May Market Update

April data reveals contrasting patterns across Bay Area property markets, with price trajectories varying significantly by location

Supply metrics show pronounced geographic disparity, with East Bay experiencing substantial growth (~43%) while San Francisco continues to face persistent inventory shortages

Detached residential properties remain predominantly in seller-favorable territory throughout most Bay Area submarkets, while condominium segments generally present more advantageous conditions for buyers

Despite regional inventory fluctuations, properties continue to transact efficiently throughout the Bay Area, with Silicon Valley maintaining exceptional velocity (8-15 days)

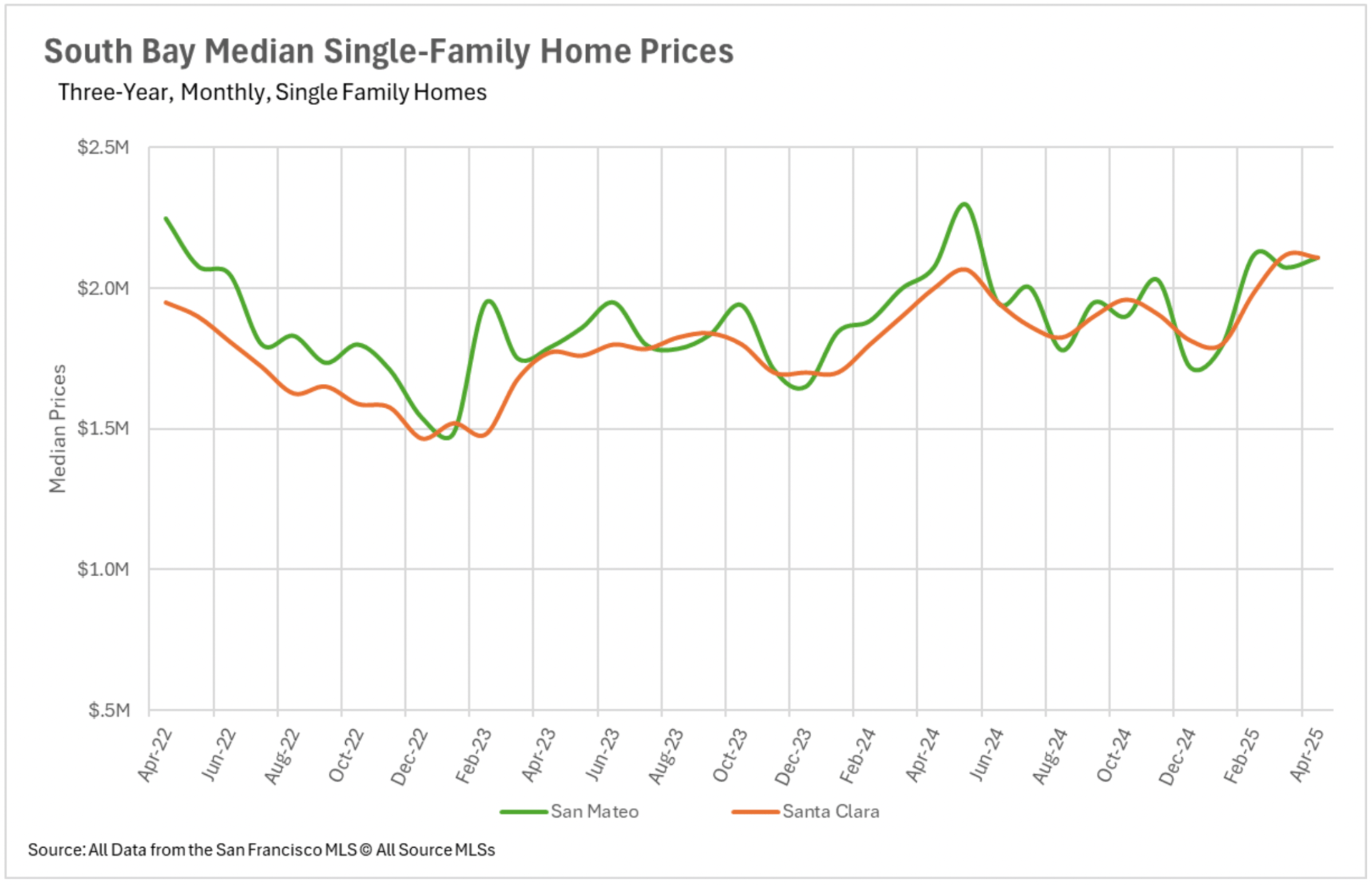

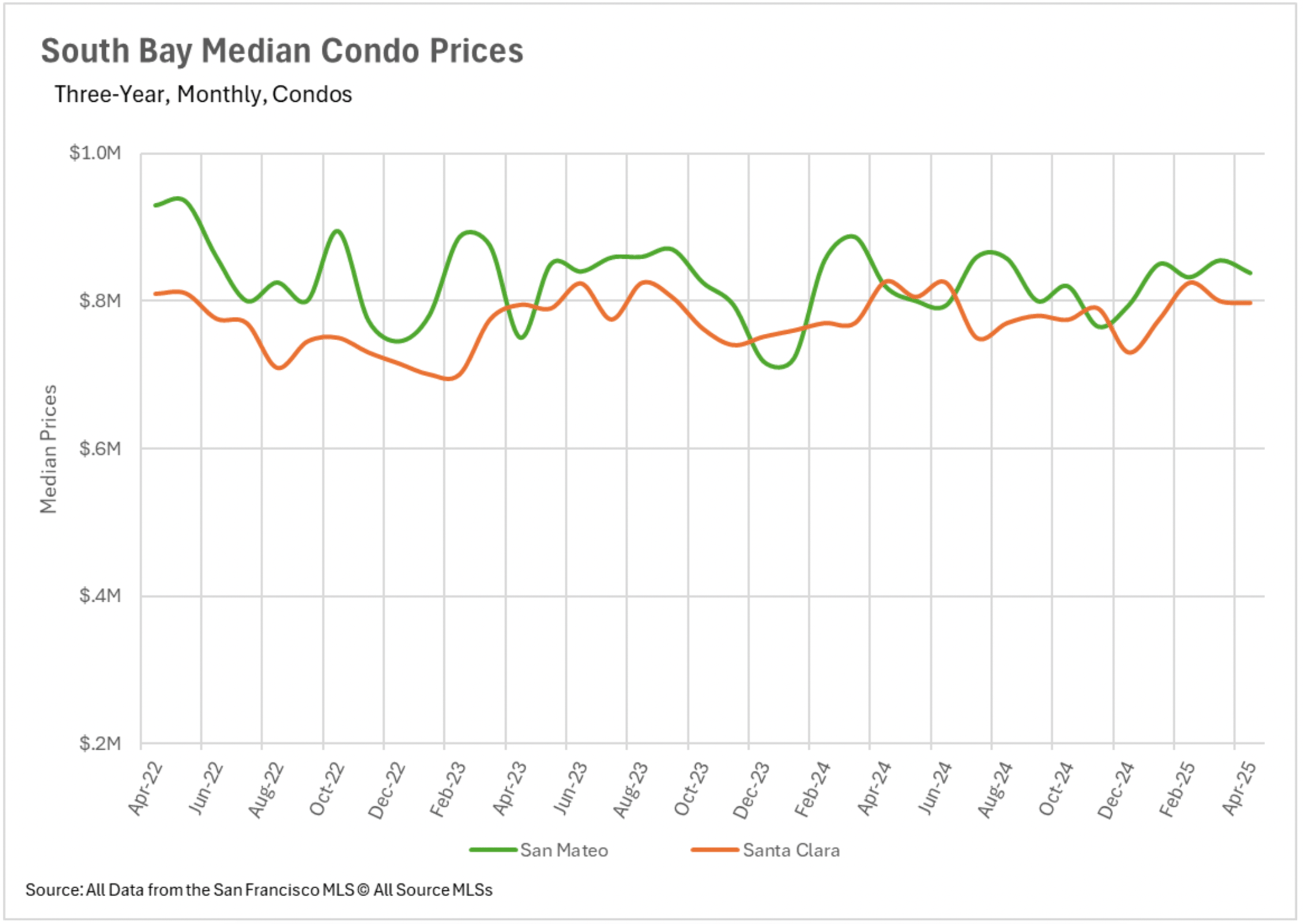

April's market performance highlighted considerable variation in price movements across Bay Area territories. Silicon Valley exhibited mixed results, with Santa Cruz County interrupting its previous twelve-month appreciation streak as median values declined 8.57% year-over-year, while San Mateo and Santa Clara Counties maintained positive momentum at 1.69% and 5.50% respectively.

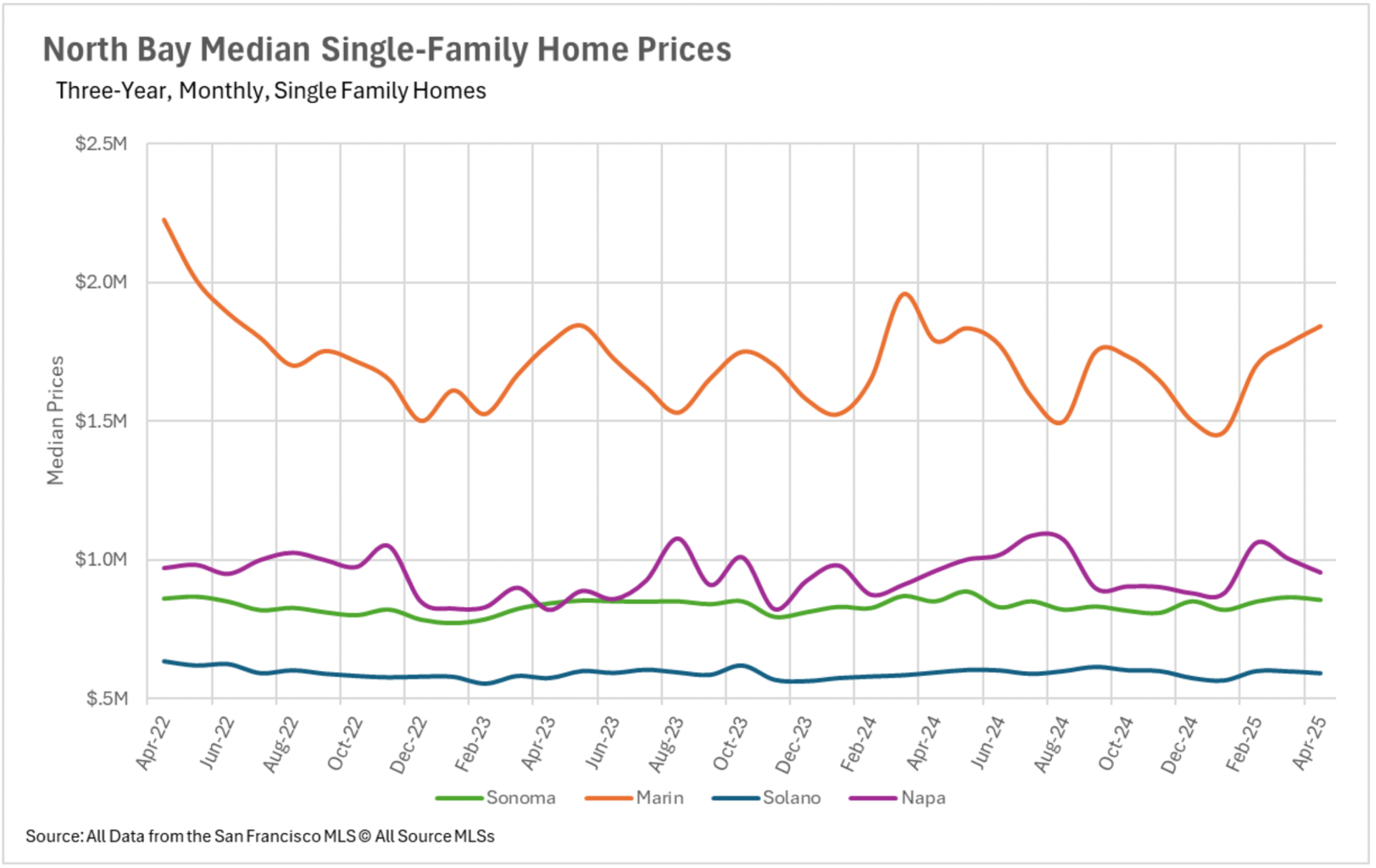

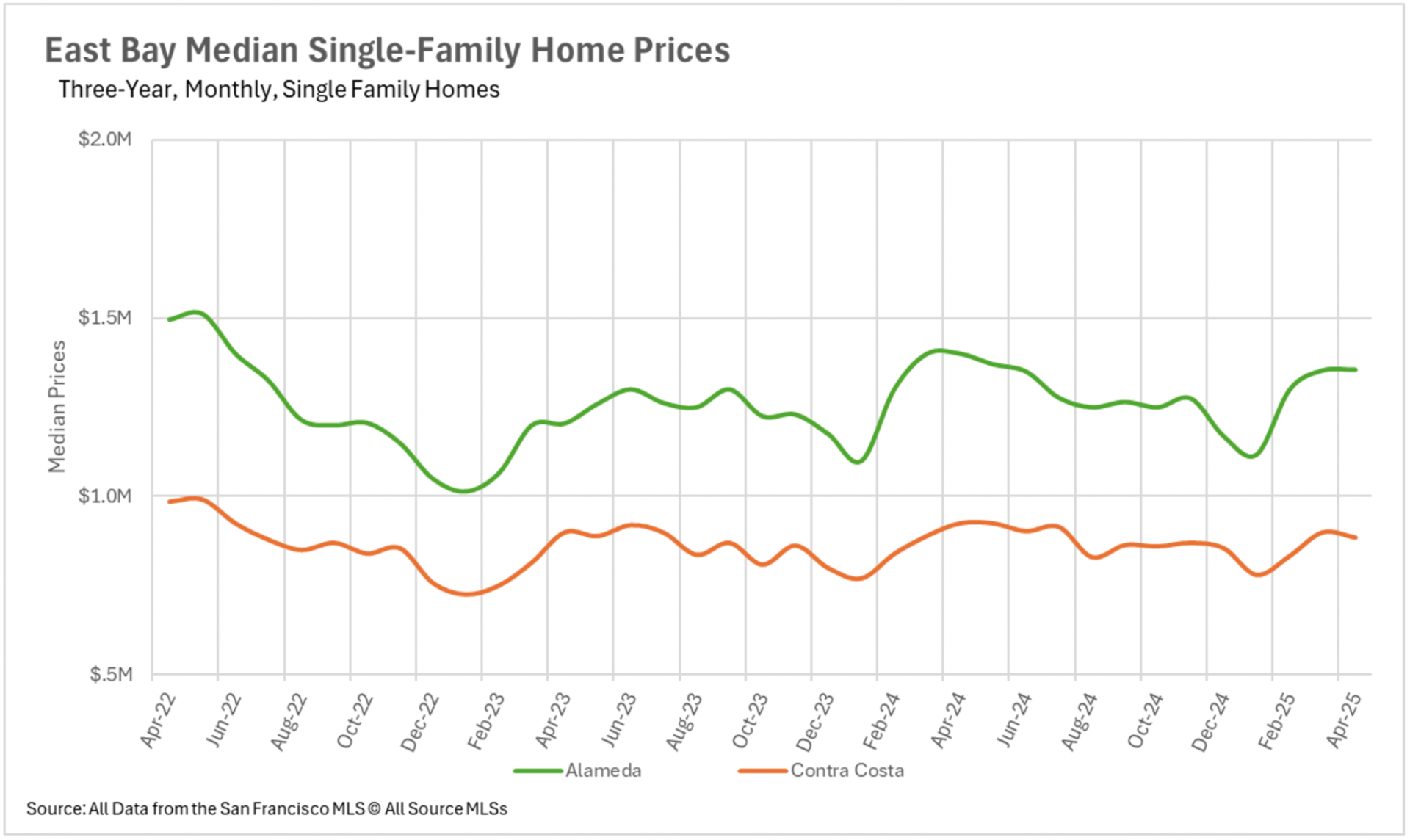

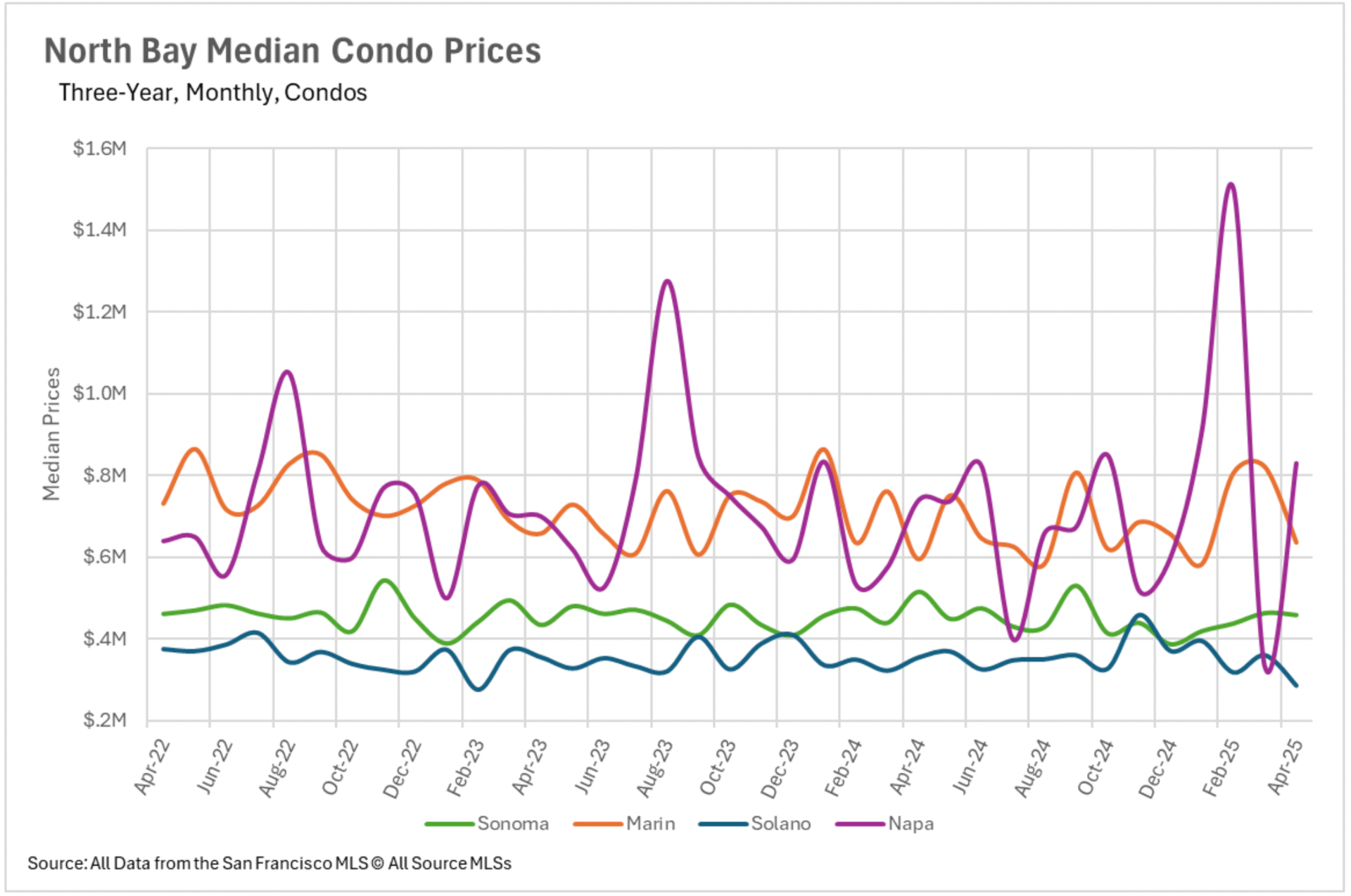

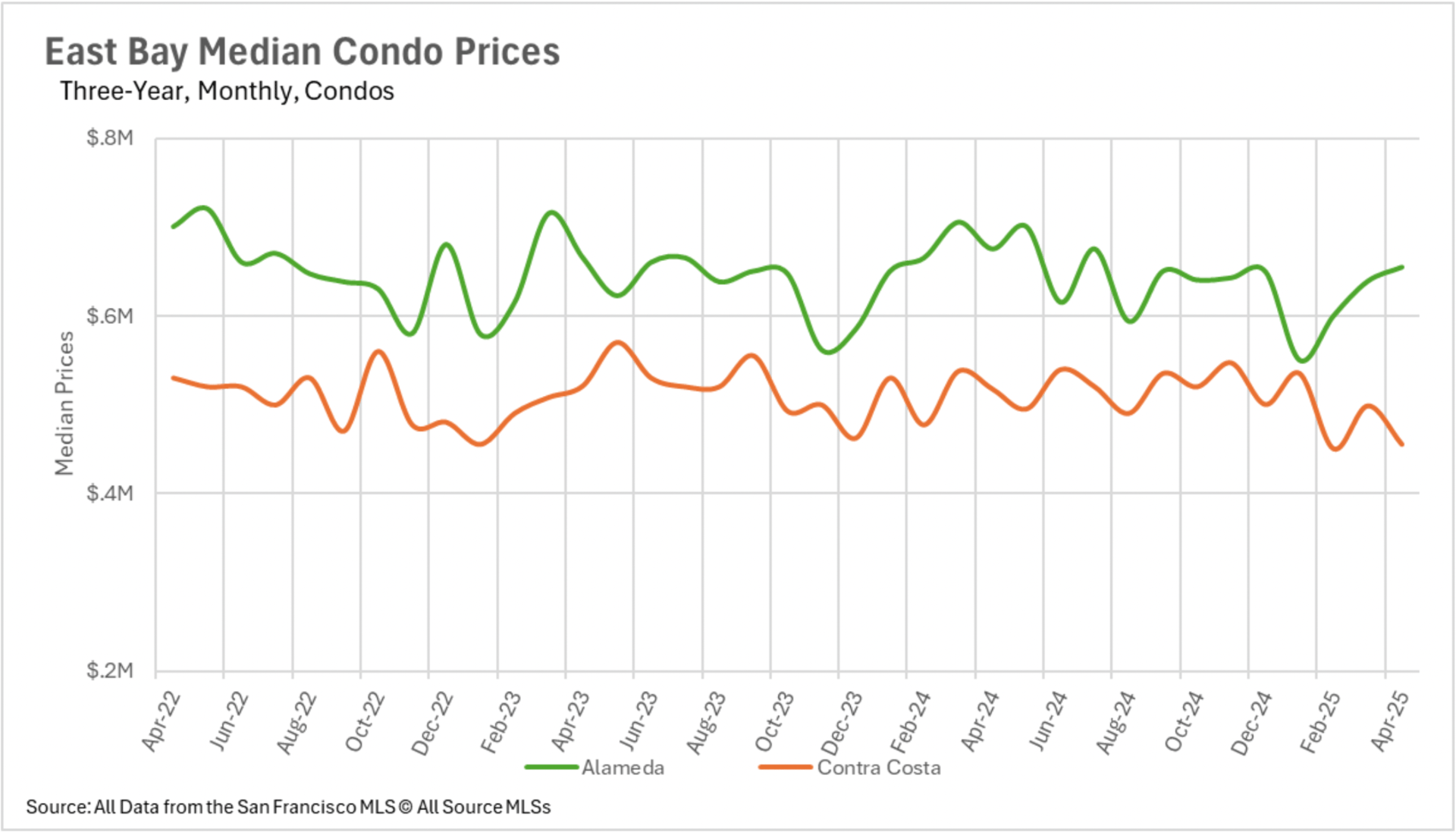

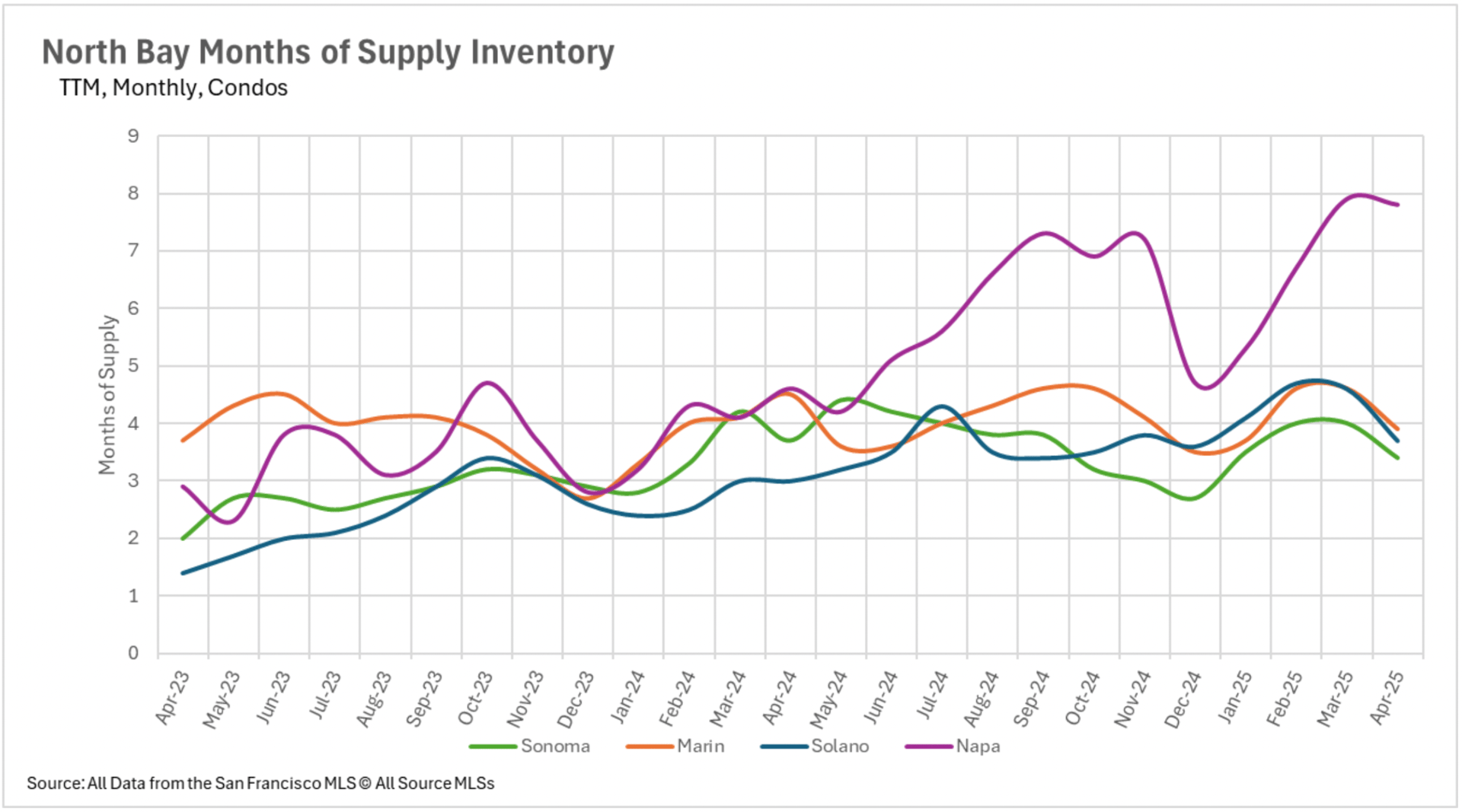

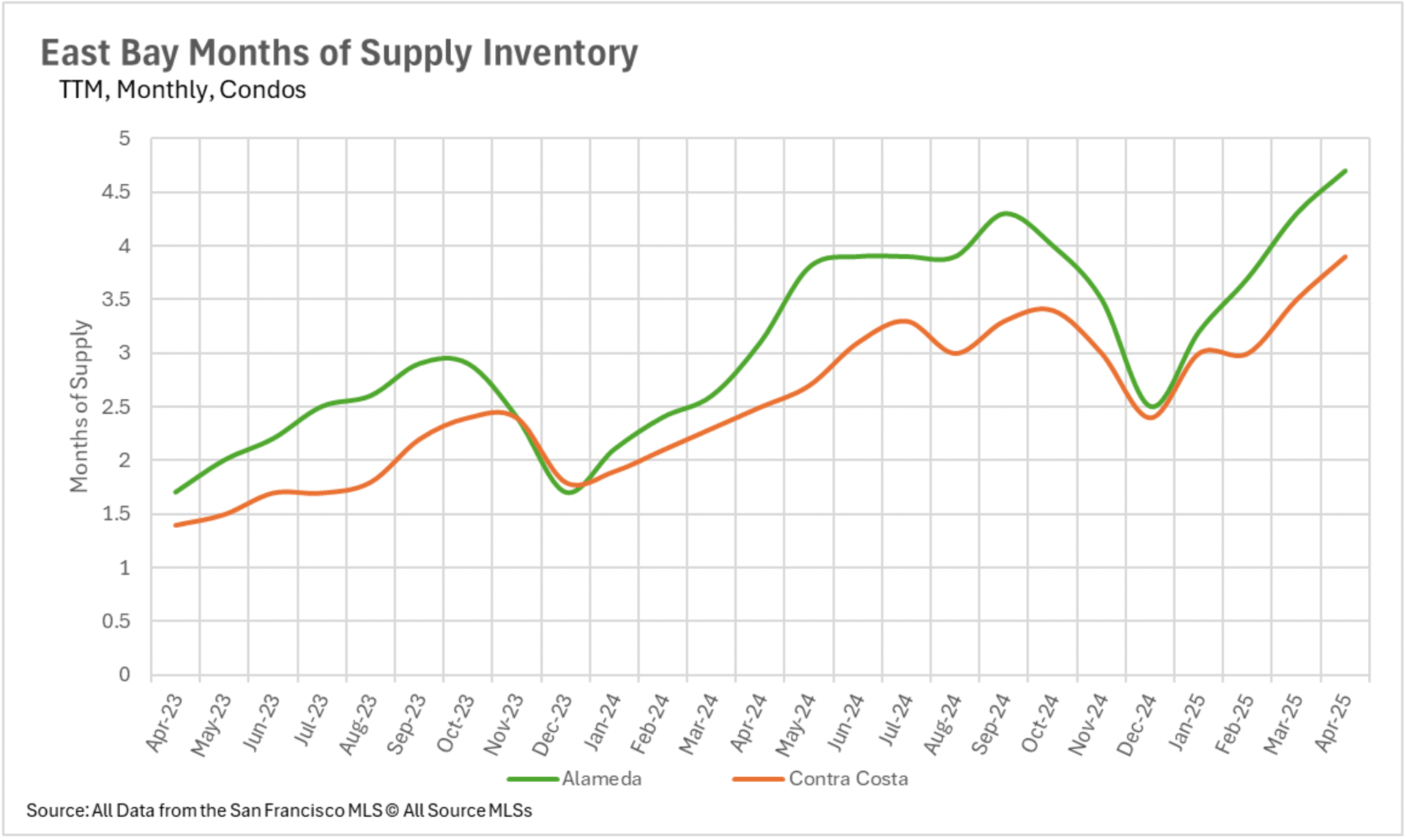

East Bay markets experienced broader price corrections, with single-family residences in Alameda and Contra Costa Counties recording decreases of 3.21% and 4.31%, alongside a pronounced 12% reduction in Contra Costa condominium values. North Bay valuations remained comparatively stable, with minimal fluctuation across Sonoma, Marin, Solano, and Napa Counties (ranging between +2.93% and -0.52%).

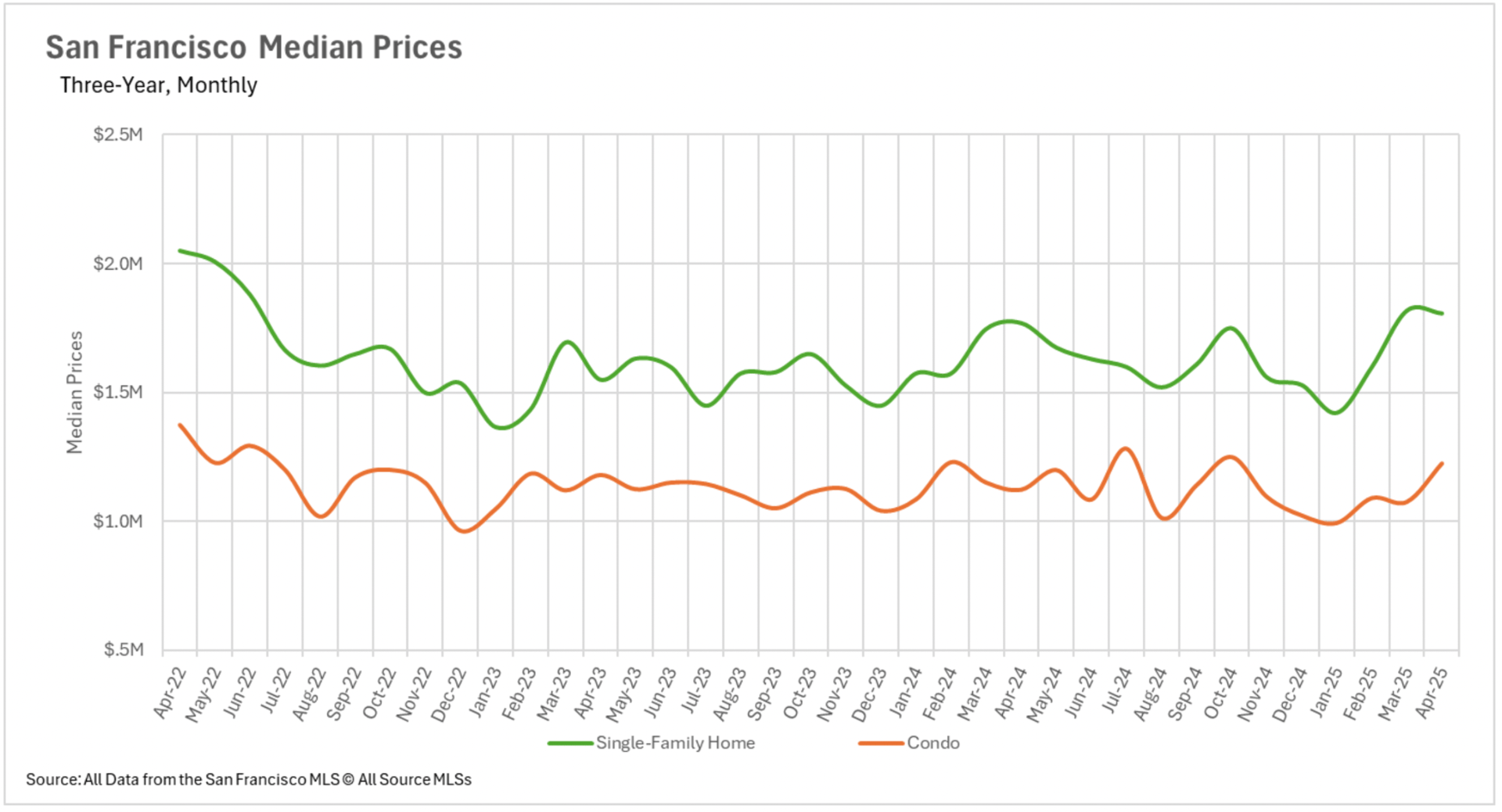

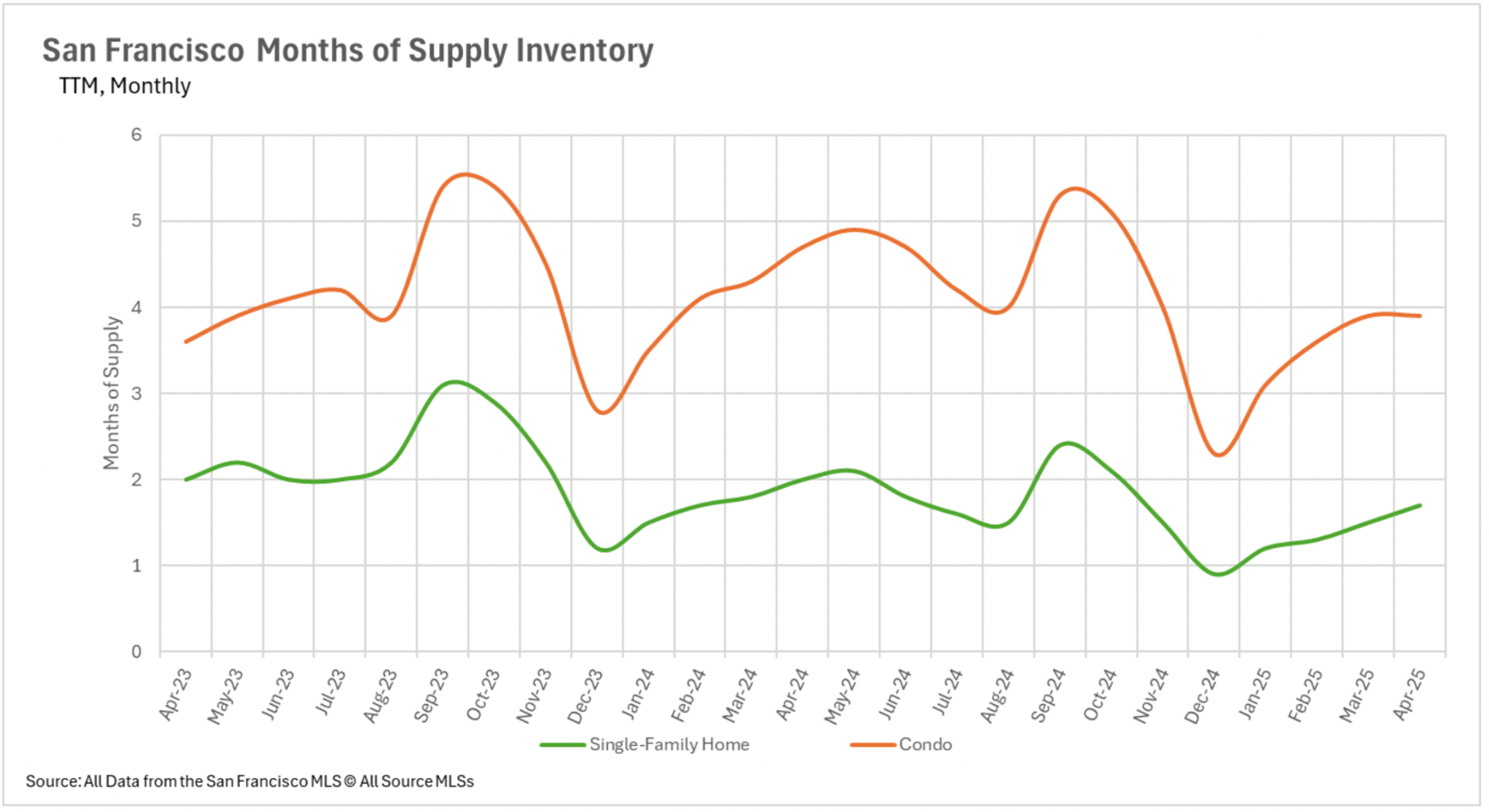

San Francisco's market displayed divergent trends, with single-family home values advancing modestly by 2.12%, while condominium prices reversed their previous five-month downward trajectory with a significant 9.13% increase, potentially indicating an inflection point for San Francisco's multi-family segment.

April's inventory landscape demonstrates substantial regional disparities across the Bay Area. East Bay markets recorded considerable supply expansion, with both single-family and condominium inventories growing approximately 43% year-over-year, driven by a 7.47% increase in new single-family listings while transaction volume contracted 12.21%.

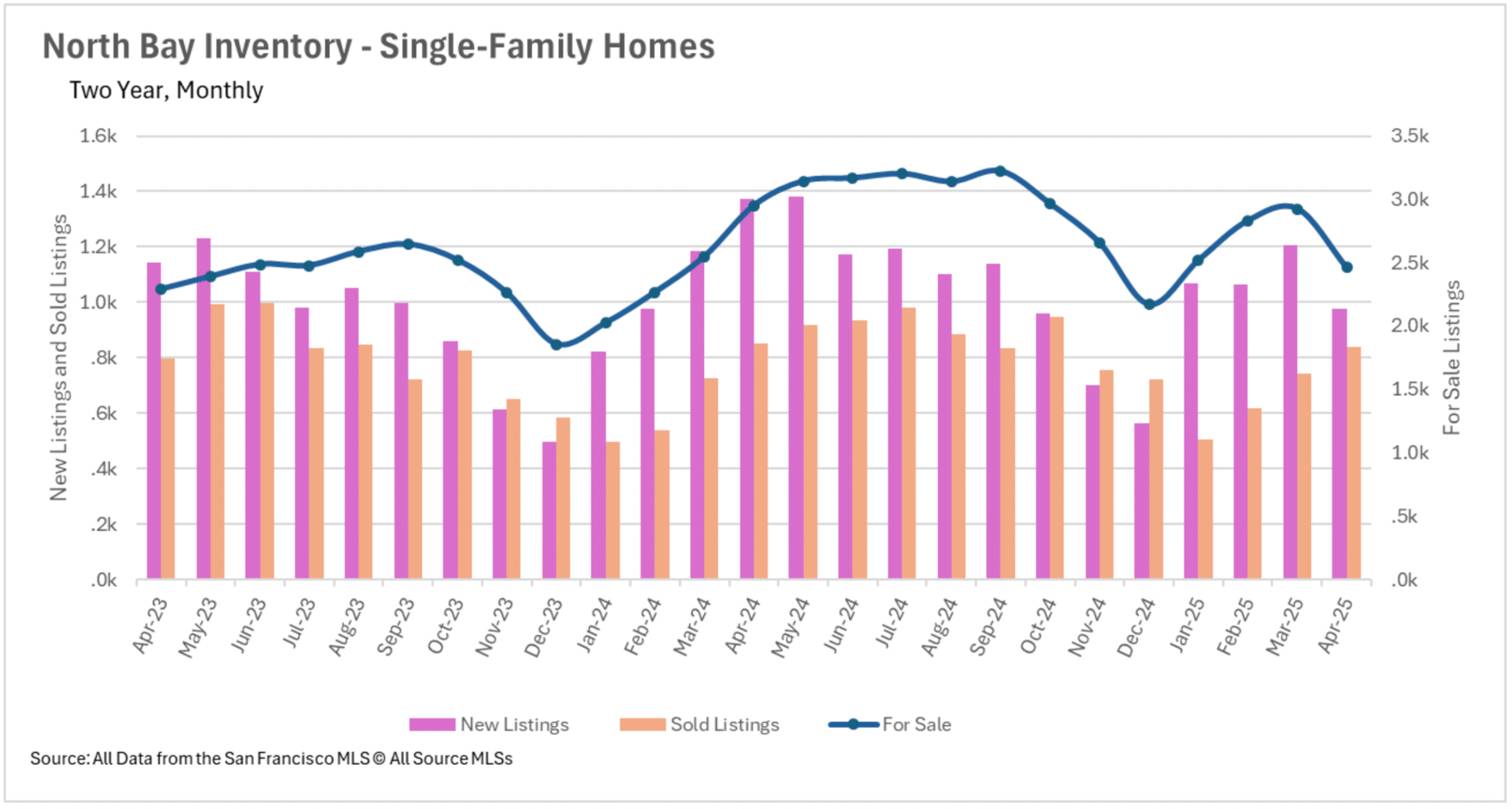

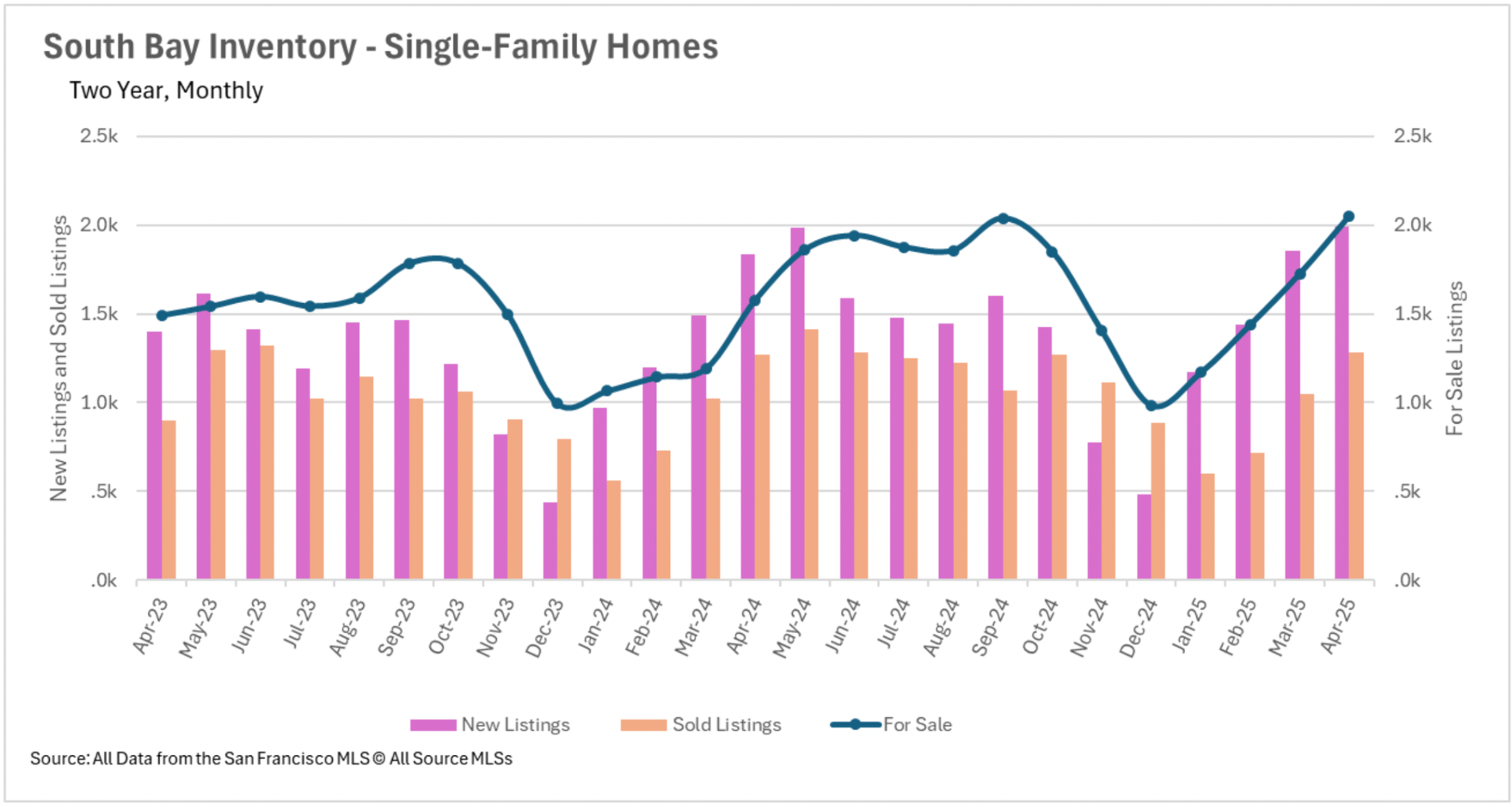

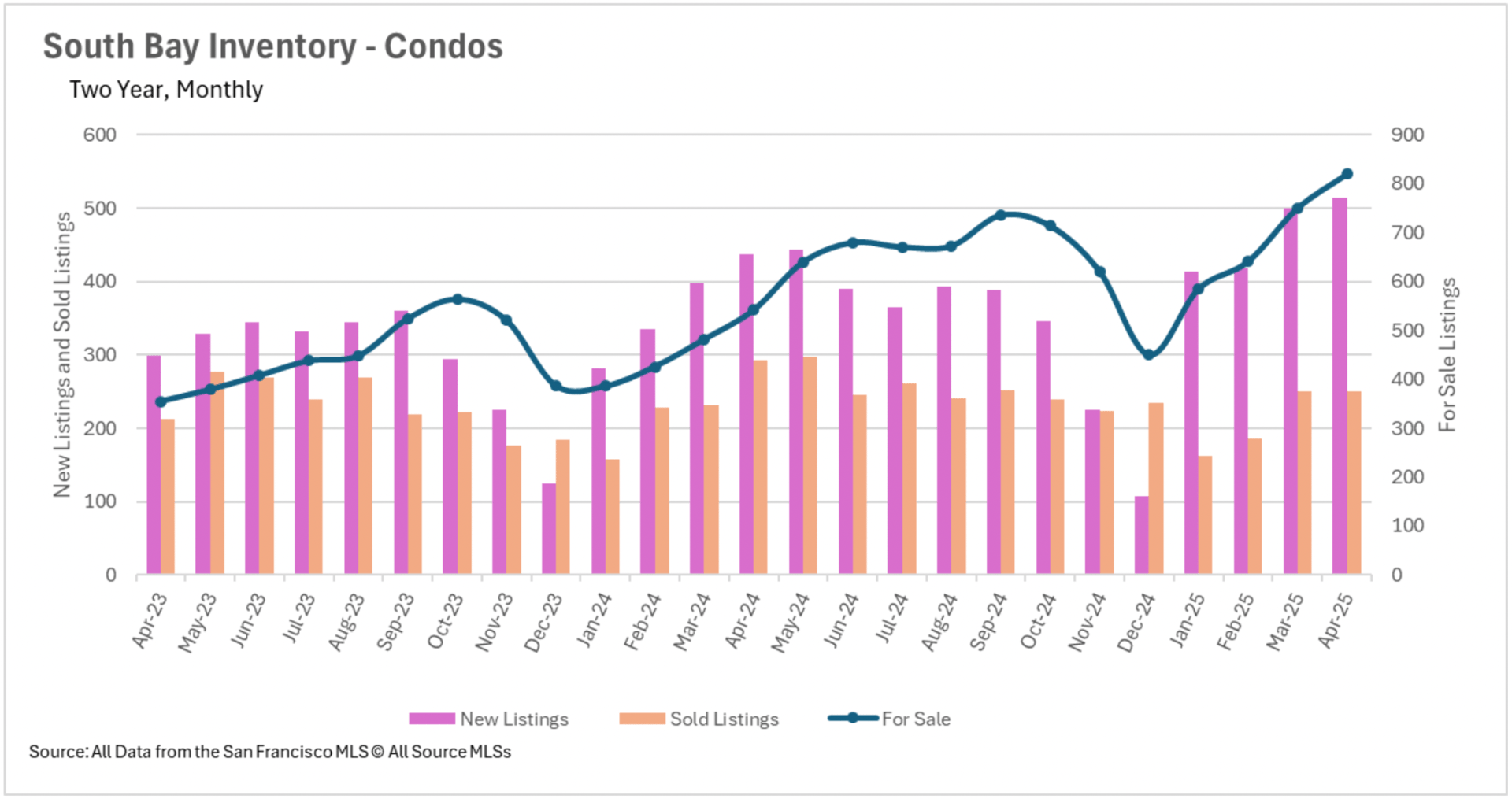

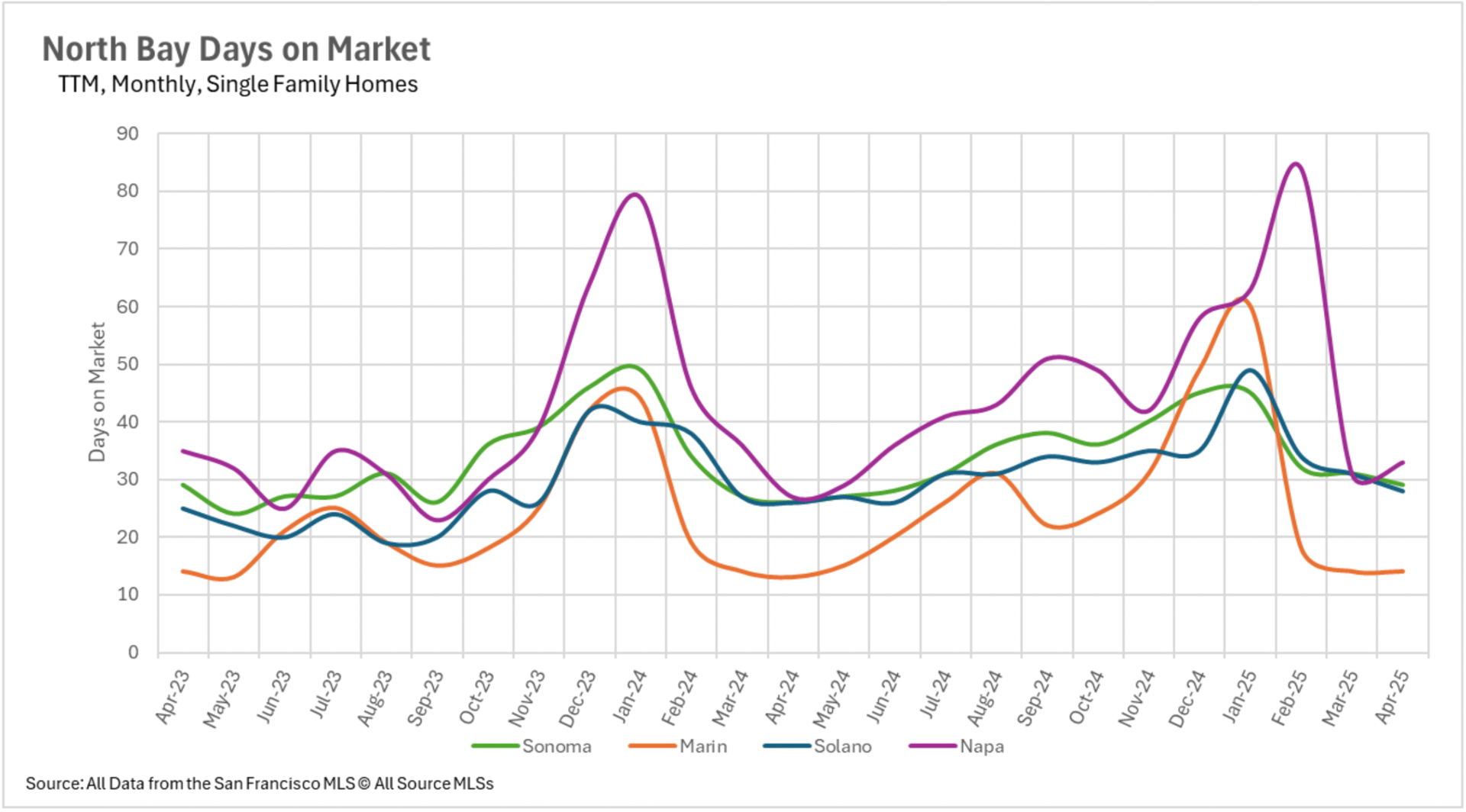

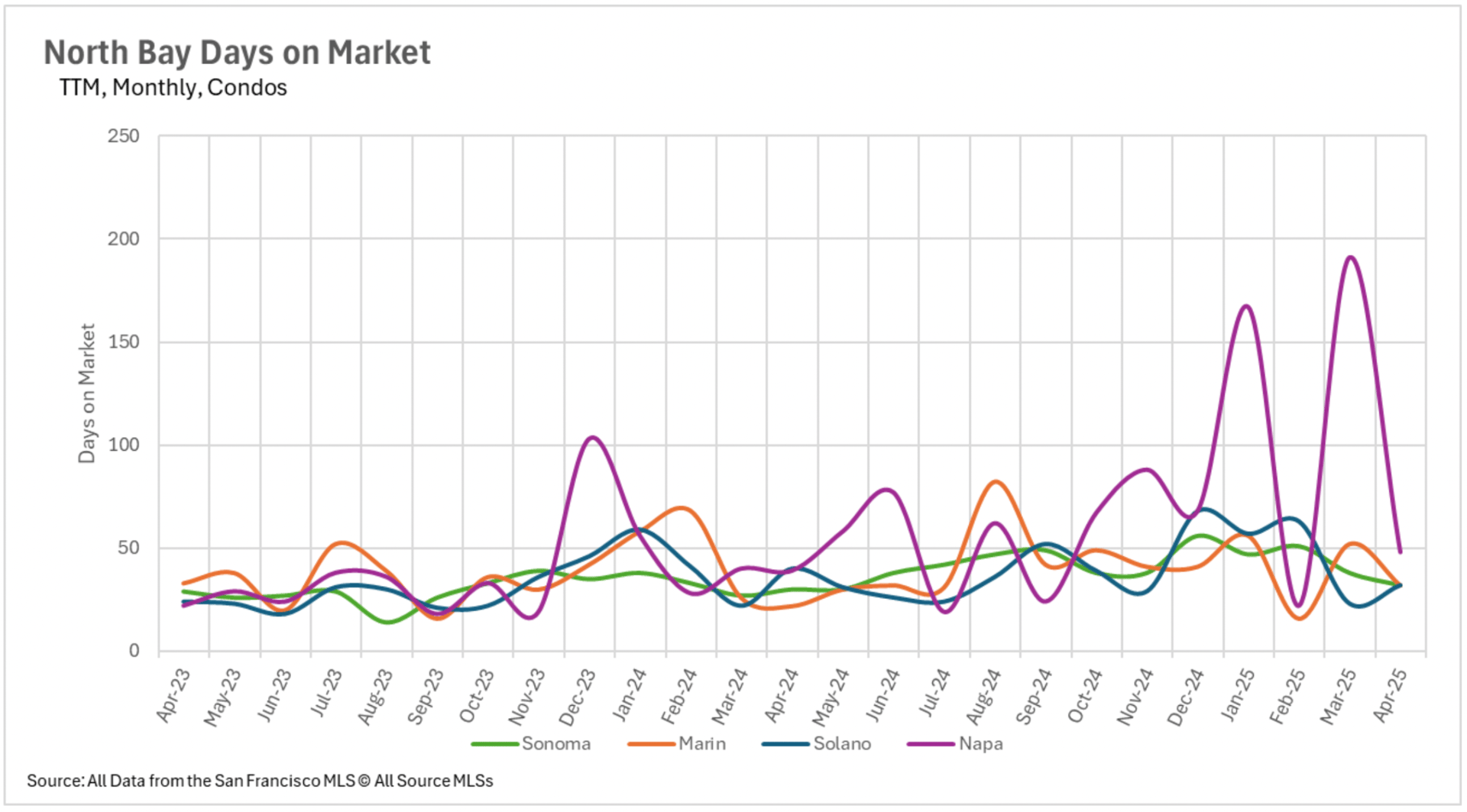

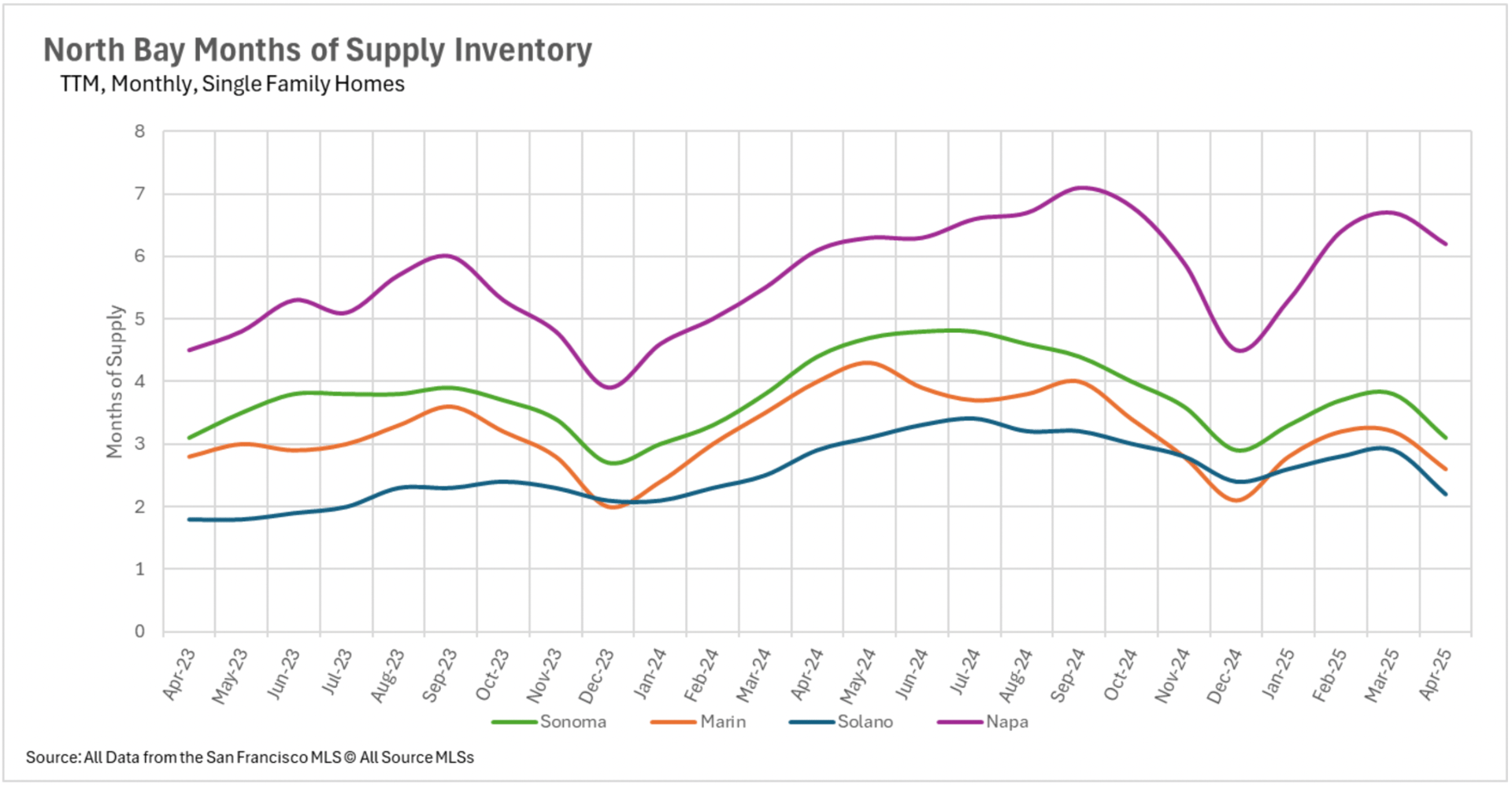

Silicon Valley similarly experienced inventory growth, with single-family supply increasing nearly 30% year-over-year while condominium availability surged by an impressive 51.29%, as new property introductions outpaced completed transactions. In marked contrast, North Bay inventory metrics continued their contraction, with a 16.61% year-over-year and 15.87% month-over-month reduction in active listings, primarily attributable to 30% fewer new market introductions compared to the previous year.

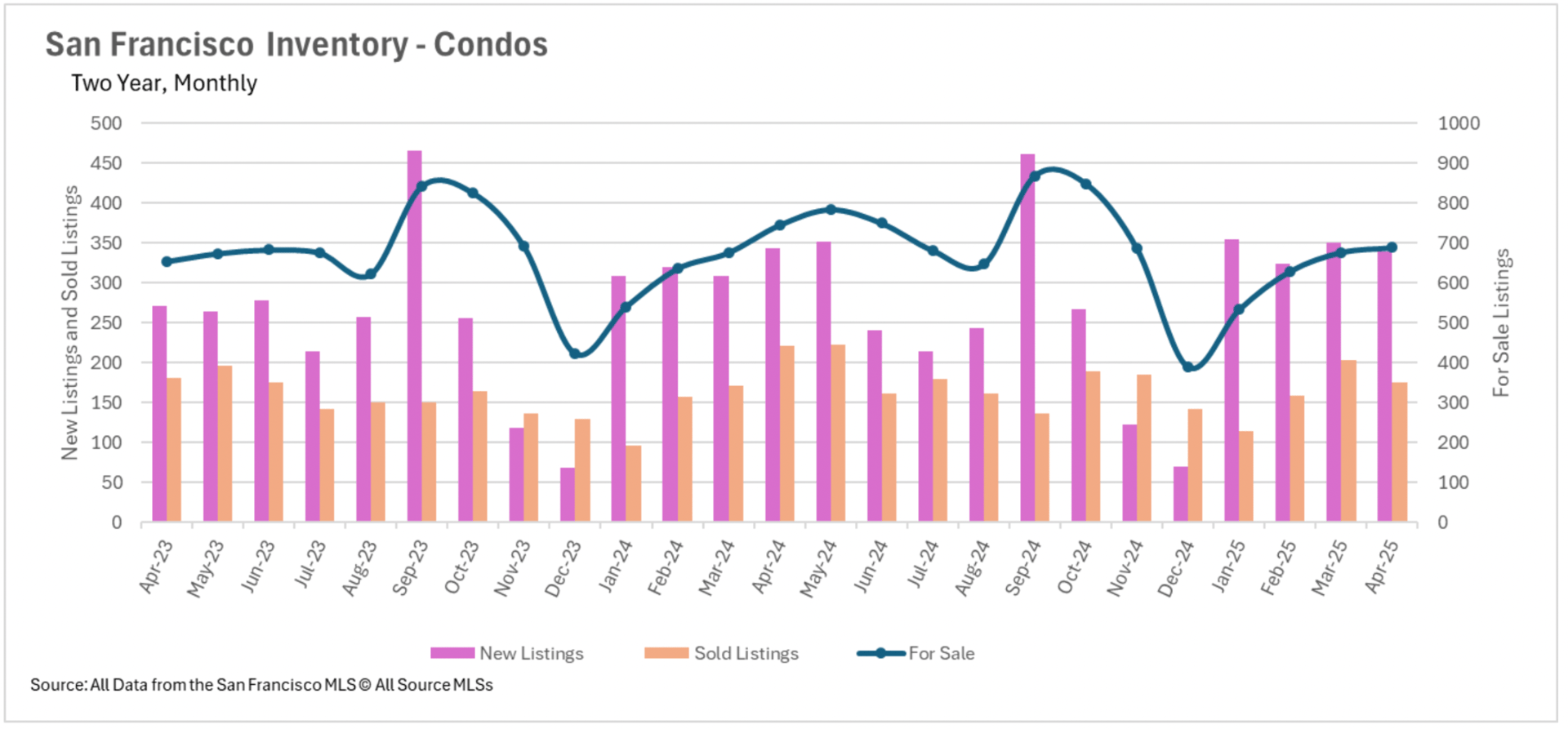

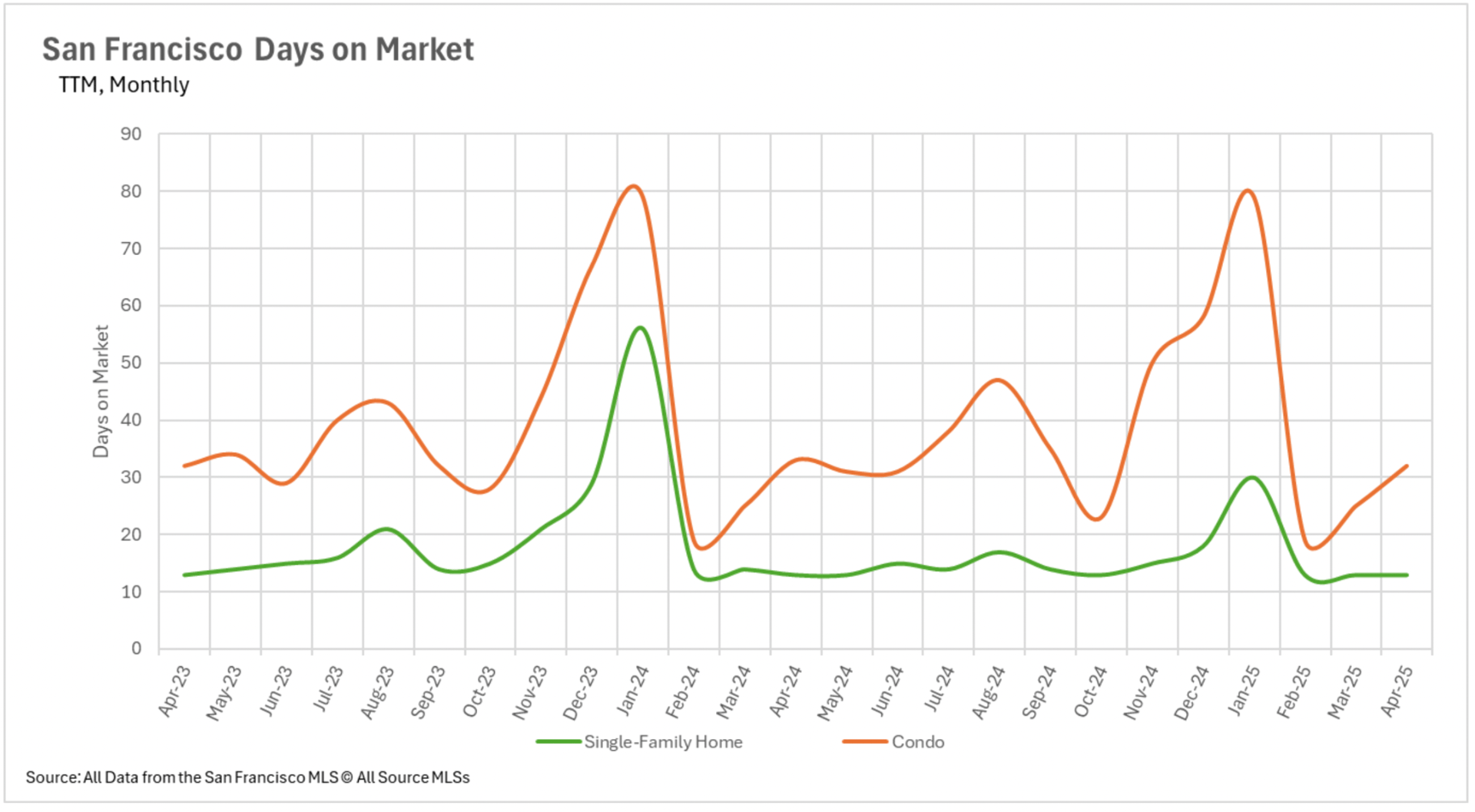

San Francisco's supply challenges remain particularly acute, with single-family listings declining 6.29% and condominium availability decreasing 7.52% year-over-year, accompanied by a substantial 21.17% reduction in condominium sales – one of the most significant contractions in recent periods.

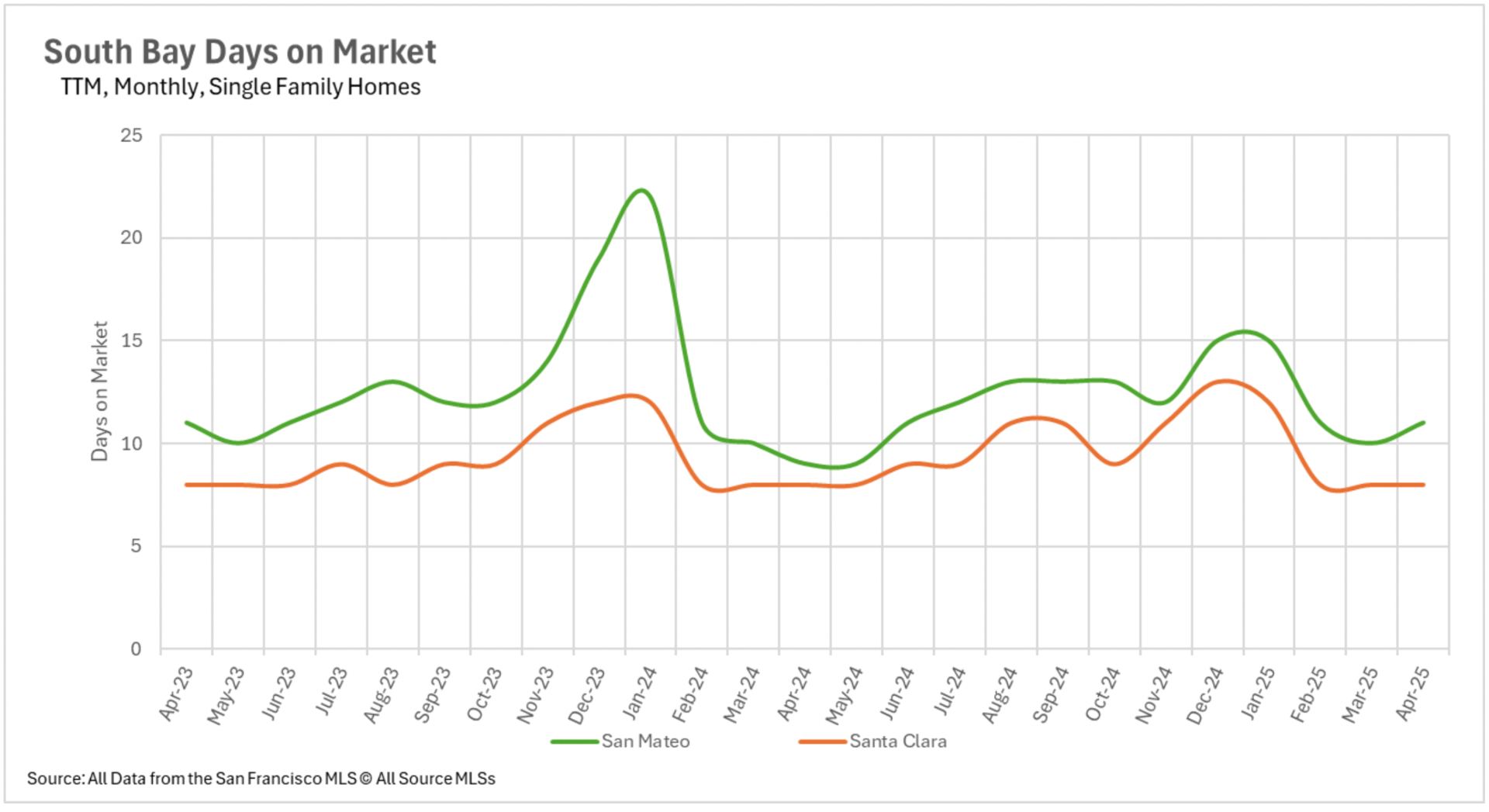

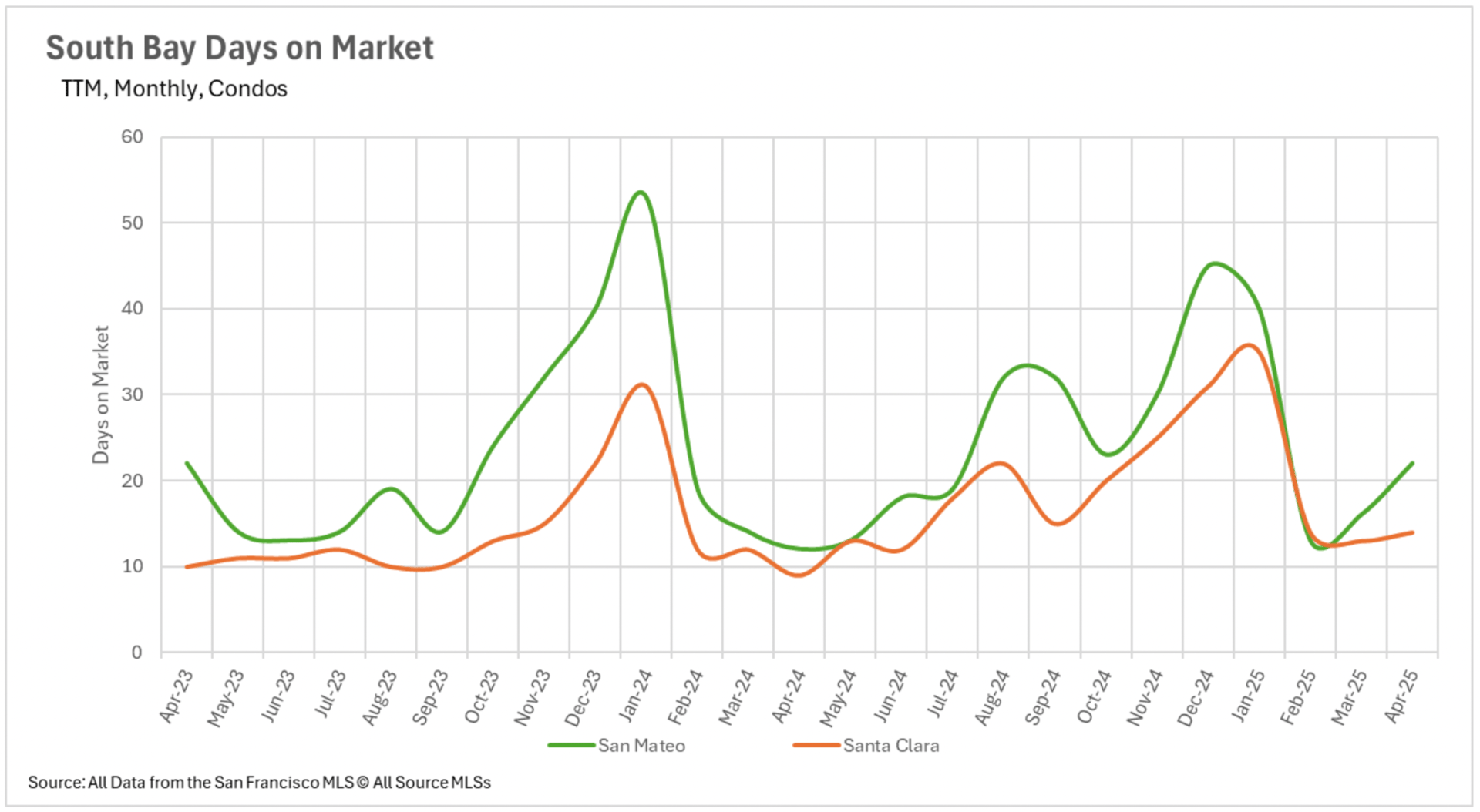

Notwithstanding diverse inventory conditions and price trajectories, properties throughout the Bay Area continue to sell with relative efficiency. Silicon Valley maintains the region's most accelerated market dynamics, with typical single-family residences in Santa Clara County transacting in merely 8 days, followed by San Mateo and Santa Cruz Counties at 11 and 15 days respectively.

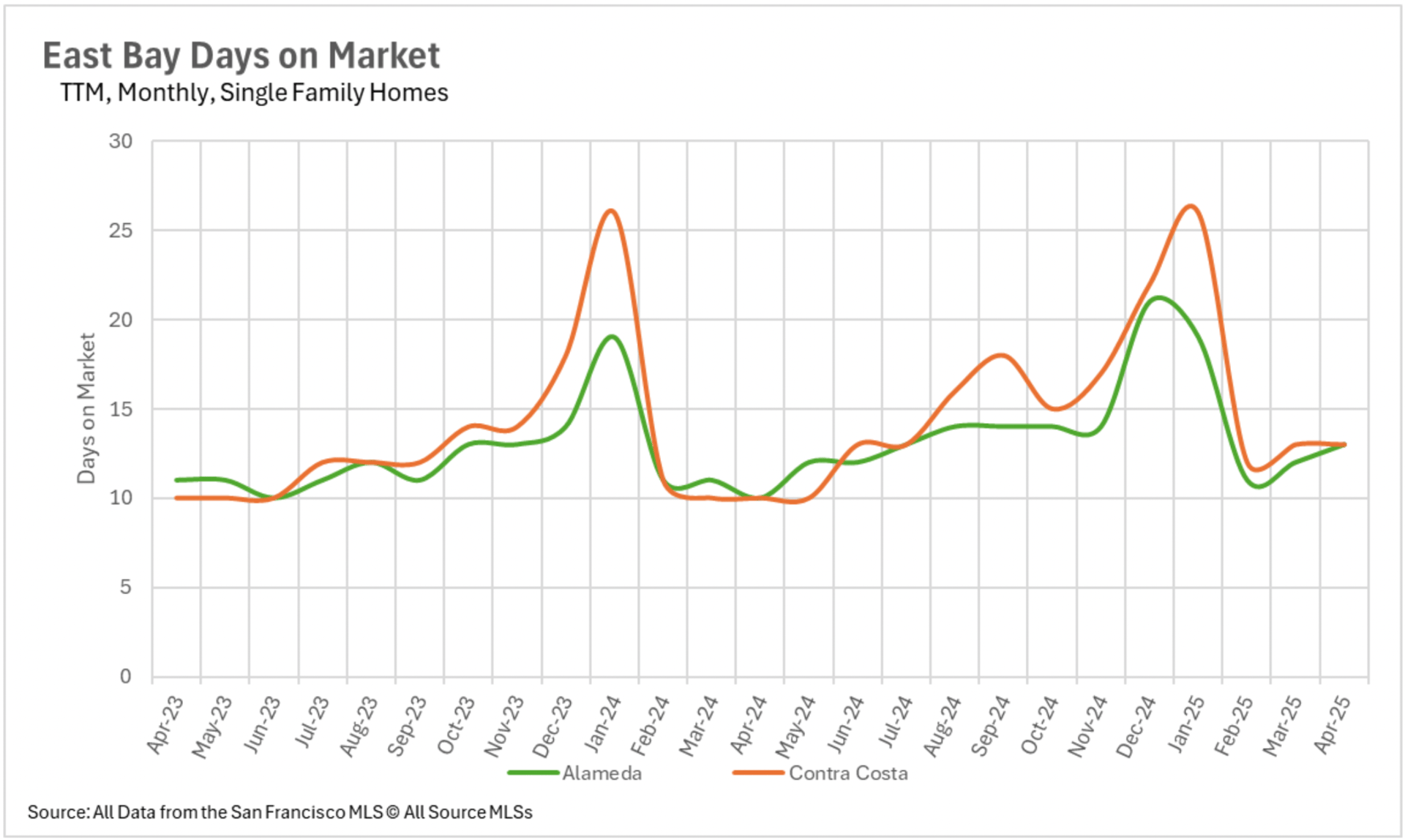

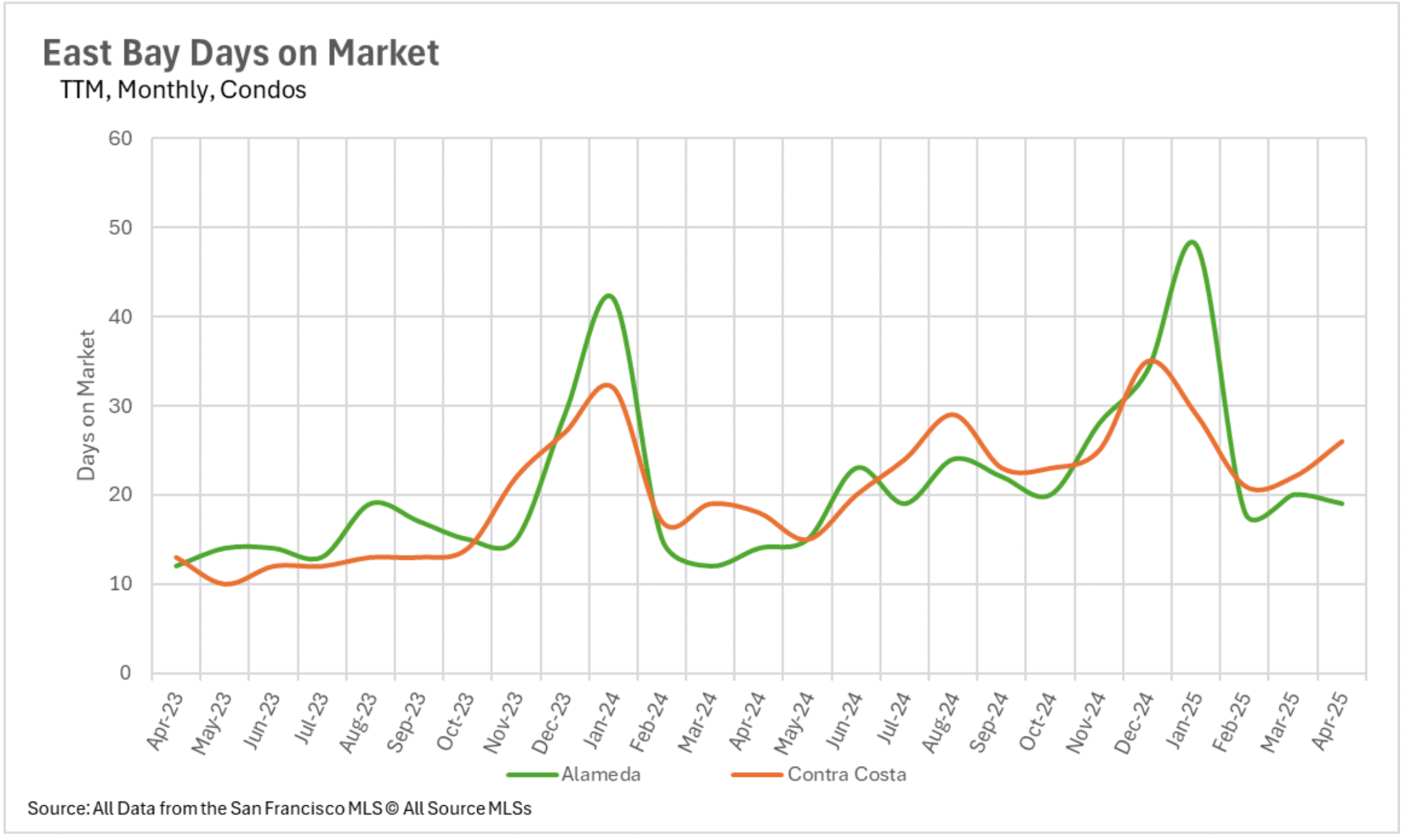

East Bay markets likewise demonstrate robust transaction velocity, with single-family properties typically remaining available for just 13 days, while condominiums sell in 19 days in Alameda County and 26 days in Contra Costa. North Bay regions are experiencing marginally extended marketing periods compared to previous year benchmarks, but still maintain reasonable timeframes.

San Francisco's single-family segment not only exhibits swift transactions but commands substantial premiums, with average properties securing 14.2% above asking price, though condominiums transact closer to list values (just 0.4% premium). These comparatively brief marketing intervals, despite inventory expansion in certain regions, suggest persistent buyer demand throughout substantial portions of the Bay Area.

The months of supply inventory (MSI) metric reveals a consistent pattern across Bay Area markets, with single-family properties generally maintaining seller-favorable conditions while condominiums advantage buyers. San Francisco single-family homes register just 1.7 months of supply (decisively favoring sellers), while condominiums exhibit 3.9 months (tilting toward buyers).

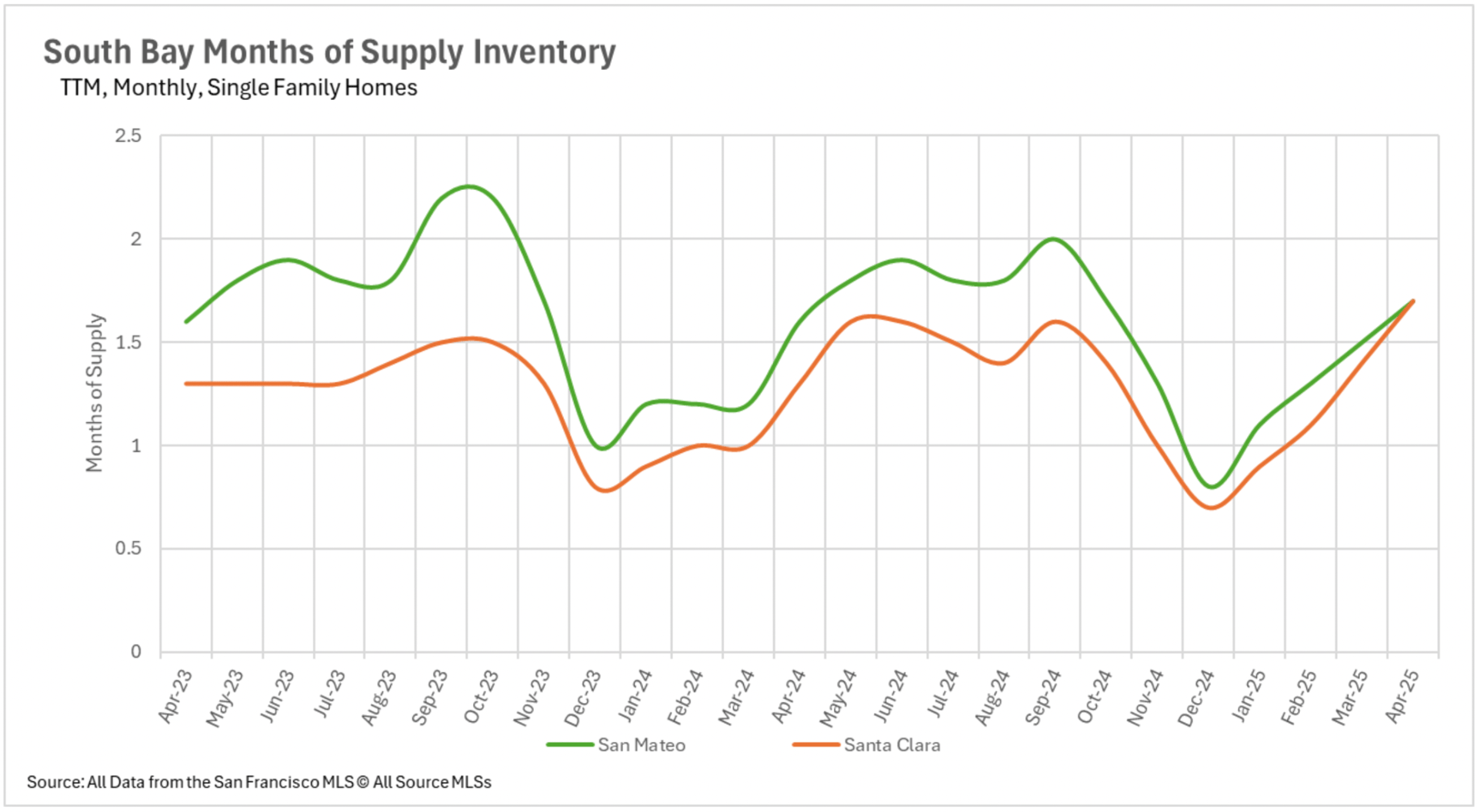

Silicon Valley displays a similar dichotomy, with San Mateo and Santa Clara Counties showing 1.7 months for single-family residences, while condominiums range between 3.2 and 5.6 months of supply. East Bay single-family segments register 2.2 months in Alameda and 2.5 months in Contra Costa, indicating seller leverage persists for now, though expanding inventory could shift dynamics toward buyer advantage this summer.

Meanwhile, East Bay condominiums clearly favor purchasers with 4.7 and 3.9 months of supply in Alameda and Contra Costa Counties respectively. North Bay markets demonstrate greater variation, with Napa County at 6.2 months (strongly advantaging buyers), Sonoma at 3.1 months (balanced), and Marin and Solano at 2.6 and 2.2 months respectively (favoring sellers). This consistent pattern of lower MSI for single-family properties versus condominiums manifests throughout the Bay Area, underscoring the sustained preference for detached housing.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

March 5, 2026

February 28, 2026

January 16, 2026

December 30, 2025

December 4, 2025

November 19, 2025

October 21, 2025

September 24, 2025

September 23, 2025

You've got questions and we can't wait to answer them.