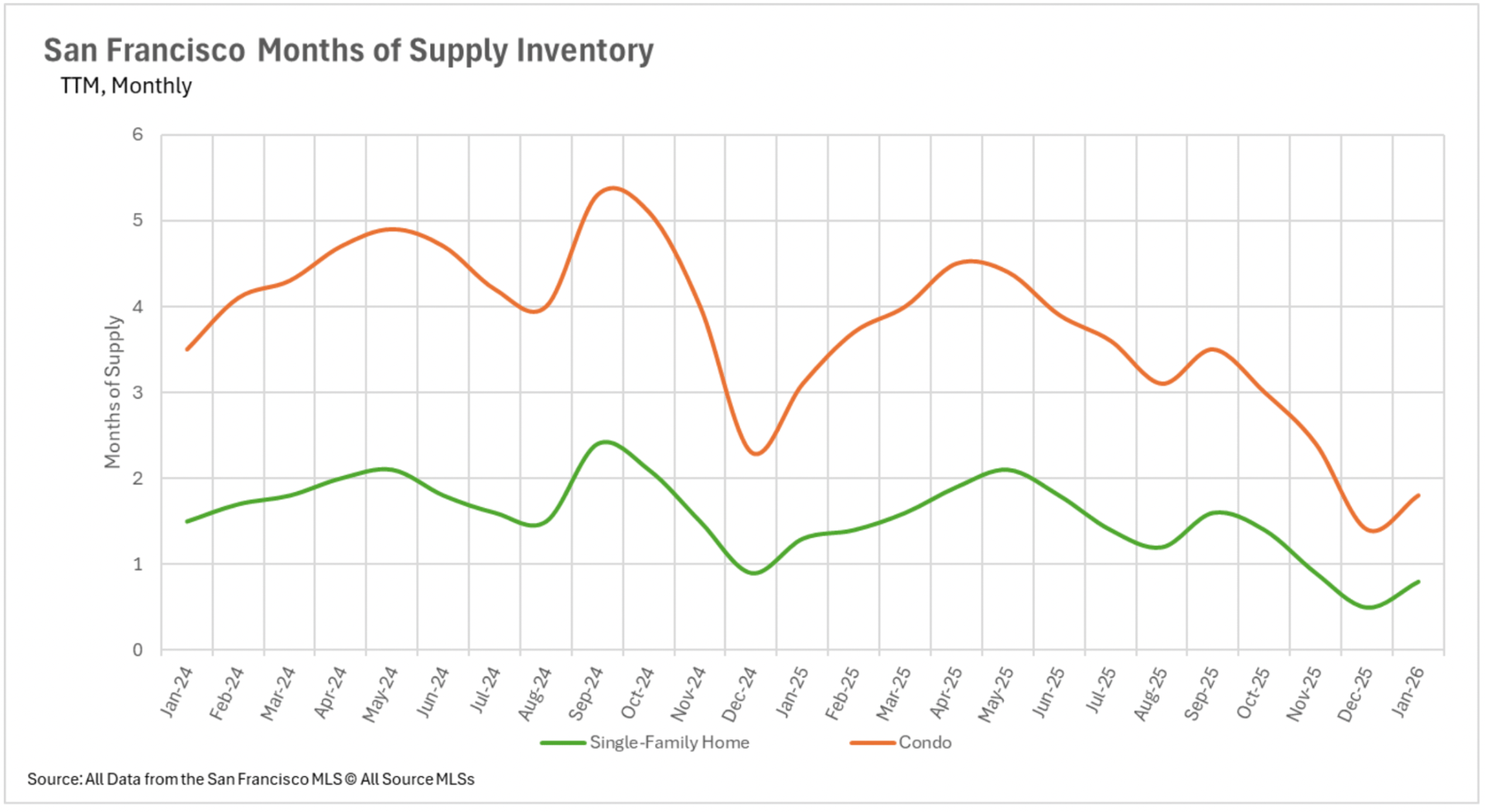

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

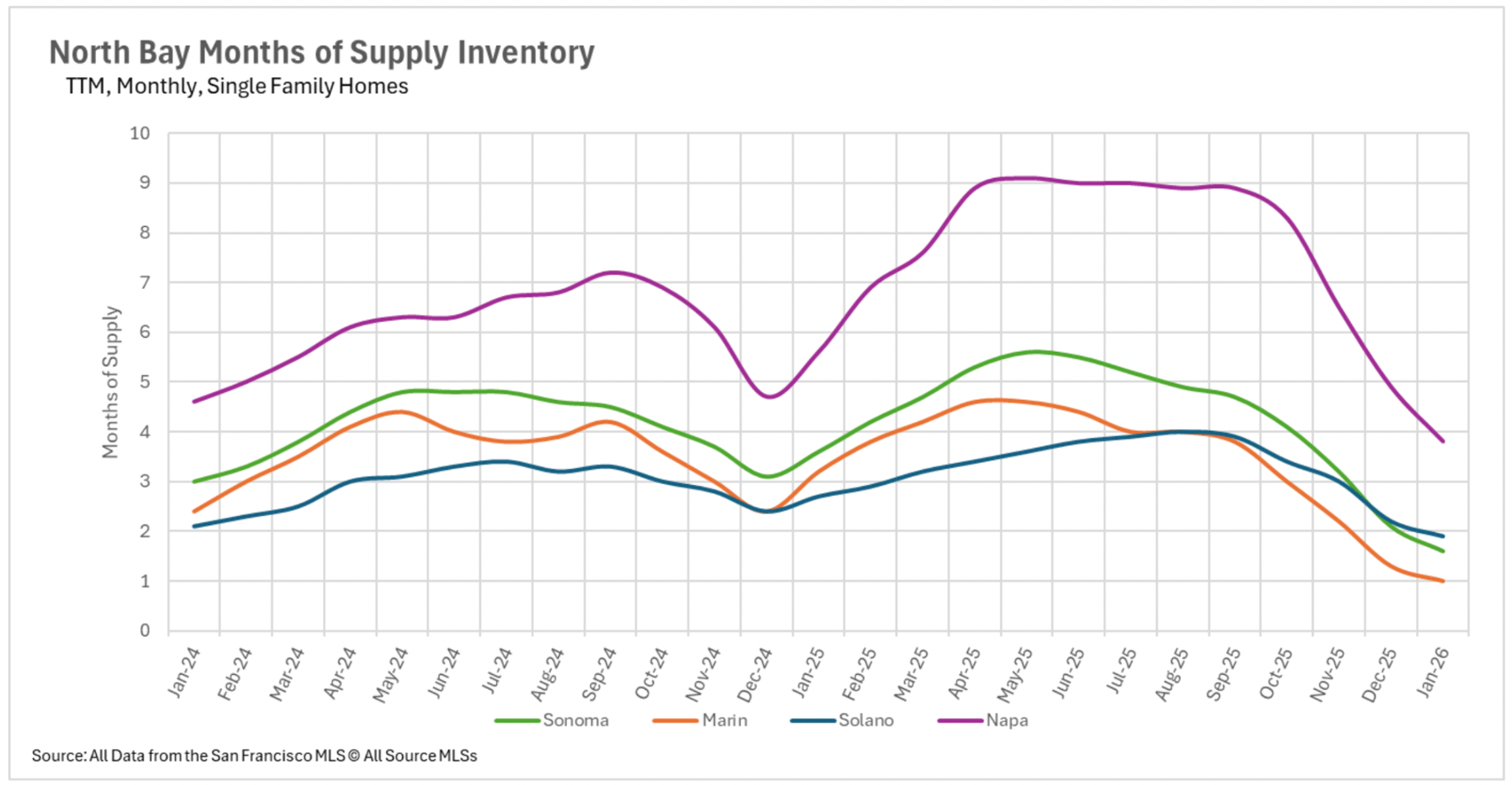

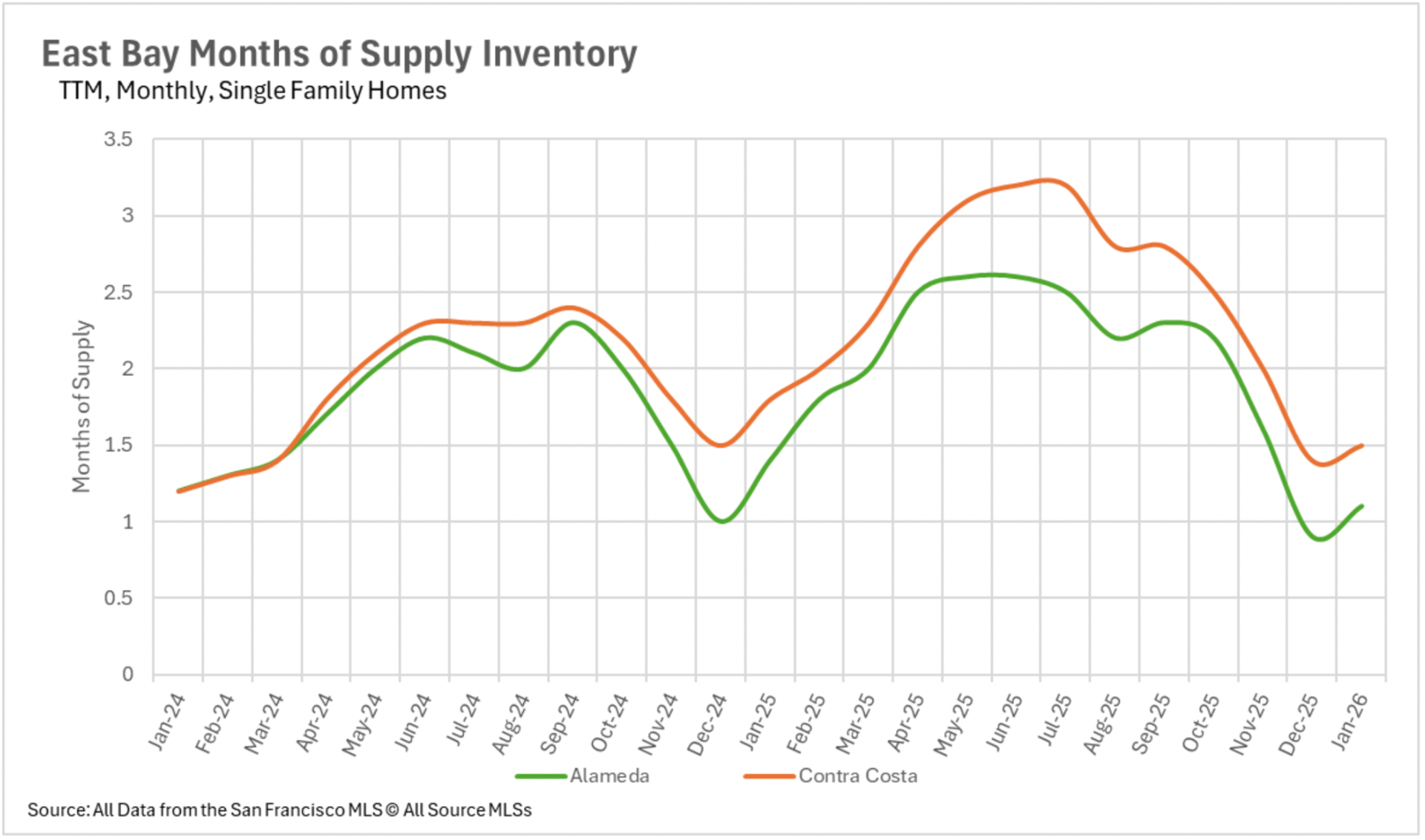

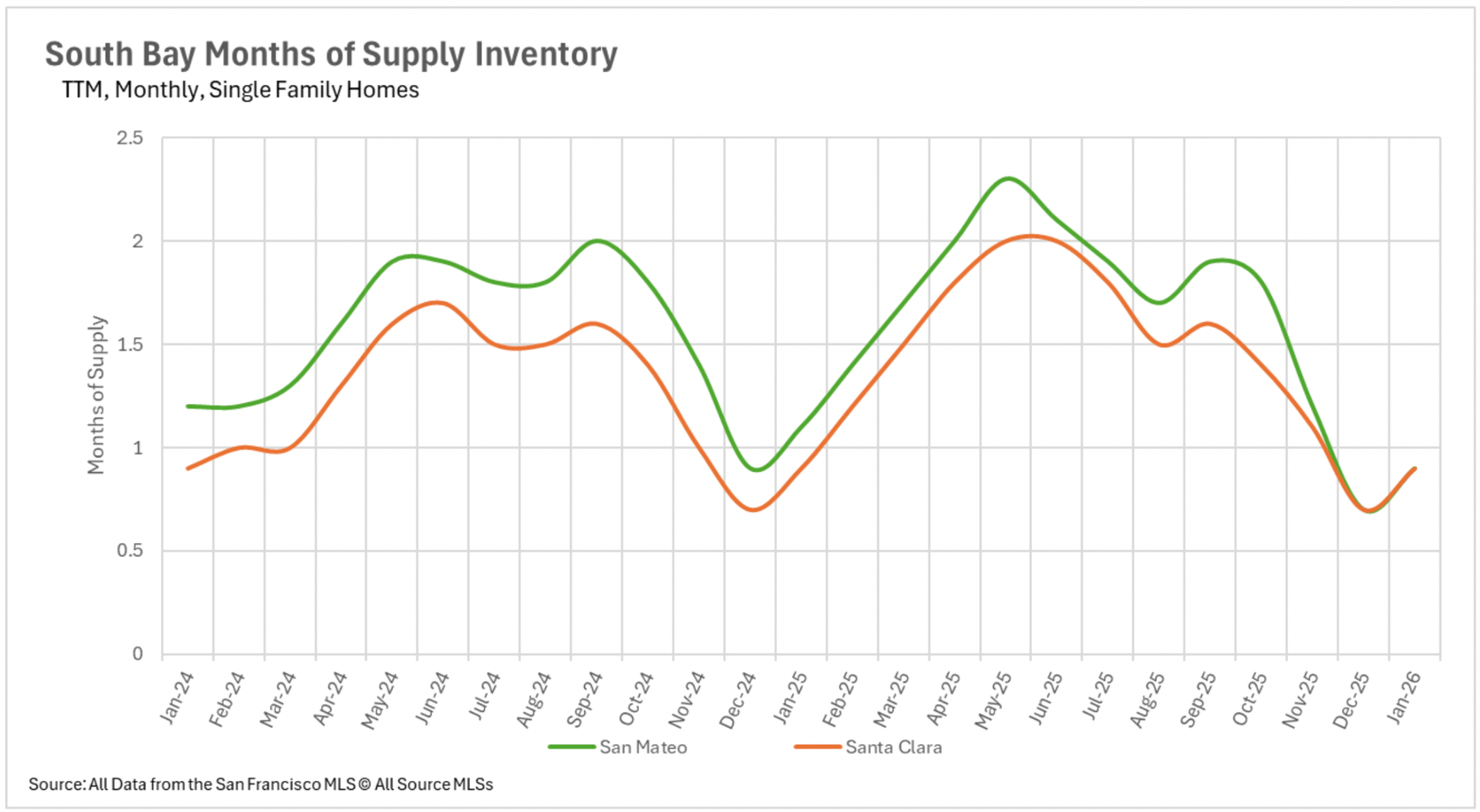

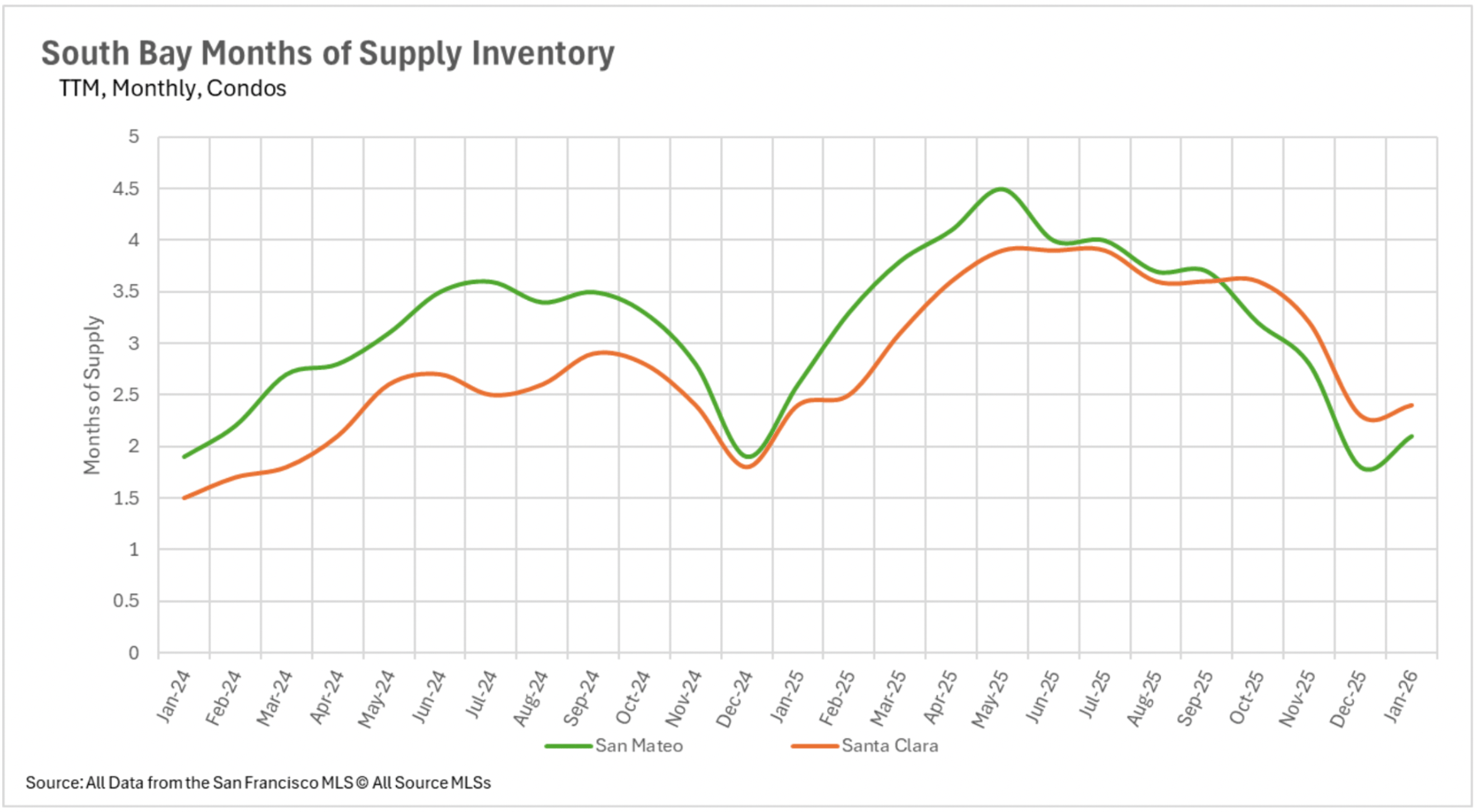

January established seller-favorable market conditions across nearly every segment of the Bay Area's single-family property market. San Francisco and Santa Clara County are registering merely 0.8 and 0.9 months of supply, respectively, while Marin County maintains just 1 month of supply, declining an exceptional 68.75% annually. Alameda County maintains 1.1 months, Contra Costa County maintains 1.5 months, and Sonoma County maintains 1.6 months. Even Napa County, which sustained robust buyer-favorable conditions throughout substantial portions of 2025, has contracted to 3.8 months. The condominium sector has also compressed considerably, though several pockets maintain buyer-favorable territory, including Santa Cruz County at 3.3 months, Solano County at 3.6 months, and Napa County at 3.7 months. With availability at historically minimal levels and the active spring transaction season approaching, sellers maintain an excellent position heading into the forthcoming months.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

April 18, 2026

April 17, 2026

April 11, 2026

March 21, 2026

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

December 4, 2025

You've got questions and we can't wait to answer them.