April Market Update

Bay Area property segments show divergent performance patterns, with detached homes consistently outperforming condominiums across most subregions

Supply conditions reflect substantial geographic variation, as Silicon Valley experiences inventory expansion while San Francisco continues to face persistent shortages

Detached homes throughout most Bay Area counties maintain seller-favorable conditions, while condominium segments generally exhibit higher supply levels advantageous to buyers

Marketing timelines exhibit dramatic regional disparities, ranging from ultra-competitive 8-16 day periods in Silicon Valley to substantially extended timeframes elsewhere

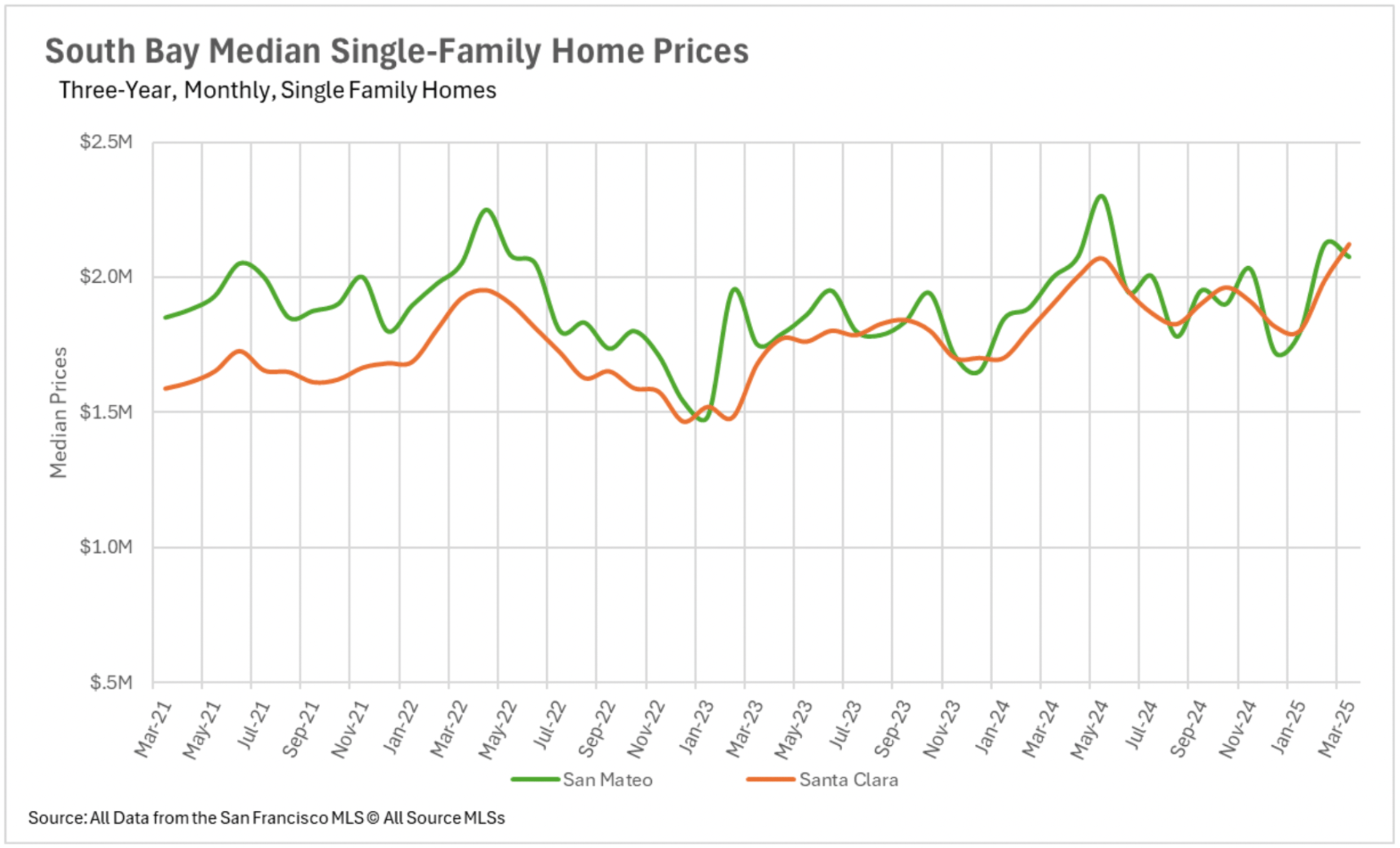

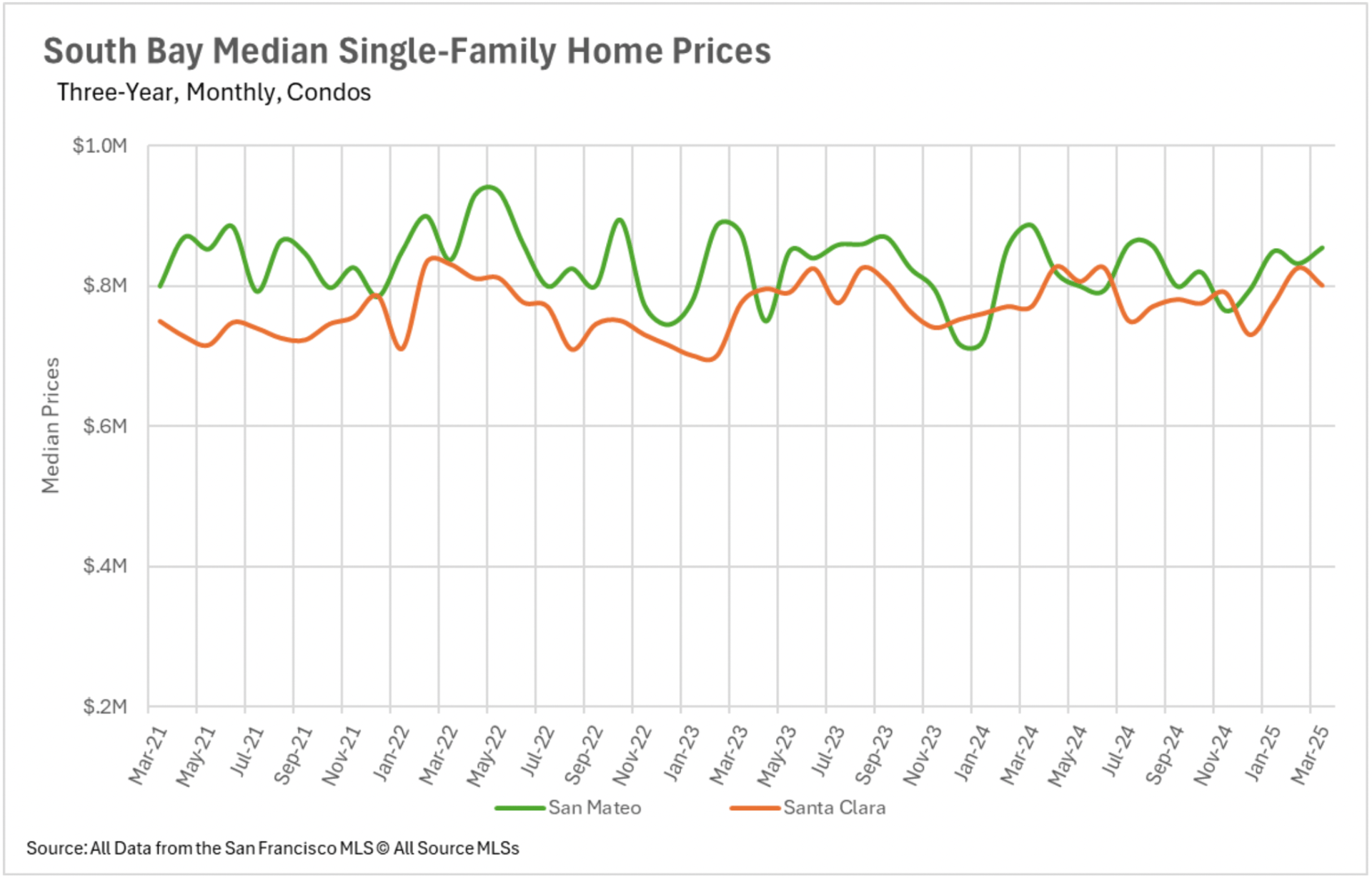

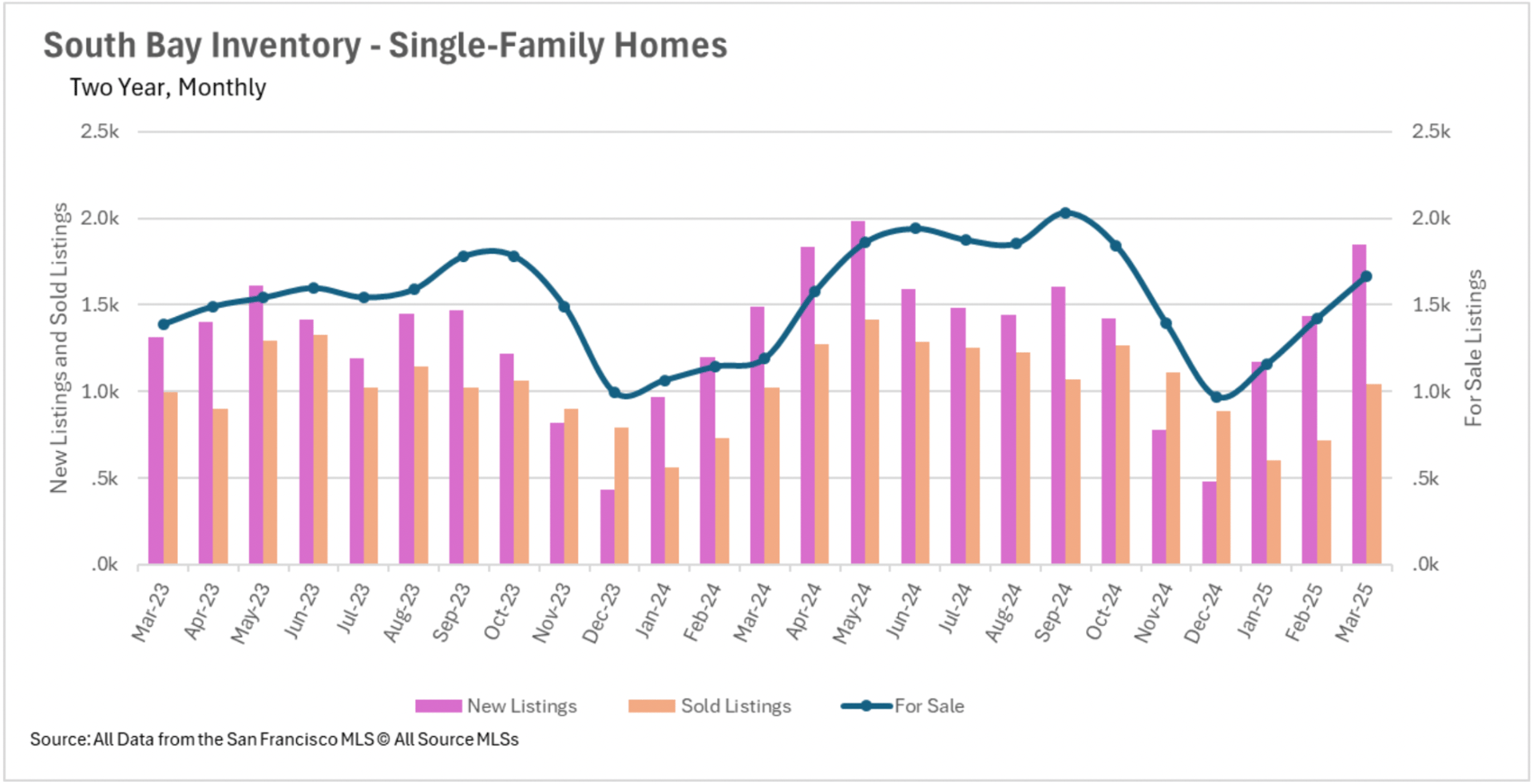

The Bay Area's residential market presents a complex tapestry of performance across its diverse subregions. Silicon Valley remains the epicenter of appreciation, with Santa Clara County recording a substantial 11.58% year-over-year median price increase this March. Neighboring San Mateo and Santa Cruz counties similarly experienced healthy growth at 3.75% and 7.27% respectively.

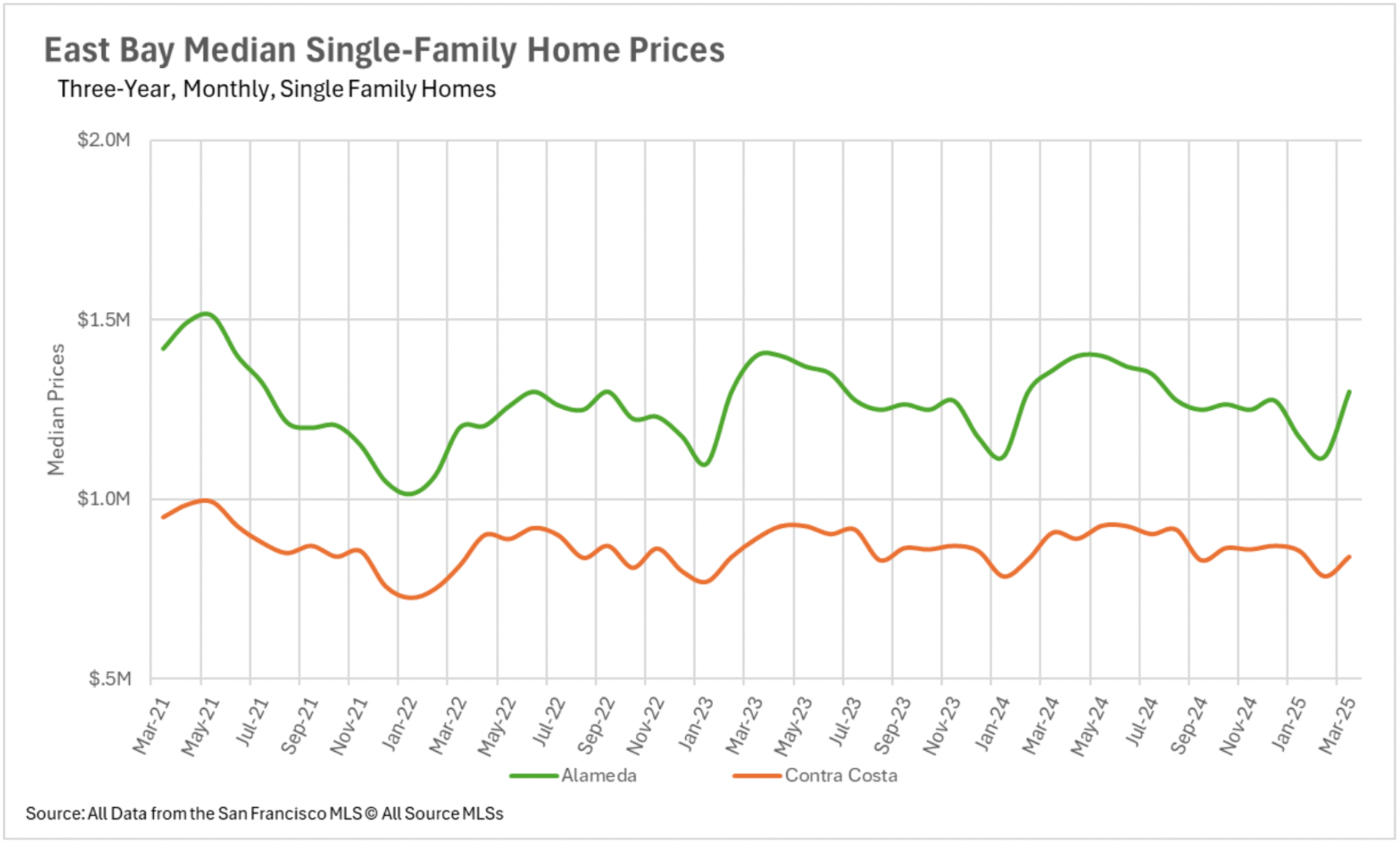

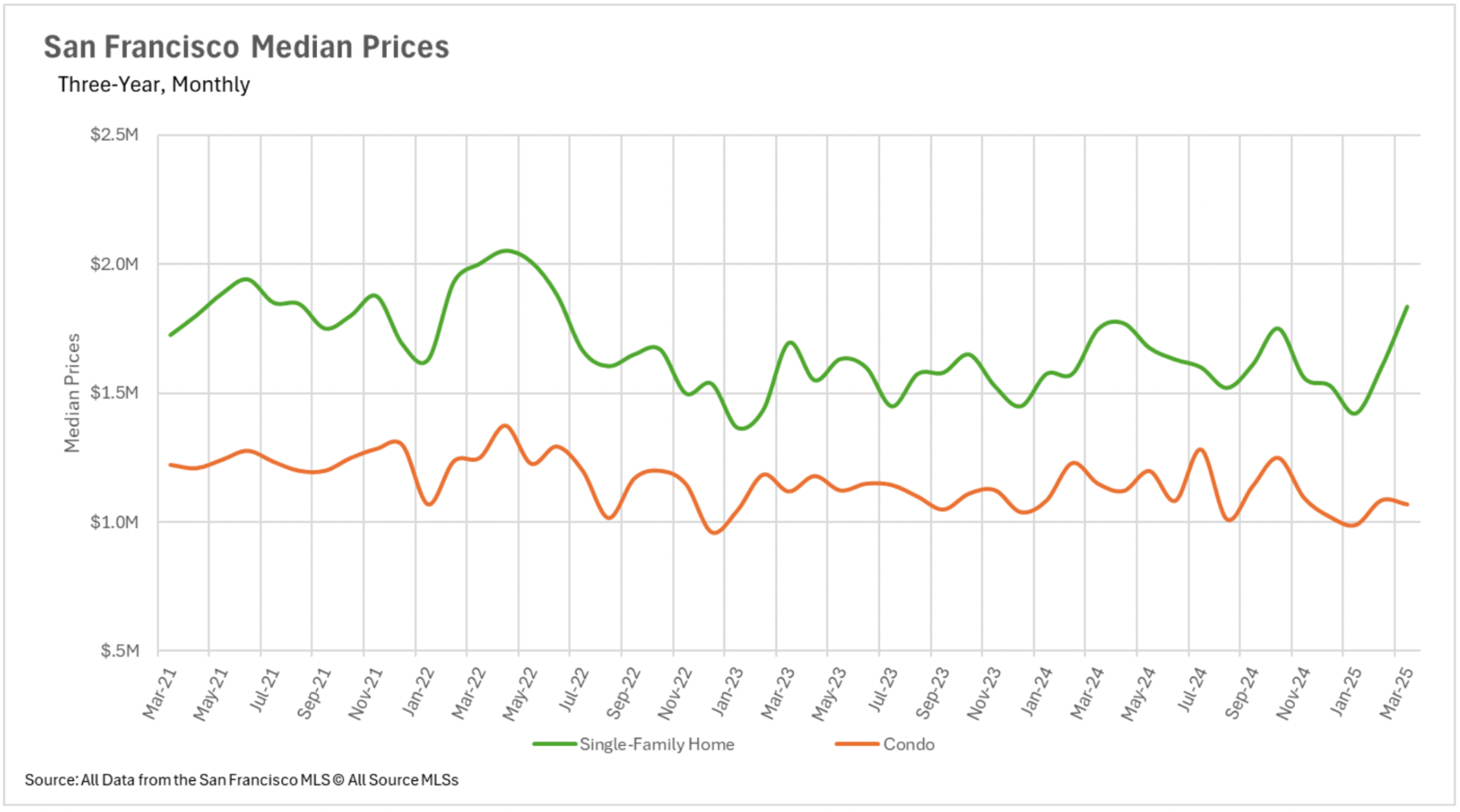

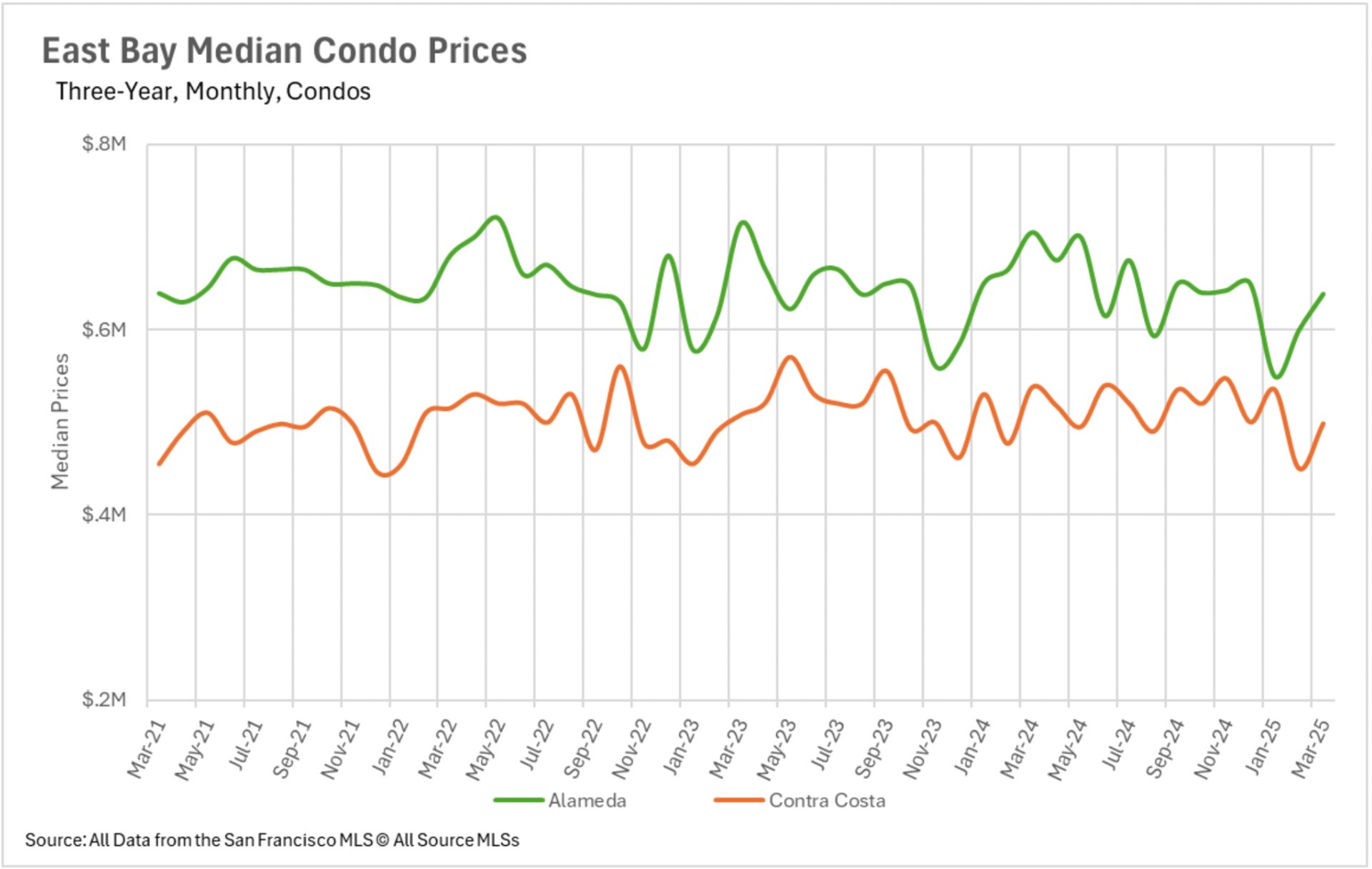

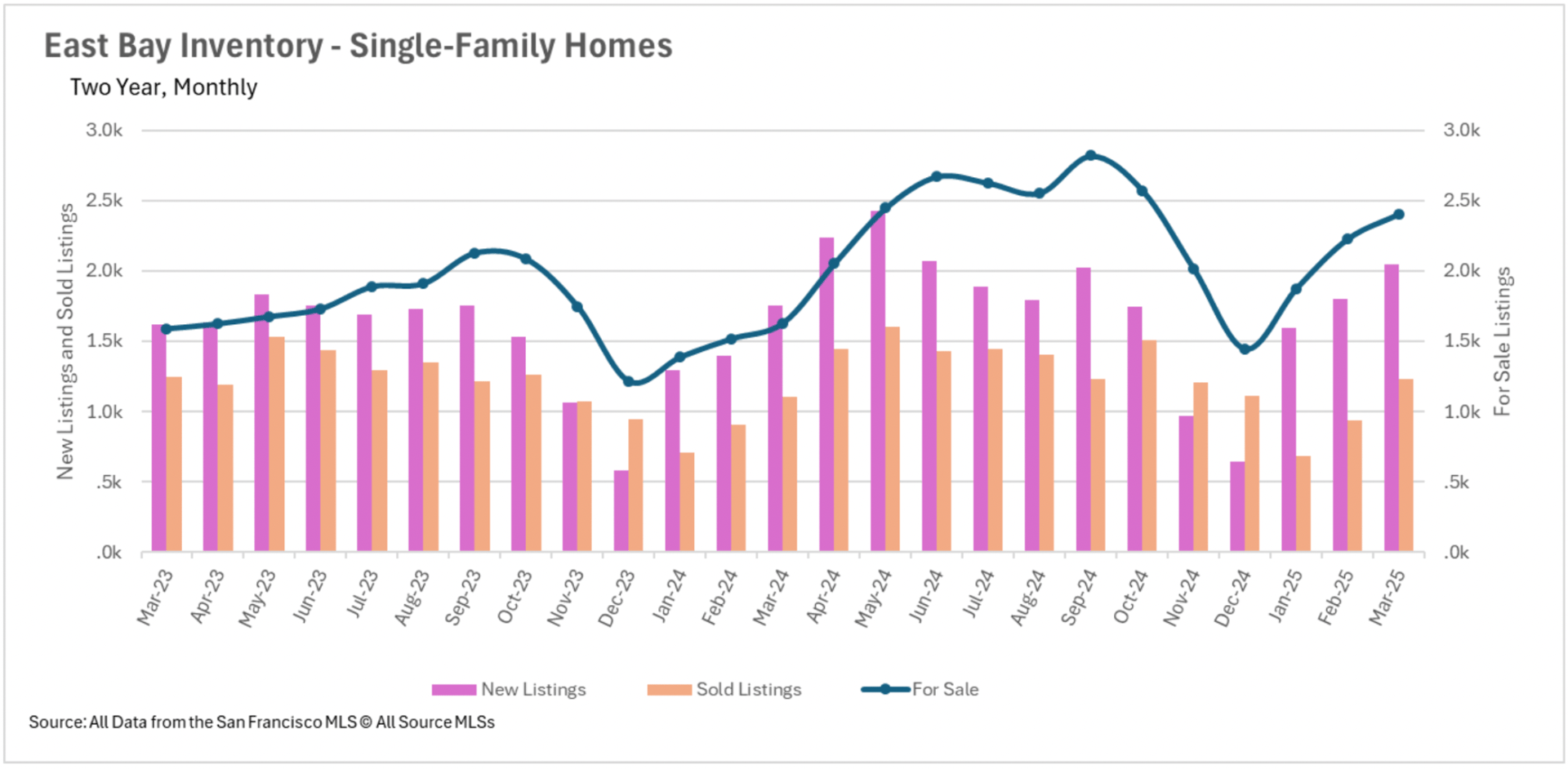

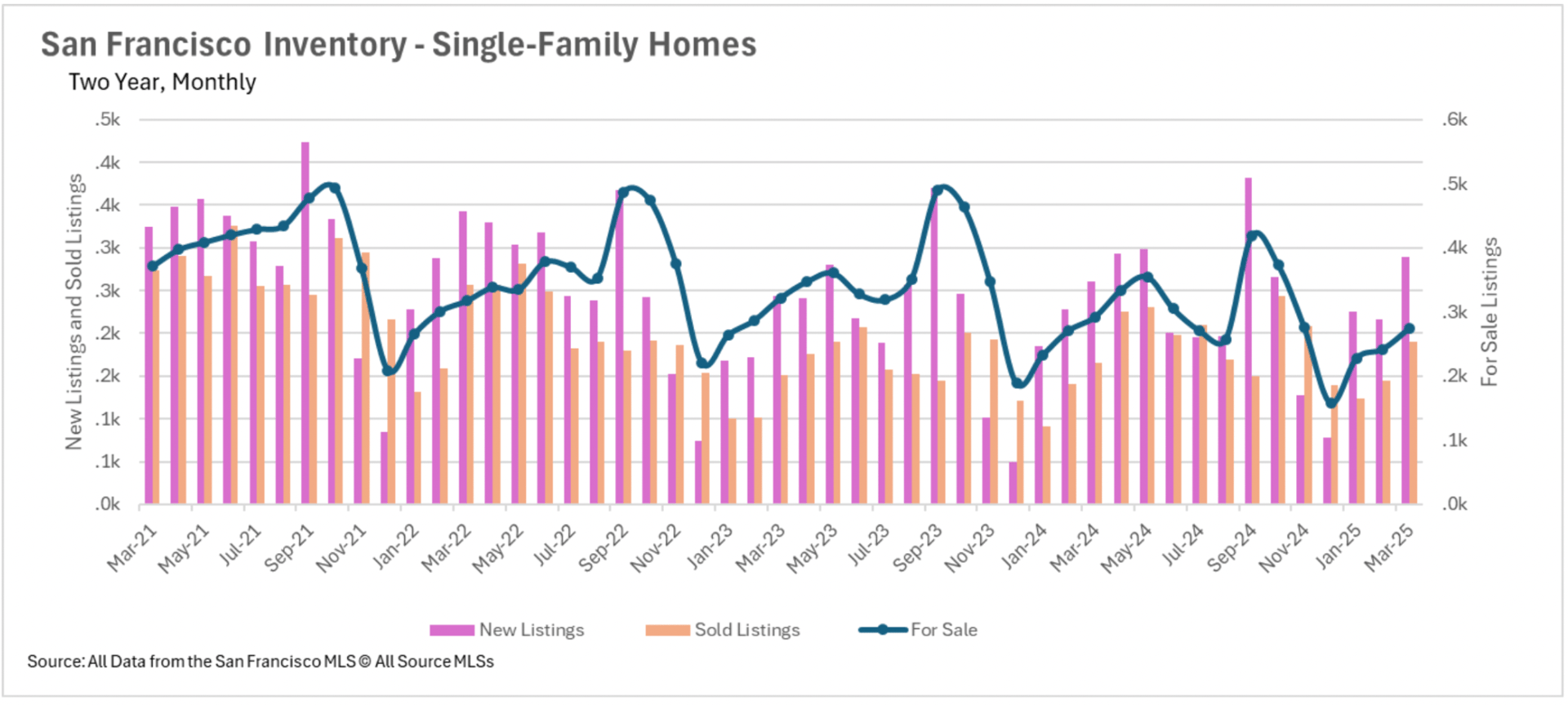

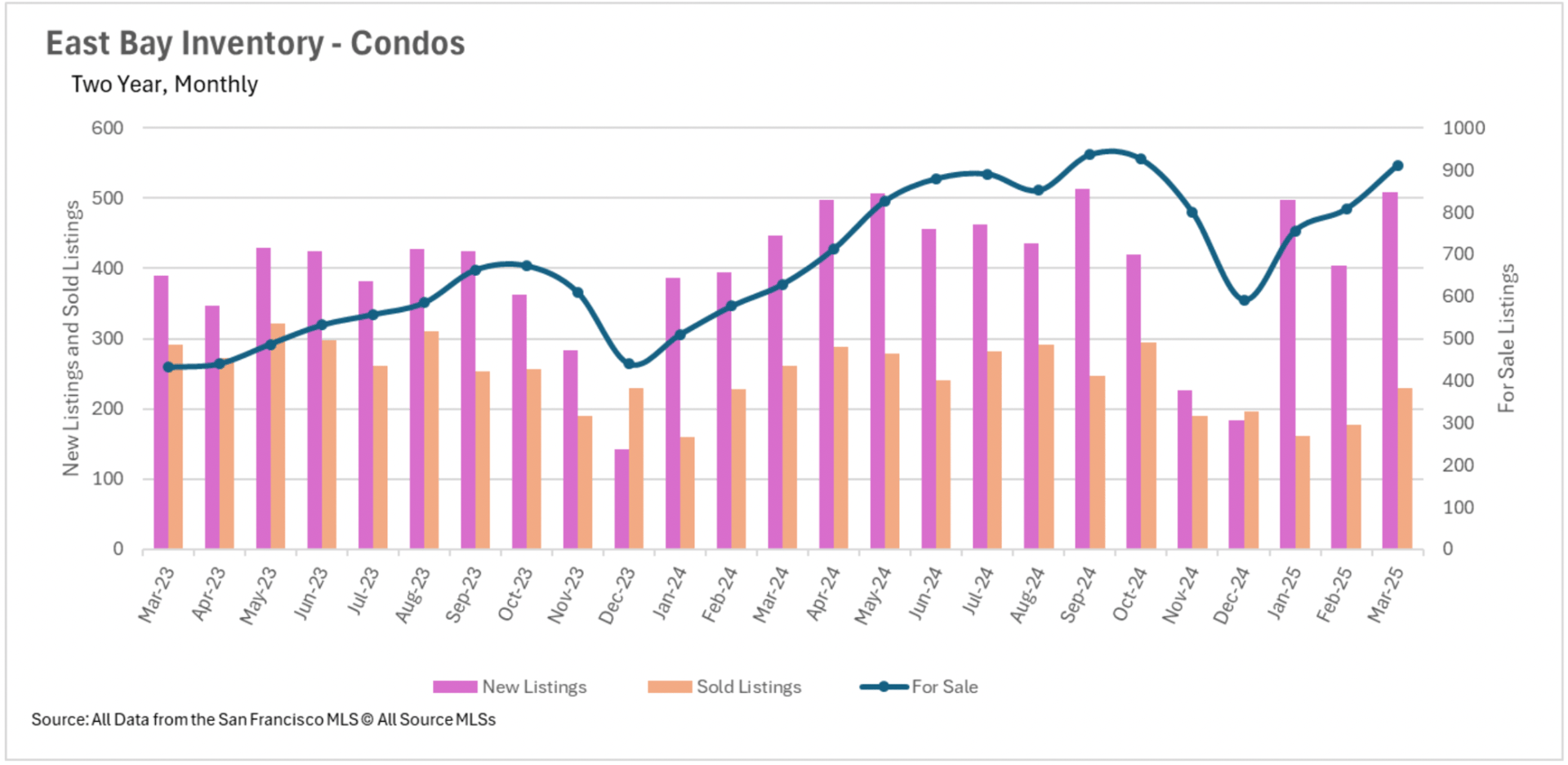

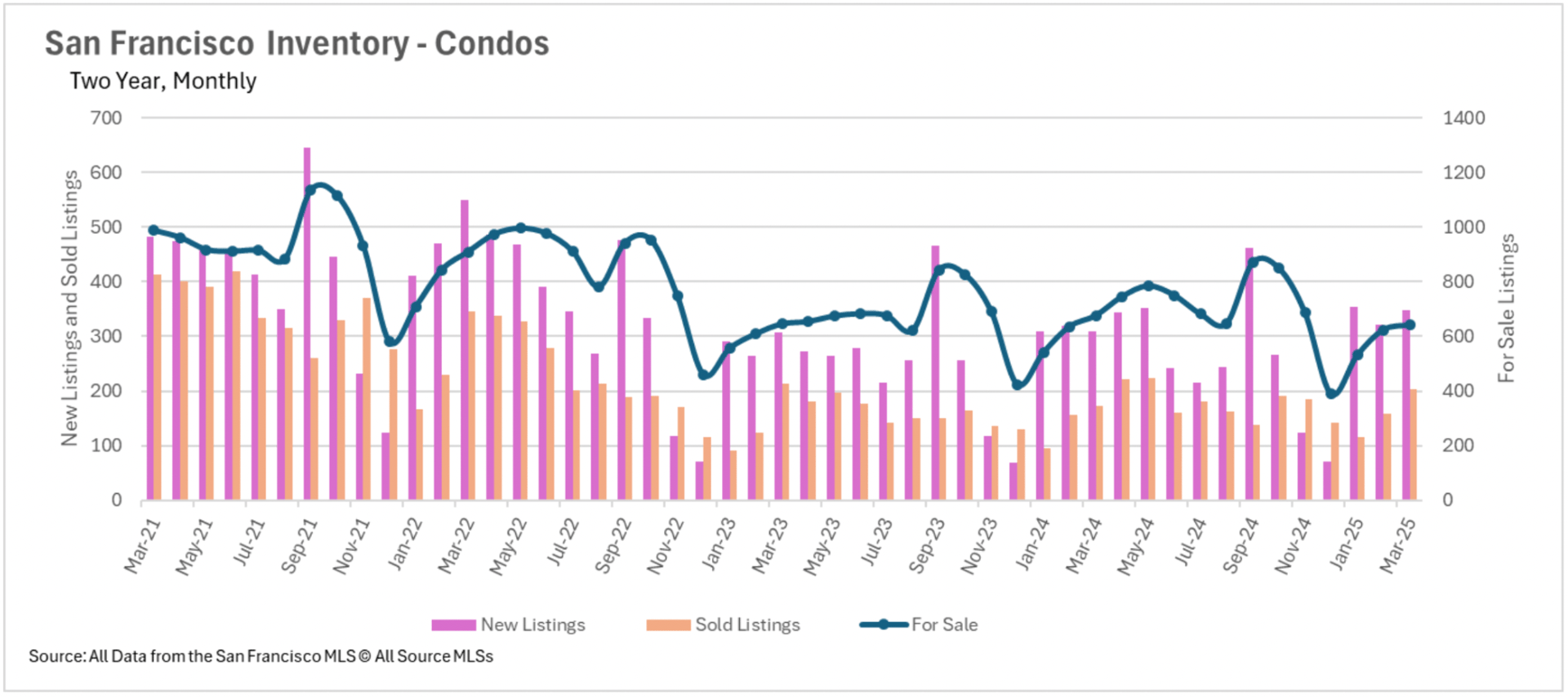

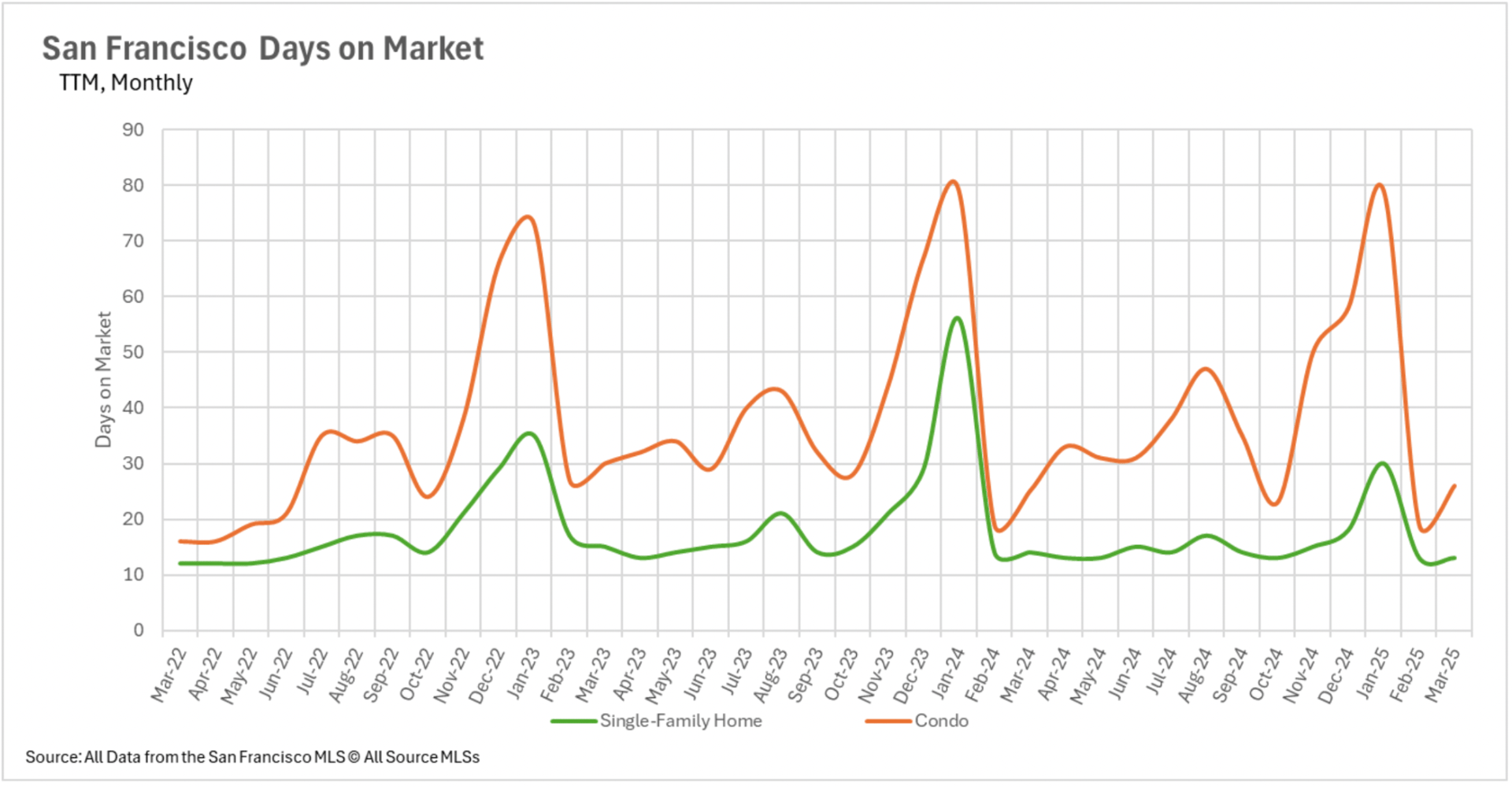

Conversely, East Bay markets have experienced cooling conditions, with Alameda County median prices declining 4.41% year-over-year and Contra Costa County dropping 7.44%, though recent month-over-month indicators show signs of stabilization. San Francisco's market exhibits a pronounced dichotomy – single-family residences have appreciated 6.63% over the past four years, while condominium values have contracted 12.52% during the same period, underscoring consumer preference for detached housing over shared structures.

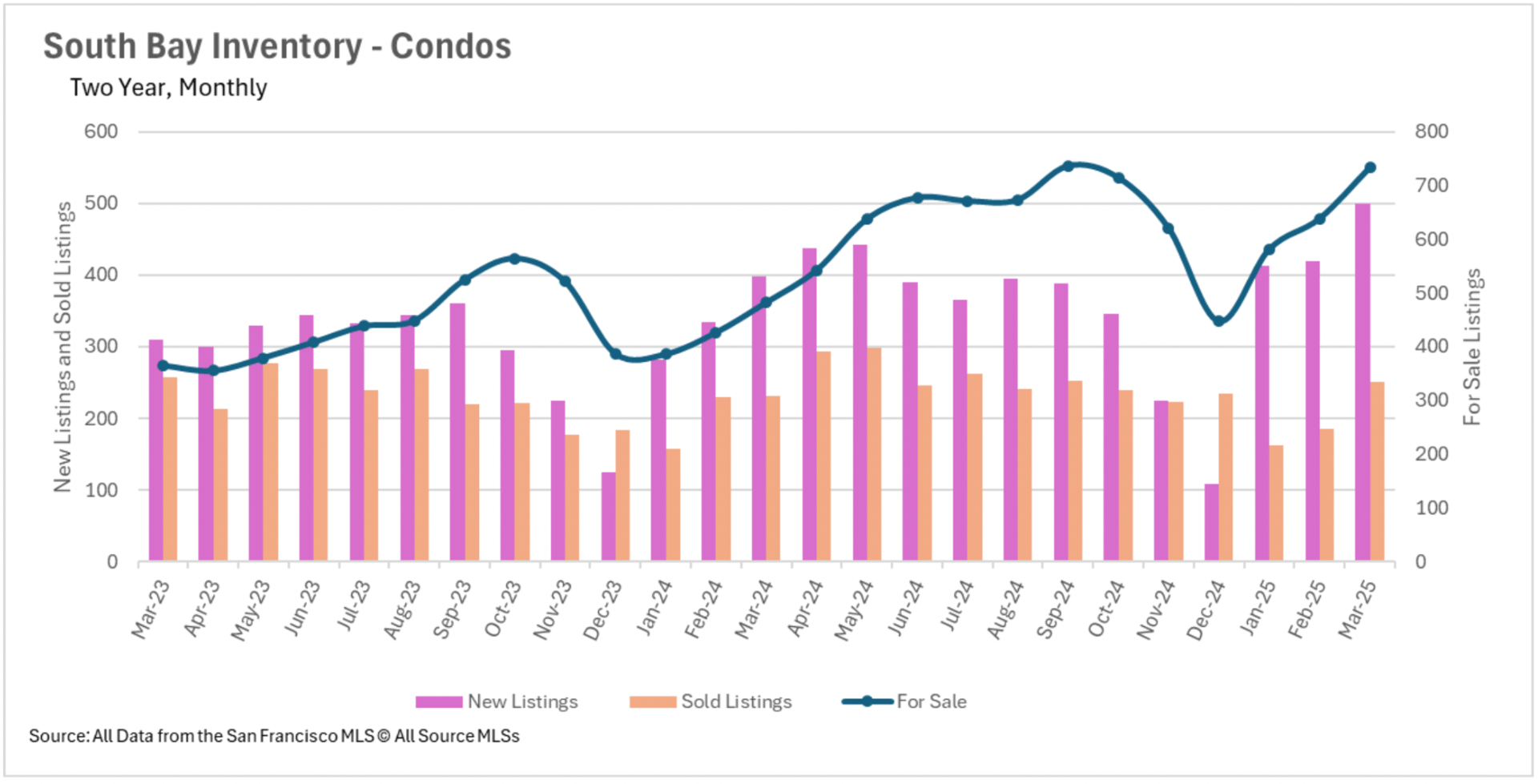

Inventory conditions across Bay Area markets reveal striking geographical differences. Silicon Valley is witnessing robust supply expansion, with single-family home inventory growing 40.05% in March, supported by a 23.83% year-over-year increase in new listings. Similarly, East Bay active listings surged 47.79% compared to last year, with March new listings climbing 16.78%.

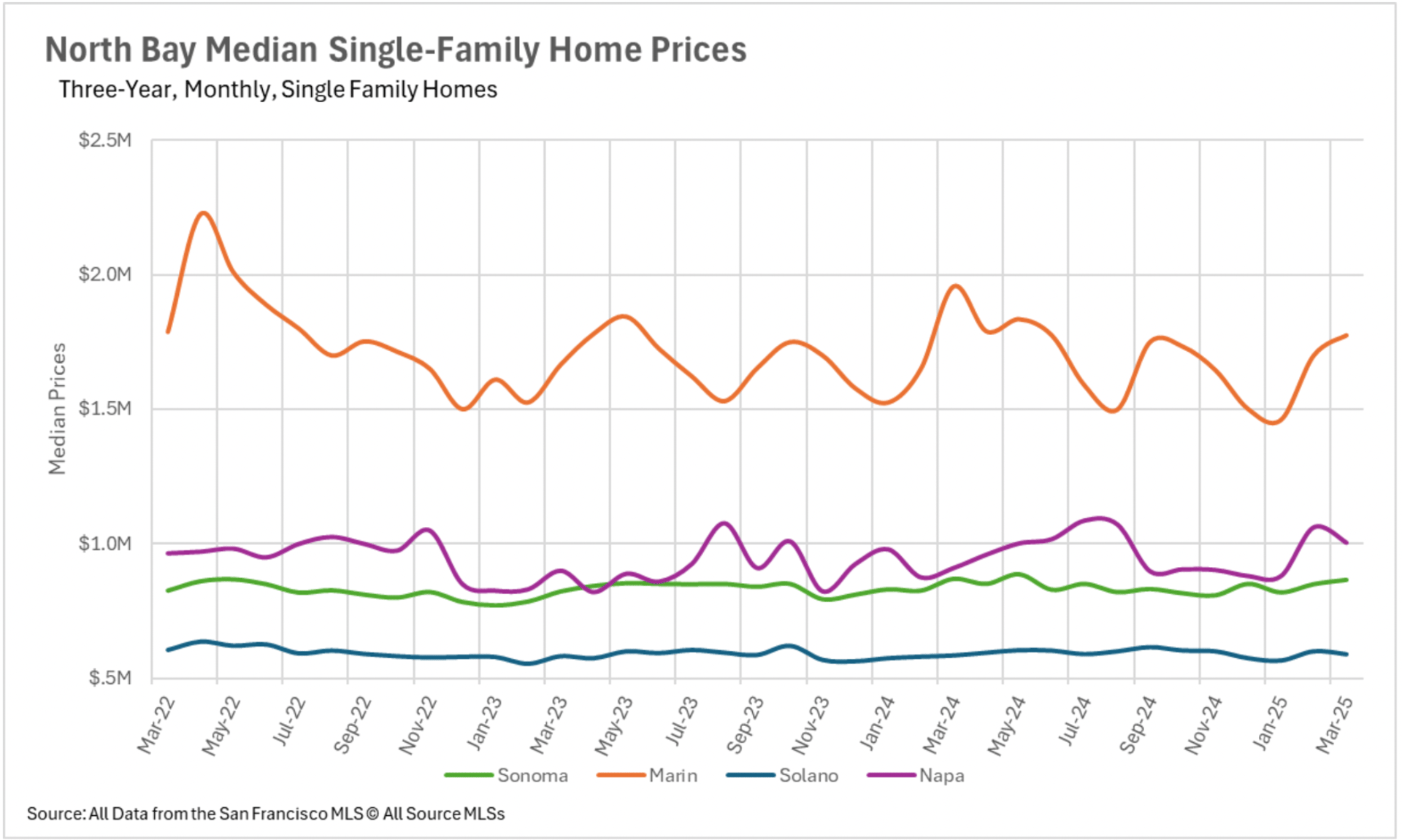

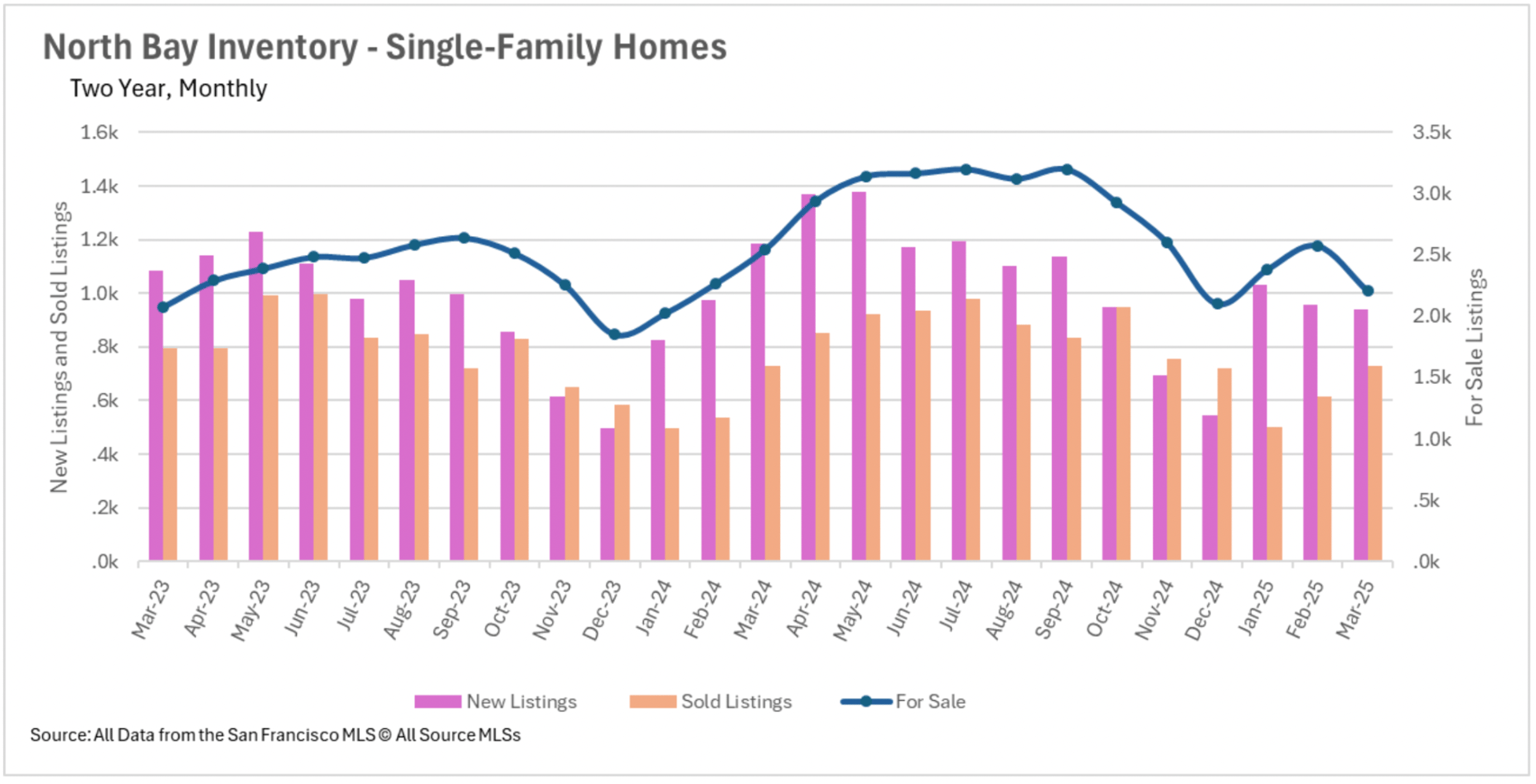

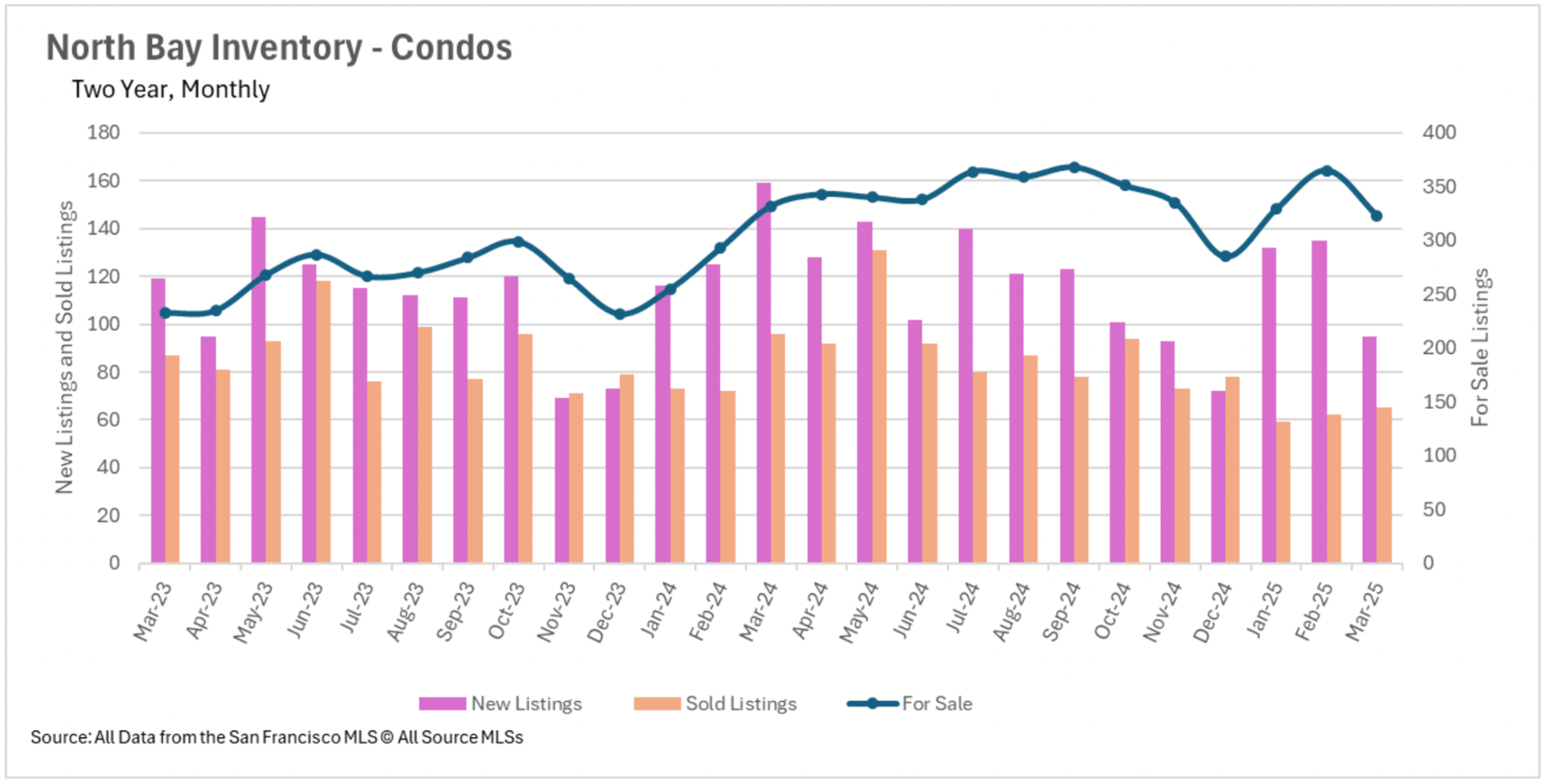

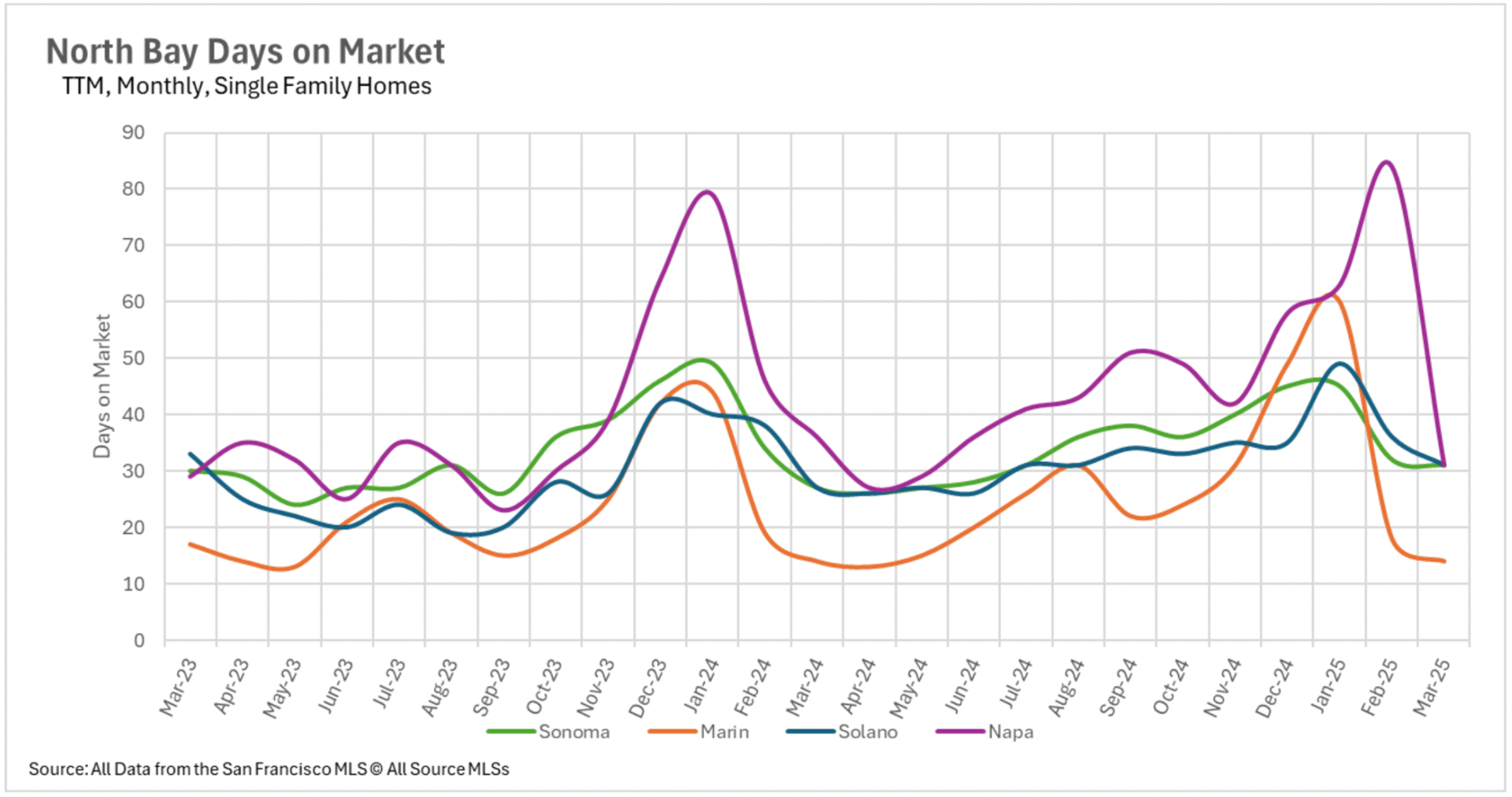

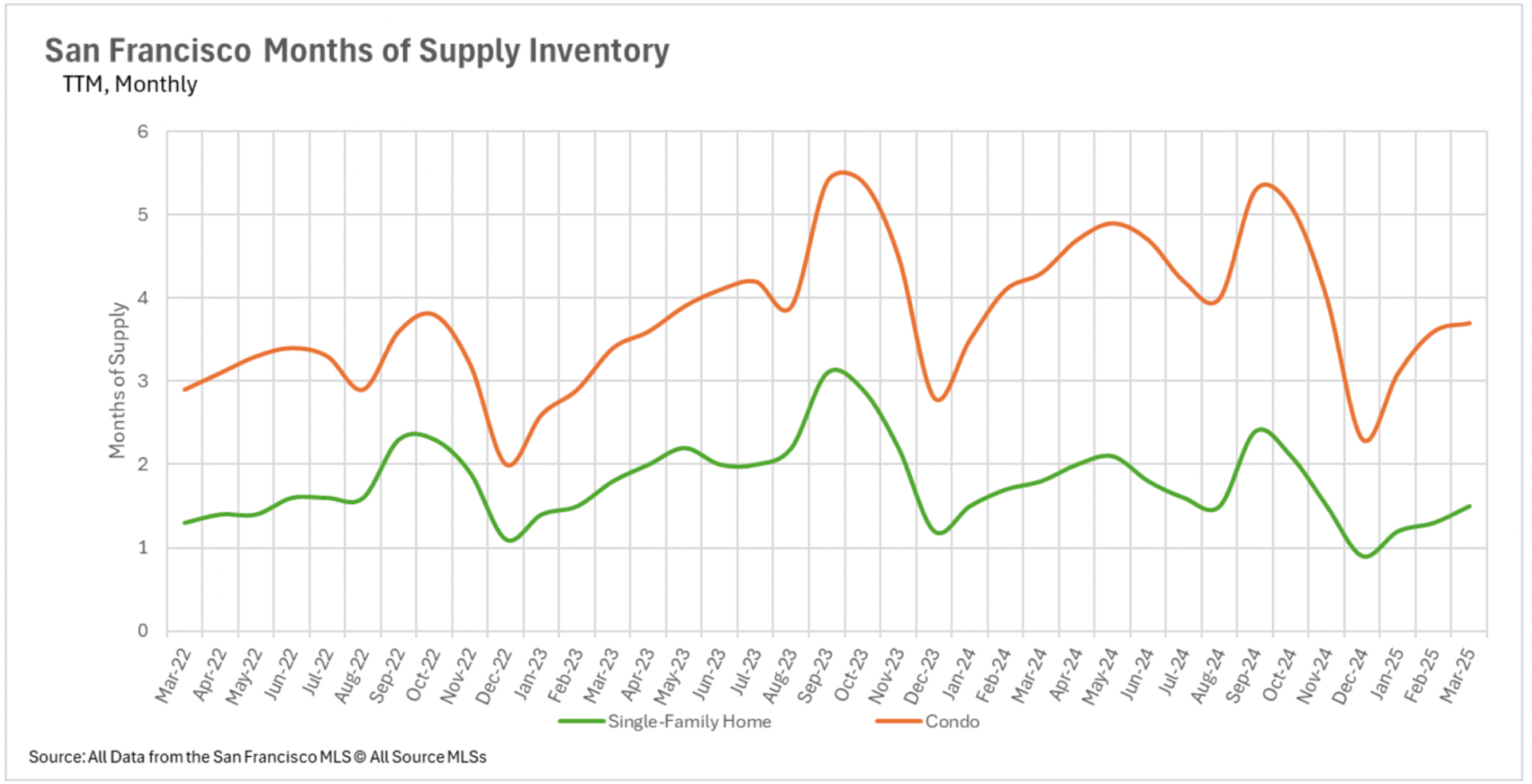

By stark contrast, San Francisco continues to grapple with persistent inventory constraints, particularly in the single-family segment where just 1.5 months of supply remains available. The North Bay region likewise faces supply challenges, recording a 14.28% month-over-month inventory decrease in March alongside 20.78% fewer new listings compared to March 2024. These contrasting supply conditions are driving distinctly different market dynamics across Bay Area regions.

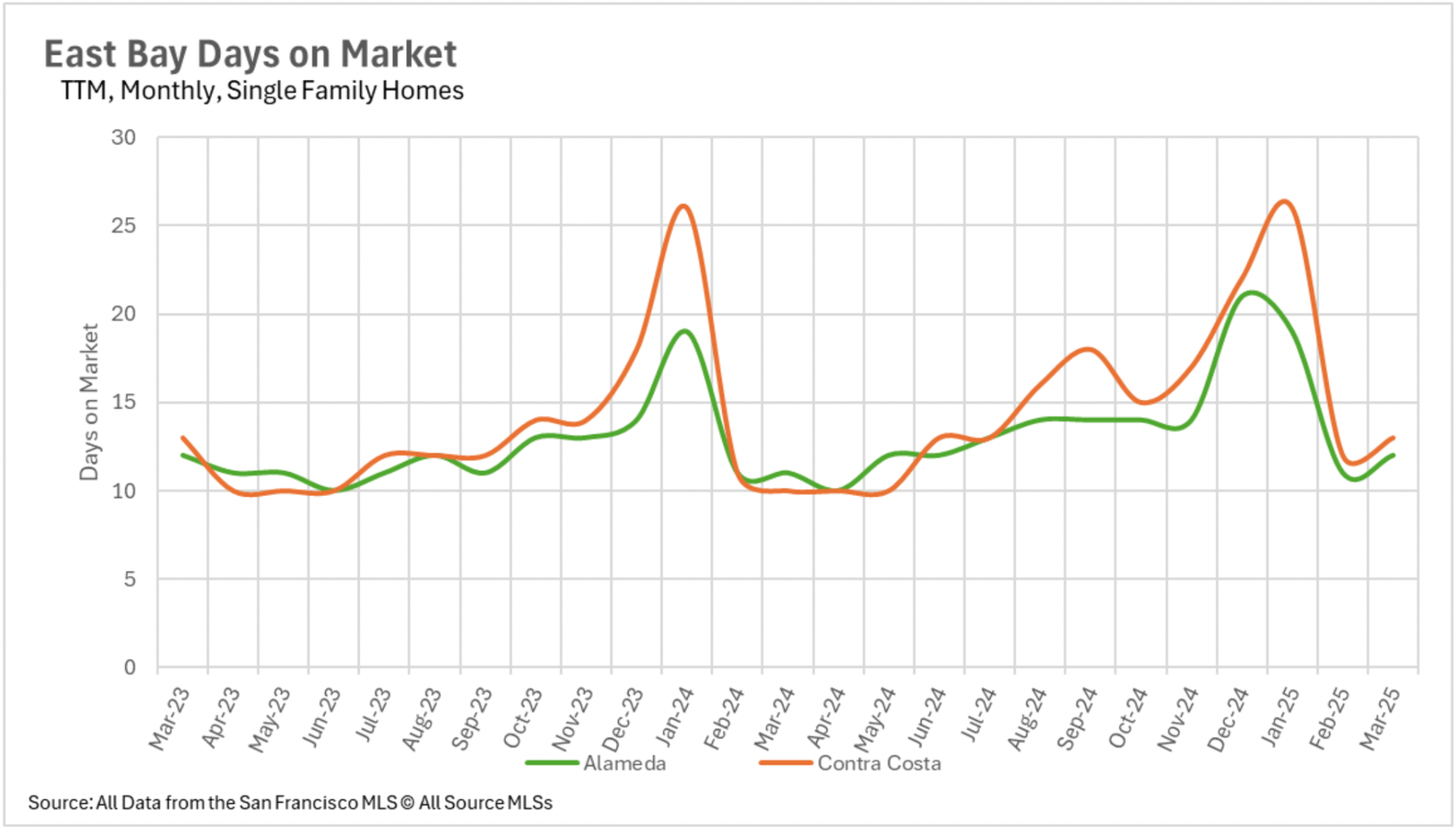

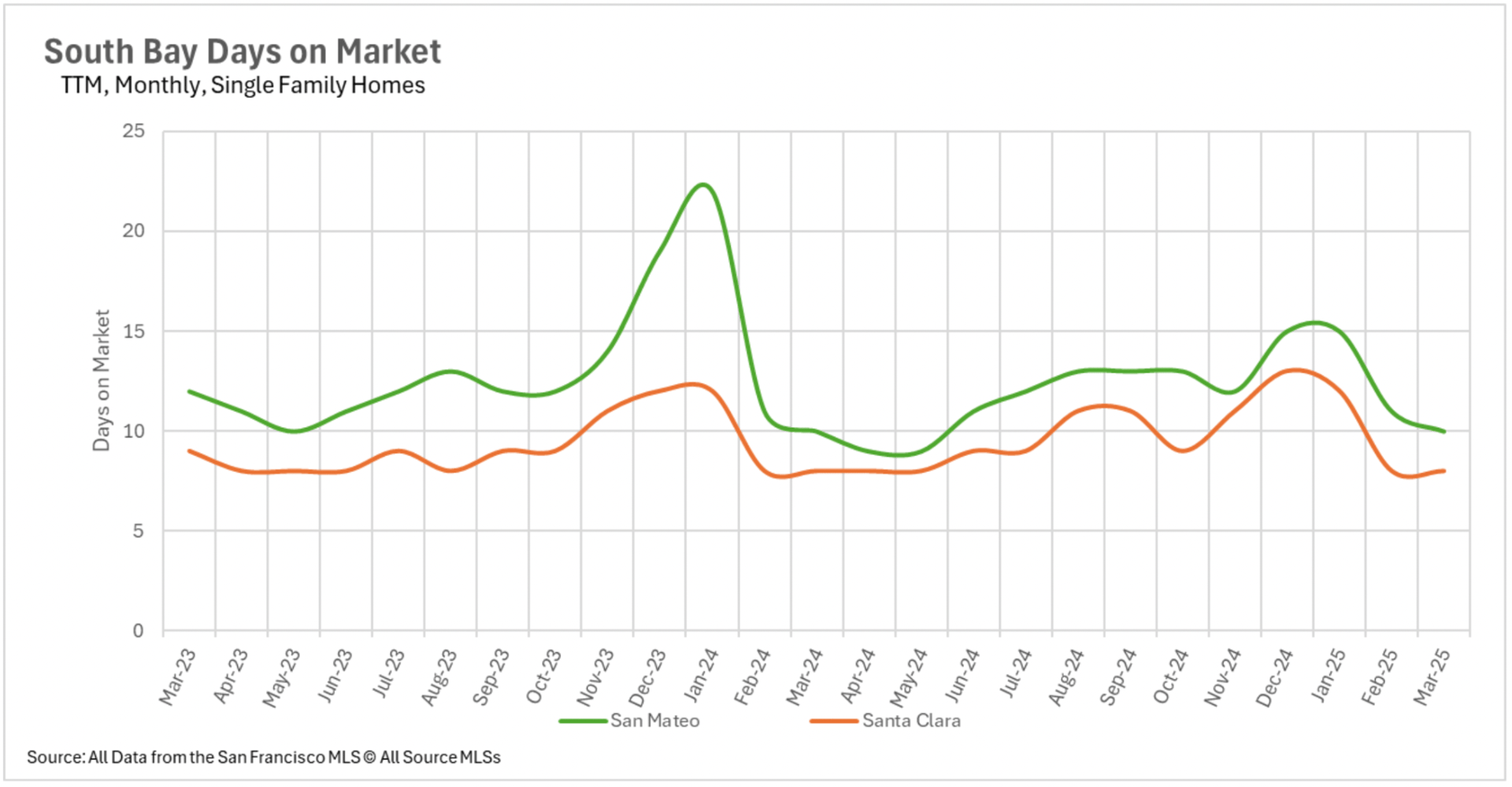

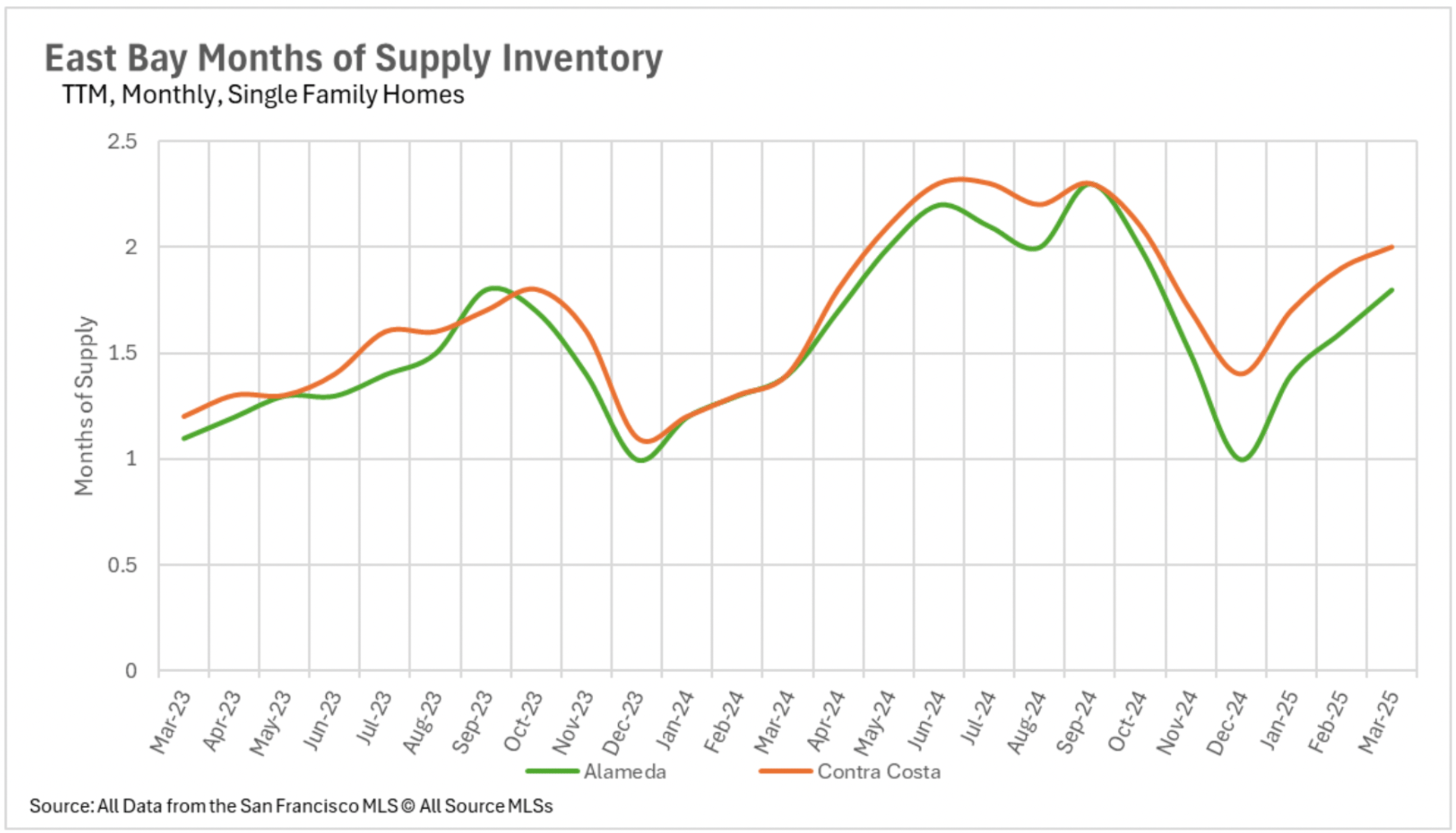

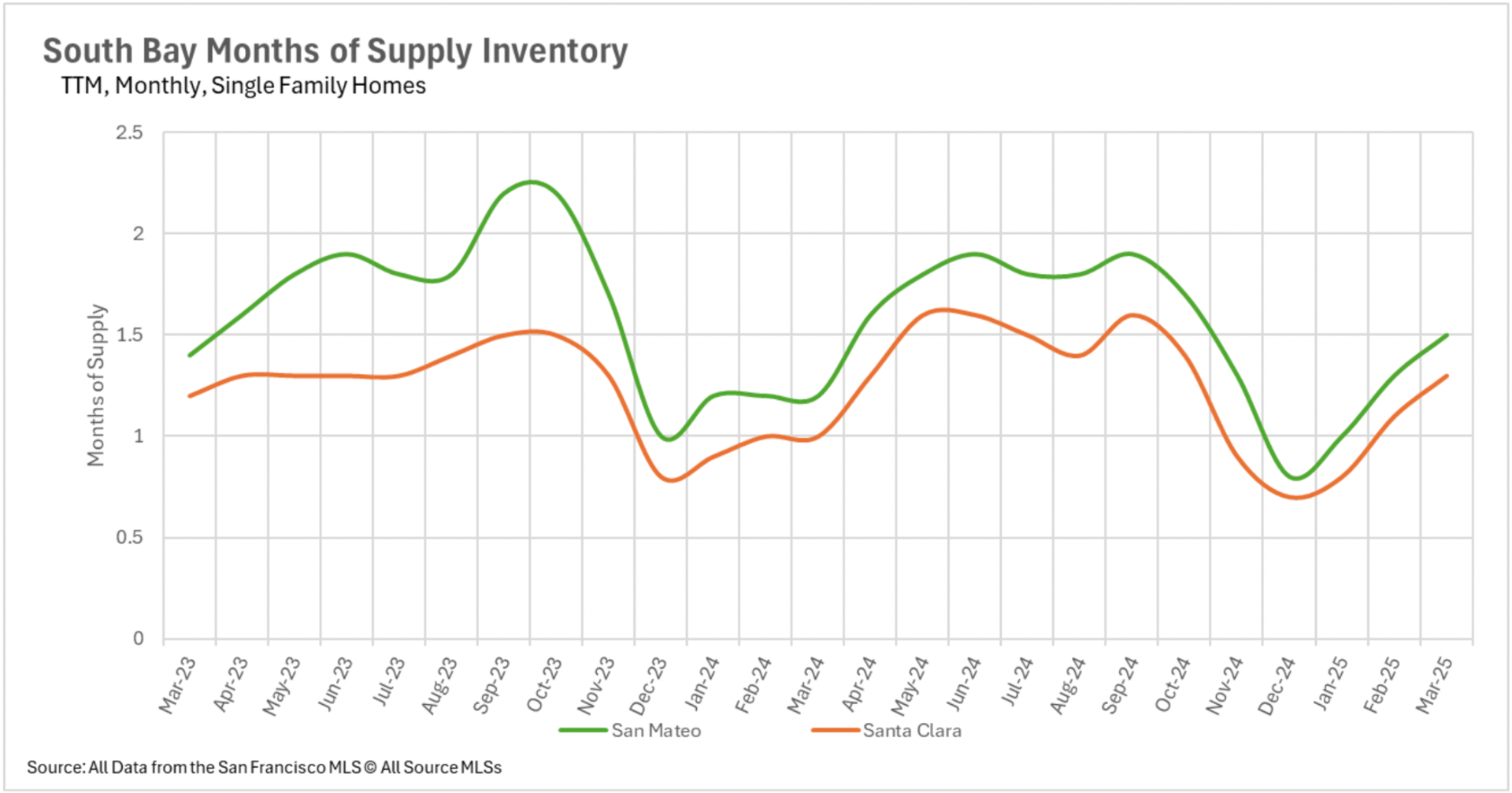

Perhaps the most pronounced variation across Bay Area submarkets lies in property marketing timeframes. Silicon Valley properties are transacting at exceptional velocity, with listings averaging just 8 days on market in Santa Clara, 10 days in San Mateo, and 16 days in Santa Cruz counties. East Bay markets also demonstrate relative efficiency with typical marketing periods of 12 days in Alameda County and 13 days in Contra Costa County, despite substantial year-over-year inventory increases.

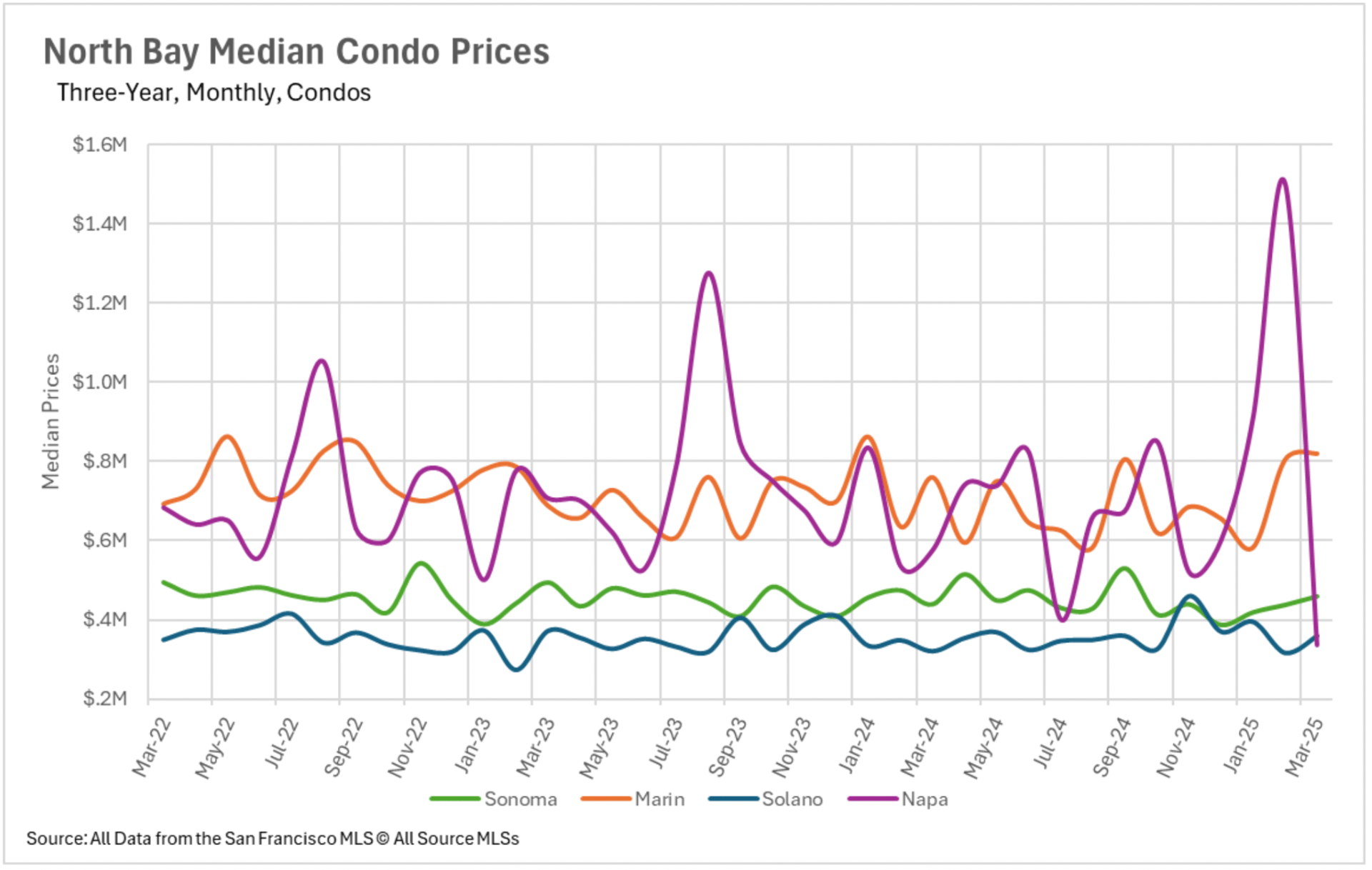

San Francisco's single-family segment continues to generate competitive bidding environments, with properties commanding 114.7% of original asking prices – a premium level not witnessed since before the Federal Reserve's rate increase cycle began in June 2022. This stands in marked contrast to North Bay conditions, where Sonoma and Solano county properties are experiencing approximately 15% extended marketing periods compared to the previous year.

The months of supply inventory (MSI) metric provides clear insight into market power dynamics, with California historically averaging around three months of supply. Lower figures suggest seller leverage, while higher numbers indicate buyer advantage.

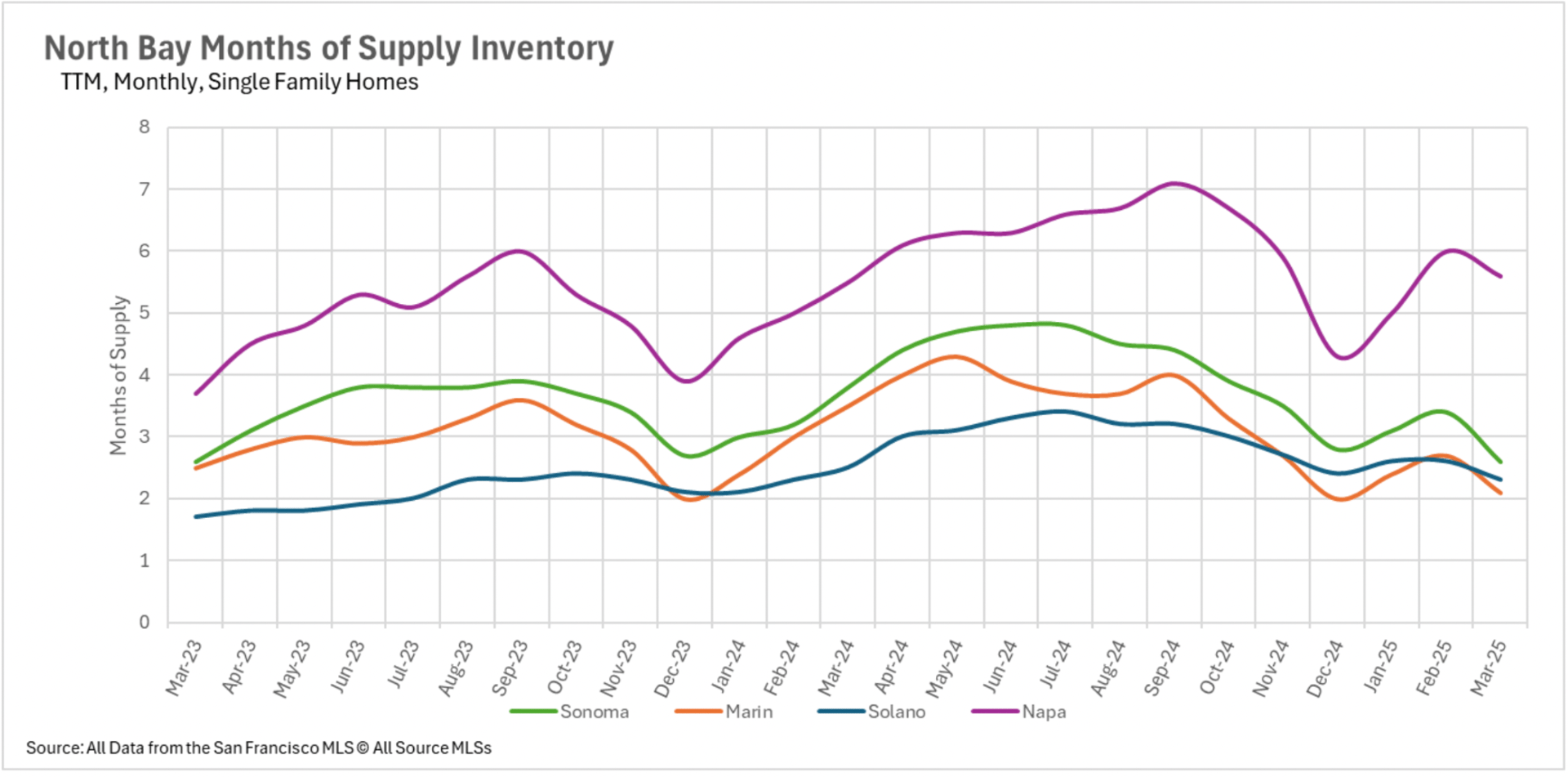

Throughout most Bay Area counties, single-family homes remain firmly in seller-favorable territory. Silicon Valley exhibits just 1.3 months in Santa Clara and 1.5 months in San Mateo (though Santa Cruz presents balanced conditions at precisely 3 months). East Bay markets similarly favor sellers with 1.8 months in Alameda County and 2 months in Contra Costa County. San Francisco maintains tight supply at just 1.5 months of single-family inventory, while most North Bay submarkets (with the exception of Napa County at 5.6 months) also favor sellers.

The condominium segment, however, presents a markedly different scenario, generally advantaging buyers with elevated inventory levels: 2.8 months in Santa Clara, 3.4 months in San Mateo, 4.4 months in Santa Cruz, 4.1 months in Alameda, 3.4 months in Contra Costa, and 3.7 months in San Francisco. This pronounced differentiation between single-family and condominium market conditions remains consistent throughout the Bay Area.

Thinking of buying or selling? Contact me today!

Stay up to date on the latest real estate trends.

August 15, 2025

July 15, 2025

July 12, 2025

June 28, 2025

June 3, 2025

May 17, 2025

May 17, 2025

April 17, 2025

April 4, 2025

You've got questions and we can't wait to answer them.